Sample Category Title

Market Update – Asian Session: China Deleveraging Efforts Showing Signs Of Working

Asia Summary

Asian equity markets opened mixed again with quiet trade in equities and FX. The USD firmed up slightly against regional currencies, on avg ~0.1% with a little economic catalyst to push things further. Traders remain focused on Jackson Hole and any indication from world leaders on their plans for fiscal policy. Growth concerns re-enter the peripheral as Trump indicates at yesterday rally that he is fine shutting down the government to get what he wants. The PBOC had its 4th consecutive drain, though skipped OMO; while setting the yuan at an 11-month high of 6.6525.

Key economic data

(NZ) NEW ZEALAND JULY TRADE BALANCE (NZD): +85M V -200ME; YTD: B V -3.51BE; Exports: 4.63B v 4.42Be; Imports4.55 B v 4.60Be

(KR) South Korea Q2 Short Term External Debt: $117.3B v $115.4B prior

Speakers and Press

China/Hong Kong

(CN) FX Regulator SAFE Capital Account Dep Head Guo Song: Proposes stable outbound direct investment policy; work on promoting yuan convertibility under capital account - Chinese Press

(CN) China Premier Li Keqiang: China will further reduce leverage at central State-owned enterprises (SOE) by establishing multiple channels to reduce corporate debts - State Council executive meeting

(CN) China MOFCOM: US probe into China, sabotages international trade system; will use necessary ways to defend legitimate right

(CN) Analysts note that PBOC efforts to deleverage have resulted in a noticeable decline in CODs in August - Chinese press

Korea

(KR) South Korea Fin Min Kim: To announce 'comprehensive' measures on household debt in Sept; Domestic consumption low and employment weak

Asian Equity Indices/Futures (00:00ET)

Nikkei -0.2%, Hang Seng +0.5%; Shanghai Composite -0.0%, ASX200 +0.3%, Kospi +0.4%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.0%, Dax +0.1%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1766-1.1748; JPY 109.83-109.37; AUD 0.7918-0.7883; NZD 0.7283-0.7232

Dec Gold -0.1% at $1,293/oz; Oct Crude Oil -0.04% at $48.38/brl; Sept Copper +0.3% at $2.99/lb

(CN) China PBOC skips OMO v CNY180B in 7 and 14-day reverse reports prior: net drains CNY100B v drains CNY40B prior

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6525 V 6.6633 PRIOR

(CN) PBoC auctions CNY80B in 3-month MoF deposits at 4.51% v 4.46% prior

(NZ) New Zealand sells NZ$150M v NZ$150M indicated in 3.5% 2033 Bonds; avg yield 3.2883%; bid-to-cover 2.23x

(CN) China sells CNY36B in 3-yr bonds

(JP) Japan MoF sells ¥3.59B in 3-month bills; avg yield -0.1463%

Equities notable movers

Australia/New Zealand

FLT.AU Reports FY17 (A$) Net profit 230.8M v 225Me; EBITDA 402.1M v 399Me; Rev 2.68B v 2.64B y/y; +11%

BLY.AU Reports H1 (A$) Adj Net loss 41.8M v loss 52.1M y/y; adj EBITDA 21.4M v 13.5M y/y; Rev 356.2M v 310.5M y/y; +22%

MPG.NZ Chairman: 4-month Rev flat y/y; sees H1 flat y/y – AGM; -11.5%

The Jackson Hole Symposium Starts Today

The Jackson Hole Symposium Starts Today

Market movers today

The Jackson Hole Symposium starts today but financial markets will have to wait until tomorrow to get the key speeches by both ECB President Mario Draghi and Fed President Janet Yellen. There may be some interesting interviews at the fringes though to look out for.

On the data front , US initial jobless claims and US existing home sales are due. Initial claims have been edging lower again in recent weeks and fell to 232k last week – very close to the cycle low in February. It points to a robust labour market with a very low rate of layoffs.

In the UK, the second GDP estimate for Q2 is due for release. The first estimate showed sluggish quarterly growth of 0.3%, driven primarily by the service sector, while construction and manufacturing dragged. However, there is speculation that the second estimate will revise the figure upwards, as we also observed sluggish growth of 0.2% in Q1 and the Bank of England had expected a figure of 0.4%. In the second estimate, we will also get data on the expenditure components and it will be interesting to see whether private consumption growth continues to remain low and investments in Q2 saw high growth (1.2% in Q1).

We have a busy calendar in Scandinavia today: In Norway, the Q2 GDP figures and the Q3 Oil investment survey are due and in Sweden, the Riksbank's Kerst in af Jochnick is due to speak at 13.00. For more details, see Scandi Markets on page 2.

Selected market news

Risk sentiment was weighed down yesterday by renewed concerns about US politics and US equity markets mirrored the declines in Europe with S&P 500 closing 0.35% lower. In Asia, the picture is more mixed this morning with Japanese and Chinese markets trading slight ly lower, while most other regional indices are higher. One of the drivers appears to be some previous comments from US President Donald Trump, who on Thursday threatened a government shutdown if Congress did not pay for his proposed border wall for Mexico. Trump's hard rhetoric has added concerns about a potent ial government shutdown in connect ion with the upcoming debt ceiling negotiations and reminded investors that it might not be easy to get a tax reform deal.

On the data side, euro area PMIs showed an upbeat economic picture in August , supporting our const ruct ive view of euro area growth for this year – we forecast 2.0%. In the US, data was more mixed with US Markit PMI manufacturing falling to 52.5 in August from 53.3 against expectations of an increase to 53.5, with PMI service surprising to the upside rising to 56.9 from 54.7 in July.

Mario Draghi's speech yesterday offered lit t le hints on future monetary policy and while we still have to wait until Draghi's speech at Jackson Hole on Friday at 21:00 CET for more details, we got a little bit of colour on the ECB's stance as ECB member Ardo Hansson said in an interview yesterday that he is not currently concerned about the strength of the euro.

Aussie Dollar Trading Marginally Lower In The Morning Session

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7908.

LME Copper prices declined 0.4% or $29.0/MT to $6555.0/MT. Aluminium prices declined 1.1% or $22.0/MT to $2082.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7905, with the AUD trading a tad lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7886, and a fall through could take it to the next support level of 0.7867. The pair is expected to find its first resistance at 0.792, and a rise through could take it to the next resistance level of 0.7935.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Manufacturing Sector Activity At A 2-Month High In August, Services Sector Growth Cooled To A 7-Month Low In...

For the 24 hours to 23:00 GMT, the EUR rose 0.43% against the USD and closed at 1.1814, following robust economic data from across the Euro-zone.

Data indicated that the Euro-zone's flash Markit manufacturing PMI unexpectedly advanced to a level of 57.4 in August, expanding at its fastest pace in two months, indicating that manufacturing sector continues to be one of the important bellwether for the region's economic recovery. Market participants had expected the PMI to drop to a level of 56.3, following a reading of 56.6 in the prior month. On the contrary, the region's preliminary Markit services PMI unexpectedly fell to a seven-month low level of 54.9 in August, while markets were anticipating it to remain steady at a level of 55.4 registered in the previous month.

In other economic news, the flash consumer confidence index in the common currency region unexpectedly improved to a level of -1.5 in August, compared to a level of -1.7 in the prior month. Markets were anticipating the index to ease to a level of -1.8.

Separately, Germany's manufacturing sector growth unexpectedly jumped to a level of to 59.4 in August, confounding market consensus for a decline to a level of 57.6. In the preceding month, the PMI had registered a reading of 58.1. Moreover, activity in the nation's services sector expanded more-than-expected to a level of 53.4 in August, compared to a reading of 53.1 in the prior month, while markets were expecting the PMI to rise to a level of 53.3.

The greenback lost ground against a basket of currencies, as the US President, Donald Trump's warning of a government shutdown dampened investor sentiment.

The US President vowed that he will shut down government if he does not get funding to build a border wall with Mexico. Further, Trump also threatened of possible termination of the North American Free Trade Agreement (NAFTA).

Meanwhile, Fitch Ratings warned that failure of the US government to raise the debt ceiling in a timely manner would prompt it to review its rating on US sovereign debt for a possible downgrade.

On the macro front, the US preliminary Markit manufacturing PMI unexpectedly eased to a 2-month low level of 52.5 in August, defying market expectation for a rise to a level of 53.5 and compared to a reading of 53.3 in the previous month. On the other hand, the nation's flash Markit services PMI rose to a level of 56.9 in August, topping market expectations of an advance to a level of 55.0. In the prior month, the PMI had recorded a level of 54.7.

Other data showed that new home sales in the US sharply fell by 9.4% on monthly basis, to a level of 571.0K in July, compared to a revised reading of 630.0K in the previous month, while market participants had envisaged it to drop to a level of 610.0K. Also, the nation's mortgage applications slid 0.5% in the week ended 18 August. In the prior week, mortgage applications had risen 0.1%.

In the Asian session, at GMT0300, the pair is trading at 1.1804, with the EUR trading 0.08% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1755, and a fall through could take it to the next support level of 1.1706. The pair is expected to find its first resistance at 1.1838, and a rise through could take it to the next resistance level of 1.1872.

In absence of any major macroeconomic releases in the Euro-zone today, traders will pay attention to the US weekly jobless claims followed by existing home sales data for July, both scheduled to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading Lower, Ahead Of Britain’s GDP Data

For the 24 hours to 23:00 GMT, the GBP declined 0.13% against the USD and closed at 1.2804.

In the Asian session, at GMT0300, the pair is trading at 1.2788, with the GBP trading 0.12% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2766, and a fall through could take it to the next support level of 1.2744. The pair is expected to find its first resistance at 1.2822, and a rise through could take it to the next resistance level of 1.2856.

Going ahead, investors will closely monitor Britain's flash 2Q GDP report, slated to release in a few hours, to gauge the strength in the British economy. Moreover, the nation's BBA mortgage applications data for July, will also be eyed by traders.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Yen Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.76% against the JPY and closed at 108.88.

The Japanese Yen gained ground against the USD, as investors fretted over the US President Donald Trump’s warning of the Federal Government shut-down if Congress fails to fund his long-promised border wall with Mexico.

In economic news, Japan’s final machine tool orders advanced more than initially estimated by 28.0% on an annual basis in July, after recording a gain of 31.1% in the previous month. The preliminary figures had indicated an advance of 26.3%.

In the Asian session, at GMT0300, the pair is trading at 109.17, with the USD trading 0.27% higher against the JPY from yesterday’s close.

The pair is expected to find support at 108.78, and a fall through could take it to the next support level of 108.4. The pair is expected to find its first resistance at 109.62, and a rise through could take it to the next resistance level of 110.08.

Looking forward, Japan’s national consumer price index for July, scheduled to release overnight, will be on investors’ radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading Lower, Ahead Of Switzerland’s Industrial Production Data

For the 24 hours to 23:00 GMT, the USD declined 0.34% against the CHF and closed at 0.9651.

In the Asian session, at GMT0300, the pair is trading at 0.9661, with the USD trading 0.1% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9637, and a fall through could take it to the next support level of 0.9612. The pair is expected to find its first resistance at 0.9691, and a rise through could take it to the next resistance level of 0.972.

Ahead in the day, Switzerland's industrial production data for the second quarter, set to release in a while, will be eyed by investors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Higher This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the CAD and closed at 1.2547.

In the Asian session, at GMT0300, the pair is trading at 1.2544, with the USD trading marginally lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2521, and a fall through could take it to the next support level of 1.2499. The pair is expected to find its first resistance at 1.2582, and a rise through could take it to the next resistance level of 1.2621.

Amid a lack of macroeconomic releases in Canada today, investor sentiment will be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.03; (P) 139.91; (R1) 140.39; More

Intraday bias in GBP/JPY remains on the downside as fall from 147.76 is still in progress for 138.65 support. Break there will extend the fall from 147.76 towards 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. On the upside, above 141.02 minor resistance will turn intraday bias neutral first.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. We'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

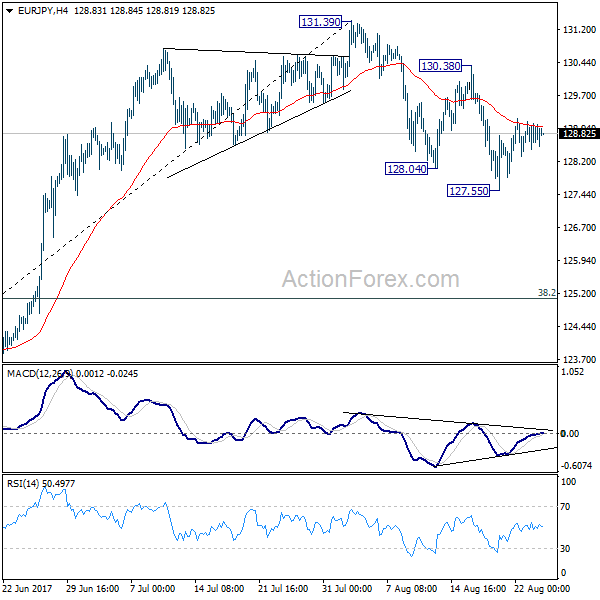

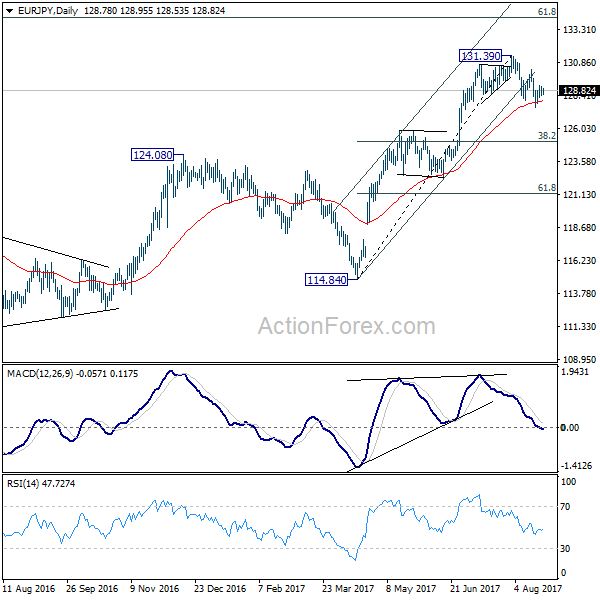

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.43; (P) 128.77; (R1) 129.06; More...

Intraday bias in EUR/JPY stays neutral first. As noted decline from 131.39 is seen as correcting whole rise from 141.84. Deeper fall is expected as long as 130.38 resistance holds. Below 127.55 will target 38.2% retracement of 114.84 to 131.39 at 125.05. Nonetheless, break of 130.38 will argue that the pull back is completed and turn focus back to 131.39 high.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds. However, firm break of 124.08 will argue that rise from 109.03 is completed and turn outlook bearish.