Sample Category Title

Market Morning Briefing: The Mentioned Resistance At 1.1830 On The Euro

STOCKS

Sharp recovery seen in Dow (21899.89, +0.90%) yesterday on talks about renewed hope of the US Tax reforms. While the index remains above 21675, there is scope of re-testing levels near 22000 tonight.

Dax (12229.34, +1.35%) has bounced back from levels near 12000. It could test 12300 on the upside over today and tomorrow before again coming off towards 12100-11950 levels.

Nikkei (19475.85, +0.47%) continues to look weak just now and the downside chances of testing 19000 remains open. Also note that Dollar Yen may have an immediate support near 107.50 which if holds could produce a bounce in both dollar Yen and Nikkei in the near term. In that case, Nikkei may possibly delay a fall towards 19000.

Shanghai (3291.95, +0.06%) could re-test 3300/05 in the coming sessions before coming off sharply towards 3260. In the earlier cases where the index has tested 3300 levels in Nov’16 and Apr’17, it has reversed its trend thereafter. We need to be cautious at current levels and look for any change in the uptrend.

Nifty (9765.55, +0.11%) has been trading just above important support zone of 9750-9700 for the last 2-sessions. In case the index breaks below 9700, we could see a fall towards 9600 soon. Near term looks bearish.

COMMODITIES

Gold (1289) is hovering around its key physiological resistance of 1300 and if this resistance breaks, a quick bounce towards 1317-25 can’t be ruled out. Otherwise it remains in a sideways move which may take it to the support of 1275 and 1259. Silver (16.93) is also trading within the range of 16.50-17regions. Only a daily close above 17.05 could open up 17.50 levels.

Copper (2.96) is trading within the narrow range of 2.85-98. Only above 2.98, higher resistances of 3.05 and 3.12 can come into consideration. We will remain bullish on copper while it is trading above 2.85 regions.

We have U.S crude oil inventory today at 8.00 pm with an expectation of a shortage of 3.3MB. If the actual data will reflect the same then it will be the 9th consecutive week of shortage in U.S. oil inventory which could be beneficial for the whole energy pack. At the same time Brent (51.75) is trading within the range of 49.70-52.80.Only a close above 52.80 could open up 55 regions. WTI (47.50) is also trading within the range of 46.50-49 as well. We will remain bullish on Brent and WTI while they are trading above 49.70 and 46.50 regions respectively.

FOREX

The mentioned Resistance at 1.1830 on the Euro (1.1762) held beautifully yesterday, pushing the Euro down to 1.1745 in the European session itself. If the German-US 10Yr yield Spread (-1.81%) does not bounce from the Support at the current level, it can threaten the existing uptrend in the Euro.

Still, Euro-Yen (128.95) has been stable as Dollar-Yen (109.65) has risen alongwith the fall in the Euro, establishing 108.60 as a credible Support for now. Watch Resistance at 110.00 today. Break thereof can propel the market up to 110.70 else we may see sideways range trade between 110-109. Peeks above 110.00 could get sold.

The Pound (1.2821) has come down quite a bit in line with expectation, perhaps opening up chances of further decline towards 1.26.

The Aussie (0.7898) has dipped along with the Euro and could test Support near 0.7845-30, where it could find buying interest again. In the bigger picture The overall uptrend since the May '17 low near 0.7319 remains in force but the Resistance at 0.80 needs to be broken in order to take the Aussie higher. Resistance above 3.00 on Copper could hold the Aussie down for a while.

We might see further strength in the Chinese Yuan (USDCNY = 6.6592) towards 6.6150. Dollar-Rupee remains stable between 64.10-25-40, as expected.

INTEREST RATES

The US yields are hovering around their crucial areas of supports. If 2.18 holds then the 10Yr (2.21%) could test 2.23% and 2.25% within few days of time.

Euro looks stable and there can be scope for upside if the German-US 2Yr Spread (-2.03%) and the German-US 10Yr Spread (-1.81%) bounce from current Supports in the near term and rise towards -1.97% and -1.75% respectively.

The Japan 5Yr (-0.09%) and the 10Yr (0.05%) are moving upwards.If this will continue then The Japan 30Yr (0.84%) might move upward towards 0.90%.

The UK yields had also rebound from their lows. The 10YR (1.08%) and the 20YR (1.63%) are stable at this moment, but both have scope of testing 1% and1.50% on the downside.

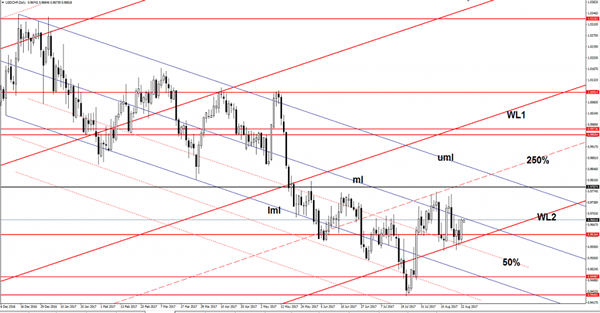

USD/CHF Gaining Pace

Price is trading in the green and looks determined to take out the dynamic resistance from the median line (ml). Technically should increase further after the failure to close on the WL2. A valid breakout will send the rate towards the 0.9787 static resistance and towards the 250% and the upper median line (uml).

We have an important confluence area formed at the intersection between the 250% line and the upper median line (uml), which could attract the price.

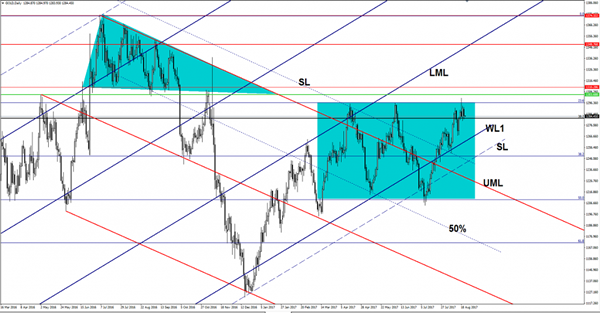

GOLD Consolidates The Lates Gains

The yellow metal continues to move in range on the Daily chart, only a valid breakout will bring us a clear direction. Is trapped within the 23.6% and the 50% retracement level, you can see that we had a false breakout above the 23.6% and above the $1295 per ounce on Friday, signaling an exhaustion.

Now is retesting the long term 38.2% retracement level, will increase further if the support will hold, while a breakdown will signal a drop at least till the WL1.

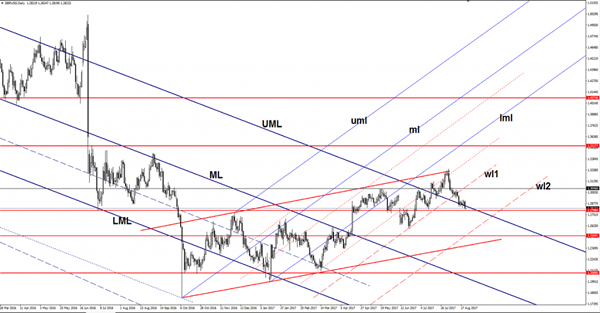

GBP/USD Hovers Above Critical Support

Price is still heavy on the Daily chart and seems poised to hit new lows on the Daily chart. Has changed little in he morning as the USDX is undecided as well. Has managed to drop below a major dynamic support and is approaching a crucial static support, a valid breakdown will open the door for more declines in the upcoming weeks.

Technically is somehow expected to drop further, but the rate will be driven by the fundamental factors in the upcoming days. We have to be very careful during the Jackson Hole Symposium because we may have a high volatility.

GBP/USD dropped through the upper median line (UML) of the major descending pitchfork and now is almost to hit the 1.2798 static support. A valid breakdown below this downside obstacle will attract more sellers, which will lead the price towards fresh new lows.

Price is very heavy after the failure to stabilize above the upper median line (UML) of the major descending pitchfork. Is very important to see what will happen on the USDX as well, which is located right above the 93.50 psychological level, but is trapped below a dynamic resistance.

GBP/USD is somehow expected to drop at least till will reach the second warning line (wl2) of the minor ascending pitchfork. Could reach this level, even if will stay above the UML and above the 1.2798 static support.

The Dollar Tax Trade

The US dollar trade is slowly evolving into a bet on Washington and its ability to deliver a tax cut. USD was the top performer while NZD lagged. Japan manufacturing PMI from Nikkei is up next. After closing the USDJPY short yesterday w/ 185 pip-gain, 6 trades are currently in progress (all in green) 2 in FX, 2 in indices 2 in metals.

Ray Dalio+ the head of the world's biggest hedge fund, wrote on Monday that markets are more sensitive to politics than any time in our lifetimes. We see it every day in the way that political headlines have more impact than economic data.

A big part of Tuesday's USD rally was the increasing sense that Trump is morphing into a classic Republican, something we warned about to start the week. It began with the ouster of Bannon on Friday and continued with the embrace of the war in Afghanistan. If markets conclude that he will be more like George W. Bush than Candidate Trump in the rest of his term, then the implied FX impact could be the one Ashraf warned about 7 months ago here.

Ultimately, markets are concerned with the bottom line -- A shift to the center from the President could help to break the gridlock in Congress. That would lower the temperature and raises the odds of tax reform. In the meantime, the US dollar trade will be increasingly tied to the likelihood of success. Tuesday's climb was a small step as it remains at vulnerable levels, particularly USD/JPY.

Another spot to watch in the day ahead is GBP/USD. The July low of 1.2811 is pips away after another slump. $1.2770 is the take-out target for the bears.

Looking to Asia-Pacific trading, the main release on the calendar is the August preliminary Nikkei Japan PMI. The prior reading was 52.1. Later, Markit is out with services and/or manufacturing data for France, Germany and the US as well.

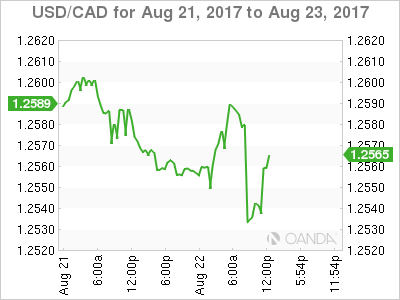

Canadian Dollar Rallies after Strong Retail Sales

Canada Retail Sales Strong

Data this morning showed that Canadian retail sales rose for the fourth consecutive month in June, edging up +0.1% to +CA$49.0B.

Sales were up in 6 of 11 subsectors, representing +38% of total retail trade.

Higher sales at general merchandise stores, clothing and clothing accessories stores, and building material and garden equipment and supplies dealers offset lower sales at motor vehicle and parts dealers and gasoline stations. Ex- the latter two subsectors, retail sales were up +1.1%.

After removing the effects of price changes, retail sales in volume terms increased +0.5%.

The loonie (CA$1.2550) is forecast to trade stable in a defined CA$1.24-$1.28 range for the foreseeable future because little new is expected from the upcoming Bank of Canada (BoC) meeting on Sept 6.

Dealers are not expecting anything dramatic in terms of shifting U.S rate expectations at this week Jackson Hole symposium and it is not clear that there are big swing factors in prospect for the Canadian monetary policy either in the coming month.

USD/CAD is trading generally in line with interest rate differentials. In Canada, the market remains more confident than in the U.S that a further rate hike will be delivered before the end of the year.

Fed fund futures are currently attaching a +40% probability for a U.S rate hike, and a +66% probability for a BoC hike.

Note: At the start of August, the probability was +75%. If this process continues it would be consistent with USD/CAD trading back up to $1.2800 territory.

There is little reason for Governor Poloz at the BoC to downplay market expectations for a rate hike, but neither are they likely to feel compelled to reinforce hike expectations.

NAFTA

NAFTA negotiations are underway and in the early stages there is always scope for the rhetoric to sound more divisive as the sides adopt their starting negotiating position. But it is not clear that this will have a very large impact on the CAD.

The U.S, Canada and Mexico wrapped up their first round of talks on the weekend, vowing to keep up a blistering pace of negotiations.

In a joint statement issued at the end of five days of negotiations in Washington, the top trade officials from the three countries said Mexico would host the next round of talks from Sept. 1 to 5.

The joint statement said the three countries made "detailed conceptual presentations" across the scope of NAFTA issues and began work to negotiate some of the agreement's texts, although it did not provide details on the topics.

Oil on CAD

The influence of oil prices over the commodity sensitive CAD has been declining during H2 and remains low.

The correlation between daily changes in the oil price and the exchange rate has been -0.13 over the last month. At the end of June, the measure was -0.64.

This may be because there has been less excitement in the oil story than in the BoC's pivot towards the exit in recent months, but the trend of lower highs in the oil price since late-February suggests a market still under pressure.

Crude Oil Showed Signs of Stall

Limited recovery action on Tuesday, after the price showed signs of stall after failing to sustain gains above initial barriers at $47.89/98 (converged 100/10SMA's) keep near-term risk shifted lower.

Strong support, provided by daily cloud top ($47.01) which contained Monday's strong bearish acceleration, could be retested if the price continues to lose traction.

Violation of cloud top would then risk retest of key near-term support at $46.44 (17 Aug low) reinforced by 55SMA, loss of which would signal bearish continuation of the downleg from $50.41 (01 Aug high).

Conversely, sustained break above 100/10 SMA's would sideline downside risk, but extension above $48.72 pivot (double upside rejection / 20SMA) is needed to neutralize and turn bias higher.

Res: 47.89; 47.98; 48.72; 49.51

Sup: 47.35; 47.01; 46.44; 46.22

Bulls Push USD Higher ahead of Jackson Hole

US dollar bulls were active today due to speculations about possible hawkish rhetoric from the Fed's chairwoman Janet Yellen on Friday at the economic symposium in Jackson Hole. An increase in the possibility of a third rate hike by the Fed for this year should be able to offset some of the pressure the greenback is feeling due to the political tensions in the US. The euro declined today also due to weak data from the ZEW Economic Sentiment index for the Eurozone that showed a decline to 29.3 for August against the expected fall to 34.2.

The pound sterling was unable to show positive dynamics despite the fall in public net borrowings in the UK by 0.8 billion pounds in July versus the growth of 5.7 billion pounds in June. Further news from the UK showed the CBI industrial order expectation index came in at 13 which is 5 better than forecasted. Negotiations on the Brexit terms is still holding back the bulls from buying the GBP/USD. The Richmond manufacturing index release had little effect on traders' mood as it remained at 14 for August despite the forecasted decline to 11.

Traders ignored the strength of the US dollar and continued buying the Canadian dollar after the release of the core retail sales report in Canada which showed an increase of 0.7% for June against the expected zero change. Additional pressure on the USD/CAD came from positive dynamics from oil prices which traditionally impact the pair's quotes.

EUR/USD

The EUR/USD price was not able to gain a foothold above the important 1.1800 level and to fix beyond the limits of the descending channel. As a result, the price tested the 1.1750 mark and its breaking may lead to further price falls to 1.1700 and 1.1620. We do not rule out the possibility of fixing above 1.1800 and that may become a trigger for continued growth to 1.1900 and 1.2000.

GBP/USD

After some price consolidation of the GBP/USD near 1.2900 we have seen a confident decline with quotes approaching support at 1.2800. Its breaking may be the push the pair needs for a continued decline to 1.2660. In order to reverse the current negative trend, the price has to break through 1.2900. In this scenario, increases may continue up to 1.3050 and 1.3250.

USD/CAD

The USD/CAD demonstrates a high level of volatility but the amplitude of price fluctuation is reducing. The RSI on the 15-minute chart is near the oversold zone, and that, together with the approach to the angled support line, may point to an upward correction soon due to profit taking. The next target level within the fall may be at 1.2470. Overcoming the local high at 1.2600 may lead to growth acceleration with goals at 1.2665 and 1.2800.

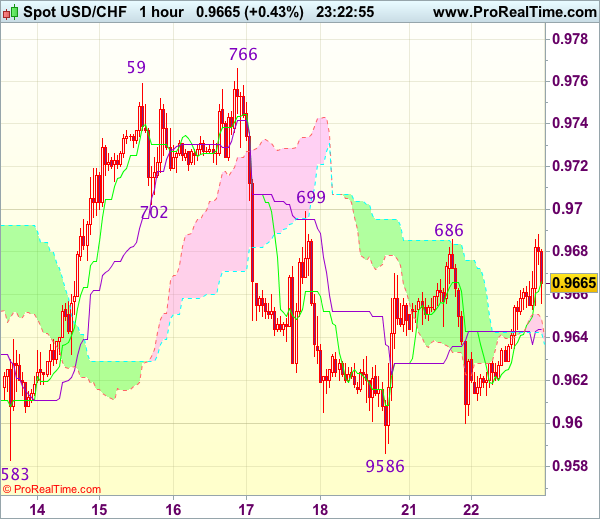

Trade Idea Wrap-up: USD/CHF – Buy at 0.9630

USD/CHF - 0.9662

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9666

Kijun-Sen level : 0.9644

Ichimoku cloud top : 0.9649

Ichimoku cloud bottom : 0.9643

Original strategy :

Buy at 0.9630, Target: 0.9730, Stop: 0.9595

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9630, Target: 0.9730, Stop: 0.9595

Position : -

Target : -

Stop : -

As dollar’s rebound gathered momentum, suggesting the retreat from 0.9766 has ended at 0.9586 last week and consolidation with mild upside bias is seen for gain to 0.9720, then 0.9740, however, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are looking to buy dollar on pullback as 0.9620-30 should limit downside. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

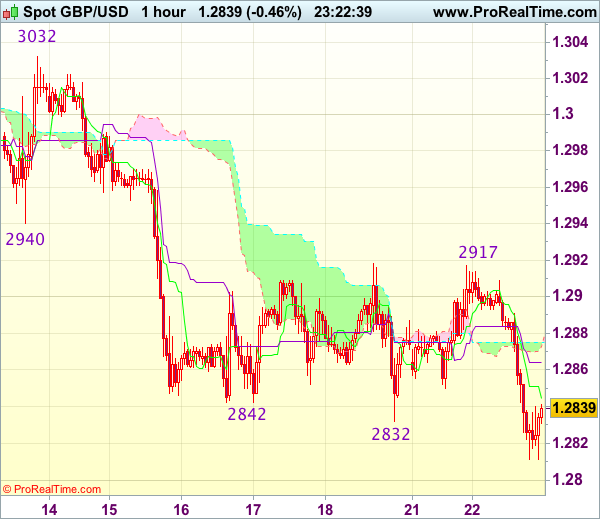

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2840

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2845

Kijun-Sen level : 1.2864

Ichimoku cloud top : 1.2875

Ichimoku cloud bottom : 1.2873

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable finally resumed recent decline as the pair broke below support at 1.2832, loss of downward momentum should prevent sharp fall below previous support at 1.2812 and reckon 1.2770 would limit downside, price should stay above 1.2750 today and risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above the upper Kumo (now at 1.2875) would suggest an intra-day low is formed and bring a stronger rebound to 1.2890 but only break of resistance at 1.2917-18 would signal a temporary low is formed, bring retracement of recent decline to 1.2933-40 (previous support) first.