Sample Category Title

Strong Retail Sales To Start the 3rd Quarter

Retail and food services surged 0.6 in July while the original 0.2 percent decline in June was revised upwardly to 0.3 percent. Thus, consumer demand started the third quarter on a strong footing.

Strong Retail Sales Even With Weak Gasoline Sales

Gasoline sales declined 0.4 percent in July after a dropping 1.5 percent in June. However, none of those declines were able to put a dent on consumer demand in either month as retail and food services sales increased an upwardly revised 0.3 percent in June and a strong 0.6 percent print in July. The strength in retail sales was broad based, with motor vehicle and parts dealers' sales increasing 1.2 percent while building material & garden equipment & supplies dealers' sales increased 1.2 percent after printing 1.1 percent in June. Even department stores sales, a sector that has been negatively affected by the eruption of online sales, posted a strong 1.0 percent increase for the month. Still, the sector is down 2.7 percent on a year-earlier basis and followed a 0.7 percent decline in June.

Other weak sectors in July were electronics & appliance stores' sales, declining 0.5 percent, while clothing & clothing accessories stores sales declined 0.2 percent compared to June.

However, the rest of the sectors were up during the month, portraying a very strong consumer at the end of the second quarter as well as at the start of the third quarter, which is completely contrary to the view we observed by looking at second quarter PCE numbers released several weeks ago.

Furniture & home furniture stores' sales were up 0.4 percent after increasing 0.5 percent in June, while food & beverage stores sales were up 0.4 percent after declining 0.7 percent in June. Health & personal care stores sales were up 0.4 percent after increasing 0.3 percent the previous month. Meanwhile, sporting goods, hobby, book & music stores' sales were up 0.3 percent, partially recovering the 0.5 percent decline in June.

The strongest sector in June was the miscellaneous store retailers sector, growing 1.8 percent during the month after declining 1.7 percent in June. Meanwhile, non-store retailers' sales were up 1.3 percent after a strong 1.0 percent increase in June. This sector was up 10.4 percent on a yearearlier basis.

Control Group Sales Strong in July

The July retail sales report was strong overall and this was also reflected in the retail sales control group aggregate, which goes into the calculation of GDP. This aggregate increased 0.6 percent compared to expectations of a 0.4 percent increase. Furthermore, control group sales were upwardly revised from a 0.1 percent decline in June to an increase of 0.1 percent. This means that not only is Q2 PCE probably going to be revised higher from an already strong 2.8 percent, but that the expectations for PCE during the third quarter are also going to be marked up going forward. That is, both indicators for the consumption of goods and services from the retail sales report are looking promising for the start of the third quarter of the year. It will be interesting to see if they can keep their momentum.

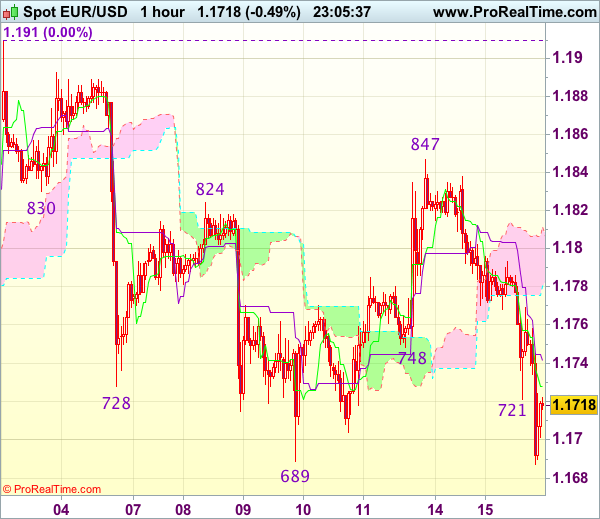

Trade Idea Wrap-up: EUR/USD – Sell at 1.1755

EUR/USD - 1.1720

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1728

Kijun-Sen level : 1.1742

Ichimoku cloud top : 1.1812

Ichimoku cloud bottom : 1.1780

Original strategy :

Sell at 1.1755, Target: 1.1655, Stop: 1.1790

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1755, Target: 1.1655, Stop: 1.1790

Position : -

Target : -

Stop : -

Current selloff adds credence to our view that the rebound from 1.1689 (last week’s low) has ended at 1.1847 and a firm break below said support would extend recent decline from 1.1910 top to 1.1640-50 (50% Fibonacci retracement of 1.1370-1.1910 and previous support), below there would encourage for subsequent fall towards 1.1600-10 which is likely to hold from here due to near term oversold condition.

In view of this, we are looking to sell euro on recovery as 1.1755-60 should limit upside and bring another decline later. Above 1.1790-95 would abort and risk a stronger rebound to 1.1820 but price should falter below said resistance at 1.1847.

Spot Gold Extended Pullback for the Second Day

Spot Gold extended pullback from $1292 peak for the second day, with further bearish acceleration coming from fresh strength of dollar on better than expected US data. Renewed risk-on mode that reduced safe haven assets demand puts gold price under increased pressure.

Today's action broke below important supports at $1276 (Fibo 38.2% of $1251/$1292 upleg) then daily Tenkan-sen at $1271 and met next target at $1267 (Fibo 61.8%) where temporary footstep was found.

Fresh bears may take a breather here as near-term studies are oversold, but limited upside action could be expected, as strong bearish signals on south-heading daily RSI/slow stochastic which reversed from overbought zone, suggesting further downside.

Broken Fibo 38.2% at $1276 is seen capping extended upticks before bears resume.

Close below $1267 pivot is needed to confirm bearish continuation and expose targets at $1264 (20SMA) and $1261 (Fibo 76.4%).

Res: 1271; 1276; 1282; 1285

Sup: 1267; 1264; 1261; 1258

Trade Idea Wrap-up: USD/JPY – Buy at 110.15

USD/JPY - 110.52

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 110.57

Kijun-Sen level : 110.14

Ichimoku cloud top : 109.50

Ichimoku cloud bottom : 109.31

Original strategy :

Buy at 110.20, Target: 111.20, Stop: 109.85

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.15, Target: 111.15, Stop: 109.80

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after breaking above resistance at 110.18, suggesting the rebound from 108.73 low is still in progress and gain to previous resistance at 111.05 cannot be ruled out, however, break there is needed to retain bullishness and extend this rise for a stronger correction of early decline to 111.25-30, however, near term overbought condition should prevent sharp move beyond previous resistance at 111.71, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as the Kijun-Sen (now at 110.14) should limit downside. Only below previous resistance at 109.80 would abort and signal top is formed instead, bring weakness towards support at 109.42.

Retail Sales in US Strengthened the Greenback

The greenback is gaining position amid less attention to the tension linked with the nuclear threat from North Korea. This fact resulted in more attention to macro statistics. Thus, the EUR/USD was under pressure from the weaker than expected growth of German GDP in the second quarter. This, according to the preliminary report was only 0.6% vs forecasted 0.7%. The positivity for the bulls in the US dollar is due to the retail sales growth in America up by 0.6% in July, twice better than the average prediction. Retail sales are the key indicator for consumption driven American economy. An additional factor that added strength to the dollar was the increase of Empire State manufacturing index to 25.2 vs 9.8 in the previous period.

The sharp decline today has been seen in the price of the GBP/USD due to an increase of the consumer price index in the UK by only 2.4% in July against anticipated growth by 2.5%. Slower inflation growth may restrain the Bank of England from raising interest rates which is negative for the bulls in the pound Sterling. Tomorrow the center of attention will be the retail sales report in the UK.

The AUD/USD is still under pressure of lowering prices on commodity markets and the USD growth. The statement from the RBA according to which the interest rate remained at the 1.50% level, had limited impact on the quotes. The central bank has concerns about possible declines in spending due to the low pace of wage increase in the country. Traders are waiting for the labor market report in Australia that will be published tomorrow at 01:30 GMT.

EUR/USD

The single currency quotes accelerated its fall after a slight correction. Now the quotes are rebounding after testing the support at 1.1700. In the case of overcoming this level we may see a continued decline to the next targets at 1.1620 and 1.1500. The upward correction is likely to be limited by the upper limit of the channel and the resistance at 1.1800.

GBP/USD

After some consolidation above the important 1.2950 level the quotes have shown a sharp decline. The overcoming of 1.2880 may be the stimulus for a continued drop to 1.2800 and 1.2635. In order to change the trend to positive, the quotes need to fix beyond the limits of the descending channel and in this case the potential goal will be at 1.3250.

AUD/USD

The aussie has reached the lower limit of the descending channel and may test the important support at 0.7800. After the fall and considering the RSI on 15-minute chart being in the oversold zone there is an increased possibility of an upward correction with a potential of increase to 0.7850-0.7900. In case of breaking through to 0.7800 we may see a decline to 0.7740 and 0.7700.

Canadian Dollar Edges Lower as US Retail Sales Rebounds

The Canadian dollar has edged higher in the Tuesday session. In North American trade, USD/CAD is trading at 1.2756, up 0.28% on the day. On the release front, there are no Canadian events for a second straight day. In the US, Retail Sales came in at 0.6%, above the estimate of 0.4%. Core Retail Sales also looked sharp, with the gain of 0.5% beating the forecast of 0.3%. There was more good news from the manufacturing sector, as the Empire State Manufacturing Index soared to 25.2, crushing the estimate of 10.1 points. On Wednesday, the US releases Building Permits and Housing Starts. As well, the FOMC publishes its minutes from the July FOMC meeting.

It's been a disappointing August for the Canadian dollar, which has dropped 2.2% this month. The currency has become less attractive with the current tensions in the Korean peninsula. Investors have lost some of their risk appetite and stayed away from minor currencies such as the Canadian dollar, preferring safe-haven assets such as the Japanese yen and gold. Still, Canadian fundamentals are in good shape, as recent employment and housing numbers have been strong. The currency is closely linked to oil prices, with the loonie gaining ground in July as oil prices went up, only to retract in August as crude prices have dropped this month.

The markets were jittery last week, as the saber-rattling between the US and North Korea reached a fever pitch. North Korea threatened to fire missiles at Guam, and President Trump warned of severe consequences in response. The crisis weighed on stock markets last week, but the markets have rebounded as the war of words between Washington and Pyongyang has abated somewhat, increasing risk appetite on the part of investors. Still, tensions remain high in the Korean peninsula, and if either side ratchets up the rhetoric, the markets could again lose ground, and this could hurt the Canadian dollar.

Trade Idea: EUR/GBP – Buy at 0.9000

EUR/GBP - 0.9107

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

New strategy :

Buy at 0.9000, Target: 0.9130, Stop: 0.8960

Position : -

Target : -

Stop : -

As the single currency has risen again after brief pullback, suggesting recent erratic upmove is still in progress and bullishness is seen for further gain to 0.9145-50, however, weakening of near term upward momentum should prevent sharp move beyond 0.9175-80 and price should falter below 0.9200, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy euro on subsequent pullback as 0.9000-05 would limit downside. Below 0.8960-70 would defer and suggest a temporary top is possibly formed, bring correction to 0.8922 support which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Sell at 1.2825

USD/CAD - 1.2759

Trend: Down

Original strategy :

Sell at 1.2800, Target: 1.2600, Stop: 1.2860

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2825, Target: 1.2625, Stop: 1.2885

Position: -

Target: -

Stop:-

Although the greenback has risen again after brief pullback and near term upside risk remains for the corrective rise from 1.2414 low to extend gain to 1.2800, as this move is still viewed as retracement of recent decline (tentatively wave iv), reckon upside would be limited to 1.2825-35 and bring retreat later, below 1.2650-55 would suggest top is possibly formed, bring weakness to 1.2600 but break of support at 1.2553 is needed to provide confirmation, bring further fall to 1.2500 first. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii possibly ended at 1.2414, hence wave iv correction is underway.

In view of this, would be prudent to stand aside for now and look to sell on further subsequent rebound as 1.2825-30 should limit upside. Above 1.2880-85 (50% Fibonacci retracement of wave iii) would abort and signal a temporary low is formed, bring a stronger rebound to 1.2940-50 but price should falter below 1.2990-95 (61.8% Fibonacci retracement) and bring retreat later this week.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Yen Slides as US Retail Sales Beats Estimate

USD/JPY has jumped higher in Tuesday's North America session. In North American trade, the pair is trading at 110.78, up 1.04% on the day. On the release front, Japanese Revised Industrial Production rebounded with a strong gain of 2.2%, beating the forecast of 1.6%. In the US, Retail Sales came in at 0.6%, above the estimate of 0.4%. Core Retail Sales also looked sharp, with the gain of 0.5% beating the forecast of 0.3%. There was more good news from the manufacturing sector, as the Empire State Manufacturing Index soared to 25.2, crushing the estimate of 10.1 points. On Wednesday, the US releases Building Permits and Housing Starts. As well, the FOMC publishes its minutes from the July FOMC meeting.

The yen posted strong gains last week, as the saber-rattling between the US and North Korea reached a fever pitch. North Korea threatened to fire missiles at Guam, and President Trump warned of severe consequences in response. The safe-haven yen gained 1.3% last week, but the dollar has regained these losses, as a reduction in the rhetoric between Washington and Pyongyang has increased risk appetite on the part of investors. Still, tensions remain high in the Korean peninsula, and if either side ratchets up the rhetoric, the markets could again get jittery and the yen could gain ground.

The Japanese economy has shown signs of improvement, and this was underscored as Preliminary GDP in Q2. Japan has now posted a sixth consecutive of growth, marking the longest expansion in over a decade. Although exports have declined, domestic demand has rebounded. With a tight labor market and the business sector confident about economic conditions, better times could continue in 2017. The fly in the ointment remains inflation, as BoJ's ultra-easy monetary policy has failed to eliminate the threat of deflation. The BoJ has insisted that it will not tighten policy before inflation climbs closer to the bank's inflation target of 2%, but clearly this goal is unrealistic in the short term, and the BoJ may have to lower its inflation target.

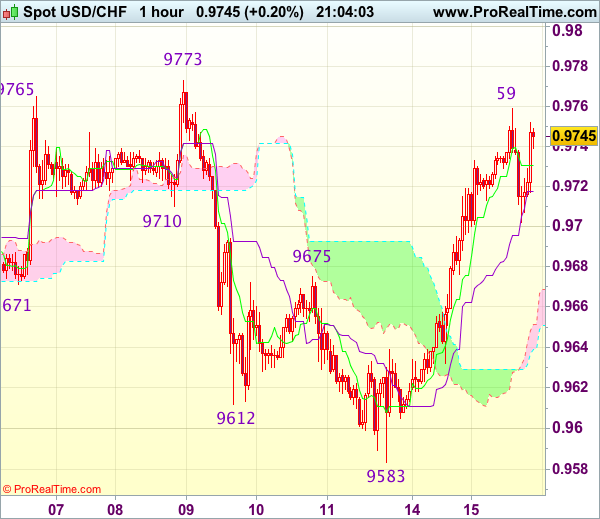

Trade Idea Update: USD/CHF – Buy at 0.9695

USD/CHF - 0.9734

Original strategy :

Buy at 0.9695, Target: 0.9795, Stop: 0.9660

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9695, Target: 0.9795, Stop: 0.9660

Position : -

Target : -

Stop : -

As the greenback has continued heading north after this week’s anticipated rally, suggesting the retreat from 0.9773 has ended at 0.9583, hence consolidation with upside bias remains for another test of said resistance, however, break there is needed to confirm early rise from 0.9438 low has resumed and extend gain to 0.9808 and possibly 0.9825 resistance, however, near term overbought condition should limit upside and price should falter below previous support at 0.9859.

In view of this, we are looking to reinstate long on pullback as 0.9695-00 should limit downside and bring another rise later. Below previous resistance at 0.9675 would defer and risk weakness towards 0.9640 but downside should be limited to 0.9615-20 and bring another rise later.