Sample Category Title

Euro Drifts Lower as Eurozone Economic Activity Stagnates and Consumers Spend Less

Today's evidence of Eurozone's economic activity and consumption will sound good news to ECB policymaker's ears on Thursday when they will gather to decide on monetary policy in Frankfurt. Despite overall economic activity slowing down in August and retail sales declining in the same period, their levels remained robust, supporting GDP growth in the third quarter of the year. In the wake of the data, the euro reacted negatively while it was trying to build an uptrend.

Following upbeat manufacturing PMI results out of the Eurozone last Friday which showed that the manufacturing PMI remained at six-year high levels in August, the service PMI index for the same month, released during European trading hours, came in slightly lower than expected. However, the performance of the services sector held strong as it was comparable to the ones seen prior the recent financial crisis in the region. According to IHS Markit, service PMI in the block retreated by 0.7 points to a seven month low of 54.7 in August, missing the forecast of 54.9. Overall, the composite PMI for the region which summarizes manufacturing and service activities, fell moderately by 0.1 points to 55.7, below the 55.8 expected.

Inflow of new business was mainly observed in the service sector while job growth and rising prices were the main supporters of the composite index. The flow of new business remained above its long-run trend despite it fell to a seven-month low while jobs grew slower but continued expanding for the fourth consecutive month. Output charges and Input costs rose in August, hitting three-month highs. Nevertheless, inflation slowed down from previous peaks posted in the year. Companies optimism eased to the lowest year-to-date mark after it touched a record high in May.

Among the five European countries participating in the survey, Germany and Ireland registered the highest outputs. While Germany experienced the highest increase in production volumes since 2011, it posted the lowest growth in service activities among other participants. Ireland saw an improvement in both manufacturing and service activities.

Regarding Eurozone consumption, it turned negative in July after six months of rising higher. Month-on-month retail sales declined by 0.3% while analysts expected a fall of 0.2%. June's mark was revised from a positive 0.5% to a positive 0.6%. On a yearly basis, retail sales expanded by 2.6%, surpassing the forecast of 2.5% but scaled back from June's reading of 3.3% which was upwardly revised from 3.1%. July's mark was the second best registered during the year.

Although the above numbers highlight the block's resilience to economic shocks, the ECB is said to maintain its current monetary policy steady at its meeting on Thursday in Frankfurt, as several ECB officials expressed their concerns over an appreciating exchange rate. However, this might increase the odds of stimulus reduction in 2018 – with the announcement probably made at October's meeting – given that economic indicators would support such actions by the ECB. Despite inflation lagging the target of 2%, the central bank signaled in July that it would probably announce a reduction in its asset purchases – known as quantitative easing program – "this autumn" before the program expires in November, as GDP growth follows a solid path year to date.

In the forex markets, euro/dollar fell immediately by 0.30% to 1.1867 in the wake of the news but managed to recover soon after, climbing to 1.1894. Euro/yen did not react much to the data but dropped to a one-week low of 129.87 amid rising risk-off sentiment in the markets while euro/pound retreated by 0.27% to 0.9180 following the figures before it headed downwards to 0.9157 due to option expiries.

Capital Spending Firms Despite Soft Print for Factory Orders

The 3.3 percent decline in factory orders for July is largely a reflection of a drop in aircraft orders following a surge in the prior month. Core orders and shipments still indicate steady improvement in business spending.

Taking Stock

- The payback from June's surge in aircraft orders was enough to pull the headline into negative territory, but ex-transportation orders were up 0.5 percent—the best month since January.

- Inventories increased for a second-straight month; this is consistent with our expectation for inventories to be additive to growth in the second half. The fact that the inventory-toshipment ratio came down suggests the stockpiling is justified.

Despite Choppy Headlines, Gradual Firming in Core

- Shipments of core capital goods orders increased 1.2 percent in July, lifting the 3-month annualized growth rate to 5.4 percent. This is consistent with our forecast for gradual firming in equipment investment in the third quarter.

- In a positive sign for future spending prospects, core capital goods orders also increased in July, growing 1.0 percent which puts the 3-month annualized rate for that series at 5.1 percent.

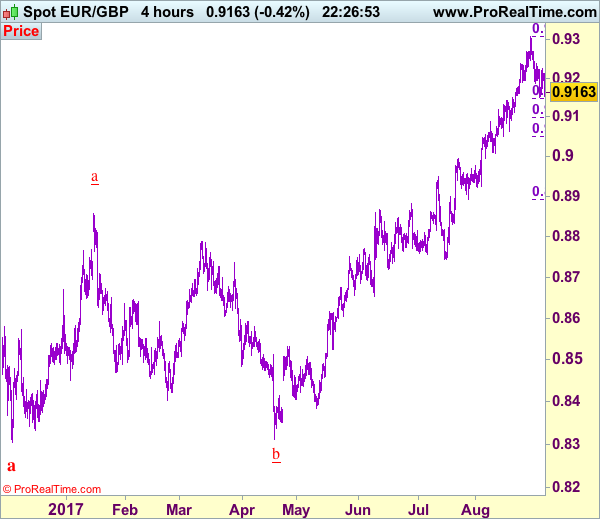

Trade Idea: EUR/GBP – Sell at 0.9265

EUR/GBP - 0.9172

Original strategy :

Sell at 0.9265, Target: 0.9115, Stop: 0.9305

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9265, Target: 0.9115, Stop: 0.9305

Position : -

Target : -

Stop : -

Euro’s retreat after rising to 0.9307 last week suggests consolidation below this level would be seen and reckon 0.9250-60 would limit upside, bring another decline to 0.9148-50 (38.2% Fibonacci retracement of 0.8892-0.9307 and previous support), break there would add credence to our view that top is possibly formed there, bring retracement of recent rise to 0.9110-15 and possibly towards 0.9095-00 (50% Fibonacci retracement) which is likely to hold from here.

In view of this, we are inclined to sell euro on recovery as 0.9265-70 should limit upside. Only above said resistance at 0.9307 would revive bullishness and extend recent upmove to 0.9325-30 and possibly towards 0.9350 but loss of upward momentum should limit upside and price should falter below 0.9390-00.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Dollar Maintains a Soft Bias

- European equities trade near opening levels with the German Dax outperforming (+0.5%). US stock markets open on a weak footing following the long Labour Day weekend as the explosive relation with North-Korea weighs on risk sentiment.

- Russian President Vladimir Putin has lambasted Washington and Seoul's drive to toughen sanctions against North Korea, adding that Pyongyang would "eat grass" rather than simply give up its nuclear programme.

- Washington Fed-based governor Brainard said the US central bank needs to pay careful attention to underlying inflation before raising interest rates again, as longer-run price pressure trends appear to be lower.

- Britain's economy is falling further behind a fast-recovering euro zone as firms worry about Brexit and consumers feel the pinch of rising inflation and the weak pound. The August services PMI declined more than expected, from 53.8 to 53.2. The final EMU services PMI was downwardly revised from 54.9 to 54.7.

- Switzerland's economy grew at its slowest annual rate in nearly eight years in the second quarter, according to data likely to reinforce expectations that the Swiss National Bank will keep monetary policy ultra-loose when it meets next week.

- German Chancellor Angela Merkel said European Union leaders should decide whether to suspend or end membership talks with Turkey at its summit next month, backtracking from her call to end accession talks.

Rates

US Treasuries take strong start

US and German bonds eke out moderate to minor gains in a session devoid of key economic news. US Treasuries opened higher in a catching up move linked to the North Korean nuclear threat. Following a stabilization, a second leg higher occurred shortly after the speech of Fed governor Brainard (14h30), which might have been the trigger of the move, even if some legitimate doubts remain timing-wise and cross markets. Brainard, a dove, is concerned about persistent low inflation and wants more evidence that inflation will move to target before raising rates further. She said the current neutral real FF rate may be close to 0% and the long run one close to 1%. This suggests the Fed has time to resume its tightening and may go still more gradual than previously thought. Of course, Brainard's view is only one and we hope to get more info when NY Fed Dudley, a key player, speaks later this week. The Bund opened unchanged and tested the downside, but when equities came off intra-day highs, the Bund marched higher in a long gradual climb. The Bund continued to advance also when equities slid in sideways trading mode.

At the time of writing, German yields drop between 1.2 bp (2-yr) to 1.9 bp (30-year). US bonds outperform German bonds, even taking into account yesterday's small dip of German yields. US yields decline by 3.2 bps at the 2-yr to 5.7 bps at the 10-yr tenor. In the intra-EMU bond markets 10-yr yield spreads are virtually unchanged.

Fed governor Brainard gave a speech at the NY Economic club. She is happy with the state of the economy, but sounds concerned about the persistent shortfall of inflation vis-à-vis the Fed's symmetrical 2% target. She downplays the impact of transitory factors on inflation, as the shortfall is persistent for 5 years. The underlying inflation is lower than before the crisis, contributing to the shortfall of inflation from the objective. The reason for that may be the experience of persistency of below target inflation which affects the perception of households and firms of underlying inflation. The Phillips curve is flatter than before. Monetary policy setting should take into consideration the persistency of the inflation shortfall. She sees the balance sheet tapering as a passive instrument to work in the background and to focus on the interest rate tool to help inflation towards target. Brainard pleads for cautiousness about tightening rates further until the Fed is confident inflation is on track to achieve the inflation target. She sees indications that the neutral rate of interest is very low currently and low relative to historic norms in the longer run and speaks about a zero real rate now and 1% long run FF rate in the long run (which would translate in a 1.5% nominal FF rate, now 1.125%, and a 3% in the long-run. "For these reasons, my current expectation is that the short-run neutral rate of interest may not rise much over the medium term. But this is an open question and bears close monitoring." She is aware that monetary policy may result in overextended asset prices and sees some signs of that. It calls for vigilance, but they aren't accompanied by excessive leveraging.

Currencies

Dollar maintains a soft bias

The eco data didn't provide a clear guide for EUR/USD or USD/JPY trading. The EMU data were slightly softer than expected, but EUR/USD hovered around the 1.19 pivot as investors await Thursday's ECB meeting. US investors returned from the long weekend in a cautious risk-off mood, keeping USD/JPY near the 109 level.

This morning, Asian markets traded mixed awaiting the next developments in the Korean crisis. The yen maintained a cautious bid as Japanese equities underperformed. USD/JPY dropped to the 109.25 area. EUR/USD was again little affected, trading just north of 1.19.

The euro showed some intraday swings during the European session. A first down-move occurred when the EMU PMI's were revised lower from the preliminary reading. However, we doubt it was the real reason behind the euro decline. There were other such swings later in the session without any concrete eco data behind. Interest rate differentials were also no obvious driver. We consider the moves as ST position adjustment ahead of Thursday's ECB meeting.

The dollar lost some further momentum in early US dealings. Soft comments from Fed's Brainard (she is on the dovish side of the Fed spectrum) were a slight USD negative. Lingering political uncertainty in Washington and globally (Korea) and a downward bias in US yields didn't help the dollar. However, after all, the changes in the major dollar cross rates were again limited. No technically relevant levels were challenged. EUR/USD continues trading in well-known-territory near 1.19. USD/JPY returned to the 109.15/20 area. The trade-weighted dollar holds within reach of the recent lows indicating that sentiment in the US currency remains fragile.

Sterling resumes technical rebound

The technical rebound of sterling took a breather yesterday but resumed today. The UK data didn't provide a valuable explanation. The UK August services PMI declined slightly more than expected from 53.8 to 53.2 (53.5 was expected). As is the case for EUR/USD, we see current GBP price action mainly as technical in nature. Last week's Brexit negotiations didn't yield any concrete progress and this issue will return to the forefront but sterling shorts apparently are taking some chips of the table, in particular against a strong euro. EUR/GBP drifted south and trades currently in the 0.9155 area. Cable is changing hands just below the 1.30 mark.

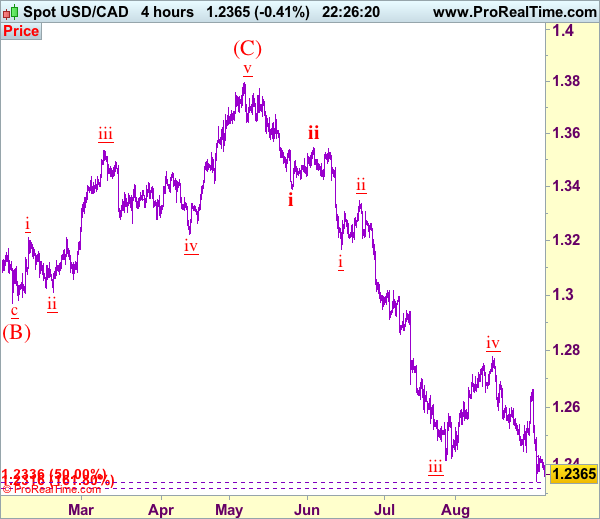

Trade Idea: USD/CAD – Sell at 1.2490

USD/CAD - 1.2363

Trend: Down

Original strategy :

Sell at 1.2500, Target: 1.2340, Stop: 1.2560

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2490, Target: 1.2340, Stop: 1.2550

Position: -

Target: -

Stop:-

Although the greenback recovered after falling to 1.2340 on Friday, reckon upside would be limited to 1.2420-25 and renewed selling interest should emerge around 1.2490-00, bring another decline, below 1.2340 would extend recent decline in wave v to 1.2300-10, having said that, oversold condition should limit downside and reckon current wave v would be limited to 1.2250-60, price should stay above 1.2200-10. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction possibly ended at 1.2778, wave v should extend towards 1.2200.

In view o this, would not chase this fall here and would be prudent to sell on recovery as 1.2490-00 should limit upside. Above 1.2550 would suggest a temporary low is formed instead, bring a stronger rebound to 1.2575-80 but indicated resistance at 1.2663 should remain intact.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

As Brexit Talks Falter, UK Services Activity Slows But Exporters See Signs of Upturn

After defying all the Brexit doom-mongers in the initial aftermath of the shock referendum result, the British economy appears to be succumbing to the uncertainty, with GDP in the first half of the year growing at its slowest in five years. Talks between Britain and the European Union have not gotten to a very good start, with little progress made on key issues after three rounds of negotiations.

The uncertain future of the UK's relationship with its European partners is weighing not just on business spending plans but is also hitting companies' ability to find available and skilled workers. Many EU citizens residing in the UK are leaving the country, while others are becoming less reluctant to move there. However, wages have yet to see significant upside pressure from the staff shortages. Combined with the surge in import prices as a result of the pound's tumble after the Brexit vote, UK consumers are feeling the pinch as living costs rise faster than household income.

The fall in people's disposable income is a serious risk to Britain's consumer led economy, where consumption accounts for about two thirds of GDP. There was further evidence of this today from the Markit/CIPS services PMI. The index fell from 53.8 to 53.2 in August, missing expectations of 53.5. This was the weakest reading since September 2016. Respondents to the survey said fragile business confidence and the uncertain outlook for the economy impacted on business decision making, while rising input costs added pressure on firms to raise prices. However, despite the deteriorating outlook, many firms reported a rising backlog of work and sought to raise capacity by hiring more people, pushing the employment index to a 19-month high.

In the manufacturing sector, the tide may finally be turning for UK exporters. Markit/CIP's latest manufacturing survey showed the PMI rising to a four-month high of 56.9 in August from an upwardly revised 55.3 in July, beating forecasts 55.0. Output was driven by stronger domestic as well as overseas demand and employment grew at its fastest since June 2014.

In a further sign that the weaker pound is finally boosting exports, the manufacturers' trade association, EEF, reported strong increases in output and orders in its latest quarterly survey today. The output balance rose to +34% in the third quarter from +26% in the prior quarter. The balance for export orders jumped to +33% and total orders hit a historic high of +37%.

Reaction to the above data has been limited in forex markets, with Brexit concerns and moves in other currencies being a bigger driver for sterling in recent days. The pound has been ranging in the $1.28-$1.30 region for the past week, while against the euro, it remains close to last week's 10½-month low of 0.9306 per euro.

It remains to be seen if the rebound in manufacturing activity will be sustainable and whether this will be enough to offset the slowdown in consumer spending. Progress in the Brexit negotiations will be crucial in assuring businesses that the UK is not headed for a cliff-edge exit when its withdrawal from the EU takes effect in March 2019. Prolonged uncertainty can only be negative for the pound and would further weigh on the economy's longer-term prospects.

GBP/USD Rejected By Dynamic Support

Price is trading in the green and looks determined to approach and reach fresh new highs in the upcoming period. Technically, is expected to climb much higher as it's located in the buyer's territory. The dollar is losing altitude as the USDX is still under massive selling pressure. USDX needs a bullish spark to be able to climb much higher in the upcoming period.

The index hovers right above the 92.49 static support, a rejection will signal a USD potential increase, but is premature to talk about this as the fundamental factors will have a significant impact in the afternoon.

The Cable increases even if the United Kingdom Services PMI dropped from 53.8 points to 53.2 points in August, has come much worse compared to the 53.5 estimate. The BRC Retail Sales Monitor increased by 1.3%, more versus the 0.9% estimate.

Price increased and erased the yesterday's losses and should reach and retest the 1.3046 static resistance. GBP/USD is expected to resume the upside movement after the failure to close the former gap down.

Technically should approach and reach at least the 1.3266 previous high. Resistance can be found at the first warning line (wl1) of the ascending pitchfork's body, where he may find temporary resistance again.

The false breakdown below the upper median line (UML) have attracted more buyers, which are trying to drive it towards fresh new highs.

EUR/USD Undecided

Price changed little today, but maybe the United States Factory Orders will bring life on this pair. The economic indicator is expected to drop by 3.3%, a better report will lift the greenback. Technically is somehow expected to climb much higher after the false breakdown below the median line (ml) of the minor descending pitchfork. Could come higher to retest the upper median line (UML) before will make a crucial decision.

NZD/USD Falling Wedge?

Price rallies and resumes the yesterday's bullish candle. You can see that the price action has developed a Falling Wedge pattern, but this is far from being confirmed. NZD/USD climbed above the 50% retracement level and is almost to touch the upside line of the Falling Wedge pattern.

Only a breakout followed by a minor consolidation above the 50% Fibonacci level will validate it and a bullish momentum.

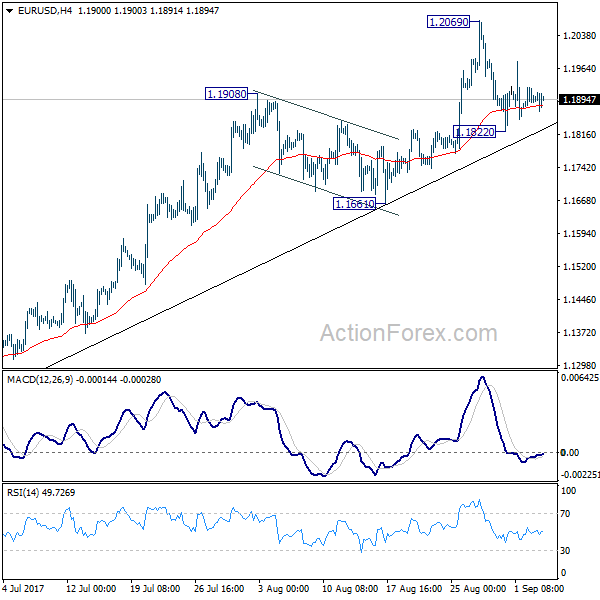

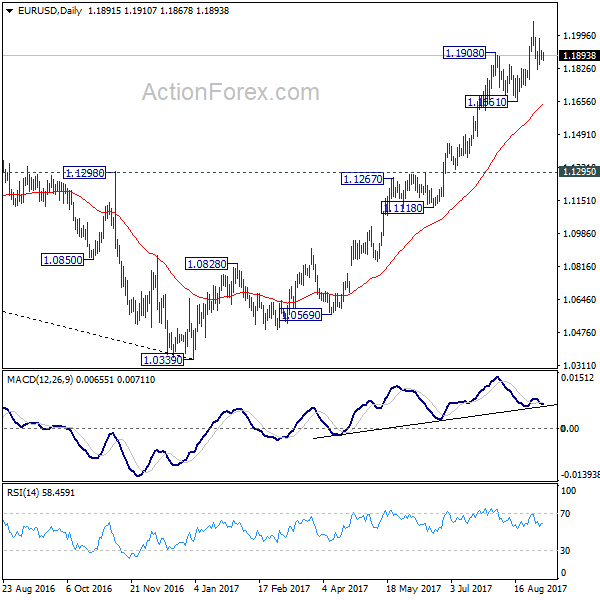

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1868; (P) 1.1895 (R1) 1.1918; More...

EUR/USD is staying in consolidation from 1.2069 and intraday bias remains neutral. Below 1.1822 will bring deeper fall. But after all, there is no clear sign of trend reversal yet. Outlook will remain bullish as long as 1.1661 holds. Break of 1.2069 will extend larger rise from 1.0339 to next key fibonacci level at 1.2516. Nonetheless, break of 1.1661 will bring much lengthier consolidation first.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1774) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.