Sample Category Title

USD/JPY Further Increase Expected

The USD/JPY rallied aggressively in the yesterday's trading session and invalidated the Friday's breakdown below the 108.12 static support. Is still trapped within the extended sideways movement and should approach and reach the third warning line (WL3) of the major descending pitchfork. A valid breakout above the WL3 will confirm an increase towards the 23.6% retracement level.

GBP/JPY Still In Range

Price has found strong support at the first warning line (WL1) of the major ascending pitchfork and now has turned to the upside again. Has managed to break above the red uptrend line, signaling that the bulls are very strong. GBP/JPY continues to move in range on the short term, technically it should approach and reach the upside line of the extended sideways movement after the failure to approach and reach the downside line of this pattern.

GBP/USD Near Crucial Resistance

The GBP/USD changed little in the start of the week, but most likely we'll have a significant move in the upcoming hours as the United Kingdom is to release the inflation data. Price has found temporary resistance on Friday and now could drop a little if the UK's data will disappoint later. The USDX increased in the yesterday's session and have forced the GBP/USD to decrease a little.

The dollar needs a strong support from the United States economy to be able to dominate the currency market again. The USD's rebound is natural only because is too oversold to drop further without a minor bounce back.

The UK's CPI is expected to increase by 2.8% in August and could beat the 2.6% in July, while the Core CPi should increase by 2.5%, exceeding the 2.4% in the former reading period.

Price moves upwards within the ascending channel, so the perspective remains bullish on the Daily chart. GBP/USD has found temporary resistance at the first warning line (wl1) of the minor ascending pitchfork and much below the 1.3266 previous high. The GBP/USD will be driven by the fundamental factors in the upcoming hours, so the direction is still uncertain on the short term.

A failure to climb above the 1.3266 previous high will signal another leg lower. Technically should reach the upside line of the ascending channel and even to jump above it after the failure to approach and retest the downside line of this pattern.

Dollar Bounces Amid Improved Market Sentiment

The Dollar Index Registers a 'U-shaped' Rebound. The greenback managed to catch a decent bounce as worries over North Korea and Hurricane Irma receded while U.S. officials tried to keep the spotlight on tax reform.

Dollar Pulls Away from 2-1/2-yr Low Vs Euro as Risk Sentiment Improves. The greenback held to large gains on Tuesday following a sharp rebound against the euro. The euro was little changed at $1.1962 after shedding 0.7 percent overnight. The common currency had reached $1.2092, its highest since January 2015, on Friday when the dollar suffered a broad retreat.

Dollar Sharply Rebounds Against Yen. The yen slumped back in the losers' bench as risk-on vibes were in play and traders cut down on their lower-yielding holdings. The dollar was steady at 109.345 yen after rallying 1.4 percent overnight, its biggest one-day surge since mid-January. It had slumped to a 10-month low of 107.320 yen on Friday, when Hurricane Irma threatened Florida and as financial markets braced for North Korea's founding day on Sept. 9.

Franc Stays Flat After Rally. The Swiss franc, often sought in times of global risk aversion along with the yen, was flat at 0.9558 per dollar after its rally to a two-year high of 0.9421 on Friday.

Oil Positively-Correlated Canadian Scored Strong Gains. The Loonie is already being supported by hawkish BOC expectations but it got another kick higher from expectations of another OPEC deal extension.

Pound Gains Vs Euro Ahead of Thursday's BoE Policy Meeting. Sterling fared better against the euro, aided by speculation that the Bank of England may sound more hawkish on interest rates in defense of the currency at its policy meeting on Thursday. The pound hovered close to a one-month high of 90.75 pence per euro set overnight.

The Australian Dollar Edges Down After Its Rally on Friday. The Australian dollar was 0.05 percent lower at $0.802 , extending its retreat from a two-year peak of $0.8125 scaled on Friday.

Oil Rallies on Potential OPEC Deal Extension. Crude oil is also in the green so far, thanks to talks of an extension on the OPEC deal extension. Recall that the oil cartel already agreed to keep a cap on production six months longer than their original end-date to March 2018 in an effort to ensure that the commodity price stays supported.

Traders Unwound Their Safe-Haven Holdings. Safe havens have been lackluster these past two days as capital returned back to risky assets. Precious metals returned some of their recent gains. The gold price tumbled 1.5% to the US$1,326 area.

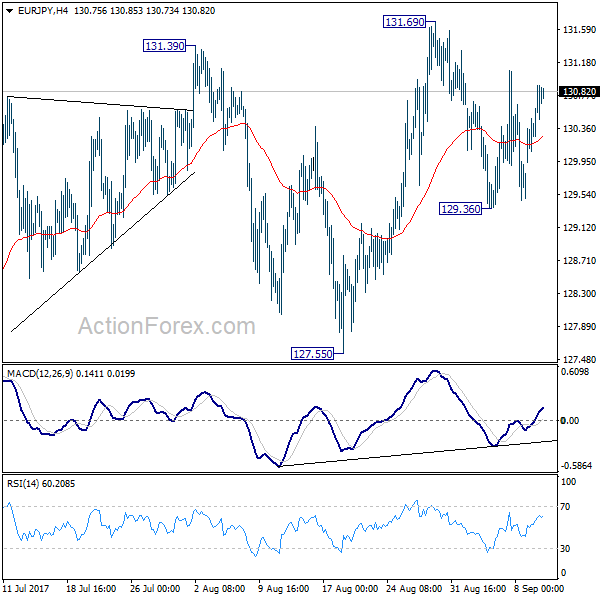

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.15; (P) 130.52; (R1) 131.10; More...

No change in EUR/JPY's outlook and intraday bias stays neutral. On the downside, break of 129.36 will turn bias to the downside for 127.55 support first. Firm break there will indicate near term reversal and deeper fall would be seen back to 122.39/125.80 support zone. In any case, we'd expect more corrective trading with risk of another fall, as long as 131.69 holds. But firm break of 131.69 will extend the medium term rise to 134.20 fibonacci level next.

In the bigger picture, current rise from 109.03 is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). as long as 124.08 resistance turned support holds, further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.

European Open Briefing: AUD/USD Slipped Lower During Sydney This Morning

Global Markets:

- Asian stock markets: Nikkei rose 1.12% %, Shanghai Composite gained 0.10 %, Hang Seng fell 0.08 %, ASX 200 climbed 0.60 %

- Commodities: Gold at $1328.77 (-0.52 %), Silver at $17.81 (-0.47 %), WTI Oil at $48.01 (-0.12 %), Brent Oil at $53.76 (-0.15%)

- Rates: US 10-year yield at 2.13, UK 10-year yield at 1.04, German 10-year yield at 0.335

News & Data:

- (AUD) NAB Business Confidence 5 vs 12 previous

- (JPY) Prelim Machine Tool Orders y/y 36.3 % vs 28.0 % previous

- (EUR) Italian Industrial Production m/m 0.1 % vs -0.5 % expected

- (CAD) Housing Starts 223 K vs 216 K expected

- UN Security Council Votes To Increase Sanctions On North Korea

- Oil prices dip as traders assess U.S. hurricane impact- RTRS

Markets Update:

Following a firm lead on Wall Street, further upside was seen in Asian equity markets as Hurricane Irma and North Korea concerns wane. The Nikkei rose 1 percent, shadowed closely by the Kospi gaining .22% with the Shanghai Composite trading higher by .10%. Meanwhile, the Hang Seng Index declined .08%.

USD/JPY action is little changed on the session. To the upside, resistance stands at 109.50 with support not expected to appear until the unit taps the 109 handle.

EUR/USD also effectively unchanged on the session. Current support positioned at 1.1950 with the candles showing signs of weakening here. The next downside target in view is September’s monthly opening level at 1.1913, followed closely by the 1.19 handle. Technically speaking, downside is favored in this market right now given the upbeat dollar. Be that as it may, it’s advised to keep USDX weekly resistance at 11854 on the radar as the dollar could turn from here.

AUD/USD slipped lower during Sydney this morning, thanks largely to another disappointing result from the weekly consumer confidence index. Recently breaking through key support at 0.8050, price is now largely free to challenge nearby support at 0.80 – a watched level in this market.

Alongside the Aussie dollar, gold also dropped marginally lower following its overnight decline, tackling support at 1325.9 and possibly clearing the runway south down to the 1320.4 neighbourhood.

Upcoming Events:

- 05:30 GMT – (EUR) French Non-Farm Payrolls Q2

- 08:30 GMT – (GBP) CPI y/y

- 08:30 GMT – (GBP) PPI Input m/m

- 08:30 GMT – (GBP) RPI y/y

- 13:45 GMT – (EUR) ECB’s Constancio Speaks

- 14:00 GMT – (USD) JOLTS Job Openings

- 23:50 GMT – (JPY) BSI Large Manufacturing Conditions (Q3)

Risk Appetite Continued To Strengthen Yesterday

Market movers today

On a day with only tier-2 data out on the global front, focus is likely to continue to be on the situation with North Korea, where markets will digest the UN vote yesterday. Further reports on the cost of Hurricane Irma may also affect whether the boost to risk sentiment over the past days has more legs (see below).

It is fairly quiet on the global data front today. The UK is due to release CPI for August where we look for a rise in CPI of 0.5% m/m (rounded up), which should be enough to push CPI inflation up from 2.6% to 2.8% y/y – in line with consensus.

The US is due to release the NFIB small business optimism index for August. The index rose sharply after the election of Donald Trump but levelled off in early 2017. However, last month it jumped higher again, adding to signs that US activity is re-gaining momentum. Consensus is for a small decline to 104.8 from the very high level 105.2 in July.

In Scandi it is time for Swedish inflation and the regional network survey from Norway. We look for Swedish inflation to be higher than consensus and the Riksbank's estimate, see Scandi Markets on the next page for more.

Selected market news

Risk appetite continued to strengthen yesterday. US stocks rallied more than 1% to a new cycle high as easing event risks are letting the strengthening business cycle shine through. See also Strategy – Strong cycle while US debt limit risk is postponed, 8 September 2017. The three event risks weighing on markets (North Korea, hurricanes and the US debt limit) have all eased and paved the way for a risk rally. US bond yields moved higher in response and EUR/USD corrected a bit further falling below 1.20 yesterday.

The UN Security Council last night agreed unanimously to step up sanctions against North Korea following its sixth and most powerful nuclear test on 3 September, see Reuters. After a week of negotiations a watered down resolution was voted through the Council as the US had to drop several measures to gain support from Russia and China. Instead of a full oil embargo, the resolution implies a reduction in oil and fuel exports to North Korea. New language was also added urging ‘further work to reduce tensions so as to advance the prospects for a comprehensive settlement'. The latter is likely to be a demand from Russia and China that do not believe sanctions are likely to stop the regime in Pyongyang from its nuclear ambitions.

In the UK, Prime Minister Theresa May won a small victory as the EU withdrawal bill passed in parliament with a vote of 326 to 290, see Bloomberg. It has been controversial as it gives ministers strong powers to change legislation without it being fully accepted by parliament (so-called ‘Henry VIII powers' named after the Tudor King).

In Norway, the parliamentary elections led to the re-election of the conservative government. Hence, any short- or long-term uncertainty regarding economic policy should be reduced.

Bank Of Japan Continues To Distort ETF Market

Key Points:

- BOJ reaches 75% ownership of the ETF market.

- Eventual unwinding poses significant risk levels.

- Watch for long term damage to ETF markets on TOPIX.

There is no doubt that the past seven years has been a watershed for macroeconomic policy, as well as financial markets, as central banks have ardently cast aside the accepted playbook and moved into the realm of policy experimentation. Subsequently, what was birthed was the quantitative easing process which saw the Bank of Japan inject huge amounts of money into the broader economy in an attempt to stimulate spending and investment activity.

However, what started out as the noblest of endeavours has quickly turned farcical as the BOJ quickly moved from running the printing presses to targeted injections of funds directly into the ETF market. Initially, this was welcomed by the broader sector as a way to provide liquidity and cash to the Exchange Traded Funds in an attempt to stimulate some economic growth and inflation. Instead, the central bank has been slowly hoovering up the majority of ETF sales in the past five years and this has caused some significant market distortions.

In fact, the most recent figures show the Bank of Japan holding just below 75% of the total present volume of the ETF market. This is staggering to say the least and should make the free market proponents amongst us queasy with risk. Subsequently, ETF assets held by the bank have surged 10 fold since the early 2010’s to the current epic proportions.

This pattern of non-monetary grade asset purchases is relatively problematic given the risk of ongoing distortions in values. Holders of ETF’s would need to ask themselves what will occur when the central bank starts to unwind those positions given that they form the major buyer in the market. The reality is that ETF values would crash relatively quickly once the central bank makes moves to unwind its positions. Subsequently, there is an inherent risk in any central bank dealing directly with the market through an asset such as an ETF.

In fact, the major question that immediately pops into my mind is the potential for calamity on the broader equity market if and when the bank starts to sell off their ETF positions. At present levels, ETF’s only represent around 5% of the TOPIX market but this is not an inconsequential figure and commencing a selling phase could signal the broader market that the game is up.

Ultimately, there is rising levels of risk within the Japanese markets and much of this is due to the uncertain outcomes around the Bank of Japan’s misguided quantitative easing program. Subsequently, it will remain to be seen what damage the inevitable unwind causes but one thing is for certain….there are no free lunches in economics.

Market Update – Asian Session: UN Security Council Passes N. Korea Sanctions

Asia Summary

Asian equity markets opened higher tracking the strength in the US session. Where the USD continued its relief rally after north Korea failed to launch as missile over the weekend and Hurricane Irma impact was less than expected in the US. Some analysts have also pointed towards increasingly stronger China data and rising inflation as another trigger to spur the buying along. The PBOC weakened the yuan reference rate by 0.4% to 6.5277, the first time in 12 sessions. Offshore yuan fell to a 6-month low on the weaker setting. PBOC did again skip open market operations for the 4th consecutive session, has not happened since early January.

The UN Security Council voted unanimously to implement stronger sanctions against North Korea. New measures will ban all textile exports, however are softer than US’s initial proposal. USD/KRW was little changed in the session and North Korea failed to comment. In the UK Lawmakers voted against opposition labor party attempt to block EU withdrawal bill; vote 326-290, Brexit bill to move to next stage. The Sterling showed muted gains on the news.

Key economic data

(AU) AUSTRALIA AUG NAB BUSINESS CONFIDENCE: 5 V 12 PRIOR; CONDITIONS: 15 V 14 PRIOR (highest level since early 2008)

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 109.8 v 114.1 prior

(PH) Philippines Jul Trade Balance: -$1.65B v -$2.4Be

(KR) South Korea Jul M2 Money Supply M/M: -0.2% v 0.4% prior; L Money Supply M/M: 0.9% v 0.3% prior

Speakers and Press

China/Hong Kong

(CN) PBoC Vice Gov Yin Yong: financial risks are on the rise while anti money-laundering efforts face challenges

(HK) Hong Kong Financial Sec Chan: HK's economy has been "very positive" in recent two months after better-than-expected growth in Q2

(CN) China Premier Li: China is resolute about opening up; Reiterates to continue proactive Fiscal policy and prudent monetary policy - press

Korea

(KR) UN SECURITY COUNCIL VOTES IN FAVOR OF INCREASING SANCTIONS AGAINST NORTH KOREA

(KR) South Korea: N. Korea is technically ready for a nuclear test

(US) US launches missile tracking plane from Kadena airbase - Japan press

Japan

(JP) Japan PM Abe Cabinet approval rating rises to 50%, up 8 pct points in poll taken Sept 8-10 – Yomiuri

Other

(UK) Lawmakers votes against opposition labor party attempt to block EU withdrawal bill; vote 326-290, Brexit bill to move to next stage

(US) US Senate Majority Leader McConnell said the debt limit will not have to be increased until 'well into 2018' 'amid the availability of extraordinary measures' - NYT Interview

Asian Equity Indices/Futures (00:00ET)

Nikkei 1.0%, Hang Seng 0.0%; Shanghai Composite +0.1%, ASX200 +0.7%, Kospi +0.1%

Equity Futures: S&P500 -0.0%; Nasdaq100 +0.0%, Dax -0.1%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1964-1.1946; JPY 109.58-109.24; AUD 0.8034-0.7998; NZD 0.7267-0.7226

Dec Gold -0.4% at $1,329/oz; Oct Crude Oil -0.1% at $48.02/brl; Sept Copper -0.6% at $3.05/lb

GLD SPDR Gold Trust ETF daily holdings +0.1% to 835.7 metric tonnes

(AU) Australia sells A$150M 2022 Indexed Bonds; avg yield 0.4025%; bid-to-cover 3.98x

(CN) PBOC SKIPS OPEN MARKET OPERATIONS (OMO) V SKIPPED PRIOR (4th consecutive skip, most since early Jan)

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT: 6.5277 V 6.4997 PRIOR (1st weaker setting in 12 sessions)

JGB (JP) Japan MoF sells ¥1.78T in 5-yr JGBS; avg yield -0.110%; bid-to-cover 4.07x

Equities notable movers

Australia/New Zealand

SGH.AU nnounces cost cutting measures, to cut 7% of employees in Australia; +3%

RAP.AU Developing the world’s first clinically-tested, regulatory-cleared respiratory disease diagnostic test and management tools for smartphones - Investor presentation; +16%

Hong Kong/China

1222.HK To sell 60% stake in site in Hong Kong for HK$2.44B; +4.3%

Japan

6502.JP Toshiba reportedly to sell chip unit to Western Digital-led consortium - Japanese press; +0.3%

Australia’s Business Conditions Climbed To Its Highest Since Early 2008 In August

For the 24 hours to 23:00 GMT, the AUD declined 0.14% against the USD and closed at 0.803.

LME Copper prices declined 0.6% or $43.0/MT to $6737.0/MT. Aluminium prices rose 1.4% or $28.5/MT to $2100.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8013, with the AUD trading 0.21% lower against the USD from yesterday's close.

Early morning data indicated that Australia's NAB business conditions index edged up to a level of 15.0 in August, notching its highest level in nine years. The index had registered a revised level of 14.0 in the previous month. On the other hand, the nation's NAB business confidence index sharply declined to a level of 5.0 in August, after recording a level of 12.0 in the prior month.

The pair is expected to find support at 0.7988, and a fall through could take it to the next support level of 0.7963. The pair is expected to find its first resistance at 0.8048, and a rise through could take it to the next resistance level of 0.8083.

Going ahead, Australia's Westpac consumer confidence index for September, due to release overnight, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.