Sample Category Title

Unwinding Safe Haven Buying

Tuesday September 12: Five things the markets are talking about

The U.S dollar is finding it difficult to build on yesterday's strong start to the week as investor concerns about lackluster inflation stateside continues to linger ahead of key data this week.

The market will be keeping a close watch on Thursday's U.S consumer price data and Friday's U.S retail sales as it tries to gauge whether the U.S economy is strong enough to allow the Fed to hike rates a third time this year. The current CME FedWatch tool projects a +27% probability of one +25 bps rate hike in December.

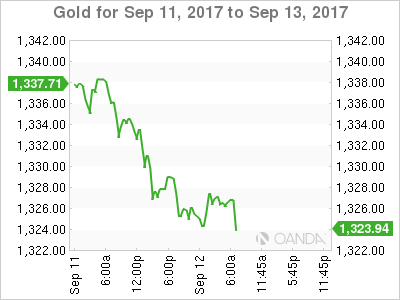

The overnight appetite for riskier assets is being supported by a lack of further confrontational developments from North Korea. Safe-haven assets such as U.S Treasuries and gold have managed to give back most of their recent gains.

Note: The UN Security Council approved a watered-down proposal to punish the nation for its latest missile and nuclear tests, omitting an oil embargo and a freeze of Kim Jong's personal assets.

1. Stocks hit record highs as Irma weakens

Global equities have climbed to record highs overnight as easing tensions over North Korea and signs that Hurricane Irma was causing less damage than feared.

In Japan, stocks climbed to their highest in a month with financials leading the way mirroring S&P's record close yesterday. The Nikkei rose +1.2%, the highest closing level since Aug. 8, while the broader Topix added +0.9%, with 32 of its 33 subsectors in positive territory.

In South Korea, the Kospi index rose +0.3%, while down-under, Australia's S&P/ASX 200 Index added +0.6%.

In Hong Kong, equities skip the bullish global move and hover atop of their two-year highs. The Hang Seng index inched up +0.1%, while the China Enterprises Index climbed +0.2%.

In China, shares inched higher with the blue-chip CSI300 index rallying +0.3%, while the Shanghai Composite Index added +0.1%.

In Europe, Germany's DAX Index climbed +0.4%, reaching its highest print in two-months on its sixth consecutive advance, while in the U.K, the FTSE 100 Index is under pressure after today's stronger inflation numbers (see below) and a stronger pound (£1.3250).

U.S equities are set to open in the black (+0.1%).

Note: Apple Inc. reveals its newest products later today.

Indices: Stoxx600 +0.5% at 381.5, FTSE -0.1% at 7405, DAX +0.5% at 12539, CAC-40 +0.5% at 5204, IBEX-35 +0.3% at 10355, FTSE MIB +0.2% at 22169, SMI +0.6% at 9034, S&P 500 Futures +0.1%

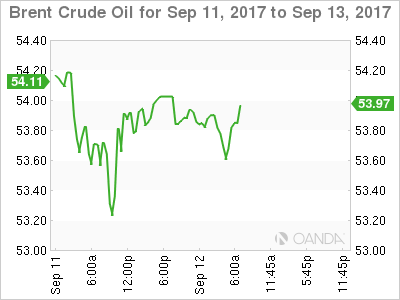

2. Oil steady as market assess U.S hurricane impact

Oil prices are steady as the market weighs up the dampening effect on demand of Hurricane Irma versus refinery restarts in the wake of Hurricane Harvey that should lead to more crude oil processing.

Brent crude futures are down -4c, or -0.07% at +$53.80 per barrel, while U.S West Texas Intermediate (WTI) crude is down -3c, or -0.06% at +$48.04 a barrel.

U.S crude inventories likely rose last week following the hurricane impact, while refined product stockpiles are forecasted to have declined.

The API and the EIA data last week are expected to show that crude stocks likely rose in the week ended Sept. 8.

Note: The API is due to release its data for last week at 4:30 pm EDT today and the EIA report is scheduled at 10:30 am EDT Wednesday.

Note: OPEC Secretary General Barkindo reiterated the view that the oil market rebalances remains in progress with output growth slightly decelerating – OECD commercial oil stocks were +195m barrels above the five-year average in July.

Ahead of the U.S open, gold has hit its lowest price in more than a week as receding concerns over N. Korea's nuclear ambitions and the impact of Hurricane Irma supports further gains in equities, softening demand for the ‘yellow' metal as a haven from risk. A steadier tone to the dollar is managing to take some pressure off the metal. Spot gold is trading atop of its two week lows at +$1,322.85.

3. Sovereign yields back up

Hurricanes Harvey and Irma are likely to trigger near-term weakness in U.S economic data leading to a challenge for the Fed regarding the appropriate stance of monetary policy.

The market expects the Fed to proceed with caution and this likely means postponement of any rate hike in December – the odds for a December rate hike have now fallen to a +27% probability.

Risk on trading has sovereign yields backing up a tad overnight. The yield on 10-year Treasuries gained +1 bps to +2.14%, the highest in more than a week.

In Germany, the 10-year Bund yield gained +1 bps to +0.35%, while in the U.K 10-year Gilt yield advanced +2 bps to +1.045% supported by this morning's inflation data ahead of Thursday's Bank of England (BoE) monetary policy decision.

In Japan, 10-year JGB's bond yield rallied to a three-week high, backing up +3 bps to +0.025%.

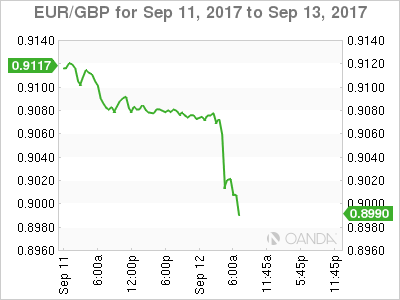

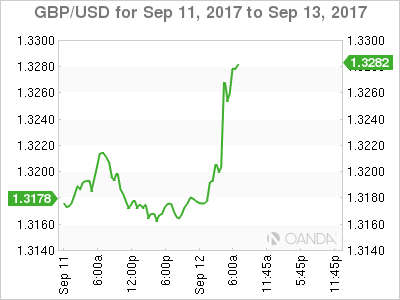

4. Sterling's stellar performance

With risk-on sentiment remaining intact for a second consecutive day as concerns over Hurricane Irma and North Korea subsides has U.S Treasury yields backing up and tentatively supporting the U.S dollar, but is it sustainable?

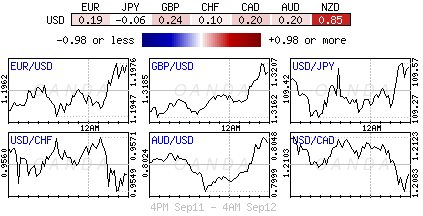

Ahead of the open stateside, USD/JPY is higher by +0.3% at ¥109.70, a three week high while EUR/USD is steady at €1.1965.

The standout currency is GBP – the pound (£1.3262) has rallied aggressively after U.K consumer inflation data this morning came in better than expected (see below). EUR/GBP is down -0.6% at €0.9021.

A stronger-than-expected inflation report would be something that the BoE would have to consider at Thursday monetary policy meeting. The data may possibly bring more members in support of a raise in interest rates.

However, inflation is thought to be rising due to a weaker pound, not due to fundamentals. The pound has also found support from the U.K Parliament yesterday voting against opposition Labor party's attempt to block E.U withdrawal bill, effectively passing its first parliamentary hurdle.

5. UK Inflation Speeds Up in August

Data this morning showed that U.K annual inflation rose to +2.9% (+2.8% e) in August, driven higher by the rising price of clothing and petrol.

Other data from the U.K's Office for National Statistics also revealed a rise in the producer price index – +1.6% (+1.2% e) in August, supported by the higher price of fuel – the first gain in six-months.

Increasing concerns about the squeeze on the cost of living will make Thursday's Bank of England (BoE) interest rate decision a tad more interesting.

Record Highs Expected As North Korea Fears Subside

- Should we be more concerned about North Korea retaliation to UN sanctions?

- UK inflation spikes again ahead of BoE meeting;

- US labor market should be primed for wage growth.

US indices are poised to open in, or close to, record territory on Tuesday as North Korean fears continue to subside.

Once again we find ourselves in a scenario in which no news is good news and while underlying risks remain, the longer we go without another nuclear or missile test, the more positive investors will become. The only problem with this is that, with the UN having just agreed on new sanctions against North Korea – spearheaded by the US – I wonder how long we will have to wait for an act of provocation in response.

With that in mind, I expect an element of caution to remain, at least until after the weekend at which point investors may decide that such a response isn't imminent. Should we get a response, then I would expect to see a similar response as we've seen in recent weeks, with traders once again favouring safe havens such as Gold, which despite having come off its highs, currently remains elevated.

In the meantime, attention will turn back to the fundamentals and this week, that is focused primarily around the UK, with data releases earlier in the week followed by the Bank of England monetary policy meeting on Thursday. Today we got the first of the releases – CPI and core CPI data – which showed prices in the UK rising at a faster pace than expected and a much faster pace than the BoE targets.

This has created a dilemma in the past for the BoE – as demonstrated by the lack of consensus in the voting in recent months – with policy makers being torn between raising interest rates in order to bring inflation back towards target and protecting the economy and hoping it naturally finds its way back to target. The latter of these strikes me as the most sensible, with price rises having largely been driven by the depreciation of the pound, the bulk of which should now be behind us. Clearly though, some policy makers are not convinced this is the case. With labor market data still to come before Thursday's monetary policy decision, it will certainly be an interesting week for the UK economy and the pound, which rallied after the inflation data on the expectation that the it adds to the case for a hike.

The bulk of the US data isn't due until later in the week, at which point we'll get inflation and retail sales figures, both of which will closely monitored. Today's we'll get JOLTS job openings data for July which is expected to have come slightly off its June high but remain just below 6 million, a sign that the labour market remains extremely healthy and primed for stronger wage growth which has so far proved elusive.

WTI Oil Futures Risk Seeing More Downside

WTI oil futures have been trading around the pivotal 47- level and keeping within a range between 45.40 and 50.40 since July.

Trading during the last few sessions has been very choppy. The recent rally from the 45-area to the September 6 high of 49.39 fizzled out after the market became overbought as was indicated by the RSI rising above 70 on the 4-hour chart. A subsequent drop found strong support at 47 from where prices bounced off.

Near-term risk is tilted to the downside based on bearish signals from technical indicators. The 20-period moving average is pointing down while momentum oscillators RSI and MACD are now in their respective bearish territory.

Should key support at 47 breaks down, this would increase downside pressure for a move towards the August 31 low of 45.56. A further extension lower would see WTI push outside the broader range and begin to shift out of the neutral phase to a more bearish one and turn the focus to the 42-level.

The odds for a push higher from current levels in the near term have diminished based on the reversal of the 20-period SMA and of the momentum oscillators. A rise above yesterday’s high of 48.24 would signal more upside potential with scope to reach the September 6 high of 49.39. From here, the key 50 level comes into view.

Only a move above the August 1 high of 50.40 would push prices out of the 6-week range. Then the short-term trend would shift to bullish. For now, the near-term bias is bearish while the medium-term is neutral.

Technical Outlook: Spot Gold – Bears May Extend Towards $1317 Support While 10SMA Caps

Spot Gold remains in red on Tuesday and met its target and strong support at $1323 (Fibo 38.2% of $1267/$1357 upleg), where temporary footstep was found. Near-term action is in narrow consolidation above $1323 handle and holds below broken 10SMA ($1331), maintaining bearish near-term bias. Relief from North Korea/Hurricane Irma's impact concerns reduced safe-haven demand and keep gold price under pressure. Bears may extend towards next pivotal support at $1317 (Fibo 38.2% of $1251/$1357 upleg) loss of which would expose another strong support at $1304 (daily Kijun-sen). Scenario is expected to remain in play while the price holds below 10SMA, otherwise, strong downside pressure would ease on break and close above 10 SMA.

Res: 1329, 1331, 1336, 1340

Sup: 1323, 1317, 1312, 1304

PBOC Removes Capital Control. Yet, Renminbi Internationalization Remains Distant

USDCNY continues to recover after the pair slumped to the lowest level since December 2015 last Friday. The rebound, long-awaited as the broad-based USD weakness has caused the pair to decline over the past 4 months, is facilitated by PBOC’s announcement to remove the requirement for banks to hold the equivalent of 20% of clients' FX forward positions as reserve for a year at 0% interest. For more than a decade, China has been implementing reforms in its currency, with the ultimate goal of achieving a floating exchange rate regime and convertibility for renminbi – a movement widely described as renminbi internationalization. However, this report seeks to explain that the government has only been moving back and forth, without making significant progress in transforming renminbi into a market-oriented exchange rate.

'811-Reform'

On August 11, 2015, PBOC abruptly devaluated renminbi by -2%. On trading, CNY plunged -1.8% against USD, the biggest one-day decline since 1994. Besides, PBOC announced a new renminbi fixing mechanism, suggesting that the components used in setting that daily fixing rate include previous’ day’s close, FX demand and supply conditions and movement of major currencies. The market believed that the new mechanism had paved the way for renminibi to join IMF’s special drawing right (SDR). PBOC explained that it had to devaluate the currency as the midpoint had been diverging from the market rate for some time. However, we believe it was a means to rescue the slowdown in economic growth.

While inclusions of demand/supply conditions, as movement of major currencies in its calculation marked an effort to make renminbi more market-oriented, the surprising devaluation had dampened market confidence on the currency and evidenced that the currency remained under manipulation to the authority despite the rhetoric of market-orientation.

Panic selling of renminbi following the so-called '811-reform' triggered the government adopt a series of capital control measures, including the abovementioned 20% FX reserve ratio effective from October 2015. Other capital control measures include strengthening supervision of foreign exchange purchases by foreign-held non-resident accounts (NRA), monitoring firms’ foreign exchange buying and tightening supervision of bank clients’ foreign exchange deals.

FX Reserve

Another prominent feature of China’s defense of renminibi depreciation is the massive selloff of FX reserve. US$630B of FX reserve was evaporated from Aug-2015 to Dec-2016. During the period, renminbi deprecated -10% against US dollar. PBOC aggressive selling sent FX reserve below US$ 3 trillion in January this year. There is no coincidence for the consecutive monthly rise in FX reserve and USDCNY’s decline since February.

CEFTS index

Remaining under pressure for the rest of 2015 and in 2016, renminbi’s weakness had been a result of concerns over further government devaluation in light of soft economic growth and a strong US dollar amidst rising expectations of Fed funds rate hike and reflation trade upon Donald Trump’s victory as the US president. Renminbi depreciation despite stringent capital control measures led to the 're-introduction' of the CEFTS index in December 2016. Attempting to shift the market’s focus from renminbi vs US dollar to renminbi vs a basket of currencies, the government expanded the number of currencies in the CFETS basket to 24 from 13 in January 2017.

Counter-Cyclical Factor

Less than four months ago, the government indicated that it considered adding a 'counter-cyclical factor' in its fixing mechanism. As such, components in the daily fixing calculation would include previous day’s close+ changes in renminbi’s value against a basket of currencies+ counter cyclical factor. The authority explained that the new component would help prevent renminbi from being excessively affected by external volatility. Yet, it revealed no details about how the countercyclical factor would be computed or its weight in the new fixing mechanism. Introduction of the counter-cyclical factor evidenced that the government has chosen to control the currency movement, instead of increasing its transparency and taking a step forward in currency internationalization.

Indeed, we doubt whether the Chinese government is committed to achieving a floating exchange rate regime and convertibility for renminbi. Over the past decade, it has been moving one step forward and then several steps backward in its internationalization process. We are not hopeful that renminbi would become a global currency in the next decade, let alone a major reserve currency.

Technical Outlook: GBPJPY – Extended Bullish Acceleration Faced Strong Headwinds At Daily Cloud Top

The pair extends strong rally into second straight day, as fading concerns over North Korea / Hurricane Irma’s impact drastically reduced safe-haven demand and pound got additionally inflated by upbeat UK inflation numbers.

The cross dented target at 145.70 (daily cloud top) on today’s strong acceleration higher and may extend recovery rally on sustained break above the cloud.

The price is currently riding on the wave C (from 141.18 trough) of five-wave cycle from 139.30 (24 Aug low) which could extend towards its Fibo138.2% Expansion at 146.18 and 146.80 (03 Aug lower top) in extension.

Daily studies turned into full bullish setup and are supportive for further advance.

However, overbought conditions suggest corrective action in the near term (no signal yet), as daily cloud is narrowing and will twist next week that may also attract for stronger pullback.

Initial support lies at 114.79 (broken FE 100.0%), followed by session low /55SMA at 143.90 and rising daily Tenkan-sen at 143.45.

Key near-term support lies at 143.25 (daily cloud base/Fibo 38.2% of 139.30/145.71 ascend).

Res: 145.70, 146.18, 146.80, 147.05

Sup: 144.79, 144.19, 143.90, 143.45

CRUDE OIL Sharp Decline

Crude oil has strongly declined after the commodity monitored the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance can be found at 50.43 (31/07/2017). Expected to show continued short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Profit-Taking

Silver has failed to reach strong resistance at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in an uptrend channel. Expected to show another leg higher.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

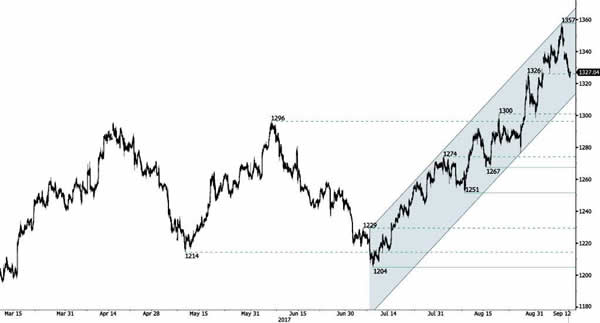

GOLD Consolidating Within Uptrend Channel

Gold has seen increased buying interest, clearing rising trend-line. Hourly support is given at a distance 1326 (gap low). Key resistance is located at 1375 (06/07/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Renewed Buying Pressures

Bitcoin's buying interest is getting stronger again.Technical picture remain bullish as long as key support hold. Monitor the key support at 4078. Strong support lies very far at 3599 (22/08/2017 low). Key resistance can be located at 4921 (01/09/2017 high).

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.