Sample Category Title

USDJPY Analysis: Stops At 109.92

The way the currency rate moved yesterday completely matched with expectations. Due to absence of any additional stimulus, the buck continued to lose value against the Yen up until the weekly R1 at 109.92. The pair made a few attempts to break to the bottom but failed. For today, projection remains approximately the same. The pair is not expected to resume a successful plunge, as the southern side remains reliably protected by the 100- and 200-hour SMAs as well as by the weekly and monthly PP. On the other hand, a release of the US employment data today at 12:30 GMT might alter this scenario and, in contrast, help the buck to surge towards the weekly R3 at 111.13.

GBPUSD Analysis: Rebounds From Weekly R1 At 1.2942

As it was projected, in the first half of the previous trading day the currency rate had easily plunged to the weekly PP at 1.2858, using barrier-free area on its way. However, by the end of the day the Pound has already managed to restore all lost positions and confirmed an existence of junior descending channel. As a result, today the exchange rate is expected to keep moving in the southern direction in an attempt to reach the 200-hour SMA near 1.2858. However, there is a need to remember that release of information on the UK Manufacturing PMI as well as the US Average Hourly Earnings and Non-Farm Employment Change might significantly alter the above scenario, depending on the result.

EURUSD Analysis: Makes An Expected Rebound

In line with expectations, yesterday the buck relentlessly tried to break though the combined support level formed by the monthly PP, the 200-hour SMA and the ascending channel's bottom boundary. As it was suspected, it managed to slightly overstep beyond the barrier. However, the downside momentum was not strong enough to fix the result. Today the pair is expected to make one more unsuccessful attempt to slip to the bottom. The only difference is that this time the southern side will be additionally secured by the weekly PP at 1.1881. Similarly to the previous trading day, it might break to the bottom. But, in any case, the fall is not expected to go below the 1.1840-50 mark, as it represents a location of the dominant ascending channel's lower trend-line.

EUR/USD: Pending Home Sales

The EUR/USD currency pair confirmed an upward trend on Thursday, as the US economic reports failed to provide sufficient support for the Greenback. The Euro gained 0.17% against the US Dollar to continue a side move above the 1.1890 mark until the Friday morning session. The National Association of Realtors revealed that pending home sales in the United States fell 0.8% over the month of July, as the property market kept facing hurdles form a limited supply of available houses, which pushed prices up. The report suggested that sales would not break out in the coming months, as inventories are unlikely to improve significantly, while higher property prices are set to continue outpacing wage growth further, causing more strains on first-time buyers.

USD/CAD: Canadian Gross Domestic Product

The Canadian Dollar strengthened significantly against its American counterpart as the GDP report showed stronger-than-anticipated figures. The USD/CAD pair dropped by 83 base points or 66% to reach the 1.2568 level and continued its gradual decline. Statistics Canada announced that the country's GDP expanded at a 4.5% annualised pace in the June quarter, beating forecasts for a 3.7% increase. The main contributors to growth were broad-based increases in consumer spending, exports and business investment. Strong figures marked Canada as the best performer amongst the G7, suggesting higher chances that the Bank of Canada would continue to raise key interest rate this year.

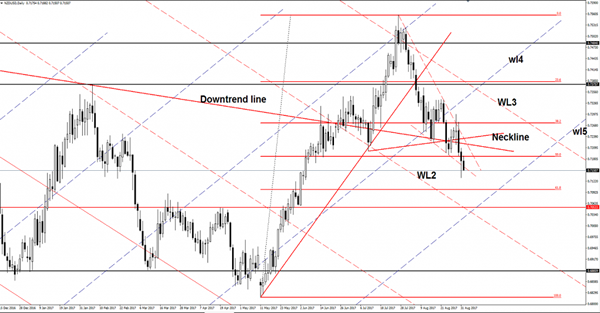

EUR/CHF Stands On Thin Ice

EUR/CHF posted little gains today and tries to stay in the buyer’s territory, but I don’t know if will be possible after the false breakout above the WL4. Has come down to retest the WL2 and maintains a bullish bias as long as stays above this level. Will increase further only if will stabilize above the WL4 and if it will retest the upper median line (uml) of te minor ascending pitchfork.

NZD/USD Stabilized In The Red Zone

Price is trading in the red and tries to resume the corrective phase. Price squeezed a little in the US session and recovered after the massive drop. NZD/USD is trading near the 0.7150 level and looks determined to breakdown below the down sloping line (dotted line), which will confirm a further drop. Technically is expected to drop more than 300 pips after the breakdown below the Head and Shoulders neckline.

USD/JPY Narrowing

USD/JPY increased a little today and tries to recover after the yesterday’s drop. Continues to move sideways on the short term, so is better to stay away until we’ll have a clear direction and a fresh trading signal. I believe that we’ll have a clear direction in the upcoming days as the United States data will have a big influence.

Price increased as the USD was driven higher by the USDX’s rebound, the index failed to reach the near term support from 92.55 and from 92.49 level. A USDX’s accumulation will signal a broader rebound, but we have to be patient to see what the US data will bring in the afternoon.

The USD will dominate the currency market again if the United States will impress later, but I want to remind you that another disappointment will ruin any upside perspective.

Price continues to be trapped between the 23.6% and the 50% Fibonacci levels, has broken above the warning line (wl1), but this could be a false breakout. Is pressuring the warning line (wl1), but technically seems too overbought to resume the upside movement and could drop towards the 50% retracement level again.

The United States data will shake the markets, not only the USD/JPY pair, you should be careful because this will be a crucial day for the greenback. Some good numbers will force the FED to think at another rate hike till the end of the year.

Dollar Ticks Up In Asia Ahead Of NFP, Aussie Weaker Ahead Of Busy Week

With geopolitical risks remaining in the background and the tropical Storm Harvey devastating the Southern US, the dollar managed to reverse some of yesterday’s losses during the Asian session. Investors were also forming their predictions for the widely expected nonfarm payrolls released later today. The aussie posted short-lived gains during today’s trading after AIG manufacturing index and the Chinese Caixin came in better than expected.

Following disappointing inflation and consumer spending readings published on Thursday as well as US Treasury Secretary Steven Mnuchin’s remarks which favored a lower currency, the dollar recovered slightly against its peers, with the dollar index edging up by 0.09% to 92.75.

Investors will now wait for the closely watched nonfarm payrolls to be published later today after the private survey ADP showed that the private sector added 237,000 jobs compared to 185,000 expected. In contrast, forecasts for nonfarm payrolls are for them to increase by 180,000, below the previous mark of 209,000.

Moreover, Trump’s trade negotiations team will meet with the Canadian and Mexican representatives in Mexico City to start the second round of NAFTA negotiations. Trump has threatened several times to quit the trade deal, as he believes that it harms the US trade terms and is unfair to American workers after the first round of talks led nowhere.

The yen retreated against the greenback after a sudden rise late on Thursday when renewed geopolitical risks led the currency higher. Particularly, South Korea and Japan participated in joint military exercises on Thursday, using U.S bombers above the Korean peninsula. Dollar/yen was slightly up today by 0.16% at 110.14.

The euro followed a negative path during the Asian trading, falling despite inflation figures released yesterday came in stronger than expected. The currency was trading weaker by 0.22% at 1.1881 as the ECB is expected to reduce asset purchases only gradually after expressing its concerns over a strengthening euro. Note that the ECB policy meeting will kick off next Thursday in Frankfurt.

The 'non-decisive ' progress in Brexit negotiations as it was characterized by the European Brexit negotiator, Michel Barnier yesterday, continued weighing on the pound today, driving the currency down by 0.12% at $1.2914.

Meanwhile, China and Australia released their Manufacturing activity surveys for the month of August. The Chinese Caixin manufacturing PMI increased by 0.5 points to 51.6, while analysts projected the indicator to decline to 50.9. The Australian Industry Group (AIG) manufacturing index also improved, rising to 59.8 from 56 seen in the previous month.

The above data supported the aussie overnight. However, the currency could not sustain its gains afterwards. Dollar/aussie rose from a closing price of 0.7944 yesterday to a session high of 0.7955 before it sunk to 0.7933. This comes ahead of a busy calendar next week for the aussie as a bunch of data will be released, including inflation and GDP growth numbers, while the RBA is also expected to decide on interest rates on Tuesday.

The kiwi fell by 0.31% to $0.7156 as terms of trade in the second quarter published early in the Asian session grow less than expected. The figure decreased from 8% in the previous quarter to 2.4%, missing the expectations of 3%.

Looking at commodities, oil prices were down despite the disastrous tropical storm Harvey, which caused key refineries and other energy facilities in Texas to shut down, including the Colonial pipeline which is the country’s largest energy supply system. WTI crude fell by 1% to $46.76 while Brent was down by 0.61% at $52.54. Gold dropped by 0.25% to $1318.58 per ounce.

US Inflation Data Disappoints

Thursday saw the release, by the US Department of Labor, of Weekly Jobless Claims that came in in-line with expectations at 236K, underscoring a strong labor market. More importantly, US Core Consumption Expenditure came in at 1.4% annualized, decreasing from the previous release of 1.5%. As the preferred measure of inflation, it is drastically lower than the Fed's target of 2%. USD held steady on the back of these releases but was put under downward pressure on comments from US Treasury Secretary Munchin who said a weaker currency is “somewhat better” for trade.

With Tropical Storm Harvey causing the closure of several key gasoline pipelines, the price of Gasoline has risen by more than 10 cents compared to a week ago. This increase is likely to result in a higher Consumption Expenditure in September but the increase is likely to be short lived as the Gulf States rebuild.

Markets will be focusing on today's Nonfarm Payroll, Unemployment and, more importantly, Average Earnings releases to gauge the strength of the US economy. The Nonfarm Payroll report is the last before the next FOMC policy meeting and is likely to determine the timing of the Fed's next rate hike.

EURUSD was little changed overnight, currently trading around 1.1890.

USDJPY is currently trading near to Friday's high around 110.14.

GBPUSD is currently trading towards the day's low around 1.2915.

Gold recovered from recent losses, trading as high as $1,321.98 in early trading. With tensions simmering between the US & North Korea the markets appear to be entering the traditional safe haven that is Gold. Currently, Gold is trading around $1,320.

WTI will continue to be influenced by the devastation caused in the US by Tropical Storm Harvey. Estimates suggest that the closure of many refineries has resulted in the loss of 4.4 million barrels a day of refining capacity. With refining being affected more than production WTI continues to see downward pressure and currently trades around $47.35pb.

At 13:30 BST, the US Department of Labor releases; Nonfarm Payrolls, Average Hourly Earnings (MoM & YoY) and Unemployment for August. The recent positive trend in NFP releases continued in July with 209,000 new positions added which helped reduce the unemployment rate to 4.3%. NFP for August, per market consensus, is expected to come in at 180,000, underscoring a strong US Labour Market. The markets will also be closely watching the Average Hourly Earnings release with many hoping to see an improvement on the previous two readings of 2.5%. Average earnings need to increase for consumer spending to rise, which will then help increase inflationary pressure. Analysis indicates that the market-implied probability that the Fed raises rates by year-end is around 30%. Fed funds futures are not fully pricing in another 0.25% rate hike until September 2018.