Sample Category Title

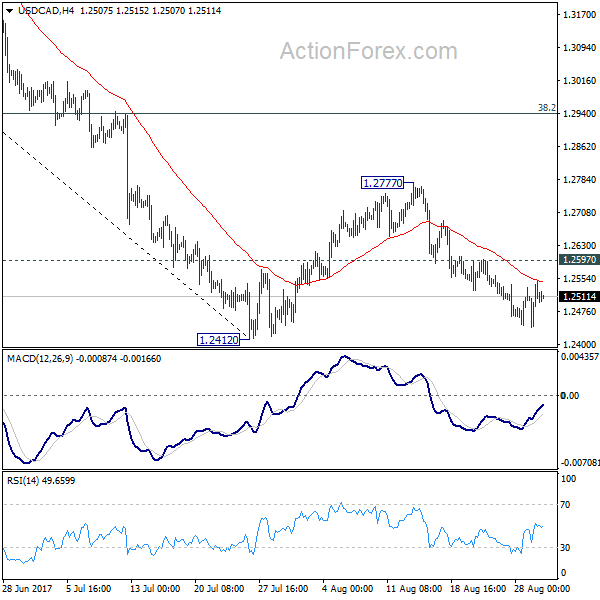

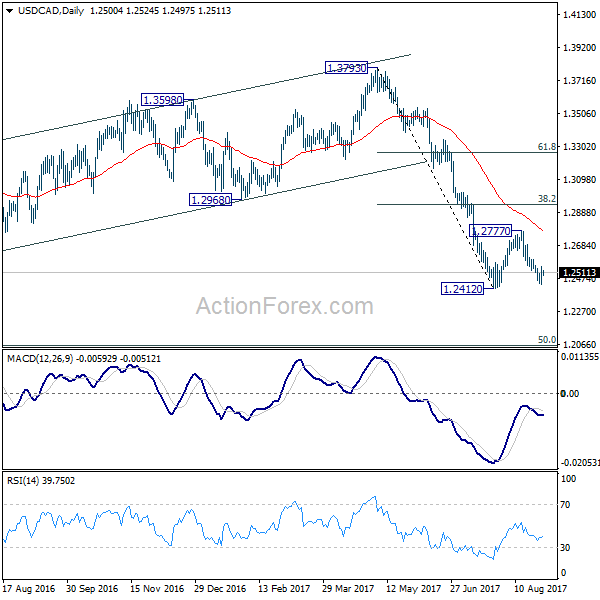

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2449; (P) 1.2500; (R1) 1.2559; More....

Intraday bias in USD/CAD stays neutral for the moment. On the downside, break of 1.2412 will resume recent fall from 1.3793 and target next long term fibonacci level at 1.2048. On the upside, above 1.2597 minor resistance will extend the consolidation from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

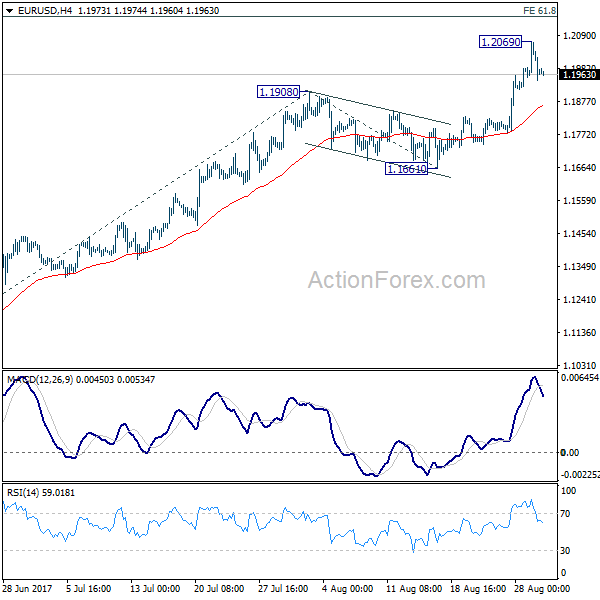

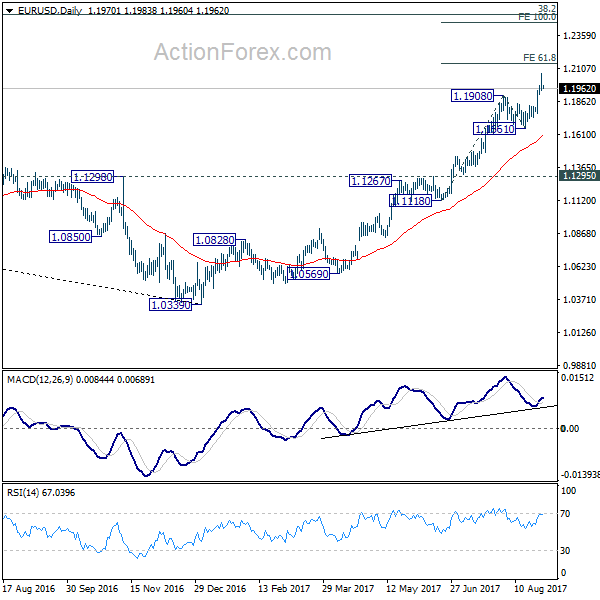

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1921; (P) 1.1996 (R1) 1.2046; More...

A temporary top is in place at 1.2069 and intraday bias is turned neutral first. Some consolidations would be seen but downside should be contained well above 1.1661 support to bring rise resumption. Above 1.2069 will extend the whole rally from 1.0339 to 61.8% projection of 1.1118 to 1.1908 from 1.1661 at 1.2149 first. Break there will target 100% projection at 1.2451 next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

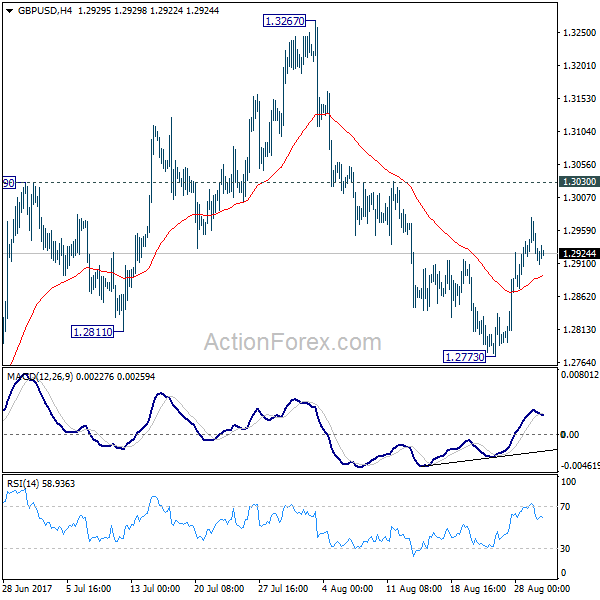

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2895; (P) 1.2937; (R1) 1.2959; More...

Intraday bias in GBP/USD remains neural for the moment as it's staying in consolidative trading in range of 1.2773/3030. We're favoring the case that correction from 1.1946 is completed at 1.3267. Below 1.2773 will target 1.2588 key near term support first. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. Though, break of 1.3030 will dampen this bearish view and turn bias back to the upside for retesting 1.3267.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

European Open Briefing: Asia-Pacific Equity Markets Rebounded

Global Markets:

- Asian stock markets: Nikkei up 0.70 %, Shanghai Composite rose 0.02 %, Hang Seng climbed 0.92 %, ASX 200 up 0.02 %

- Commodities: Gold at $1317.33 (-0.10 %), Silver at $17.42 (+0.07 %), WTI Oil at $46.31 (-0.28 %), Brent Oil at $51.45 (-0.41 %)

- Rates: US 10-year yield at 2.14, UK 10-year yield at 1.00, German 10-year yield at 0.34

News & Data:

- AUD Building Approvals m/m -1.7 % vs -5.4 % expected

- AUD Construction Work Done q/q 9.3 % vs 0.9 % expected

- USD CB Consumer Confidence 122.9 vs 120.9 expected

- EUR GfK German Consumer Climate 10.9 vs 10.8 expected

- GBP Nationwide HPI -0.1 % vs 0.0 % expected

- EUR French GDP (QoQ) 0.5 % vs 0.5 % expected

- CAD RMPI m/m -0.6 % vs -0.2 % expected

- NZD Building Consents (MoM) -0.7 % vs -1.3% previous

- U.S. consumer confidence hits five-month high; house prices rise- RTRS

- Crude dips, gasoline spikes as floods knock out one-fifth of U.S. refineries- RTRS

Markets Update:

Asia-Pacific equity markets rebounded after selling off a day earlier following North Korea's latest missile launch. The Global investors returned to investing in risk assets as fear of further escalation receded after President Donald Trump's measured response.

USDJPY is currently seen trading around 109.90 as the dollar rose 0.1 percent against the Yen today, making the overall rise to 0.5 percent against the Yen. The pair after having spent the early hours of Wednesday under 109.60 from its late US high, started its steady march back up again as Tokyo got active.

EURUSD continued to be steady albeit not much changed in the Asian session on Wednesday. The Euro is currently trading around 1.1980 against the US Dollar after reaching highs of over 1.2060 after almost 3 years. The dollar index. DXY, which tracks the greenback against a basket of six major peers, edged up 0.1 percent to 92.317.

AUDUSD jumped 0.5 percent to 0.7996 early on Wednesday with building approvals numbers coming in better than expected and most importantly the Q2 construction work data showing a huge improvement to 9.3 % on the quarter, quite the surge from the expected 0.9 %. On the other hand, Reserve Bank of New Zealand Governor Wheeler's speech made the NZD drop from above 0.7260 to around 0.7230 very quickly and then bouncing back to around 0.7260 where the kiwi is currently seen trading

Upcoming Events:

- (EUR) German Prelim CPI m/m

- 07:00 GMT – (CHF) KOF Economic Barometer

- 07:00 GMT – (EUR) Spanish Flash CPI y/y

- 08:30 GMT – (GBP) Net Lending to Individuals m/m

- 12:15 GMT – (USD) ADP Non-Farm Employment Change

- 12:30 GMT – (CAD) Current Account

- 12:30 GMT – (USD) Prelim GDP q/q

- 13:15 GMT – (USD) FOMC Member Powell Speaks

- 14:30 GMT – (USD) Crude Oil Inventories

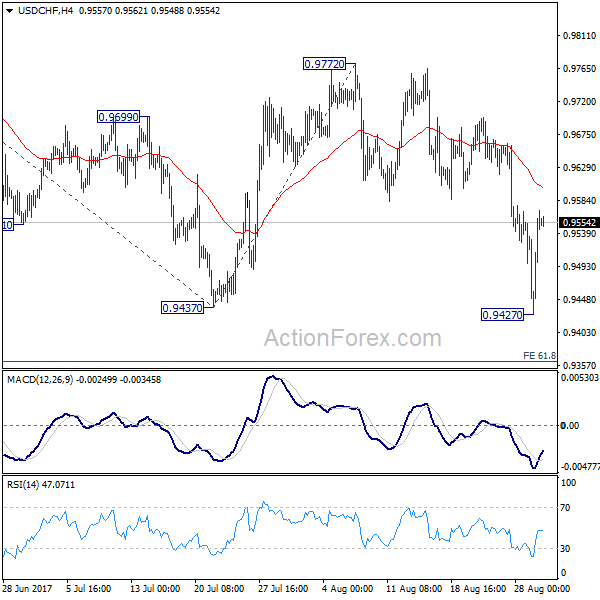

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9466; (P) 0.9513; (R1) 0.9599; More....

USD/CHF rebounded notably after hitting 0.9427 and intraday bias is turned neutral firm. Some consolidations would be seen and considering that it's close to 0.9443 key support, the rebound could extend higher. Still, break of 0.9772 resistance is needed to confirm near term reversal. Otherwise, outlook stays bearish for another decline. Break of 0.9427 will target 61.8% projection of 1.0099 to 0.9437 to 0.9772 at 0.9363.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090.

Crude Oil Continues To Slide As Storm Rages

Key Points:

- Crude oil supply glut worsens as tankers stuck offshore awaiting refinery openings.

- Meteorological data suggests storm could target Louisiana refinery area.

- Monitor the pending EIA Crude Oil Inventory figures which are due out shortly.

Crude oil prices have remained under pressure overnight as the ongoing damage from flooding in Texas, and the Gulf Coast, continues to wreak havoc amongst refineries. Subsequently, in what is being touted as potentially the most expensive of the decade, is severely impacting refinery operations throughout most of the U.S. In fact, if the rain and flooding continues to move as predicted, we could see further ramifications for gasoline production in the wider Southern regions. Subsequently, there could be further price declines for the black gold on the cards in the coming days.

Presently, WTI prices are trading around the $46.29 a barrel mark and are down around 1.17% for the prior day. However, what is potentially very interesting is the fact that oil and gasoline prices have diverged strongly as, due to the lack of refinery capacity, crude oil supplies continue to stack up. In fact, at last count there are currently 9 oil tankers offshore from Texas awaiting an opportunity to unload. Subsequently, the supply glut is likely to worsen as more tankers continue to arrive with little prospect of increased refinery operations in the near term.

In fact, prospective damage to the Gulf Coast refineries is yet to be assessed and it could be a significant period of time before they are again returned to full capacity. Additionally, many of the roads and infrastructure around these key supply points have been damaged and it remains uncertain as to what extent they will be able to be utilised to carry product. Subsequently, there still remains plenty of unknown factors and a rapid return to maximum production seems fairly unlikely.

Subsequently, the market could potentially be dealing with a significant crude oil supply glut for at least the next few weeks as both refinery and infrastructure damages are assessed and accounted for. Additionally, it would still take significant time to process the current crude oil stockpiles even if full capacity was returned rapidly. However, if the storm continues to move towards the Louisiana refineries, as met data seems to suggest, we could be in for a much deeper decline in crude oil prices.

Ultimately, WTI prices are likely to remain around the $46.00 handle in the coming days until further information is received on the status of the Texas based refineries and the surrounding infrastructure. However, monitor the EIA’s weekly oil inventory data because this could provide somewhat of a cushion to crudes bearishness if it shows a moderate draw.

Australia’s Building Approvals Declined In July

For the 24 hours to 23:00 GMT, the AUD rose 0.47% against the USD and closed at 0.7955.

LME Copper prices rose 1.2% or $83.0/MT to $6797.0/MT. Aluminium prices declined 0.2% or $4.5/MT to $2092.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7990, with the AUD trading 0.44% higher against the USD from yesterday's close.

Early morning data indicated that Australia's seasonally adjusted building approvals dropped less-than-anticipated by 1.7% on a monthly basis in July, compared to market consensus for a fall of 5.0%. In the prior month, building approvals had registered a rise of 10.9%.

On the other hand, the nation's seasonally adjusted construction work done sharply rebounded by 9.3% on a quarterly basis in 2Q 2017. In the prior quarter, construction work done had fallen by 0.7%.

The pair is expected to find support at 0.7943, and a fall through could take it to the next support level of 0.7895. The pair is expected to find its first resistance at 0.8017, and a rise through could take it to the next resistance level of 0.8043.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

German Consumer Confidence Unexpectedly Soared To Its Highest Level Since October 2001 In September

For the 24 hours to 23:00 GMT, the EUR rose 0.07% against the USD and closed at 1.1975, after data showed that Germany’s GfK consumer confidence index surprisingly jumped to a nearly sixteen-year high level of 10.9 in September, while markets expected the index to remain steady at a level of 10.8 registered in the previous month.

Macroeconomic data released in the US indicated that the CB consumer confidence index rose more-than-expected to a level of 122.9 in August, notching a five-month high level, as a healthy job market and optimism about current business conditions boosted investor sentiment. Meanwhile, market participants had envisaged the index to advance to a level of 120.7, following a revised reading of 120.0 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1976, with the EUR trading a tad higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1925, and a fall through could take it to the next support level of 1.1875. The pair is expected to find its first resistance at 1.2048, and a rise through could take it to the next resistance level of 1.2121.

Moving ahead, traders will look forward to the Euro-zone’s final consumer confidence and Germany’s flash consumer price inflation data, both for August, slated to release in a few hours. Moreover, the US 2Q annualised GDP and ADP employment change data for August, slated to release later today, will keep investors on their toes.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

UK’s Nationwide House Prices Surprisingly Fell In August

For the 24 hours to 23:00 GMT, the GBP slightly declined against the USD and closed at 1.2928.

On the macro front, Britain's seasonally adjusted Nationwide house prices recorded an unexpected drop of 0.1% on a monthly basis in August, compared to a revised advance of 0.2% in the prior month, while markets anticipated for a flat reading.

In the Asian session, at GMT0300, the pair is trading at 1.2926, with the GBP trading marginally lower from yesterday's close.

The pair is expected to find support at 1.2901, and a fall through could take it to the next support level of 1.2876. The pair is expected to find its first resistance at 1.2965, and a rise through could take it to the next resistance level of 1.3004.

Looking ahead, UK's net consumer credit and mortgage approvals data, both for July, set to release in a few hours, will garner a lot of market attention. Moreover, the nation's GfK consumer confidence for August, due to release overnight will also be eyed by traders.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Japanese Yen Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.87% against the JPY and closed at 109.60.

In the Asian session, at GMT0300, the pair is trading at 109.76, with the USD trading 0.15% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's retail trade advanced 1.1% MoM in July, compared to a gain of 0.2% in the previous month and beating market consensus for it to climb 0.3%. On the contrary, the nation's large retailers' sales dropped 0.2% on a monthly basis in July, at par with market expectations and after recording a rise of 0.2% in the previous month.

The pair is expected to find support at 108.71, and a fall through could take it to the next support level of 107.67. The pair is expected to find its first resistance at 110.36, and a rise through could take it to the next resistance level of 110.97.

Looking forward, investors will pay attention to Japan's flash industrial production data for July, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.