Sample Category Title

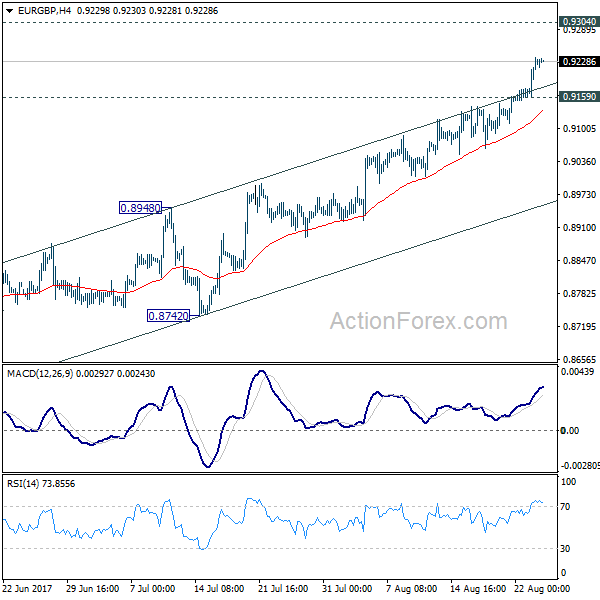

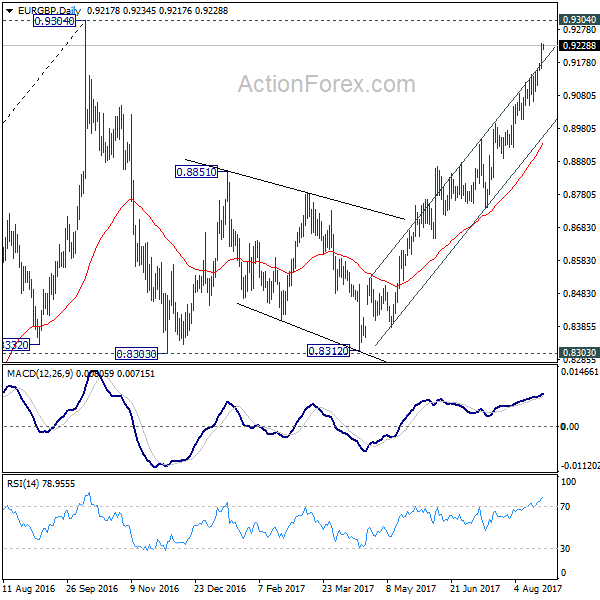

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.9177; (P) 0.9207; (R1) 0.9253; More

Intraday bias in EUR/GBP remains on the upside as rise from 0.8312 is in progress for testing 0.9304 high. At this point, there is still is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. But firm break of 0.9304 will confirm up trend resumption and pave the way to 0.9799. On the downside, below 0.9159 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes. In that case, 2008 high at 0.9799 will be the next target.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4873; (P) 1.4920; (R1) 1.4983; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the upside, above 1.5019 will resume the rise from 1.4421 and target a test on 1.5226 high. On the downside, below 1.4732 will extend the consolidation from 1.5226 with another fall. But we'd expect 1.4421 cluster support (50% retracement of 1.3624 to 1.5226 at 1.4427) to hold and bring rebound.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1376; (P) 1.1399; (R1) 1.1422; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 1.1537 is still in progress. On the upside, break of 1.1477 resistance will argue that the consolidation from 1.1537 has completed and larger rise is resuming. However, firm break of 38.2% retracement of 1.0830 to 1.1537 at 1.1267 will extend the correction to 61.8% retracement at 1.1100 before completion.

In the bigger picture, firm break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

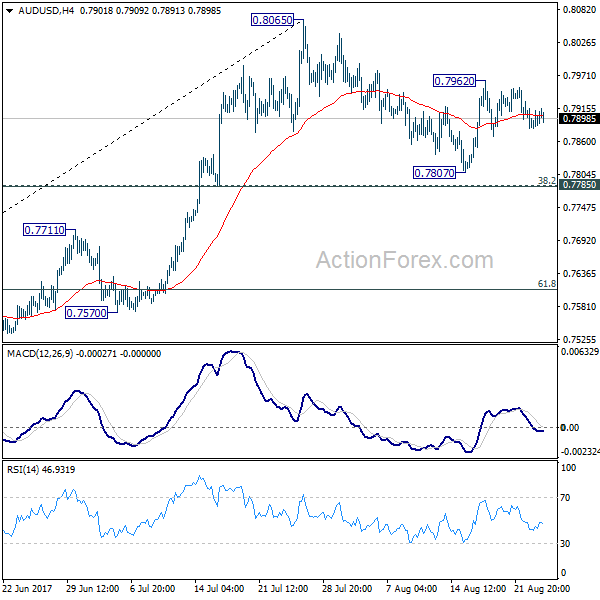

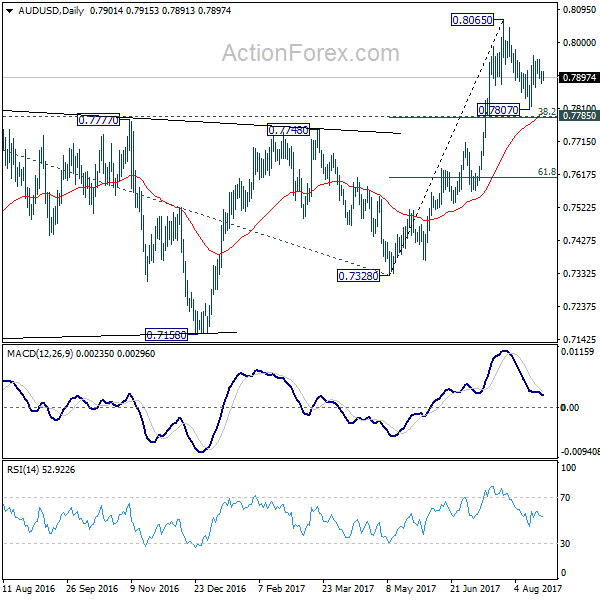

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7885; (P) 0.7900; (R1) 0.7919; More...

Intraday bias in AUD/USD remains neutral at this point. Correction from 0.8065 might extend. But downside should be contained by 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to bring rebound. Above 0.7962 will target a test on 0.8065 resistance first. Firm break of 0.8065 will resume the medium term rise and target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8097) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

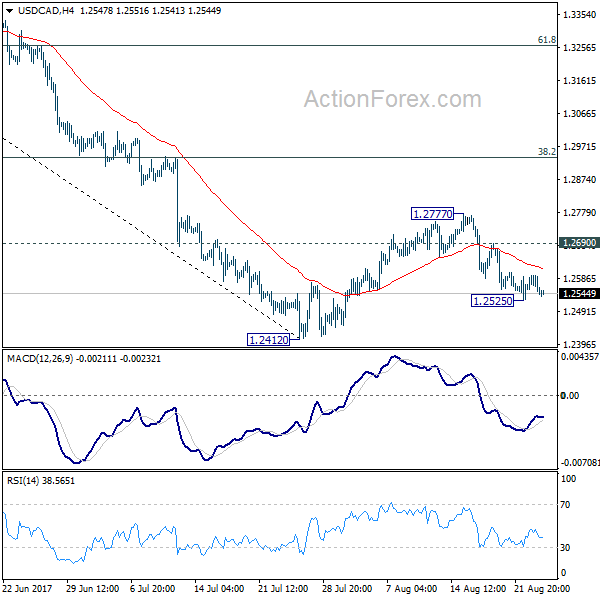

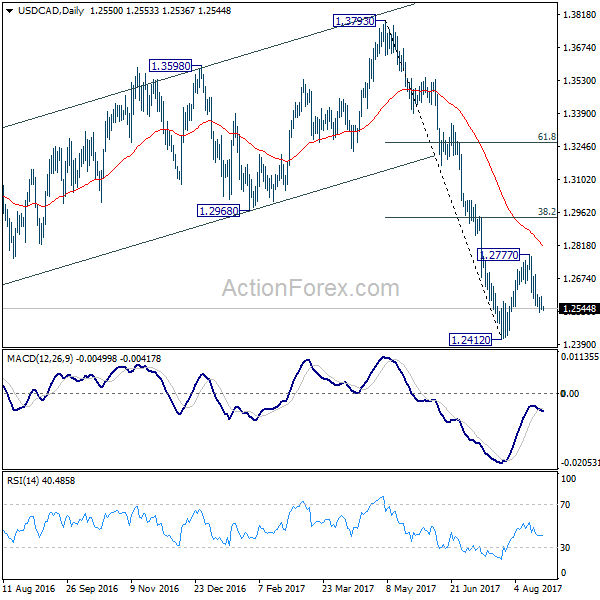

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2527; (P) 1.2562; (R1) 1.2585; More....

Intraday bias in USD/CAD remains neutral for consolidation above 1.2525 temporary low. Deeper fall is expected as long as 1.2690 minor resistance holds. Below 1.2525 will target 1.2412 first. Break there will resume the larger decline and target next long term fibonacci level at 1.2048. On the upside, above 1.2690 will extend the correction from 1.2412 with another rise. But we'd expect upside to be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption eventually.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

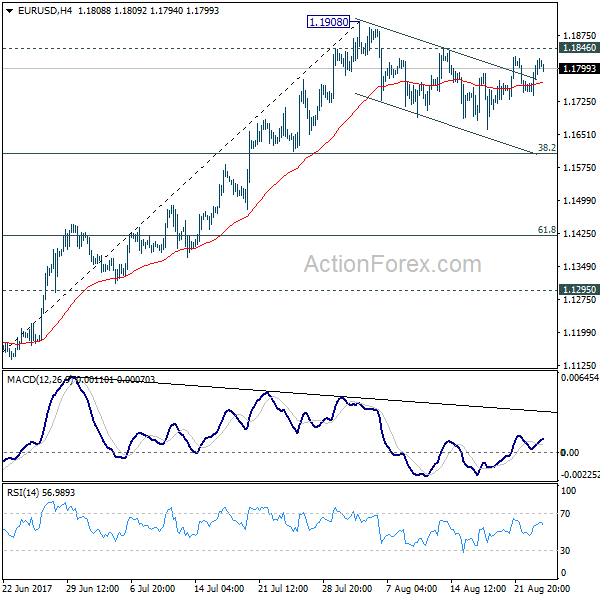

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1756; (P) 1.1789 (R1) 1.1840; More...

The consolidation pattern from 1.1908 is still in progress and intraday bias remains neutral for the moment. In case of deeper fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break of 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9632; (P) 0.9664; (R1) 0.9688; More....

No change in USD/CHF's outlook as it's bounded in range of 0.9582/9772. Intraday bias remains neutral at this moment. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9849) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, we're slightly favoring the case that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

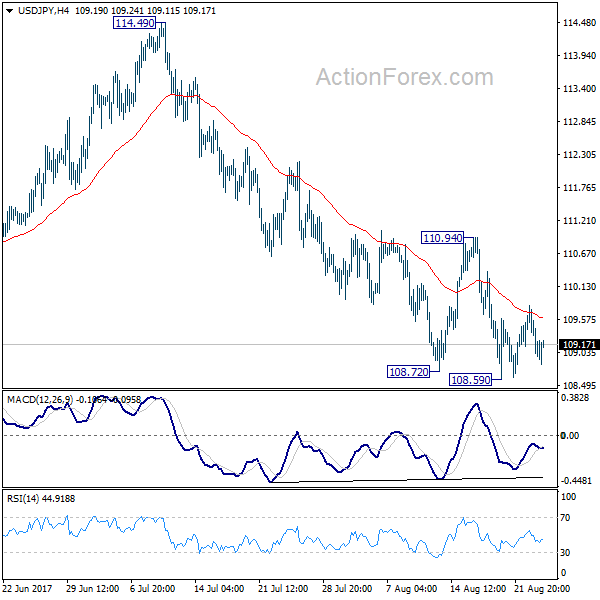

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.69; (P) 109.26; (R1) 109.59; More...

USD/JPY is staying in consolidation above 108.59 temporary low and intraday bias remains neutral. Near term outlook stays bearish with 110.94 resistance intact and deeper decline is expected. Break of 108.59 will target a test on 108.12 low. Whole corrective decline from 118.65 is possibly resuming and break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, firm break of 110.94 will indicate short term bottoming and turn bias back to the upside.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

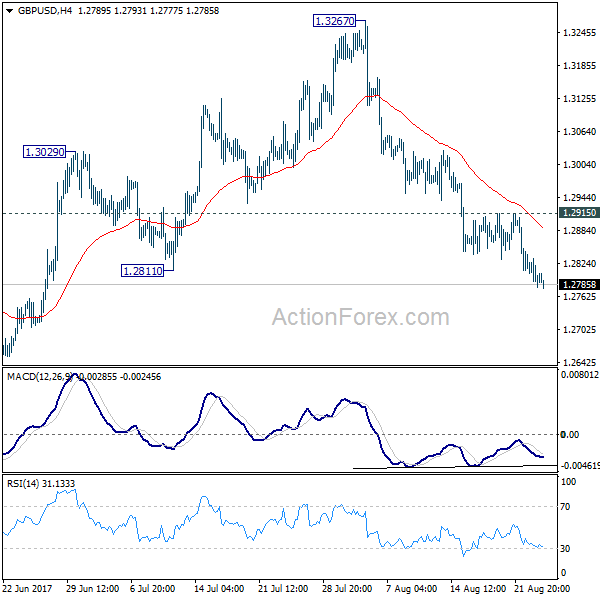

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2803; (R1) 1.2828; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3267 is still in progress for 1.2588 key near term support. As noted before, we're favoring the case that correction from 1.1946 is completed at 1.3267. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. On the upside, break of 1.2952 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Trump’s Government Shutdown Threat Stole Spotlight from Jackson Hole

While markets are awaiting speeches of Fed Chair Janet Yellen and ECB President Mario Draghi in the annual Jackson Hole symposium, they are unsettled by US President Donald Trump's comments on shutting the government. DOW gave up some of the gains on revived hope on tax reform and closed down -87.8 pts or -0.40% at 21812.09. S&P 500 dropped -8.47 pts or -0.35% to close at 2444.04. Dollar index is heading back to 93 handle and is kept well below near term resistance at 94.28, and thus maintaining bearishness. More notable movement is seen in 30 year yield which recent recent fall and closed down -0.04 at 2.749. 10 year yield also lost 0.044 to close at 2.171 but it kept above last week's low at 2.163. In the currency markets, Sterling and Kiwi are trading as the weakest one for the week and there is no sign of a rebound.

Shutdown threat complicates debt ceiling plan

Trump's pledge in a rally in Phoenix that "if we have to close down our government, we're building that wall" is seen by analysts as unsettling. He has requested USD 1.6b for building the US-Mexico border wall but that is widely rejected by Democrats. And, even though the House has passed a spending package with the wall funding, Trump doesn't have enough support to pass in the Senate by September 30. And he could in the end veto the spending bill if wall funding is not included. At the same time, some Republicans are working on a bipartisan bill with Democrats on raising debt ceiling. But the Democrats are clear on their rejection of attaching any condition to the debt bill. Now, it's believed that Trump's veto on spending will not only risk government shut down on October 1, but debt payment defaults shortly after that.

Fitch warns of rating review with negative implications

Credit ratings agency Fitch warned that failure to raise the debt ceiling would prompt a review on US AAA sovereign rating "with potentially negative implications". Fitch warned that "brinkmanship over the debt limit could ultimately have rating consequences, as failure to raise it would jeopardize the Treasury's ability to meet debt service and other obligations." It noted that "republican fiscal conservatives are likely to make support for lifting the debt limit conditional on measures to aggressively reduce the budget deficit. A 'clean' debt limit increase, unattached to other policy measures, appears possible, although it may require support from Democrats." And, "in Fitch's view, the economic impact of stopping other spending to prioritize debt repayment, and potential damage to investor confidence in the full faith and credit of the U.S., which enables its 'AAA' rating to tolerate such high public debt, would be negative for U.S. sovereign creditworthiness."

Impact on Fed's policy

Bearing a resemblance to the situation in 2013, one may worry about Fed's move in light of possible government shutdown. Back in 2013, the FOMC, led by the then Chair Ben Bernanke. Haunted by threats of not raising debt ceilings by Republicans at the time, Bernanke refrained from making announcement on tapering at the meeting on September 17-18. As noted in the minutes, the Fed acknowledged that "a number of significant risks remained, including those related to the potential economic effects of the sizable increases in interest rates since the spring, ongoing fiscal drag, and the possible fallout from near-term fiscal debates". US dollar slumped with the DXY index sinking over -1% on the day of this dovish announcement. More in US Debts Approach Limit. How Will It Affect Fed's Policy?

On the data front

New Zealand trade surplus narrowed to NZD 85b in July but was better than expectation of NZD -200m deficit. UK will release Q2 GDP revision, BBA mortgage approvals and CBI realized sales. US will release jobless claims and existing home sales.

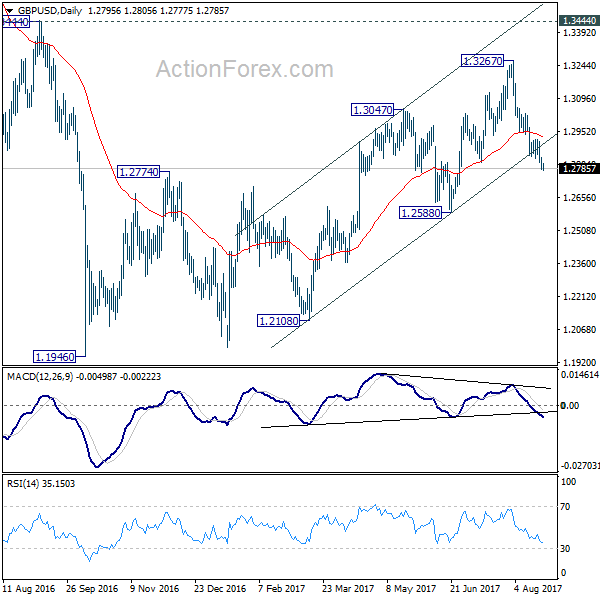

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2803; (R1) 1.2828; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3267 is still in progress for 1.2588 key near term support. As noted before, we're favoring the case that correction from 1.1946 is completed at 1.3267. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. On the upside, break of 1.2952 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | 85M | -200M | 242M | 246M |

| 8:30 | GBP | BBA Mortgage Approvals Jul | 40.2K | |||

| 8:30 | GBP | GDP Q/Q Q2 P | 0.30% | 0.30% | ||

| 8:30 | GBP | Index of Services 3M/3M Jun | 0.50% | 0.40% | ||

| 8:30 | GBP | Total Business Investment Q/Q Q2 P | -0.10% | 0.60% | ||

| 10:00 | GBP | CBI Realized Sales Aug | 14 | 22 | ||

| 12:30 | USD | Initial Jobless Claims (AUG 19) | 236K | 232K | ||

| 14:00 | USD | Existing Home Sales Jul | 5.57M | 5.52M | ||

| 14:30 | USD | Natural Gas Storage | 53B | |||

| Jackson Hole Symposium |