Sample Category Title

Focus Remains On Euro Area Inflation In August

Market movers today

Focus remains on euro area inflation in August . Yesterday's German and Spanish figures were both higher than expected but the upside surprise was driven mainly by energy price inflation and the higher inflation should not alter the ECB's current view on its monetary policy strategy. We have revised our euro area headline inflation forecast slightly higher to 1.5% y/y in August but still believe core inflation will move in the opposite direct ion and decline to 1.1% y/y in August . As we have argued previously, the stronger euro will become a headwind to inflation in 2018 and 2019,

Euro area and German unemployment rate figures are also due for release today. Both figures have declined over the past years and the German unemployment rate is very low in a historical perspective. This has been one factor supporting consumer sentiment , which is at the highest level in more than 15 years. The ongoing strong economic situation in Germany bodes well for Angela Merkel in the upcoming election. See more about the possible outcome at the election in German Election Monitor No. 1: Next euro area election unlikely to rock the boat, 29 August 2017.

US inflation figures will at tract attention in the afternoon with the release of the PCE figure. The decline in PCE core inflation in the first half of this year has sparked some concern about lack of inflation pressure within the Fed. Nevertheless, the Fed has said quantitative tightening will begin ‘relatively soon' and we expect it to be announced in September. The Fed getting ready to pull the trigger on quantitative tightening means USD liquidity could start to become scarce from Q4.

Selected market news

Overnight , Chinese PMI manufacturing rose to 51.7 in August from 51.4 in July against the expectations of a drop. This adds to the perception that the world economy is in good shape, as euro area growth is strong at the moment and US Q2 GDP growth was revised up to 3.0% from 2.6% yesterday.

The Trump administration seems divided on the North Korea situation. While President Trump tweeted yesterday that ‘talking is not the answer', Defense Secretary James Matt is said that the US is still trying to find a diplomatic solution. The administration is expected to brief the Senate on the situation next week. For more on the North Korea crisis see Flash Comment: Another wave of escalation in North Korean crisis, 29 August 2017.

Bloomberg has an excellent overview of why the Brexit negotiations are progressing slowly (the third round is taking place this week). While the EU says the UK needs to clarify its positions, the UK accuses the EU for not being flexible enough. While it seems unlikely that the first phase of the negotiations can be concluded before the EU summit in October, one has to take into account that it is normal for political negotiations to progress slowly until close to midnight

Australia’s HIA New Home Sales Dropped In July

For the 24 hours to 23:00 GMT, the AUD declined 0.63% against the USD and closed at 0.7905.

LME Copper prices declined 0.6% or $42.0/MT to $6755.0/MT. Aluminium prices declined 1.2% or $25.5/MT to $2066.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7907, with the AUD trading a tad higher against the USD from yesterday's close.

Earlier today, data indicated that Australia's HIA new home sales eased 3.7% on a monthly basis in July. New home sales had registered a drop of 6.9% in the previous month. On the contrary, the nation's private sector credit registered a rise of 0.5% on a monthly basis in July, meeting market expectations. The private sector credit had climbed 0.6% in the prior month.

Elsewhere in China, Australia's largest trading partner, the NBS manufacturing PMI unexpectedly advanced to a level of 51.7 in August, defying market consensus for a fall to a level of 51.3. The PMI had registered a reading of 51.4 in the prior month. On the other hand, the nation's non-manufacturing PMI recorded a drop to a level of 53.4 in August, following a reading of 54.5 in the previous month.

The pair is expected to find support at 0.7864, and a fall through could take it to the next support level of 0.7821. The pair is expected to find its first resistance at 0.7973, and a rise through could take it to the next resistance level of 0.8039.

Going ahead, traders will focus on Australia's AiG performance of manufacturing index for August, slated to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

German Inflation Advanced As Expected In August

For the 24 hours to 23:00 GMT, the EUR declined 0.66% against the USD and closed at 1.1896.

Macroeconomic data indicated that the Euro-zone's economic confidence index unexpectedly advanced to a level of 111.9 in August, hitting its highest level since July 2007, propelled by higher optimism among industrial and the services sector. Market participants had expected the index to remain unchanged at a revised level of 111.3. Further, the region's final consumer confidence index improved to a level of -1.5 in August, in line with the flash estimate. The index had recorded a level of -1.7 in the prior month.

Separately, Germany's flash consumer price index (CPI) climbed 1.8% on an annual basis in August, meeting market expectations and compared to a rise of 1.7% in the prior month.

Meanwhile, rating agency, Moody's upgraded Euro-zone's growth forecast for 2017, citing robust momentum across the Euro-bloc. The agency now expects economic growth across the common currency region to hit 2.1% this year, revised up from its earlier forecast of 1.7%.

The greenback gained ground against its key counterparts, following the release of a pair of upbeat economic data.

The second estimate of annualised gross domestic product (GDP) in the US was revised sharply higher to 3.0% in the second quarter of 2017, expanding at its fastest pace in more than two years. The preliminary figures had indicated an advance of 2.6%, while market participants had envisaged for an expansion of 2.7%. In the previous quarter, GDP had posted a revised rise of 1.2%.

Other data showed that ADP's private sector employment in the US increased more-than-expected by 237.0K in August, rising at its fastest pace in five months and boosting optimism over the state of the nation's labour market. ADP's private sector employment rose by a revised 201.0K in the prior month, while markets had anticipated for a rise of 185.0K. On the contrary, the nation's MBA mortgage applications fell 2.3% in the week ended 25 August 2017, after recording a drop of 0.5% in the prior week.

Meanwhile, Moody's slashed US growth forecasts for this year and next, stating that the economy disappointed with a weaker performance in the first half of this year. The agency trimmed 2017 growth forecast from 2.4% to 2.2% and cut forecast for 2018 to 2.3% from 2.5% predicted earlier.

In the Asian session, at GMT0300, the pair is trading at 1.1878, with the EUR trading 0.15% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1839, and a fall through could take it to the next support level of 1.1799. The pair is expected to find its first resistance at 1.1951, and a rise through could take it to the next resistance level of 1.2023.

Trading trend in the Euro today is expected to be determined by the release of the Euro-zone's flash consumer price inflation for August as well as Germany's retail sales for July and unemployment rate for August, all scheduled to release in a few hours. Additionally, the US pending home sales, personal income as well as spending data, all for July coupled with the nation's initial jobless claims data, all set to release later in the day, will pique significant amount of investor attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s Mortgage Approvals Surged A 16-Month High In July, While Consumer Credit Grew At Its Weakest Pace This Year...

For the 24 hours to 23:00 GMT, the GBP marginally declined against the USD and closed at 1.2922.

On the data front, Britain's mortgage approvals for house purchases jumped to a sixteen-month high level of 68.7K in July, offering tentative signs that the nation's housing market could be picking up. In the prior month, number of mortgage approvals for house purchases had registered a revised reading of 65.3K, while investors had expected for an advance to a level of 65.5K. Meanwhile, the nation's net consumer credit rose less-than-anticipated by £1.2 billion in July, rising at its weakest pace in seven months and compared to a revised advance of £1.4 billion in the previous month. Markets were expecting net consumer credit to increase by £1.5 billion.

In the Asian session, at GMT0300, the pair is trading at 1.2911, with the GBP trading 0.09% lower against the USD from yesterday's close.

Overnight data showed that the nation's GfK consumer confidence unexpectedly improved to a level of -10.0 in August, despite gloomier economic outlook. The index had registered a reading of -12.0 in the prior month, while market participants had envisaged it to ease to a level of -13.0.

The pair is expected to find support at 1.2881, and a fall through could take it to the next support level of 1.2850. The pair is expected to find its first resistance at 1.2940, and a rise through could take it to the next resistance level of 1.2968.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japanese Industrial Production Deteriorated In July

For the 24 hours to 23:00 GMT, the USD rose 0.68% against the JPY and closed at 110.34.

In economic news, data indicated that Japan's small business confidence index registered a drop to a level of 49.0 in August, compared to a level of 50.0 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 110.52, with the USD trading 0.16% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's flash industrial production slid 0.8% MoM in July, more than market expectations for a drop of 0.3%. Industrial production had recorded a rise of 2.2% in the previous month.

The pair is expected to find support at 109.92, and a fall through could take it to the next support level of 109.33. The pair is expected to find its first resistance at 110.86, and a rise through could take it to the next resistance level of 111.21.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Switzerland’s ZEW Economic Expectations Index Fell In August

For the 24 hours to 23:00 GMT, the USD rose 0.89% against the CHF and closed at 0.9632.

On the macro front, Switzerland's ZEW economic expectations index fell to a level of 25.0 in August, compared to a reading of 34.70 in the previous month. Further, the nation's KOF leading indicator eased to a level of 104.1 in August, compared to market consensus for a drop to a level of 107.0. In the previous month, the index had registered a revised reading of 108.0.

On the other hand, the nation's UBS consumption indicator rose to a level of 1.38 in July, compared to a revised level of 1.30 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 0.9640, with the USD trading 0.08% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9571, and a fall through could take it to the next support level of 0.9501. The pair is expected to find its first resistance at 0.9678, and a rise through could take it to the next resistance level of 0.9715.

Amid no macroeconomic releases in the Switzerland today, investor sentiment will be determined by global macroeconomic events.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading On A Weaker Footing, Ahead Of Canada’s GDP Data

For the 24 hours to 23:00 GMT, the USD rose 0.9% against the CAD and closed at 1.2623.

In the Asian session, at GMT0300, the pair is trading at 1.2644, with the USD trading 0.17% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2546, and a fall through could take it to the next support level of 1.2448. The pair is expected to find its first resistance at 1.2697, and a rise through could take it to the next resistance level of 1.2750.

Ahead in the day, market participants will closely monitor Canada's crucial GDP figures for June.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Oil Bounces As Harvey Weakens, Currency Trends May Have Passed A Tipping Point

Dollar Lifts On Positive Economic Data. The latest batch of U.S. data turned out better than expected, reviving some hope for another Fed rate hike in the coming months. The greenback gained a lift after the Commerce Department said on Wednesday that its second estimate of U.S. gross domestic product showed that the economy grew at an annual 3.0 percent annual in the second quarter, the quickest in more than two years. In addition, the ADP National Employment Report showed U.S. private-sector employers hired 237,000 workers in August for the biggest monthly increase in five months, driving expectations for a solid U.S. August non-farm payrolls figure. In the wake of such solid economic indicators, market expectations for the chances of a Fed rate hike in December may start to increase and support the dollar.

Sterling Might Have To Fall Further. The pound continued to slay during the U.S. trading session as traders unwound their Brexit shorts and picked up on stronger risk-on vibes.

Dollar Edges Higher Vs Yen. The dollar and yen were back in the winners’ circle as both lower-yielding currencies managed to end positive for the session. The dollar hit a two-week high versus the yen on Thursday, extending its gains after strong U.S. economic data bolstered expectations for a solid U.S. jobs report later this week. The dollar rose to as high as 110.545 yen, its strongest level since Aug. 16. It last changed hands at 110.51 yen, up 0.2 percent from late U.S. trade on Wednesday.

Euro Nurses Losses After 0.7 Pct Drop On Wednesday. The euro nursed its wounds after falling 0.7 percent against the dollar on Wednesday in its biggest daily percentage drop against the dollar in nearly four weeks. The euro edged up 0.1 percent on the day to $1.1890, having retreated from a more than 2-1/2 year high of $1.2070 set on Tuesday.

Gold Retreats As GDP Growth Revised Up. Commodities failed to hold on to their winnings, with precious metals giving up some of their previous safe-haven gains. Gold prices fell following the release of better-than-expected second quarter GDP data.

Gasoline Rallies, Oil Ends At A More-Than-1-Month Low. The improvement in risk appetite, combined with the weakening tropical storm Harvey and a larger than expected draw in crude oil stockpiles, boosted Black Crack prices. The hurricane making landfall again in Louisiana this time and reports that refineries farther west could reopen soon knocked the prices of crude and gasoline back a bit. Traders should note that news related to ports and pipelines reopening may also influence trading going forward.

Watch Out For:

08:00 am GMT: EUR Unemployment Data

09:00 am GMT: EUR Consumer Price Index

12:30 am GMT: USD Personal Consumption Expenditure

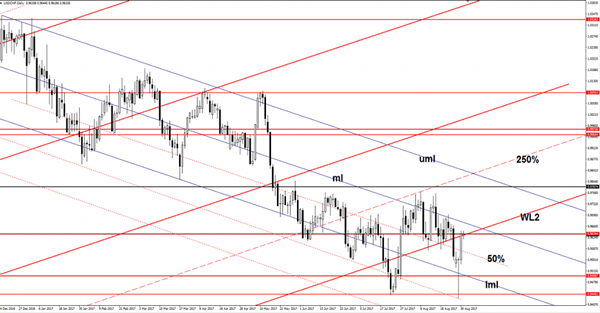

USD/CHF Registered An Amazing Jump

Price is moving in a range on the Daily chart, but looks like that is poised for an upside move. The Tuesday’s candle suggests a reversal, but we still need confirmation before we can take action again. Only a valid breakout above the 0.9634 and most important above the median line (ml) will confirm a further increase towards the upper median line (uml).

USD/JPY In The Buyers Territory

USD/JPY rallied and extended the upside movement, a retest of the warning line (wl1) will confirm a further increase. Continues to move in range on the daily chart, we’ll have a clear direction once we’ll have a valid breakout from this extended sideways movement.

The next upside target will be at the confluence area formed between the 38.2% retracement level with the WL3