Sample Category Title

Easing U.S.-North Korea Tensions Trigger Dollar Short-Covering

U.S. Retail Sales Post Biggest Rise In Seven Months. The dollar inched slightly lower on Wednesday but held most of its gains made after U.S. retail sales data suggested the economy continued to gain momentum in the third quarter and kept alive hopes for another Federal Reserve interest rate increase this year. U.S. retail sales rose 0.6% and core sales rose 0.5% in July beating economists’ estimate of a 0.4% and 0.4% reading. Minutes from the Fed’s July meeting will be watched for clues on the timing of rate hikes as well as whether the Fed is likely to announce a reduction in its balance sheet at its September meeting.

Gold Falls On U.S. Retail Sales Data. Gold prices were moderately lower prior to the release largely due to profit-taking pressure after prices hit a nine-week high on Friday. But, immediately after the data was published, December Comex gold fell even further, trading at $1,274.20, down 1.26% on the day. Gold prices firmed early on Wednesday as the dollar weakened slightly, with investors waiting for the release of minutes from the U.S. Federal Reserve’s last meeting in July for clues on the pace of potential interest rate hikes.

Oil Prices Edge On Falling US Crude Inventories. Oil prices rose early on Wednesday on a fall in U.S. crude inventories, although analysts said that markets were still being weighed down by general oversupply. Brent crude futures, the international benchmark for oil prices, were at $51.01 per barrel at 0023 GMT, up 21 cents, or 0.4 percent, from their last close.

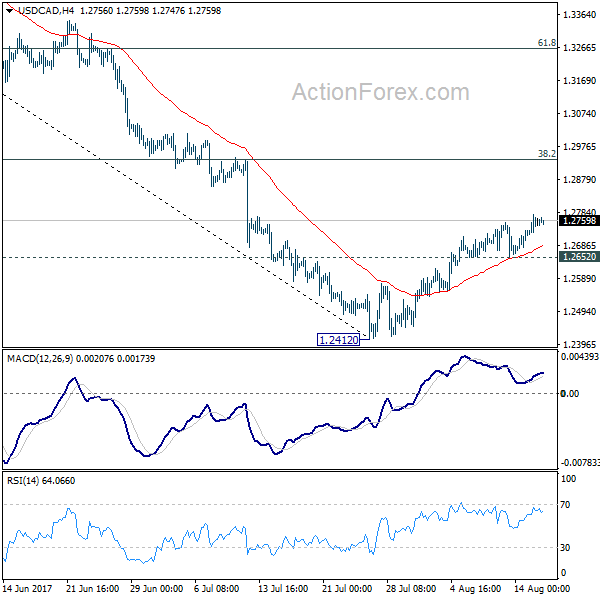

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2723; (P) 1.2750; (R1) 1.2784; More....

USD/CAD's recovery from 1.2412 resumed and reaches as high as 1.2777 so far. Intraday bias is mildly on the upside for further rise. Nonetheless, such rise is viewed as a corrective move. And based on current momentum, upside should be limited by 38.2% retracement of 1.3793 to 1.2412 at 1.2940 to bring fall resumption. On the downside, below 1.2652 minor support will argue that the recovery is completed and turn bias back to the downside for retesting 1.2412.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is still expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Nonetheless, on the upside, sustained break of 1.2968, 38.2% retracement of 1.3793 to 1.2412 at 1.2940 will be the first sign of completion of the correction and will turn focus back to 1.3793 key resistance.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

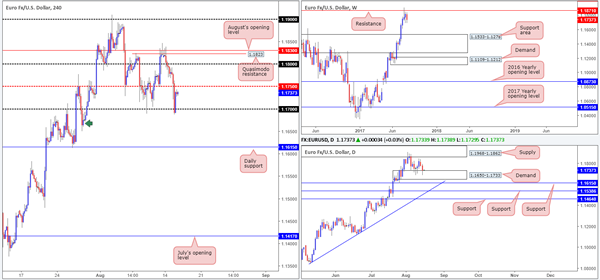

EUR/USD

The EUR/USD experienced another wave of selling on Tuesday, exacerbated by a broad-based advance in US retail sales. The single currency did, however, recover some ground going into the US segment as price struck the 1.17 handle, together with a minor daily demand base coming in at 1.1650-1.1733. Closing just ahead of the H4 mid-level resistance at 1.1750, where does this leave us in terms of trading opportunities?

Buying above 1.1750 could be an option, but by doing so, we’d potentially be going up against weekly selling from the weekly resistance level planted at 1.1871!

What about a short below the 1.17 region? By selling sub 1.17, not only would you then be trading into daily buyers from the demand mentioned above, but you’d also be going up against possible buyers from the ‘hook’ shaped H4 demand marked with a green arrow at 1.1650-1.1664.

.Suggestions: Technically speaking, we do not see much to hang our hat on at the moment. No matter which direction we select to trade, there’s some form of higher-timeframe structure in the foreground. Therefore, we’ll remain on the sidelines for now and wait for further developments.

Data points to consider: EUR Flash GBP at 10am. US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

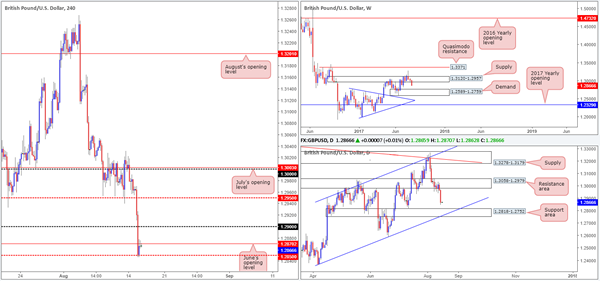

GBP/USD

The British pound took an absolute hammering on Tuesday, plummeting nearly 100 pips from open to close! The first round of selling came after UK inflation data failed to meet market expectations, eventually forcing H4 price beneath the 1.29 handle. Further selling was seen later on in the day after better-than-expected US retail sales, forcing the unit to trade below June’s opening level at 1.2870 and into the H4 mid-level support barrier at 1.2850.

While the bulls have registered some interest from 1.2850, June’s opening level seen just above is well offered at the moment. In addition to this, over on the bigger picture we can see that the daily support area at 1.3058-1.2979 finally gave way and price now looks poised to challenge the daily support area pegged at 1.2818-1.2752. Further supporting the bears, the weekly timeframe shows space for the market to trade as far down as the demand area coming in at 1.2589-1.2759.

Suggestions: Although the higher timeframes suggest further selling could be upon us, shorting this market sub 1.2850 is challenging. Positioned only 30 pips beneath this number is the top edge of the aforementioned daily support area, followed closely by the 1.28 handle drawn on the H4 chart (not seen on the screen).Given the lack of space for sellers here, we’re going to take the safest position of all today: FLAT.

Data points to consider: UK employment figures at 9.30am. US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

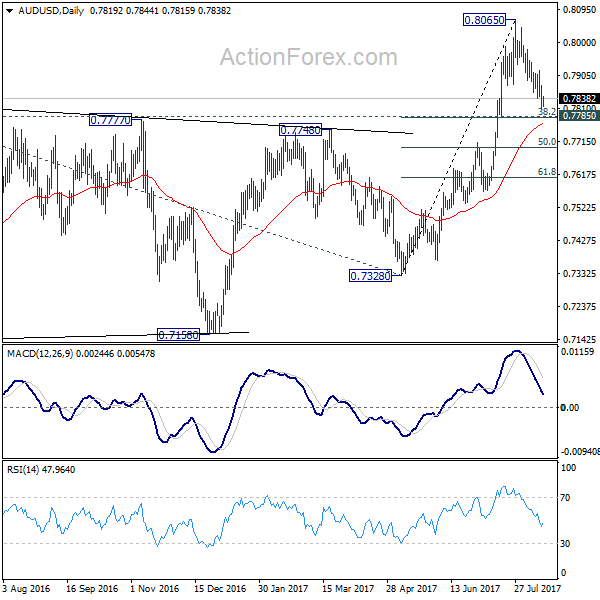

AUD/USD

For those who read Tuesday’s report you may recall that we set a pending buy order at 0.7805, with a stop-loss order tucked beneath H4 demand at 0.7784. Thanks to yesterday’s selloff, fueled by better-than-expected US retail sales figures, we may see this order filled later on today.

Why we chose this H4 demand as a buy zone is due to the following:

The weekly candles recently came into contact with a support area marked at 0.7849-0.7752.

The daily timeframe also shows price interacting with a demand at 0.7786-0.7838, which encases a broken Quasimodo level at 0.7819.

The 0.78 handle is seen housed within the current H4 demand.

Suggestions: Wait for the pending buy order to fill and look to target 0.7850 as your initial take-profit zone. With a 21-pip stop and 42 pips to the first target, we have attractive risk/reward in play here.

Data points to consider: US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: 0.7805 ([pending order] stop loss: 0.7784).

- Sells: Flat (stop loss: N/A).

USD/JPY

The US dollar continued to rise against its Japanese counterpart on Tuesday, reaching a high of 110.84 on the day. Those who were looking to short the 110.50 region based on yesterday’s report, the level was unfortunately violated due to upbeat US retail sales figures. Never trade before high-impacting news!

The H4 candles are currently seen capped between June’s opening level at 110.80 and the 110.50 boundary, so where does one go from here? Well, according to the daily structure, a move lower could be on the cards due to price currently interacting with resistance at 110.76. The flip side to this, of course, is the weekly timeframe showing the unit trading from demand at 108.13-108.95.

Suggestions: Ultimately, what we’re looking for is a daily close above the current resistance. This, on the daily timeframe, would likely clear the pathway north up to resistance pegged at 111.91. As for a possible entry, a H4 close above 111, followed up with a retest as support and a H4 bullish candle (preferably a full-bodied candle) would be enough for us to pull the trigger and target the 112 region/July’s opening level at 112.09 (positioned just above the said daily resistance).

Data points to consider: US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to close above the 111 region and then look to trade any retest seen thereafter ([waiting for a reasonably sized bullish candle to form following the retest – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

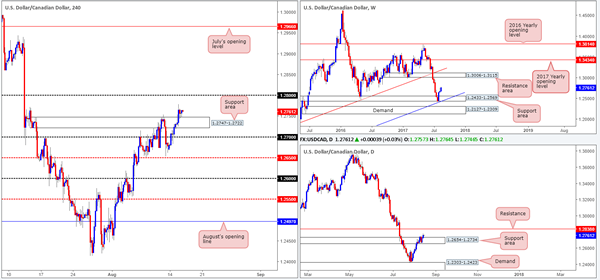

USD/CAD

Following stronger-than-expected US retail sales data, the dollar appreciated against its Canadian rival and closed above the H4 supply fixed at 1.2747-1.2722. With the H4 candles now seen retesting this area, we may see price cross swords with the 1.28 handle seen overhead. On a similar note, daily action also crossed above the resistance area coming in at 1.2654-1.2734, which could, if the bulls remain in control, send the unit up to resistance at 1.2838. Further supporting the bid-side of this market is the weekly bulls from 1.2433-1.2569. We do not see any obvious resistance on this scale until the 1.3006-1.3115 area.

Suggestions: Given how well the H4 candles have held following a retest of the recently broken supply, a buy from current price is, in our opinion, valid. However, you need to be prepared to face some opposition from 1.28, and then the daily resistance at 1.2838.

Data points to consider: US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1

Levels to watch/live orders:

- Buys: A long at current price is valid given the structure of this market (stop loss: aggressive: 1.2740 conservative: 1.2720).

- Sells: Flat (stop loss: N/A).

USD/CHF

In recent trading, the USD/CHF tested the H4 mid-level resistance at 0.9750 and managed to punch to a low of 0.9702 on the day. As you can see, 0.9750 is shadowed closely by a H4 Quasimodo resistance at 0.9764 and a daily Quasimodo resistance planted just above that at 0.9776. All of this structure – coupled with a major weekly trendline resistance extended from the low 0.9257, makes for an overbought market, in our humble view.

As we mentioned in Tuesday’s report, we are interested in the daily Quasimodo resistance mentioned above, largely because of how well price reacted when it came near to testing the boundary last week, and, of course, the converging weekly trendline resistance!

Suggestions: Although we believe price will bounce from the daily Quasimodo resistance, we still require a bearish H4 candle to form in the shape of either a full, or near-full-bodied candle. This just helps confirm whether there are interested sellers from this point.

Data points to consider: US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.9776 region ([waiting for a reasonably sized bearish candle to form – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s wick).

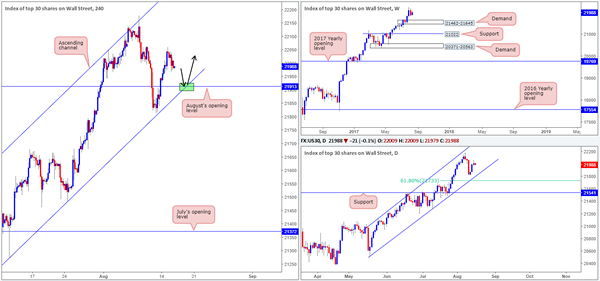

DOW 30

Of late, we’ve seen the US equity market ease from highs of 22060 and clock a low of 21968. Seen directly below current price on the H4 timeframe is August’s opening level at 21913, which happens to fuse beautifully with a channel support line extended from the low 21273.

As noted in yesterday’s report, we do not see any higher-timeframe resistances on the horizon at the moment. Therefore, a retest of August’s opening level, alongside the aforementioned H4 channel support would, in our humble view, be a nice area to consider entering long from (green zone).

Our suggestions: As you are probably already aware trendlines are unfortunately prone to being faked, so we would highly recommend being patient and waiting for a H4 bullish candle to take shape in the form of a full, or near-full-bodied candle. This will, of course, not guarantee that the level will hold, but what it will do is show bullish intent from a potential buy zone!

Data points to consider: US Housing numbers at 1.30pm, followed later by the FOMC meeting minutes at 7pm GMT+1.

Levels to watch/live orders:

- Buys: 21913 region ([waiting for a reasonably sized H4 bullish candle to form – in the shape of either a full, or near-full-bodied candle – is advised] stop loss: ideally beyond the candle’s tail).

- Sells: Flat (stop loss: N/A).

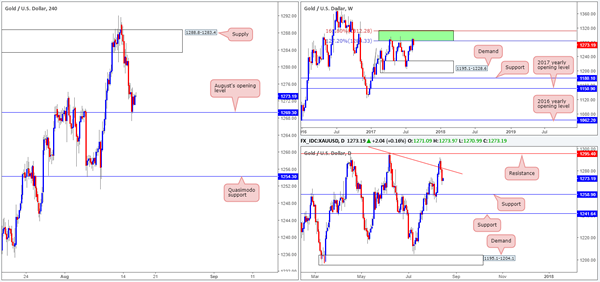

GOLD

Demand for the safe-haven metal continued to diminish on Tuesday, bringing H4 price down to August’s opening level pegged at 1269.3. With tensions easing between the US and North Korea, and weekly price trading from a resistance area comprised of two weekly Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1, a selloff in this market was high probability.

As well as seeing space for weekly price to continue selling off, we can also see that daily price shows room to trade down as far as a support level seen at 1258.9. However, as we mentioned above, August’s opening level is currently seen providing support.

Our suggestions: Until we see a H4 close print below August’s opening level, we will refrain from taking any shorts in this market. A close below this monthly line, followed up with a retest and a lower-timeframe sell signal (see the top of this report) would, in our opinion, be enough to confirm a sell trade down to the daily support mentioned above at 1258.9, followed closely by the H4 Quasimodo support at 1254.3.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Watch for H4 price to close below 1269.3 and then look to trade any retest seen thereafter ([waiting for a lower-timeframe sell signal to form following the retest is advised] stop loss: dependent on where one confirms this level).

Daily Technical Analysis: EUR/USD, GBP/USD Build Shallow Retracements After Bearish Breakout

Currency pair EUR/USD

The EUR/USD is showing bearish continuation as expected in the wave analysis earlier this week. Price is building a potential ABC (purple) correction within a larger wave 4 (green). The main target of the ABC are the Fibonacci levels of wave 4 vs 3 (green).

The EUR/USD broke below the support trend line (dotted blue) but was unable to break below the bottom (green line). Price is now building a pullback, which could be a wave 4 (brown). A break above the 61.8% and resistance trend line (red) makes a wave 4 less likely. A break below support (greens) could see price continue towards 23.6% Fib.

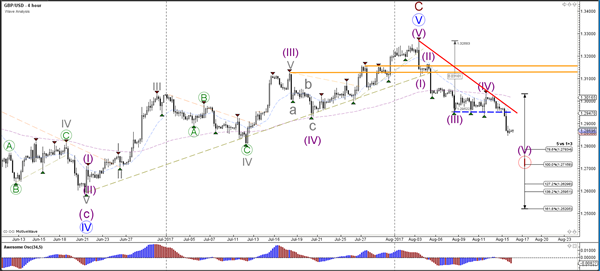

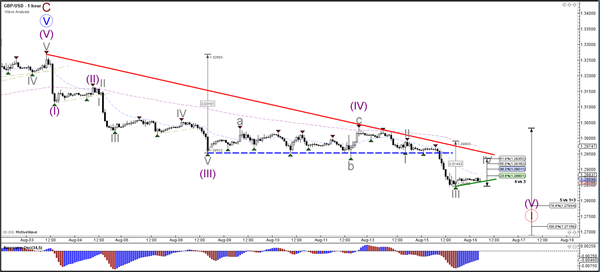

Currency pair GBP/USD

The GBP/USD broke below the support trend line (dotted blue) and continued the downtrend.

The GBP/USD is building an extension within the 5th wave with another 5 waves (grey). The current pullback is a bear flag chart pattern and could be a wave 4 (grey). A break above the 61.8% Fibonacci level invalidates the wave 4.

Currency pair USD/JPY

The USD/JPY breakout managed to reach the 38.2% Fibonacci resistance level of the wave B (brown), which could cause a bearish bounce and complete wave A (orange).

The USD/JPY seems to have completed wave 5 (purple) within wave A (orange). A bullish break above resistance (orange) could see an extension the uptrend whereas a bearish break of the support trend lines could see an ABC (purple) within wave B (orange).

European Open Briefing: Asian Equity Markets Continued To Inch Ahead Today

Global Markets:

- Asian stock markets: Nikkei rose 0.01 %, Shanghai Composite fell 0.22 %, Hang Seng climbed 0.73 %, ASX up 0.21 %

- Commodities: Gold at $1278.79 (- 0.05 %), Silver at $16.68 (- 0.16 %), WTI Oil at $47.78 (+0.48 %), Brent Oil at $51.11 (+0.61 %)

- Rates: US 10-year yield at 2.26, UK 10-year yield at 1.08, German 10-year yield at 0.43

News & Data:

- AUD Wage Price Index q/q 0.5 % vs 0.5 % expected

- NZD GDT Price Index -0.4 % vs – 1.6 % previous

- USD Retails Sales m/m 0.6 % vs 0.3 % expected

- USD Core Retails Sales m/m 0.5 % vs 0.3 % expected

- GBP CPI y/y 2.6 % vs 2.7 % expected

- GBP PPI Input m/m 0.0 % vs 0.4 % expected

- CHF PPI m/m 0.0 % vs -0.1 % previous

Markets Update:

Asian equity markets continued to inch ahead today as global Markets are starting to settle down after a tumultuous few days spurred by heightened tensions between the U.S. and North Korea

AUD/USD broke its two-day decline and started moving a little higher on the session after the wages data came in as expected, Price moved in from lows under 0.7820 to around 0.7840 gaining over 0.2 % against the US Dollar

USD/JPY was little changed in Wednesday's Asian session with price currently seen trading around it's opening price of 110.65 per dollar. It is worth mentioning that the yen had taken an added blow from the easing in risk aversion and lost 1.4 % against the dollar yesterday.

EUR/USD was little changed in the Asian session today. The Euro had experienced another wave of selling on Tuesday, exacerbated by a broad-based advance in US retail sales falling to lows of 1.16872 before recovering some ground going into the US segment as price struck above the 1.17 handle

GBP/USD slumped heavily after UK inflation numbers came in below expected, losing over 100 pips breaching key support levels against the US dollar. The pound is currently seen trading at $1.2870, having shed over 1.0 % overnight.

Upcoming Events:

- 08:30 GMT – (GBP) Average Earnings Index 3m/y

- 08:30 GMT – (GBP) Claimant Count Change

- 08:30 GMT – (GBP) Unemployment Rate

- 09:00 GMT – (EUR) Flash GDP q/q

- 12:30 GMT – (CAD) Foreign Securities Purchases

- 12:30 GMT – (USD) Housing Starts

- 12:30 GMT – (USD) Building Permits

- 14:30 GMT – (USD) Crude Oil Inventories

- 18:00 GMT – (USD) FOMC Meeting Minutes

- 22:45 GMT – (NZD) PPI Input q/q

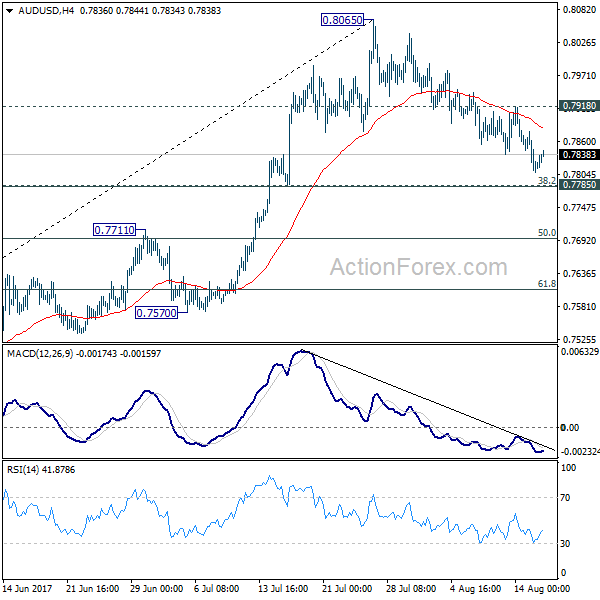

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7792; (P) 0.7834; (R1) 0.7861; More...

AUD/USD's correction from 0.8065 extends to 0.78907 so far but outlook is unchanged. We'd still expect strong support from 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to contain downside and bring rebound. Break of 0.7918 minor resistance will suggest that such pull back is completed. In this case, intraday bias will be turned back to the upside for retesting 0.8065. However, firm break of 0.7785 will extend the fall back to 0.7570/7711 support zone.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Dollar Yet to Confirm Reversal Despite Rebound, FOMC Minutes Watched

Dollar pares back some gains today but remains the strongest one for the week. FOMC minutes will be a main focus for the day which could decide whether the greenback can extend its rebound. So far, technically, such rebound in Dollar doesn't warrant a trend reversal yet. For example, EUR/USD is held above 1.1688 minor support and well above 1.1606 fibonacci level. That is, EUR/USD's near term outlook remains bullish. USD/CHF is help below 0.9772 resistance and thus, not confirming resumption of rebound from 0.9473. AUD/USD is also held well above 0.7785 cluster support, and the pull back from 0.8065 is seen as a correction. The main exception is GBP/USD which is building up the case of bearish reversal, thanks to Sterling's own weakness.

Regarding minutes of July FOMC meeting, the markets will be particularly interested in knowing policymaker's view on inflation outlook. In the accompanying statement of the meeting, policymakers acknowledged that the overall inflation and the measure excluding food and energy prices (core inflation) have "declined" and are "running below 2%". The removal of the word "somewhat" signaled the weakness in inflation is more than the Fed had anticipated. We would look to see if the Fed maintained the view that weak inflation is "transitory".

So far, Fed officials have been rather cautious regarding the chance of another rate hike by the end of the year. The main exception is New York Fed President William Dudley while remained "favor of doing another rate hike later this year". After his comments earlier this week, market pricing of Fed rate path returned to normal. For now, Fed fund futures are pricing in 98.6% chance for Fed to stand pat in September. Chance of a rate hike in December is roughly 50%.

German FM Schaeuble defends ECB asset purchases

Germany's constitutional court requested European Court of Justice for a ruling on whether ECB's asset purchase program as violated the ban on financing governments. ECB quickly acted to defend and said in a statement that "the extended asset purchase programme is in our opinion fully within our mandate." German Finance Minister Wolfgang Schaeuble also said that ECB's "mandate is being implemented" ECB was exhausting its tools to "fulfil its hellishly difficult task of devising a monetary policy for many different countries".

UK Job, Eurozone GDP to highlight European session

On the data front, Australia Westpac leading index rose 0.1% mom in July, wage cost index rose 0.5% qoq in Q2. UK job data will be a major focus in European session, which could decide whether Sterling's broad based decline will extend. Eurozone GDP is another focus. Later in US session, US will release housing starts and building permits before FOMC minutes.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7792; (P) 0.7834; (R1) 0.7861; More...

AUD/USD's correction from 0.8065 extends to 0.78907 so far but outlook is unchanged. We'd still expect strong support from 0.7785 cluster support (38.2% retracement of 0.7328 to 0.8065 at 0.7783) to contain downside and bring rebound. Break of 0.7918 minor resistance will suggest that such pull back is completed. In this case, intraday bias will be turned back to the upside for retesting 0.8065. However, firm break of 0.7785 will extend the fall back to 0.7570/7711 support zone.

In the bigger picture, rise from 0.6826 medium term bottom is still in progress. At this point, there is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, break of 55 month EMA (now at 0.8100) will target 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Westpac Leading Index M/M Jul | 0.10% | -0.10% | -0.20% | |

| 1:30 | AUD | Wage Cost Index Q/Q Q2 | 0.50% | 0.50% | 0.50% | 0.60% |

| 8:00 | EUR | Italian GDP Q/Q Q2 P | 0.40% | 0.40% | ||

| 8:30 | GBP | Jobless Claims Change Jul | 6.0K | |||

| 8:30 | GBP | Claimant Count Rate Jul | 2.30% | |||

| 8:30 | GBP | Average Weekly Earnings 3M/Y Jun | 1.80% | 1.80% | ||

| 8:30 | GBP | ILO Unemployment Rate 3M Jun | 4.50% | 4.50% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.60% | 0.60% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jun | 29.46B | |||

| 12:30 | USD | Housing Starts Jul | 1.22M | 1.22M | ||

| 12:30 | USD | Building Permits Jul | 1.25M | 1.25M | ||

| 14:30 | USD | Crude Oil Inventories | -6.5M | |||

| 18:00 | USD | FOMC Meeting Minutes Jul |

Australia’s Westpac Leading Index Rebounded In July

For the 24 hours to 23:00 GMT, the AUD declined 0.45% against the USD and closed at 0.7821.

LME Copper prices rose 0.5% or $31.0/MT to $6382.0/MT. Aluminium prices rose 1.3% or $26.0/MT to $2056.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7830, with the AUD trading 0.12% higher against the USD from yesterday's close.

Earlier today, data revealed that Australia's Westpac leading index rebounded 0.12% in July. In the prior month, the index had fallen by a revised 0.15%.

The pair is expected to find support at 0.7800, and a fall through could take it to the next support level of 0.7770. The pair is expected to find its first resistance at 0.7868, and a rise through could take it to the next resistance level of 0.7906.

Moving ahead, market participants will closely monitor Australia's unemployment rate data for July, due to release in the early hours tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

German Economy Expanded Slightly Less-Than-Expected In The Three Months To June

For the 24 hours to 23:00 GMT, the EUR declined 0.32% against the USD and closed at 1.1740.

Data indicated that Germany's seasonally adjusted flash gross domestic product (GDP) advanced 0.6% on a quarterly basis in the second quarter of 2017, as households and state authorities increased their spending and companies boosted investment. However, market participants had envisaged the nation's GDP to climb 0.7%, compared to a revised rise of 0.7% in the prior quarter.

The US Dollar nudged higher against its key peers, lifted by upbeat US economic data.

Data showed that advance retail sales in the US climbed more-than-expected by 0.6% in July, posting its sharpest increase in seven months and suggesting that consumer spending was off to a good start in the third quarter. Market participants had expected advance retail sales to gain 0.3%, after recording a revised increase of 0.3% in the previous month. Further, the nation's New York Empire State manufacturing index jumped to a level of 25.2 in August, notching its highest level since September 2014 and beating market expectations of a rise to a level of 10.0. In the previous month, the index had registered a reading of 9.8. Moreover, the nation's business inventories surged to a seven-month high, after it advanced 0.5% in June, surpassing market expectations for a rise of 0.4%. In the previous month, business inventories had risen 0.3%.

Other economic data showed that the US NAHB housing market index recorded an unexpected rise to a level of 68.0 in August, confounding market expectations for the index to remain steady at a level of 64.0. Also, the nation's import price index rose 0.1% MoM in July, meeting market expectations. In the previous month, the index had registered a drop of 0.2%. Also, the nation's export price index rebounded above expectations by 0.4% MoM in July, compared to a drop of 0.2% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1736, with the EUR trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.1687, and a fall through could take it to the next support level of 1.1637. The pair is expected to find its first resistance at 1.1786, and a rise through could take it to the next resistance level of 1.1835.

Moving ahead, investors will keep a close watch on the Euro-zone's flash 2Q GDP numbers, slated to release in a few hours, to gauge strength in the European economy. Additionally, in the US, the FOMC July meeting minutes coupled with the nation's housing starts and building permits data, both for July, all scheduled to release later in the day, will be closely watched by investors.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Britain’s Annual Inflation Came In Softer-Than-Expected In July

For the 24 hours to 23:00 GMT, the GBP declined 0.73% against the USD and closed at 1.2867, following weaker-than-expected UK inflation data.

Britain's consumer price index (CPI) climbed 2.6% on an annual basis in July, compared to a similar rise in the previous month. Market participants had expected the CPI to advance 2.7%.

In the Asian session, at GMT0300, the pair is trading at 1.2863, with the GBP trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.2816, and a fall through could take it to the next support level of 1.2769. The pair is expected to find its first resistance at 1.294, and a rise through could take it to the next resistance level of 1.3017.

Going forward, UK's ILO unemployment rate data for the three months to June, slated to release in a few hours, will grab a lot of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.