Sample Category Title

GBP/USD Just A Minor Pullback?

Price is bloodless right now, the participants are undecided ahead the US data release. The US figures will bring life on this pair. GBP/USD remains bullish as long as the 1.3046 and the warning line (wl1) are still intact, a breakdown below these obstacles will signal a major drop.

Canadian Dollar Steady Ahead of US, Canadian Job Reports

The Canadian dollar continues to trade quietly, as USD/CAD has inched lower in the Friday session. Currently, the pair is trading at 1.2570, down 0.10% on the day. Canada and the US will both release key employment numbers in the North American session, so traders should be prepared for movement from the pair. In the US, Nonfarm Payrolls is expected to slow to 182 thousand, while wage growth is forecast to edge up to 0.3%. In Canada, employment change is expected to post a gain of 13.1 thousand, after last month's huge gain of 45.3 thousand.

The Canadian dollar has enjoyed a strong run, gaining 7.8% against the greenback since May 1. The Canadian economy has improved, thanks to stronger global demand and higher oil prices. In July, the Bank of Canada raised interest rates from 0.50% to 0.75%, marking the first rate hike since 2009. The Canadian dollar jumped to an 11-month high after the rate increase, and investors will be monitoring the bank carefully – hawkish statements could lift the currency. The BoC holds its next policy meeting on September 6.

Janet Yellen & Co. continue to talk about the possibility of a December rate hike, but with the odds for a December increase pegged at just 42%, it's clear that the markets are skeptical about a third rate hike in 2017. Investor attention has shifted to the Fed's balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed's plans this week, in a clear message that was likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had 'fully recovered' from the 2008 financial crisis and called on the Fed to start trimming the balance sheet 'this fall'. Williams added that the process would be gradual and would take four years to reduce the balance sheet to a 'reasonable size'. On Wednesday, two other FOMC members also came out in support of starting to taper the balance sheet – St. Louis Fed President James Bullard and Cleveland Fed President Loretta Mester.

With the Federal Reserve widely expected to begin trimming its balance sheet next month, how will this affect the US dollar? The Fed is expected to initiate the wind-down by not replacing maturing bonds, which will reduce the balance sheet by $200 billion in 2017, according to the Institute of International Finance (IFF). The IFF estimates that this would be equivalent to three normal interest hikes, so the greenback should head upwards once the Fed starts winding down its bloated balance sheet.

Euro In Holding Pattern Ahead Of US Nonfarm Payrolls

EUR/USD has inched higher in the Friday session. Currently, the pair is trading at 1.1880, up 0.10% on the day. On the release front, German Factory Orders climbed 1.0%, beating the estimate of 0.6%. Eurozone Retail PMI slowed to 51.0, marking a 4-month low. In the US, the focus will be on employment data. Nonfarm Payrolls is expected to slow to 182 thousand, while wage growth is forecast to edge up to 0.3%.

German indicators continue to point to an expanding German economy. Retail Sales jumped 1.1%, its second-highest gain in 2017. Factory Orders gained 1.0%, while unemployment claims dropped 9 thousand – the indicator has declined every month in 2017 except one. Although the manufacturing and services PMIs dipped in July, both are well over the 50-level, indicative of expansion. The strong German numbers have helped boost the eurozone economy. Eurozone GDP gained 0.6% in the second quarter, up from 0.5% in the previous quarter. As well, Eurozone Retail Sales gained 0.5%, marking a 4-month high.

Federal Reserve policymakers continue to talk about the possibility of a December rate hike, but with the odds for a December increase pegged at just 42%, it’s clear that the markets are skeptical about a third rate hike in 2017. Investor attention has shifted to the Fed’s balance sheet, which stands at $4.2 trillion. Fed policymakers have broadly hinted at reducing purchases of bonds and securities starting in September, but San Francisco Fed President John Williams was more forthcoming about the Fed’s plans this week, in a clear message that was likely aimed at giving notice to the markets. In a speech on Wednesday, Williams said that the economy had “fully recovered” from the 2008 financial crisis and called on the Fed to start trimming the balance sheet “this fall”. Williams added that the process would be gradual and would take four years to reduce the balance sheet to a “reasonable size”. On Wednesday, two other FOMC members also came out in support of starting to taper the balance sheet – St. Louis Fed President James Bullard and Cleveland Fed President Loretta Mester.

How will the Fed’s trimming of the balance sheet affect the US dollar? The Fed is widely expected to begin the process in September, by not replacing maturing bonds, which will reduce the balance sheet by $200 billion in 2017, according to the Institute of International Finance (IFF). The IFF estimates that this would be equivalent to three normal interest hikes, so the greenback should head upwards once the Fed starts winding down its bloated balance sheet.

Strategy: Capex Set To Add Support To Global Recovery

Key points

- The outlook for global investments is becoming more positive

- A self-reinforcing capex recovery could strengthen global growth and leaves upside risk to our global growth forecasts

- We look for equities and bond yields to range trade before moving higher next year

- EUR/USD to continue higher

Investment growth has been the weak link in the global economy over the past three years. While private consumption was underpinned by robust real income growth - partly due to very low inflation - investments have been depressed. Political uncertainty, frequent shocks to the economy and depressed energy investments following the oil price collapse in 2014 kept corporate spending in check.

However, the scope for strengthening capital expenditure (capex) has increasingly been raised as a force that could make the global recovery more robust and resilient. Central banks such as the ECB and the Bank of England have also highlighted that stronger investment growth could increase the neutral rate for monetary policy and warrant higher rates in the future just to keep the policy stance unchanged.

In his speech in Sintra in June, ECB president Mario Draghi said: 'There is newfound confidence in the reform process, and newfound support for European cohesion, which could help unleash pent-up demand and investment… As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments – not in order to tighten the policy stance, but to keep it broadly unchanged.' The Bank of England governor Mark Carney similarly said that 'If these [investment] intentions are realised, the global equilibrium interest rate could rise somewhat, making a given policy setting more accommodative.'

Below we look at the scope for capex growth to enter a self-reinforcing cycle that strengthens the global recovery. Recent developments do indeed give rise for cautious optimism when it comes to investments. Some of the important drivers for investment growth have proven to be business sentiment, profit growth, financing costs and potential pent-up demand for investments following a period of depressed investments. Some of these factors are clearly correlated as stronger profit growth tends to lift business optimism. But low financing costs for example may become more stimulative if optimism is high and may not be enough to trigger investments if the outlook is uncertain and demand is weak. Hence, it could very well be that the positive effect of low yields and rates strengthens as the recovery takes hold.

Going through the above factors does indeed point to a more positive picture for investments:

First, business confidence in the OECD area is now the highest since 2011. As the global economy has gained steam companies have grown more optimistic. Reduced political uncertainty has probably added to the more upbeat expectations among companies in continental Europe. While Donald Trump has disappointed when it comes to the outlook for tax cuts and reduced regulation, corporate optimism is still quite high. In the Philadelphia Fed survey the index for capex expectations is now the highest in close to 30 years.

Second, profit growth picked up in late 2016 and early 2017 as the global economy gained steam and rising producer prices benefited the bottom line in many companies. When companies make money they are naturally more inclined to invest than when profits are falling.

Third, financing costs are historically low. In the euro area five-year corporate real yields are around zero (using core inflation as deflator) and in the US it is just around 1%. The average prior to the financial crisis was around 3½%. Fourth, there may very well be pent-up demand on the investment side. Investments as a share of GDP are still below the average prior to the financial crisis. This is most pronounced in the euro area. As the outlook improves and uncertainty declines some of this pent-up demand may come through.

The rising potential for a self-reinforcing cycle in investments poses some upside risks to our growth outlook for the coming years. And if it materialises it will put upward pressure on bond yields as demand for capital increases and central bank policy normalisation may happen faster.

Euro area growth revised higher

In Euro Area Research: Tail winds to growth dominate EUR headwind near-term published today, we have upgraded our euro area GDP forecast for 2017 to 2.0% from 1.7%. GDP for Q2 released this week increased by 0.6% q/q - the highest since 2011 - and we see several tailwinds lending support to the euro recovery: pent-up demand for investments (as mentioned above), fading political uncertainty, very strong sentiment and ongoing job creation. Despite a decline in real wage growth, consumer confidence has stayed very high and retail sales growth continued at a robust pace. However, in 2018 we expect the stronger euro to start to feed through to exports and we have lowered our GDP forecast to 1.5% from 1.6%.

What could rock the boat? North Korea and trade

While the outlook has improved, what could rock the boat and change this more positive picture? The two main candidates for creating uncertainty are a trade war started by US protectionist measures and a further escalation of the North Korean crisis.

Recently tensions have increased between the US and China as Trump has become critical again of Chinese efforts to put pressure on North Korea to stop its nuclear ambitions. At the same time there have been many reports that Trump is preparing trade measures to protect the US from what he sees as unfair trade practices by the EU and China. Secretary of Commerce Wilbur Ross this week wrote an opinion column in the Wall Street Journal called “Free trade is a two-way street” in which he argued that the US was the most free trading country in the world and countries/blocs that preached free trade (China and the EU) were much more protectionist than the US. Ross said this would change under Trump. The timing of any measures is highly uncertain. It may still take some time given all the other issues that are keeping Trump busy. But it seems likely that some protectionist measures will eventually come. Whether it triggers a trade war or not is hard to say. The risk is definitely there. But it is too early to say if it is serious enough to derail the global recovery.

When it comes to North Korea, the regime in Pyongyang is clearly advancing much faster than expected on the technological front. The second missile test in July of an intercontinental ballistic missile was even more advanced than the first and according to experts if it had been fired at a lower angle it would have been able to reach big cities on the US east coast. The problem is significant as any military strike on North Korea could cause significant loss of life in South Korea and possibly Japan. On the other hand, Trump has been clear he will not allow North Korea to reach its goal of being able to hit the US with a nuclear warhead - a technological position that North Korea is fast approaching.

Market volatility low - yields to range trade still

With a positive global macro picture and subdued inflation risk assets have continued to perform and volatility has become very low. Euro area stocks have been the exception lately with equity prices having moved lower - partly due to the significant strengthening of the euro. We are neutral on equities versus cash in the medium term (3-6M) as we believe that we are in the interim period between two reflation waves in which the market will be range trading. Longer term, though, equities are expected to outperform as the global recovery is set to continue, barring any major shocks.

Core government bond yields are expected to range trade for the remainder of 2017 as inflation pressures are very subdued still and central banks likely to move slowly. The ECB has been challenged by the strengthening of the euro lately, and in the US lower core inflation and wage growth are putting the Fed on hold on rates until the end of the year and keeping the hiking path next year very moderate.

We look for EUR/USD to continue on an upward trend over the next year and have a target of 1.22 in 12M. Gravity is pulling the USD lower still as it has been overvalued for some time on our MEVA models and current account flows work in favour of the euro area. Stronger growth performance in the euro area is also supportive of the EUR

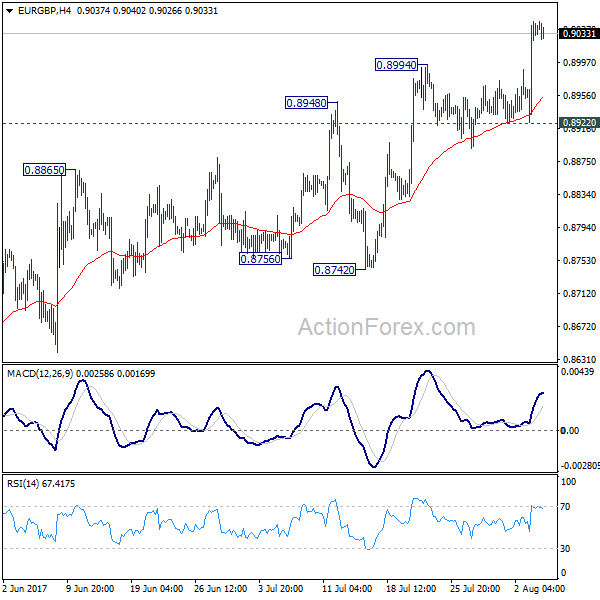

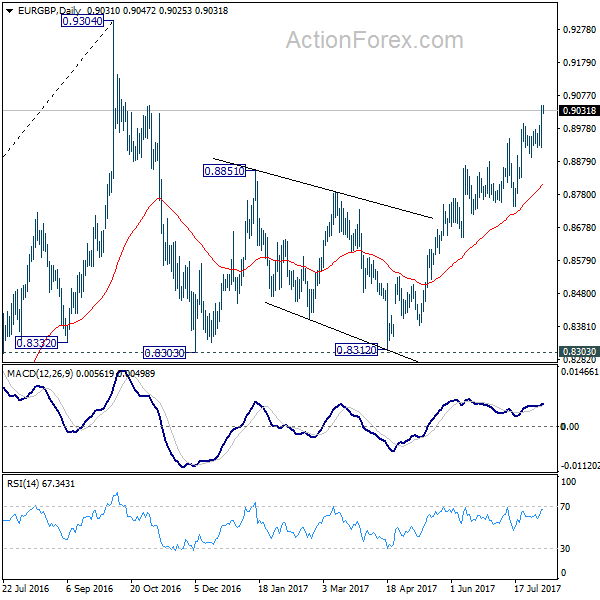

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8953; (P) 0.9001; (R1) 0.9079; More

Intraday bias in EUR/GBP remains on the upside for the moment. Current rally from 0.8312 is targeting 0.9304 key resistance level. At this point, there is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall. However, break of 0.8922 support is needed to be the first sign of short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

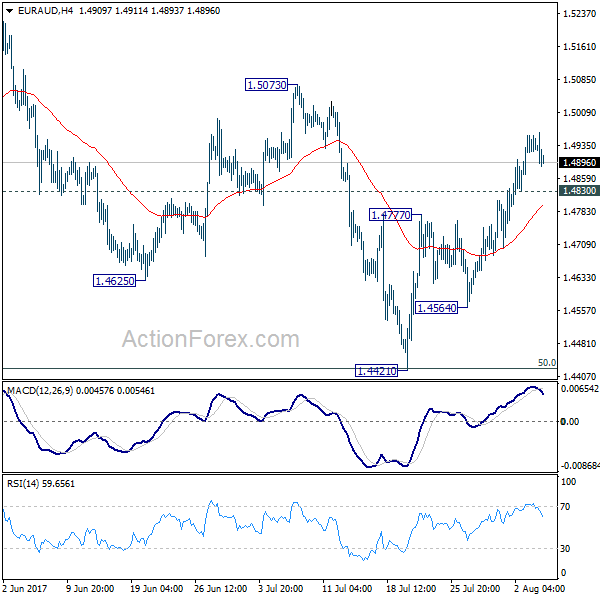

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4881; (P) 1.4919; (R1) 1.4970; More...

EUR/AUD lost some upside moment with 4 hour MACD crossed below signal line. But further rise is in favor with 1.4830 minor support intact. As noted before, correction from 1.5226 should have completed with three waves down to 1.4421 already. Break of 1.5073 will likely resume the rise from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4421 at 1.5411 next. On the downside, below 1.4830 minor support will turn intraday bias neutral first. But outlook will stay cautiously bullish as long as 1.4777 resistance turned support holds.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, another decline will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

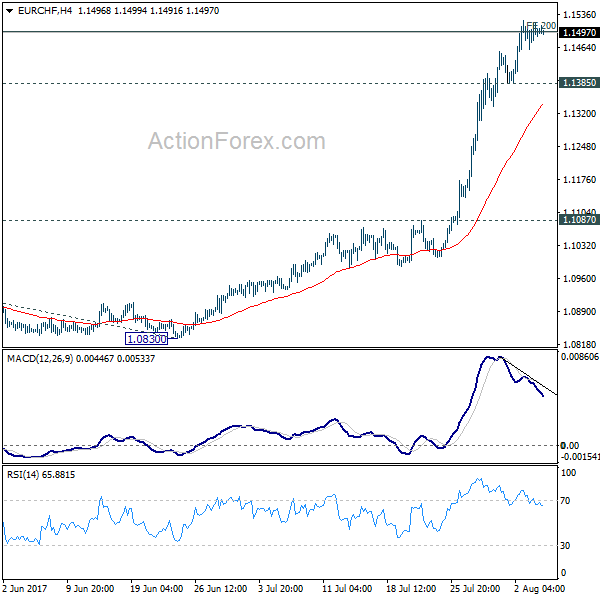

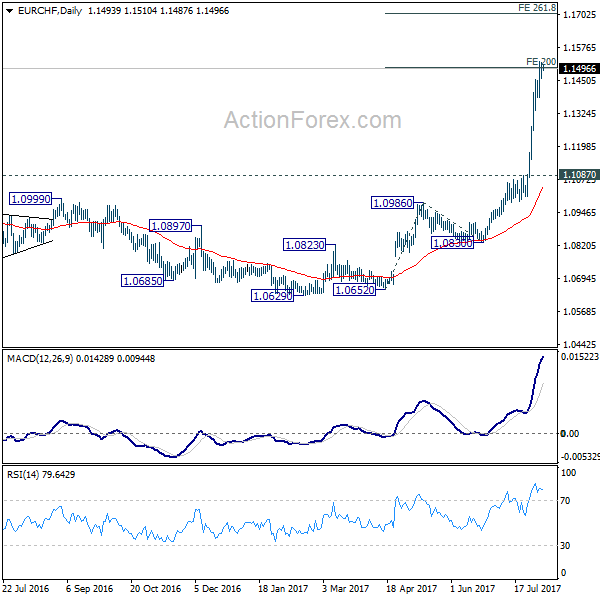

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1462; (P) 1.1490; (R1) 1.1521; More...

EUR/CHF turned sideway after meeting 200% projection of 1.0652 to 1.0986 from 1.0830 at 1.1498. But there is no clear sign of topping yet. Further rise is expected as long as 1.1385 minor support holds. Sustained trading above 1.1498 will target 261.8% projection at 1.1704 next. Nonetheless, considering bearish divergence condition in 4 hour MACD, break of 11385 support will indicate short term topping and bring lengthier consolidation first.

In the bigger picture, sustained break of 1.1198 key resistance confirms resumption of the long term rise from SNB spike low back in 2015. In this case, EUR/CHF would eventually head back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1087 resistance turned support holds.

Market Update – European Session: Quiet Session Ahead Of US Jobs Report

Notes/Observations

Awaiting US payroll data; markets for a weaker-than-expected nonfarm report

Overnight

Asia:

Japan Jun Labor Cash Earnings Y/Y: -0.4% v +0.5%e; Real Cash Earnings Y/Y: -0.8% v +0.1%e; data interrupts a 13-month trend of steady small wage gains

Australia Jun Retail Sales saw a slight beat; M/M: 0.3% v 0.2%e; Retail Sales Ex Inflation Q/Q: 1.5% v 1.2%e

RBA Quarterly statement noted that holding policy steady consistent with growth and inflation targets; recent rise in AUD currency had a modest effect on economic forecasts

Europe:

BoE Deputy Gov Broadbent: UK inflation is nearing its peak; likely rates will have to rise more than markets think (in-line with Aug BOE minutes)

Americas:

Special Counsel Mueller reportedly impanels grand jury in Russia probe suggesting that the investigation is growing in intensity and entering new phase and may continue for months to come.

Energy:

Saudi Oil Min reportedly met recently with commodity hedge funds to ask views of oil market and price outlook; sought advice on whether OPEC should target longer-dated prices

Economic Calendar

(DE) Germany Jun Factory Orders M/M: 1.0% v 0.5%e; Y/Y: % v 4.4%e

(DE) Germany July Construction PMI: 55.8 v 55.1 prior

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2029, 2033 and 2055 bonds

(ZA) South Africa sold total ZAR650M vs. ZAR650M indicated in 2029, 2033 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 flat at 3,465, FTSE +0.2% at 7,487, DAX flat at 12,158, CAC-40 +0.1% at 5,136, IBEX-35 +0.1% at 10,561, FTSE MIB -0.2% at 21,748, SMI -0.1% at 9,124, S&P 500 Futures +0.01%]

Market Focal Points/Key Themes: European stocks trading mixed; stronger Euro putting damper on equities; gold and copper rose but didn't help materials stocks much; oil slightly lower with energy stocks mixed; general theme of sideways trading; political uncertainty affecting risk sentiment; focus on NFP to be released later; upcoming US earnings releases include Cooper Tire, Cigna and Newell Brands

Equities

Consumer discretionary: Pearson PSON.UK -1.3% (earnings), Merlin Entertainment MERL.UK +1.8% (earnings), RPS Group RPS.UK +4.2% (earnings)

Industrials: Aalberts AALB.NL +2.8% (analyst action), Andritz ANDR.AT -8.2% (results)

Financials: Swiss Reinsurance RUKN.CH -0.1% (earnings), Hargreaves Lansdown HL.UK -4.8% (to not pay Div), Royal Bank of Scotland RBS.UK +2.7% (earnings)

Technology: STMicroelectronics STM.FR -1.9% (analyst action)

Telecom: MASmovil MAS.ES -6.3% (analyst action)

Healthcare: Fagron FAGR.BE +6.0% (results)

Speakers

Italy Stats Agency (Istat) Monthly Economic Note: Domestic economy moving in a positive direction

Sweden Think Tank NIER Economic updated its economic outlook which raised 2017 GDP from 2.5% to 3.0%but trimmed 2018 GDP from 2.4% to 2.2%. It also raised its 2017 CPI forecast from 1.7% to 1.9%

South Africa ANC Parliament chief whip Mthembu: Party cannot vote in favor of a motion that would collapse the govt

Indonesia Central Bank stated that it saw room to ease policy if inflation was manageable. Reiterated view that 2017 GDP growth was seen between 5.0-5.4% with growth momentum shifting to Q3

Currencies

FX markets were quiet ahead of the key US payroll data. Overall analysts believe the USD is likely to stay under pressure due to the uncertainty of the effectiveness of the Trump Administration in getting its promises through. Also a headwind for the greenback was reports that the Special Counsel Mueller had impaneled a grand jury in Russia probe suggesting that the investigation was growing in intensity and entering new phase and could continue for months to come.

Fixed Income

Bund futurestrades at 163.28 down 2 ticks consolidating after sharp rises yesterday. Initial resistance stands 163.48 followed by 163.78. Support lies at 163.08 initially with further retracement targeting 162.79.

Gilt futurestrades flat at 126.86 consolidating after a more dovish BoE yesterday which saw Gilts rise above 127 yesterday. A move back higher targets 127.20 then 127.51, with downside support at 126.51.

Friday's liquidity report showed Thursday's excess liquidity fell to €1.735T down €1B from €1.736T prior. Use of the marginal lending facility fell to €247M from €253M prior.

Corporate issuancesaw $just over $5B come to market via 4 issuers taking weekly issuance to $25.6B. Capital One and Kinder Morgan accounted for the majority of the issuance. For the week ending August 2nd IG Funds reported inflows of $1.49B, while High Yields funds reported inflows of $0.195B

Looking Ahead

(RO) Romania Central Bank (NBR) Interest Rate Decision: Expected to leave Interest Rates unchanged at 1.75%

05:30 (ZA) South Africa to sell combined ZAR650M in 2029, 2033 and 2046 bonds

06:00 (IE) Ireland Jun Industrial Production M/M: No est v 2.1% prior; Y/Y: No est v 5.5% prior

06:00 (UK) DMO to sell combined £2.0B in 1-month, 3-month and 6-month bills (£0.5B, £1.0B and £1.5B respectively)

06:45 (US) Daily Libor Fixing

07:30 (TR) Turkey July Real Effective Exchange Rate (REER): No est v 91.38 prior

07:30 (IN) Weekly India Forex Reserves

08:30 (US) July Change in Nonfarm Payrolls: +180Ke v +222K prior; Change in Private Payrolls: +180Ke v +187K prior; Change in Manufacturing Payrolls: +5Ke v +1K prior

08:30 (US) July Unemployment Rate: 4.4%e v 4.4% prior; Underemployment Rate: No est v 8.6% prior; Labor Force Participation Rate: No est v 62.8% prior

08:30 (US) July Average Hourly Earnings M/M: 0.3%e v 0.2% prior; Y/Y2.4%e v 2.5% prior; Average Weekly Hours: 34.5e v 34.5 prior

08:30 (US) Jun Trade Balance: -$44.5Be v -$46.5B prior

08:30 (CA) Canada July Net Change in Employment: +12.5Ke v +45.3K prior; Unemployment Rate: 6.5%e v 6.5% prior; Full Time Employment Change: No est v +8.1K prior; Part Time Employment Change: No est v +37.1K prior; Participation Rate: No est v 65.9% prior

08:30 (CA) Canada Jun Int'l Merchandise Trade (CAD): -1.3Be v -1.1B prior

09:00 (MX) Mexico May Gross Fixed Investment: 2.0%e v -8.6% prior

10:00 (CA) Canada July Ivey Purchasing Managers Index (Seasonally Adj): No est v 61.6 prior; PMI (unadj): No est v 63.9 prior

10:20 (BR) Brazil July Vehicle Production: No est v 212.3K prior; Vehicle Sales: No est v 195.0K prior; Vehicle Exports: No est v 66.1K prior

11:00 (EU) Potential Sovereign ratings following European close

(IS) Israel Sovereign Debt to be rated by S&P

(KW) Kuwait Sovereign Debt to be rated by S&P

(SE) Sweden Sovereign Debt to be rated by Moody's

(SK) Slovakia Sovereign Debt to be rated by Fitch

(SE) Sweden Sovereign Debt to be rated by Fitch

13:00 (US) Weekly Baker Hughes Rig Count data

14:00 (CO) Colombia Central Bank Monetary Policy Minutes

15:00 (CO) Colombia July PPI Domestic M/M: No est v -0.1% prior; Total PPI M/M: No est v -0.5% prior

Sat

13:00 (CO) Colombia July CPI M/M: No est v 0.1% prior; Y/Y: No est v 4.0% prior

PRE-NFP Coverage: EUR/USD Still Bullish But Watch The Wage Data

The NFP with Average Hourly Earnings data will be the most important today for the EUR/USD currency. The ADP missed the forecast (178k vs 187k) but it was revised higher - 191k. It implies that the NFP might not be the most important data today, but rather it will be the wage data. However, traders should be paying attention to both as the NFP might come close to 180k due to a lot of seasonal work, for tourism.

Technical analysis is showing a clear narrowing channel with a trend line that might become an inner trend line if broken to the upside. An upside break of 1.1890 should target 1.1905, 1.1932 and 1.1958. However if the price gets below the channel than POC 1.1835-50 (D L4, W H4, EMA89, ATR pivot) and/or POC2 1.1800-1.1810 ( W H3, ATR low, D L5) should provide potential rejections. The pair is still in uptrend so buying the dips could happen should the price retrace to POC zones.

Bulls should keep 1.1795 intact, as if it breaks it might be a signal for a potential reversal down to 1.1700.

Technical Outlook: AUDUSD Higher After Australian Data, Eyes US Jobs Report For Fresh Signal

The Aussie dollar is standing higher on Friday, boosted by better than expected Australian retail sales and positive outlook for Australian economy from RBA's Monetary Policy statement.

In addition, Thursday's strong downside rejection signaled that easing after multiple failure above 0.8000 handle might be losing traction.

Fresh strength today was also attracted by 4-hr cloud twist and dented initial barrier at 0.7971 (daily Tenkan-sen) close above which would bring the price into familiar area, where it was congested in past few sessions.

Overall structure is bullish and favors further upside, with final break and close above 0.8000 barrier (previous upticks failed to close above) to signal resumption of broader uptrend towards Fibo 50% barrier at 0.8164.

Conversely, fresh weakness through yesterday's low at 0.7913 would expose lower pivot at 0.7877 (Fibo 38.2% of 0.7572/0.8065, reinforced by rising 20SMA) and risk deeper pullback on break.

US jobs data are expected to give fresh direction signal.

Res: 0.7979, 0.8000, 0.8042, 0.8065

Sup: 0.7933, 0.7913, 0.7877, 0.7818