Sample Category Title

Trade Idea: AUD/USD – Stopped profit and stand aside

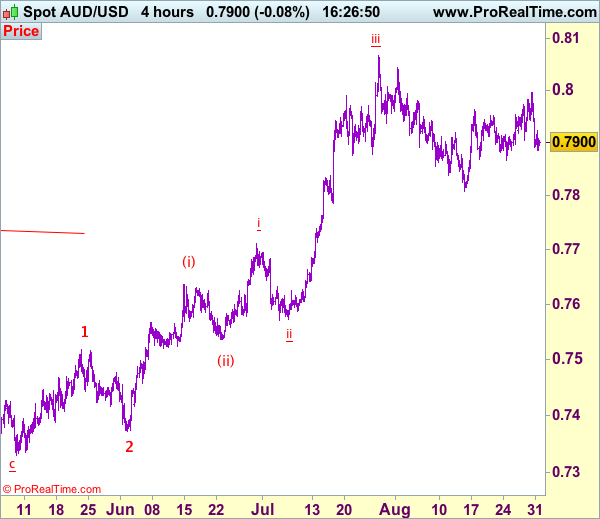

AUD/USD – 0.7999

Original strategy :

Bought at 0.7895, stopped profit at 0.7900

Position: - Long at 0.7895

Target: -

Stop: - 0.7900

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Aussie’s retreat from 0.7996 turned out to be much deeper than expected, dampening our bullishness and further consolidation would take place, near term downside risk remains for weakness to 0.7865-57, however, break there is needed to suggest the rebound from 0.7808 has ended instead, bring another leg of corrective decline towards this level later. Below 0.7808 would signal the wave iv correction from 0.8066 is still in progress for weakness to 0.7786 support, however, oversold condition should prevent sharp fall below 0.7750 and price should stay above i top at 0.7712, bring rebound later. We are keeping our latest bullish count that recent impulsive waves is unfolding as (1 2, (i)(ii), i ii) and may extend headway towards 0.8150.

In view of this, would be prudent to stand aside in the meantime. Above 0.7925-30 would bring another corrective bounce to 0.7950-60, however, said resistance at 0.7996 should hold, bring further choppy trading. Only above 0.7996-0.8000 would revive bullishness and signal the pullback from 0.8066 has ended, bring subsequent retest of this level.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

USDJPY Intraday Analysis

USDJPY (110.53): The USDJPY is seen making strong gains for what could be a third consecutive day. This comes after price retested the support level near 109.15 - 108.26. The resistance at 110.72 is now in focus, and we could expect theprice to struggle to breakout above this level. Therefore, a near-term decline could be expected. Support is seen coming in at 109.75 which previously served as minor resistance. A retest back to this level to establish support will validate the upside with USDJPY likely to break past 110.72 followed by a potential rally towards 113.00.

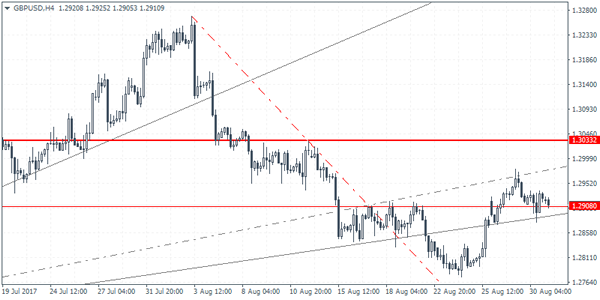

GBPUSD Intraday Analysis

GBPUSD (1.2910): The British pound managed to maintain some gains in yesterdays trading. Price action remains flat at the moment, but the medium-term bullish momentum could push GBPUSD further to the upside. The resistance level of 1.3033 could be the near-term test for the currency pair. For the moment, GBPUSD is seen retesting the support level at 1.2908. As long as this support holds, we can expect to see some near term gains. Thisis also validated by the fact that GBPUSD managed to break past the falling trend line and the previously held support level is now the prime target for resistance to be established.

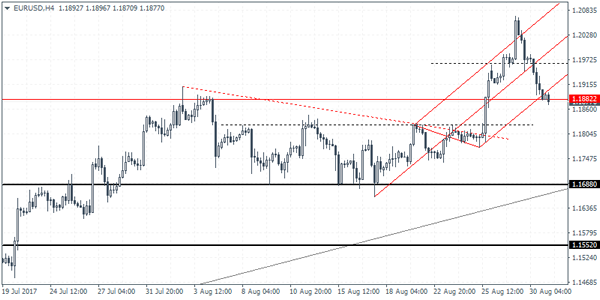

EURUSD Intraday Analysis

EURUSD (1.1877): The EURUSD extended the declines yesterday with price action falling to test the first support level at 1.1882. Further declines could see the common currency falling to the next main resistance level at 1.1825. A rebound off either of these two levels is quite possible which could see some near-term upside in prices. However, watch for a lower high being formed as a result of this bounce which could signal the start of the correction towards 1.1688. Resistance can be seen forming around 1.1963 which could see a near term reversal. EURUSD could potentially stay range bound within these levels following which a breakout trade might occur. To the upside, above 1.1963, further gains could push EURUSD past the 1.20 handle, while to the downside we expect a test of 1.1688.

US Dollar Gains On ADP Report And GDP Revisions

The greenback posted strong gains, rising on the back of a better than expected private payrolls report and a revised second quarter GDP. Official data showed yesterday that private sector hiring in the US added 237k jobs. This was higher than the forecasts of 185k while July's private payrolls were revised up to 201k. The second quarter GDP report showed that the US economy expanded at a pace of 3%, beating estimates of 2.7% and better than the initial reading of 2.6%.

Looking ahead, the economic calendar today covers the preliminary CPI from France, followed by the Eurozone's CPI data. Headline inflation is expected to accelerate 1.4%, after rising 1.3% in July. Core CPI is however forecast to remain steady at 1.2%. In the US the core PCE data will be coming out later. Forecasts point to a 0.1% increase on a month over month basis.

EURUSD Analysis: Plunges To 1.18

As it was expected, during the whole previous trading day the currency exchange rate was moving in ascending channel. At the moment, it is approaching a combined support level formed by the weekly PP at 1.1865 and the 200-hour SMA.

A rebound is expected to happen even if the rate will manage to slightly overstep beyond that barrier. One of the reasons is that a little bit lower there is located a bottom boundary of a large ascending channel that guides movement of the pair. The second reason is that there will be no notable data releases today. This means that the buck will not get any additional impulse from traders, anticipating these events (as it happened during the last couple of days).

GBPUSD Analysis: Trades In A Limbo

In line with expectations, yesterday the exchange rate continued to move towards the 100-hour SMA amid a pressure from a combination of the weekly R1 and the monthly S1 as well as from release of the US macroeconomic data. At the moment, the pair is remaining in a limbo between these support and resistance levels.

Most probably, the Pound will continue to try to sneak to the top, using a silent day for its counterpart. On the other hand, the further fall towards the 1.28 mark seems a more reasonable path, as it contains a lot of free space until the 200-hour SMA near 1.2872. Nevertheless, a summary of technical indicators vote in favour of the surge, sending a strong buy signal.

USDJPY Analysis: Breaks From Ascending Channel

Fortunately for the buck, both data releases were even better that analysts anticipated. Even though they did not arouse especially high interest, but it was still enough to push the currency pair out of the channel. The surge gradually continued until the pair faced the first resistance level set up by the weekly R2 at 110.49. Contrary to the previous three days, today the Dollar will not have any additional stimulus from the fundamental side. Accordingly, the pair is likely to retreat back to the weekly R1 at 109.92. Yet, the sharp fall is not expected, as the southern side is reliably secured by the 55-, 100- and 200-hour SMAs. However an opposite scenario is likely to happen as well, an aggregate of technical indicators sends a strong buy signal for the 5H and 1D timeframes.

XAUUSD Analysis: Slips To 1,303.75

Yesterday the American Dollar continued to strengthen against the yellow metal and even managed to form a little descending triangle, whose lower support line matched with the upper boundary of a former long-term ascending channel.

In the early Thursday morning the bullion lost another 0.33% and slipped below the 100-hour SMA. On the one hand, a forming downtrend suggests that the plunge can continue at least until the 200-hour SMA near 1,295.80. On the other hand, over the last three days appreciation of the buck was mainly driven by various fundamental events. In contrast, today there will be no significant data releases that could give the Dollar a necessary impulse for the further surge.

EUR/USD: Prelim GDP

The Euro lost against the US Dollar 14 base points, following Wednesday's report showing the second estimate for the US economic growth. The EUR/USD dropped to the 1.1950 mark and retreated back initially, though the downward trend was sustained to see the pair returning to the last Friday levels by the morning session on Thursday.

The Commerce Department reported that the US economy expanded at a faster-than-expected yearly pace of 3.0% in the Q2. The country's GDP growth marked the strongest reading in more than two years, nearing Donald Trump's target. A rise was led by higher consumer spending and business investment, which could be further translated into a stronger path in the Q3 to dampen possible effects of Hurricane Harvey.