Sample Category Title

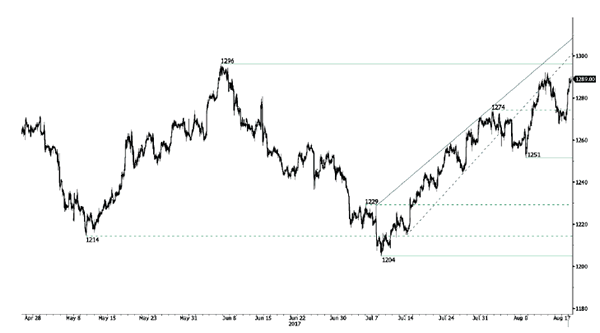

GOLD Strengthening

Gold is back towards strong resistance given at 1296 (06/06/2017 high). Hourly support is given at 1251 (08/08/2017 low). Stronger support lies at 1204 (10/07/2017 high). Expected to show continued buying pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

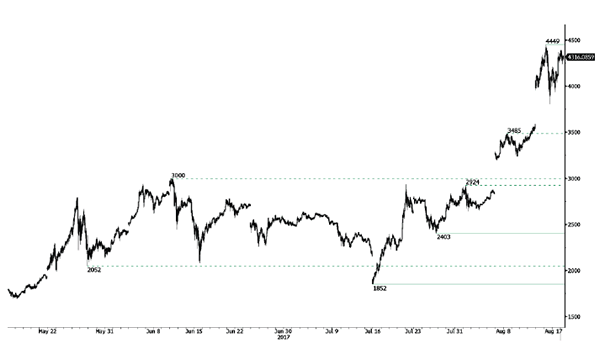

BITCOIN Ready For Another Leg Higher

Bitcoin is pausing after the massive surge over the past few days. Resistance is the all-time high at 4449 (15/08/2017 high). hourly support lies very far at 2403 (26/07/2017 low). The road is wide open for another bullish move.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

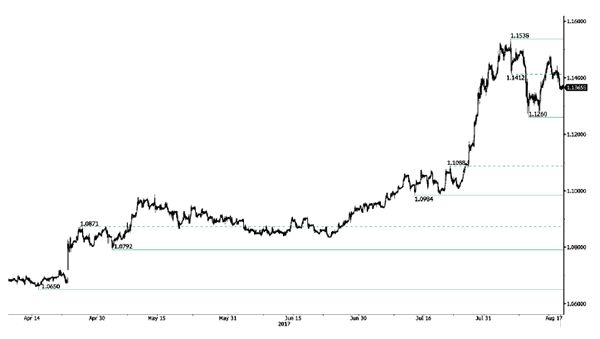

EUR/CHF Starts A Consolidation Phase Around 1.1400

EUR/CHF's short-term buying pressures are back on. Hourly support is now located at 1.1260 (04/08/2017 low). Expected to show continued increase.

In the longer term, the technical structure has reversed. Strong resistance at 1.1200 (04/02/2015 high) has been broken. Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low)

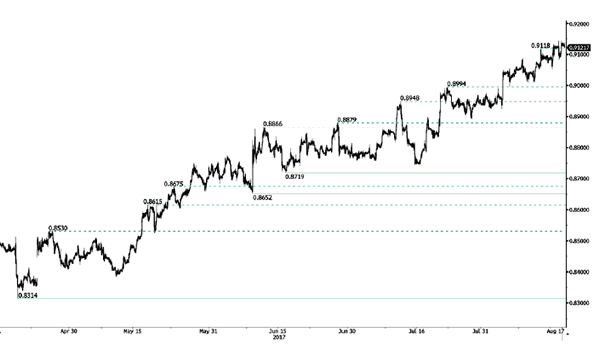

EUR/GBP Breaking 0.9100

EUR/GBP is trading around its highest levels of the year despite ongoing consolidation. Hourly resistance lies at 0.9087 (08/08/2017 high) has been brokem. Hourly support is given at a distance at 0.8742 (16/06/2017 low). Downside risks are nonetheless important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

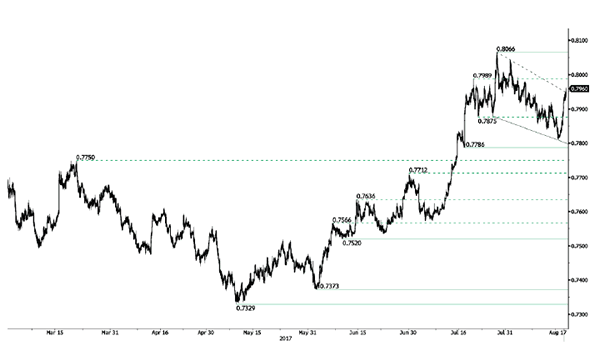

AUD/USD Surging

AUD/USD's short-term technical structure has reversed. Hourly support can be found at 0.7786 (18/07/2017 low). Hourly resistance is given at 0.8066 (27/07/2017 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

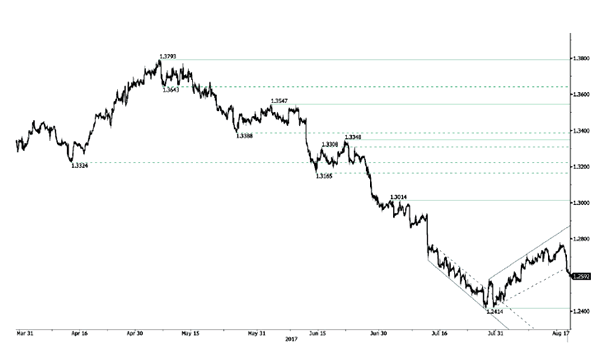

USD/CAD Bearish Breakout

USD/CAD's short-term bullish momentum is ending. Hourly support is given at a distance at 1.2414 (27/07/2017 low). Expected to show continued short-term bearish move.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low) before bouncing back. Strong resistance is given at 1.4690 (22/01/2016 high). The pair should head further lower.

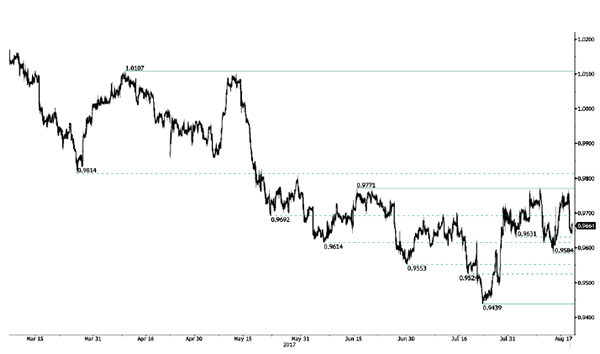

USD/CHF Failed To Monitor Resistance At 0.9771

USD/CHF is pushing higher. Resistance is given at 0.9771 (15/06/2017 high). Hourly support lies at at 0.9584 (08/11/2017 low). Expected to to bounce back lower.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

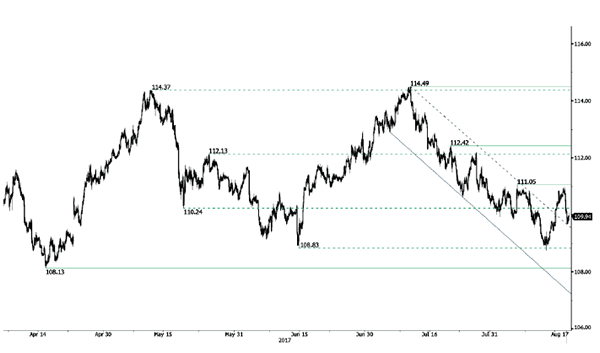

USD/JPY Renewed Bearish Pressures

USD/JPY's bearish pressures are back despite the rebound at 108.83 (17/04/2017 low). Expected to show another leg lower.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

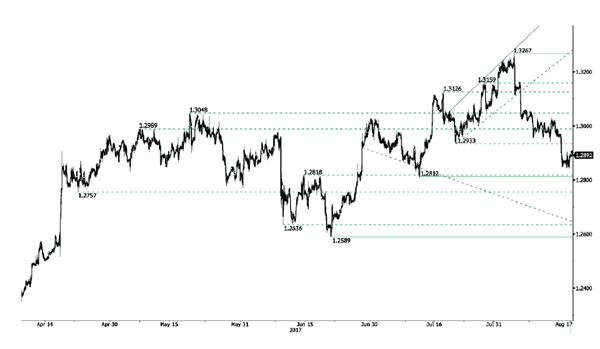

GBP/USD Bouncing Towards Support At 1.2933

GBP/USD is edging higher. Hourly resistance is given at 1.3267 (03/08/2017 high). Hourly support can be found at 1.2812 (12/07/2017 low). Expected to show continued bearish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

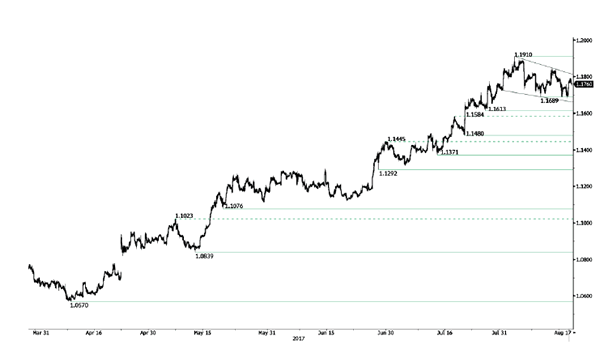

EUR/USD Weakening

EUR/USD bearish pressures are on. Hourly resistance is given at 1.1910 (02/08/2017 high) while hourly support can be found at 1.1689 (09/08/2017 high). Stronger support lies at 1.1613 (26/07/2017 low). Expected to show further short-term selling pressures.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance holding at 1.1871 (24/08/2015 high) has been broken while strong support lies at 1.0341 (03/01/2017 low).