Sample Category Title

Trade Idea Update: USD/CHF – Stand aside

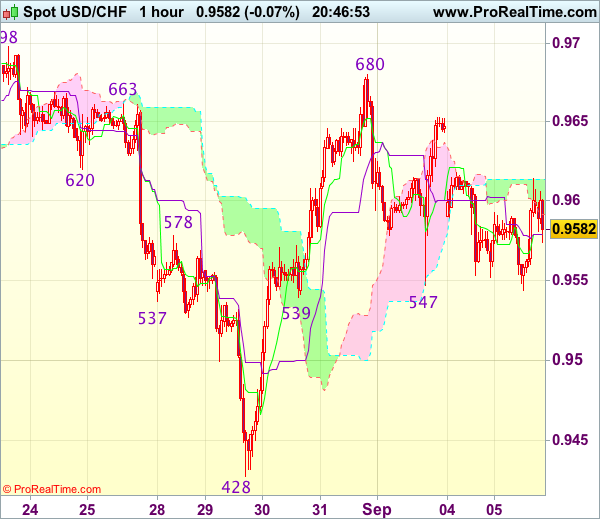

USD/CHF - 0.9585

Original strategy :

Buy at 0.9520, Target: 0.9620, Stop: 0.9485

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9520, Target: 0.9620, Stop: 0.9485

Position : -

Target : -

Stop : -

Although the greenback has rebounded after holding above previous support at 0.9539, reckon upside would be limited to 0.9615-20 and near term downside risk remains for another test of said support, however, if our view that low has been formed at 0.9428 last week is correct, downside would be limited to 0.9520 and bring another rebound later. Above 0.9615-20 would bring test of 0.9653-55 resistance, break there would bring another rise to 0.9680 but break there is needed to add credence to this view and extend gain to resistance at 0.9698-99.

In view of this, would not chase this rise here and would be prudent to buy dollar on further subsequent retreat. Below 0.9515-20 would risk weakness to 0.9490-00 but still reckon downside would be limited to 0.9450-60 and said support at 0.9428 should remain intact, bring another rebound later.

EUR/USD – Dollar Selling Prevails

The EURUSD pair has moved back towards the 1.1900 level, as the U.S dollar comes under pressure from risk-off trading sentiment. Earlier, the euro fell to 1.1868, but soon found buying interest, as North Korean fears persist.

During the upcoming U.S trading session, North American markets will return after Labour Day Holiday. Investors will look to the ongoing situation in the Korean peninsula, U.S factory orders and a host of Federal Reserve speakers.

The EURUSD pair is currently trading at its daily pivot point, located at 1.1897, however, the euro remains neutral on an intraday basis, while trading below the 1.1918 level.

Going forward, a break above the 1.1930 level remains the key to further upside, with technical resistance found at 1.1960, 1.1979 and 1.2030-40.

To the downside, key technical support is located at the monthly pivot point, at 1.1884, the Friday spike low, at 1.1850, and the former weekly price low, at 1.1822.

Trade Idea Update: GBP/USD – Stand aside

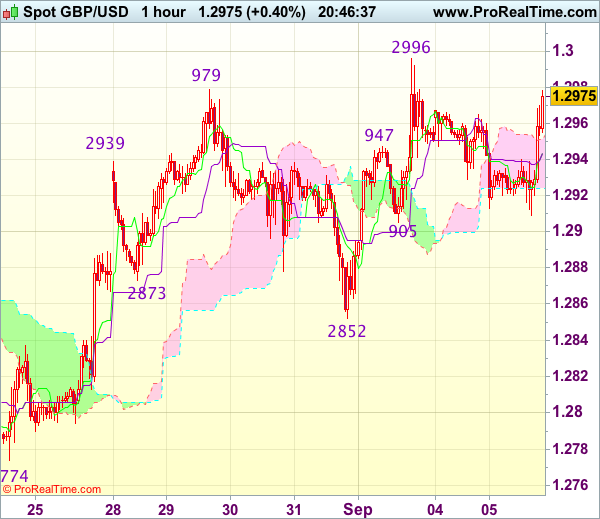

GBP/USD - 1.2981

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the British pound has rebounded again after holding above indicated support at 1.2905 and gain to 1.2996-00 psychological level cannot be ruled out, break there is needed to retain bullishness and signal recent rise from 1.2774 has resumed and extend gain to previous resistance at 1.3032, however, near term overbought condition should limit upside to 1.3055-60 (100% projection of 1.2774-1.2979 measuring from 1.2852) and reckon 1.3080 (61.8% Fibonacci retracement of 1.3269-1.2774) would hold.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.2940 would prolong consolidation and bring weakness to 1.2905 but break of latter level is needed to signal top has been formed, bring further fall to 1.2875-80 and possibly towards previous chart support at 1.2852 which is likely to hold from here.

Sterling Moves Towards Range Top

The GBPUSD pair has looked past a marginally weaker United Kingdom services sector PMI reading, and moved towards the higher-end of its recent trading range.

Today's 53.2 PMI services reading has yet to dampen demand for the British pound, with the pound gaining ground against the euro, and trading around the 1.2969 level against the greenback.

The GBPUSD pair remains confined to range-bound trading conditions between the 1.2910 and 1.2990 level, however, price-action is printing bullish higher daily price high's.

Key intraday technical resistance is located at the 50-day moving average, at 1.2984, with the former weekly price high and monthly pivot point, found at 1.2990-1.2994.

Above 1.3000 level, the GBPUSD June monthly price high offers strong resistance, at 1.3030, as does the 1.3047 level.

To the downside, key trendline support is located at 1.2948, with the weekly pivot point, at 1.2936. The daily time-frame, 100-period moving average, offers critical intraday support, at 1.2920.

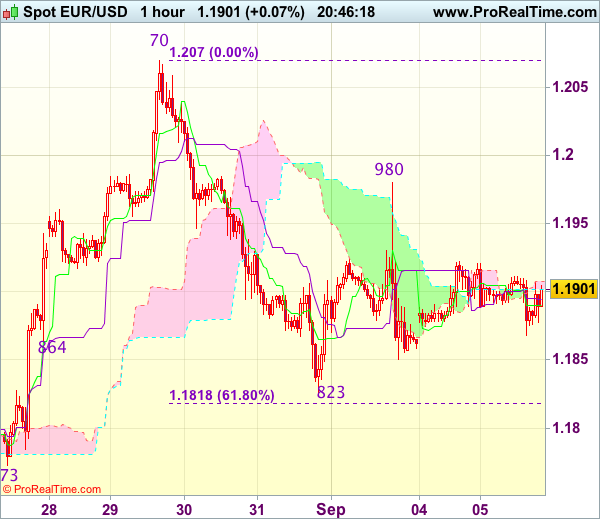

Trade Idea Update: EUR/USD – Sell at 1.1955

EUR/USD - 1.1901

Original strategy :

Sell at 1.1955, Target: 1.1855, Stop: 1.1990

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1955, Target: 1.1855, Stop: 1.1990

Position : -

Target : -

Stop : -

As the single currency has traded narrowly, suggesting further sideways trading would be seen and although another bounce to 1.1925-30 is likely, reckon 1.1950-55 would limit upside and bring another decline, below 1.1850 would signal the rebound from 1.1823 has ended, bring test of this level, break there would add credence to our view that top has been formed at 1.2070 earlier and extend the fall from there to 1.1815-18 (61.8% Fibonacci retracement of 1.1662-1.2070), then 1.1790-00 but downside should be limited and previous support at 1.1773 should remain intact.

In view of this, we are looking to sell euro again on recovery as 1.1950-55 should limit upside. Only break of said resistance at 1.1980 would abort and signal the fall from 1.2070 has ended at 1.1823 yesterday, bring further gain to 1.2000 and possibly towards 1.2025-30.

Commodity Currencies Strengthen as Risk Sentiments Continue to Stabilize

Market sentiments continue to stabilize today with European indices trading mixed. DAX is trading up 0.55% at the time of writing, CAC flat and FTSE down -0.1%. US futures point to a mildly lower open as markets come back from holiday. In the currency markets, Yen is firm against most currency except Aussie and Kiwi. But Swiss Franc is trading broadly lower as risk aversion recedes. Euro and Dollar are trading as the second and third weakest for the day so far. In other markets, gold pares back some gain but maintains near term bullishness for a take on 1350 handle later in the week. WTI crude oil staging a strong rebound and is back above 48. Strength in oil might start to life Canadian Dollar later in the session.

US to push more sanction but Russia disagrees

Concerns over Korea tensions recede temporarily even though there are reports that North Korea is quietly moving another intercontinental ballistic missile towards its west coast, readying for another launch by the end of the week. The United Nations Security Council emergency meeting ended with no consensus yesterday. US is pushing for toughing sanctions for a vote on September 11. But Russian President Vladimir Putin said that "sanctions of any kind would now be useless and ineffective" as "they'd rather eat grass than give up their nuclear programme". Putin urged to "promote dialogue among all interested parties."

Meanwhile, North Korea ambassador to UN, Han Tae Song, said in the forum in Geneva that "the recent self-defense measures by my country, DPRK, are a 'gift package' addressed to none other than the U.S." And, he warned that "the U.S. will receive more 'gift packages' from my country as long as its relies on reckless provocations and futile attempts to put pressure on the DPRK." He also emphasized that "pressure or sanctions will never work on my country." He added that "The DPRK will never under any circumstances put its nuclear deterrence on the negotiating table." And, the military measures were "restraint and justified self-defense" to counter "the ever-growing and decade-long U.S. nuclear threat and hostile policy aimed at isolating my country".

Fed Brainard: Fed should be cautious about more tightening

Fed Governor Lael Brainard said today that Fed should be " cautious about tightening policy further until we are confident inflation is on track to achieve our target." She also noted that "there is a high premium on guiding inflation back up to target so as to retain space to buffer adverse shocks with conventional policy." And she emphasized that " it is important to be clear that we would be comfortable with inflation moving modestly above our target for a time." Minneapolis Fed President Neel Kashkari and Dallas Fed President Robert Kaplan will speak later today.

UK PMI services sends warning signals

UK PMI services dropped to 53.2 in August, down from 53.8 and missed expectation of 53.5. That's also the lowest level in 11 months. Markit noted that the latest round of PMIs suggest 0.3% growth in the UK economy in the current quarter, same as Q2. However, Markit chief economist Chris Williamson warned that "momentum is being gradually lost." And, "robust manufacturing growth means the economy may be rebalancing towards goods production, aided by the weaker pound, but the slowdowns in services and construction send warning signals about the health of the economy." Also, "the overall level of optimism also remained subdued, mainly linked to Brexit uncertainty, close to levels that have previously been indicative of the economy stalling or even contracting."

Also from Europe, Swiss GDP grew 0.3% qoq, 0.3% yoy in Q2, much lower than expectation of 0.5% qoq, 1.0% yoy. CPI rose to 0.3% yoy in August, but missed expectation of 0.5% yoy. Eurozone retail sales dropped -0.3% mom in July, in line with consensus. Eurozone services PMI was revised down to 54.7 in August, Germany PMI services revised up to 53.5, France PMI services revised down to 54.9. Italy PMI services dropped to 55.1 in August.

RBA Lowe: Stimulatory policy continues to be appropriate

As widely anticipated, the RBA left the cash rate unchanged at 1.5%, historic low since August 2016. Policymakers remained confident over the economic outlook, but stayed cautious over the strength in property prices. Again, they warned that recent appreciation in Australian dollar would weigh on the outlook for growth and employment, and prolong soft inflation. It appeared that the central bank would keep its policy rate unchanged at the current level for some time. More in RBA Left Cash Rate At 1.5%.

Speaking at a dinner in Brisbane after the rate announcement, RBA governor Philip Lowe said that low interest rates are supporting job growth and inflation. And "these are positive developments." Though, he sounded cautious and said that ", it will be some time before we are at what could be considered full employment in Australia and before underlying inflation is at the mid-point of the medium term target range." Therefore, "stimulatory monetary policy continues to be appropriate."

Released earlier today, Australia current account deficit widened to AUD -9.6b in Q2. New Zealand ANZ commodity price dropped -0.8% in August. China Caixin PMI services rose to 52.7 in August.

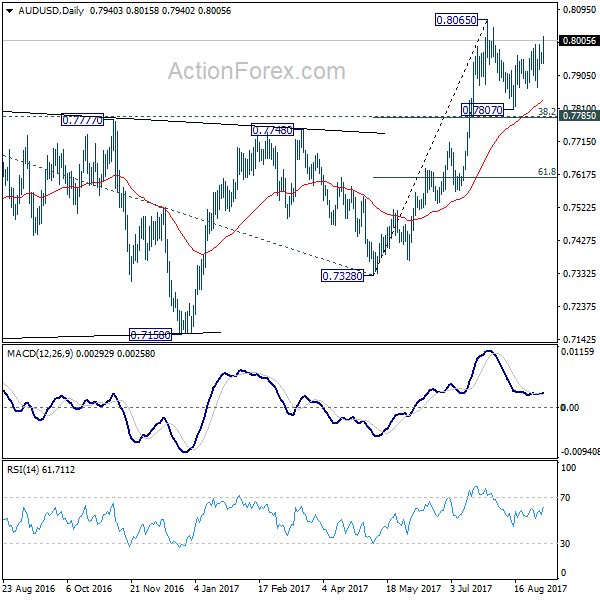

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7932; (P) 0.7952; (R1) 0.7963; More...

AUD/USD jumps notably in early US session but it's staying well below 0.8065 resistance. Intraday bias remains neutral for the moment as consolidation from 0.8065 might extend. But in case of another fall, downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. On the upside, break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8087) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | NZD | ANZ Commodity Price Aug | -0.80% | -0.80% | ||

| 1:30 | AUD | Current Account Balance (AUD) Q2 | -9.6B | -7.4B | -3.1B | -4.8B |

| 1:45 | CNY | Caixin PMI Services Aug | 52.7 | 51.8 | 51.5 | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 5:45 | CHF | GDP Q/Q Q2 | 0.30% | 0.50% | 0.30% | 0.10% |

| 5:45 | CHF | GDP Y/Y Q2 | 0.30% | 1.00% | 1.10% | 0.60% |

| 7:15 | CHF | CPI M/M Aug | 0.00% | 0.00% | -0.30% | |

| 7:15 | CHF | CPI Y/Y Aug | 0.30% | 0.50% | 0.30% | 0.10% |

| 7:45 | EUR | Italy Services PMI Aug | 55.1 | 55.5 | 56.3 | |

| 7:50 | EUR | France Services PMI Aug F | 54.9 | 55.5 | 55.5 | |

| 7:55 | EUR | Germany Services PMI Aug F | 53.5 | 53.4 | 53.4 | |

| 8:00 | EUR | Eurozone Services PMI Aug F | 54.7 | 54.9 | 54.9 | |

| 8:30 | GBP | Services PMI Aug | 53.2 | 53.5 | 53.8 | |

| 9:00 | EUR | Eurozone Retail Sales M/M Jul | -0.30% | -0.30% | 0.50% | 0.60% |

| 14:00 | USD | Factory Orders Jul | -3.30% | 3.00% |

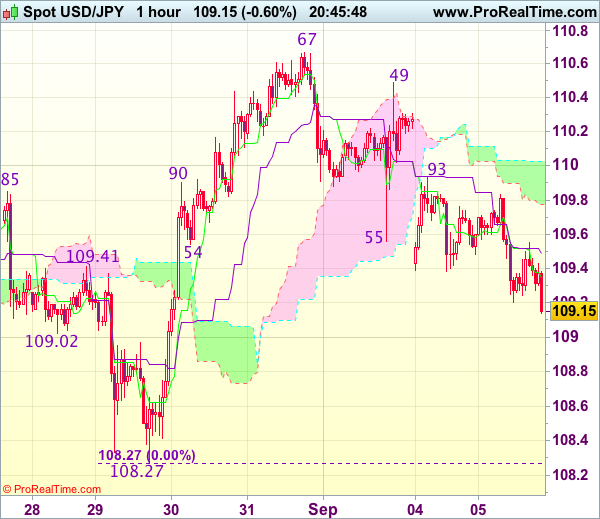

Trade Idea Update: USD/JPY – Sell at 109.80

USD/JPY - 109.20

Original strategy :

Sell at 109.80, Target: 108.80, Stop: 110.15

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.80, Target: 108.80, Stop: 110.15

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after opening lower yesterday, adding credence to our view that top has possibly been formed at 110.67 last week and consolidation with downside bias remains for weakness to 109.15-19 (61.8% Fibonacci retracement of 108.27-110.67), however, break there is needed to provide confirmation and bring further fall to 108.80-85, however, reckon 108.55-60 would limit downside and support at 108.27 remain intact.

In view of this, we are looking to sell dollar on recovery as 109.80-85 should limit upside and bring another decline later. Above 110.00-05 would defer and risk rebound to 110.30 but only break of 110.49 would signal the pullback from 110.67 has ended, bring retest of this level first.

CAC Unchanged Despite Soft French Services PMI

The CAC index is unchanged in the Tuesday session. Currently, the index is at 5,100.50, down 0.04% on the day. On the release front, Eurozone Final Services PMI dipped to 54.7, just shy of the estimate of 54.9 points. French Final Services PMI softened to 54.9, missing the forecast of 55.5 points. As well, Eurozone Retail Sales came declined 0.2%, shy of the estimate of -0.3%. On Wednesday, the eurozone publishes Retail PMI.

The eurozone economy continues to hum in the second half of 2017, as economic indicators have generally been positive. Germany continues to lead the eurozone with robust growth, but France has also enjoyed a recovery in 2017. Last week, French numbers impressed, as CPI and Consumer Spending rebounded with gains, following declines in the previous release. As well, Preliminary GDP improved to 0.5% in the second quarter.

All eyes are on the ECB, which will hold an important policy meeting on Thursday. With the economy looking brighter, what to do with the ECB quantitative easing program the main order of business. The current program terminates in December, and the bank will have to decide on a new scheme. However, analysts don't expect the details of the new program to be announced until October or possibly December. Still, every nuance from Mario Draghi's press conference will be analyzed, and any hints about changes in the ECB's monetary policy, such as withdrawing stimulus, is likely to have a sharp impact on the euro. The eurozone's strong performance in 2017 has raised speculation that the ECB will commence tapering in the near future, but the rejuvenated euro has complicated matters. The euro has gained some 13% against the dollar this year, with much of the appreciation due to speculation that the ECB will end its asset purchases. The stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening, so the ECB could decide on a slow exit from its asset purchase scheme. Aside from the headache of a stronger euro, ECB policymakers must wrestle with the dilemma of what monetary stance to take with a stronger eurozone economy that remains gripped by very low inflation.

DAX Gains on Steady Services PMIs

The DAX index has posted gains in the Tuesday session. Currently, the DAX is currently trading at 12,170.50, up 0.54% on the day. On the release front, German and Eurozone Services PMI were within expectations. Eurozone Retail Sales declined 0.2%, shy of the estimate of -0.3%. On Wednesday, Germany releases Factory Orders and the eurozone publishes Retail PMI.

The DAX has responded positively to services sector numbers, as German and Eurozone Services PMIs both pointed to slight expansion. Eurozone Services PMI slowed to 54.7, shy of the estimate of 54.9 points. However, German Services PMI improved to 53.5, edging above the forecast of 53.4 points. Retail Sales was not as positive, posting a decline of 0.3%, compared to a gain of 0.5% a month earlier. This marked the first decline since January. If upcoming consumer spending data is weak, investor risk appetite could weaken and send stock markets lower.

The ECB will hold a crucial policy meeting on Thursday, with the bank's quantitative easing program the main order of business. The ECB's current asset-purchase program terminates in December, and the bank will have to decide on a new scheme. However, analysts don't expect the details of the new program to be announced until October or possibly December. Still, every nuance from Mario Draghi's press conference will be analyzed, and any hints about changes in the ECB's monetary policy, such as withdrawing stimulus, is likely to have a sharp impact on the euro. The eurozone's strong performance in 2017 has raised speculation that the ECB will commence tapering in the near future, but the rejuvenated euro has complicated matters. The euro has gained some 13% against the dollar this year, with much of the appreciation due to speculation that the ECB will end its asset purchases. The stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening, so the ECB could decide on a slow exit from its asset purchase scheme. Aside from the headache of a stronger euro, ECB policymakers must wrestle with the dilemma of what monetary stance to take with a stronger eurozone economy that remains gripped by very low inflation. Will the ECB address these concerns at the Thursday meeting?

GBP/USD Inverted Head And Shoulders Rejecting The Price Within W H3 – W L3 Range

As we could see on my yesterday's Session Recap webinar, the GBP/USD has perfectly rejected from the POC zone I showed making a total of 60 pips that accounts for 90 % of its ATR(14). Today we can see that 2 POC(S) zones could be above the price as sellers might be waiting there. A slight miss in UK CPI could encourage fresh seller to kick in within 1.2990-1.3000 and possibly 1.3030. We can see how the price respects W L3- W H3 standard camarilla range (70 % of the time) so we might see another rejection towards the 1.2900 zone. However due to bullish SHS pattern (inverted head and shoulders) now moment buyers are exactly at the same spot where historical buyers where so we can see a buying interest within 1.2900-10 zone. The change of a trend is only possible if the price gets below 1.2900 with a strong momentum and 4h candle closes below 1.2870.