Sample Category Title

CAC Slips As French CPI And Consumer Spending Decline

The CAC index has posted sharp losses in the Friday session. The CAC is currently at 12,116.00, down 1.33% on the day. On the release front, it's a busy day for French indicators. Consumer spending came in at -0.8%, missing the estimate of -0.3%. On the inflation front, Preliminary CPI declined 0.3%, just above the forecast of -0.4%. This marked the indicator's weakest reading since January. There was better news from Flash GDP, which improved to 0.5% in the second quarter, matching the forecast. This was the strongest quarter of growth since Q1 in 2016. Later in the day, the US releases Advance GDP, with the estimate standing at 2.5%. If GDP is not within expectations, we could see some volatility from French stock markets.

It's become an all-too-familiar pattern out of Washington – trouble for the White House has translated into losses on global stock markets, as higher political risk has made investors jittery. It was déjà vu on Thursday, as President's struggling healthcare bill gasped its final breath as the bill was defeated in the Senate after three Republican lawmakers joined the Democrats and voted against the bill. This is another setback for President Trump, who has been unable to get Congress to pass any significant legislation, despite the Republicans controlling both the House and the Senate. Trump will now be able to focus on other issues such as tax reform, but investors are skeptical as to whether the President will have the support he needs in Congress to pass major legislation.

With the Federal Reserve holding rates at 1.25% at this week's policy meeting, the markets focused on the rate statement, as investors looked for clues about future rate moves. The statement was cautiously optimistic in tone, with policymakers saying that the economy was growing at a moderate pace and that the labor market remained strong. The statement made note of low inflation, but said that the Fed expected the economy to continue to expand. Another key issue on the Fed's plate is the $4.2 trillion balance sheet. The rate statement said that the Fed plans to taper asset purchases 'relatively soon', which is a likely nod at September as the start date. This would involve the Fed tapering its purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Although the Fed continues to talk about another rate hike in 2017, investors remain skeptical. The rate statement did not change many minds, as the odds of rate increase in December stand at 47%, according to the CME Group.

BoJ Summary Of Opinions Suggests Less Appetite For Stimulus

Overnight, the Bank of Japan released the summary of opinions from its July policy meeting. The summary is released ahead of the minutes, and outlines the individual views of BoJ policymakers. It was very interesting to see that some officials expressed a desire to wind down their ultra-loose stimulus program somewhat. One opinion was that the Bank should reduce its annual purchases of JGBs to 45 trillion JPY, from 80 trillion currently. Another indicated the BoJ should place more emphasis on financial stability and thus, it should abolish yield-curve control altogether. Finally, a third view was that the Bank's target level of 10-year JGB yields of 'around zero percent' should not be interpreted too strictly, implying officials should be more tolerant of yields rising a bit higher than 0%.

The yen did not really react to these points, perhaps because market participants were not at all convinced the Bank will actually reduce its stimulus anytime soon. Even though we hold the same view given very subdued inflation, we will monitor incoming comments from BoJ officials very carefully. Any further signals in the foreseeable future that the 'hawkish' camp among the BoJ may be growing larger, could prove positive for the yen.

EUR/JPY traded lower yesterday after it hit resistance slightly below 130.70 (R1), the upper bound of the sideways range that has been containing the price action since the 6th of July. Given that the rate remains within that range, we maintain the view that the short-term outlook is flat for now. Having said that, given that yesterday's slide started after the pair tested the upper bound of the sideways path, it could continue lower for a while. Now, the pair is testing the 129.50 (S1) support line, where a decisive dip could open the way towards the lower bound of the range, at 128.60 (S2). Zooming out to the longer-term timeframes, we see that EUR/JPY is still trading above the prior downside resistance line drawn from the peaks of June 2015. As such, although the short-term path is to the sideways, we still consider the broader one to be positive.

Dollar rebounds somewhat ahead of GDP data

The US dollar recovered somewhat yesterday, ahead of today's 1st estimate of GDP for Q2. The forecast is for US economic growth to have accelerated notably, something supported by the Atlanta Fed GDPNow model. We believe these data will be closely watched, as they may prove critical for market expectations regarding the timing of the next Fed rate hike.

If growth regains momentum as anticipated, that would confirm the Fed's view that the slowdown in Q1 was only transitory, and is likely to increase speculation regarding another rate hike this year. Something like that could help the dollar recover some more of its latest losses. That said though, even in that case we think that the currency's short-term outlook could remain negative. We believe that a strong rebound in inflation is needed before rate-hike expectations rise materially and help the dollar reverse its latest downtrend.

USD/CAD traded higher yesterday after it hit support at 1.2415 (S2) and then, it emerged above the 1.2525 (S1) line. The price structure still suggests a downtrend but for now, we see the likelihood for yesterday's rebound to continue a bit more. Accelerating US GDP combined with a flat growth rate in Canada, later in the day, could prove the trigger for the continuation of yesterday's corrective wave. A break above 1.2615 (R1) would confirm the case and may pave the way for extensions towards the next resistance of 1.2700 (R2).

As for the rest of today's highlights:

During the European morning, Germany's preliminary CPI data for July will be in focus. The forecast is for the nation's inflation rate to have ticked down. Even though such a decline could reverse some of the euro's latest gains, given that Germany does not report a core CPI rate, we believe investors will focus primarily on Eurozone's core CPI print due out Monday in order to gauge when and how the ECB may act next. From Sweden, we get GDP data for Q2 and expectations are for growth to have accelerated notably from the previous quarter, which could support SEK. We also get the nation's retail sales for June.

From Canada, as we already noted, we get GDP data for May and expectations are for an unchanged rate of growth. If that is indeed the case, the reaction in CAD may be limited.

We have only one speaker on the agenda: Minneapolis Fed President Neel Kashkari.

EUR/JPY

Support: 129.50 (S1), 128.60 (S2), 128.00 (S3)

Resistance: 130.70 (R1), 131.60 (R2), 132.20 (R3)

USD/CAD

Support: 1.2525 (S1), 1.2415 (S2), 1.2300 (S3)

Resistance: 1.2615 (R1), 1.2700 (R2), 1.2770 (R3)

DAX Loses Ground As Trump Loses Healthcare Vote, German CPI Next

The DAX index remains under pressure in the Friday session. In the European session, the DAX is at 12,125, down 0.79% on the day. On the release front, German Preliminary CPI is expected to remain unchanged at 0.2%. Later in the day, the US releases Advance GDP, with the estimate standing at 2.5%. If GDP is not within expectations, we could see some volatility from the German stock markets.

The German economy continues to impress, powered by strong global demand for German products and solid domestic demand. Consumers continue to give a thumbs-up to the economy, as underscored by GfK German Consumer Climate. The indicator strengthened for a fourth straight month, improving to 10.8 in the July report. This edged above the estimate of 10.7 points. Importantly, strong consumer confidence has translated into increased consumer spending, a key driver of economic growth. However, the fly in the ointment remains inflation, which is stuck at low levels. The lack of inflation is a pressing concern for ECB policymakers, and there is little chance that the bank will end its quantitative easing program before December, if inflation levels don’t move upwards.

Global stock markets remain jittery as political risk in Washington continues to intensify. On Thursday, Trump’s troubled healthcare bill gasped its last breath, as the bill was defeated in the Senate after three Republican lawmakers joined the Democrats and voted against the bill. This is another setback for President Trump, who has been unable to get Congress to pass any significant legislation, despite the Republicans controlling both the House and the Senate. Trump will now focus on other issues such as tax reform, but investors are skeptical as to whether the President will have better luck with other bills.

With the Federal Reserve holding rates at 1.25% at this week’s policy meeting, attention shifted to the rate statement, as investors looked for clues about future rate moves. The statement was cautiously optimistic in tone, with policymakers saying that the economy was growing at a moderate pace and that the labor market remained strong. The statement made note of low inflation, but said that the Fed expected the economy to continue to expand. Another key issue on the Fed’s plate is the $4.2 trillion balance sheet. The rate statement said that the Fed plans to taper asset purchases “relatively soon”, which is a likely nod at September as the start date. This would involve the Fed tapering its purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Although the Fed continues to talk about another rate hike in 2017, investors remain skeptical. The rate statement did not change many minds, as the odds of rate increase in December stand at 47%, according to the CME Group.

Market Update – European Session: European Q2 GDP Data Shows Continued Improvement On The Growth Front

Notes/Observations

Senate 'skinny repeal' bill fails; GOP dealt stiff blow in Senate's bid to repeal 'Obamacare' (Republican Senators McCain, Murkowski and Collins all voted against the amendment)

European Q2 GDP coming in better-than-expected (France, German , Sweden YoY beat)

Overnight

Asia:

Japan Jun Jobless Rate matched lowest rate since Jun 1994 ( 2.8% 3.0%e); Job-To-Applicant Ratio saw its 4th month of improvement and highest since 1974 (1.51 v 1.50e)

Japan Jun Overall Household Spending registered its 1st rise in 16 months and largest increase since Aug 2015) Y/Y: (+2.3% v +0.5%e)

Japan Jun National CPI rose for the 6th straight month in June but failed to gain momentum (Y/Y: 0.4% v 0.4%e; CPI Ex Fresh Food (Core) Y/Y: 0.4% v 0.4%e; CPI Ex Fresh Food, Energy (Core-core) Y/Y: 0.0% v -0.1%e

Bank of Japan (BOJ) Summary of Opinions for the July 19-20 policy meeting reiterates CPI likely to approach 2% around FY19 (in-line with new timeline). Reiterated that no additional easing was necessary as price momentum had been maintained

South Korea Jun Industrial Production M/M: -0.2% v +1.9%e; Y/Y: -0.3% v +1.3%e - China FX Regulator SAFE: Will safeguard and increase value of forex reserves; Will crackdown on 'forex irregularities', including underground banks

Europe:

July GfK Consumer Confidence: -12 v -11e

UK Home Sec Rudd: EU citizens will be still allowed to come to the UK to live and work after Brexit as long as they register with Home Office

Chancellor of Exchequer Hammond (Fin Min) said to seek a two phase Brexit starting with an "off the shelf" transition period. Believes the two phases should end by 2022 and does not believe there was enough time for bespoke deal to be negotiated before April 2019

Americas:

Speaker Ryan, Maj Leader McConnell and Sec Mnuchin release joint statement on tax reform; plan to move it through committee in the autumn

Fed nominee Quarles: Do not support the adoption of the Taylor rule to guide monetary policy

Economic Calendar

(NL) Netherland July Producer Confidence Index: 6.6 v 7.2 prior

(FR) France Q2 Advance GDP Q/Q: 0.5% v 0.5%e; Y/Y: 1.8% v 1.6%e

(NO) Norway Jun Retail Sales W/Auto Fuel M/M: -0.6% v +1.4% prior

(FR) France July Preliminary CPI M/M: -0.3% v -0.4%e; Y/Y: 0.7% v 0.7%e

(FR) France July Preliminary EU Harmonized CPI M/M: -0.4% v -0.4%e; Y/Y: 0.8% v 0.8%

(FR) France Jun Consumer Spending M/M: -0.8% v -0.4%e; Y/Y: 0.5% v 1.0%e

(ES) Spain Q2 Preliminary GDP Q/Q: 0.9% v 0.9%e; Y/Y: 3.1% v 3.0%e

(ES) Spain July Preliminary CPI M/M: -0.7% v -0.8%e; Y/Y: 1.5% v 1.5%e

(ES) Spain July Preliminary CPI EU Harmonized M/M: -1.2% v -1.3%e; Y/Y: 1.7% v 1.6%e

(DE) Germany July CPI Saxony M/M: 0.3% v 0.2% prior; Y/Y: 1.7% v 1.7% prior

(CH) Swiss July KOF Leading Indicator: 106.8 v 106.0e

(TR) Turkey July Economic Confidence: 103.4 v 98.9 prior

(AT) Austria Q2 Preliminary GDP Q/Q: 0.9% v 0.7% prior; Y/Y: 2.2% v 2.5% prior

(SE) Sweden Q2 Preliminary GDP Q/Q: 1.4% v 0.9%e; Y/Y: 4.0% v 2.7%e

(DE) Germany July CPI Brandenburg M/M: 0.4% v 0.2% prior; Y/Y: 1.4% v 1.5% prior

(DE) Germany July CPI Hesse M/M: 0.4% v 0.1% prior; Y/Y: 1.9% v 1.9% prior

(DE) Germany July CPI Bavaria M/M: 0.4% v 0.1% prior; Y/Y: 1.6% v 1.4% prior

(AT) Austria July Manufacturing PMI: 60.0 v 60.7 prior (19th month of expansion)

(NO) Norway July Unemployment Rate: 2.8% v 2.8%e

(TW) Taiwan Q2 Preliminary GDP Y/Y: 2.1% v 2.2%e

(DE) Germany July CPI North Rhine Westphalia M/M: 0.4% v 0.1% prior; Y/Y: 1.8% v 1.6% prior

(PT) Portugal July Consumer Confidence: 1.1 v 0.8 prior; Economic Climate Indicator: 2.2 v 2.1 prior

(EU) Euro Zone July Business Climate Indicator: 1.05 v 1.14e ; Consumer Confidence: -1.7 v -1.7e

(DE) Germany July CPI Baden Wuerttemberg M/M: 0.4% v 0.1% prior; Y/Y: 1.7% v 1.6% prior

Fixed Income Issuance:

(IN) India sold total INR150B in 2024, 2027, 2034 and 2046 bonds

(IT) Italy Debt Agency (Tesoro) sold total €6.25B vs. €5.25-6.25B indicated range in 5-year and 10-year BTP Bonds

Sold €4.0B vs €3.5-4.0B indicated in new 0.90% Aug 2022 BTP; Avg Yield: 0.88% v 0.83% prior; Bid-to-cover: 1.34x v 1.28x prior

Sold €2.25B vs €1.75-2.25B indicated in 2.2% Aug 2027 BTP; Avg Yield: 2.16% v 2.16% prior; Bid-to-cover: 1.71x v 1.39x prior

(IT) Italy Debt Agency (Tesoro) sold total €1.5B vs. €1.0-1.5B indicated range in Oct 2024 CCTeu (Floating Rate Note); Avg Yield 0.77% v 0.83% prior; Bid-to-cover: 1.65x v 1.63x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -1.1% at 378, FTSE -0.7% at 7391, DAX -0.8% at 12112, CAC-40 -1.4% at 5113, IBEX-35 -0.8% at 10518, FTSE MIB -1.0% at 21417, SMI -0.7% at 8959, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices trade lower after another heavy bout of earnings, with the negative tone set by disappointing results from Amazon overnight. This morning key banking names reported, with good results out of Credit Suisse and BNP Paribas, while Barclays shares were in focus after charges related to its divestment of its African Unit, as well as provisions for miss selling PPI. Share of French Auto manufacturer Renault trades sharply lower after strong H1 results, but an affirmation of guidance disappointing the market. In Germany Adidas outperforms after raising outlook, and reporting strong prelim results. Looking ahead, notable earners include Loews, and Dana Hlds.

Equities

Consumer discretionary [Adidas [ADS.DE] +9% (Prelim results, raises outlook), Kering [KER.FR] -2% (Earnings), Essilor [EI.FR] -3.8% (Earnings), Air France [AF.FR] +0.9% (Earnings)]

Industrials: [Renault [RNO.FR] -6.2% (Earnings), Air Liquide [AI.FR] -2.4%, Safran [SAF.FR] -0.4% (Earnings), OHL [OHL.ES] -9% (Earnings)]

Financials: [Barclays [BARC.UK] +0.3% (Earnings), Credit Suisse [CSGN.CH] +1.9% (Earnings), UBS [UBSG.CH] -3.9% (Earnings)]

Speakers

Chancellor of Exchequer Hammond (Fin Min): Brexit transition could take up to three years, length to be determined by the facts

Ireland PM Varadkar said to be pushing for Irish Sea to become the post Brexit border with the UK. Warned UK PM May that her proposal for Irish Border was unworkable and would jeopardize Northern Ireland peace process

South Africa Central Bank (SARB) Gov Kganyago: Worst is behind on the growth situation; inflation outlook broadly balanced. CPI forecasts showed marked improvement but would not hesitate to reverse rates if inflation worsened

US Senate rejected the 'skinny' Obamacare repeal (as expected ). Republican Senators McCain, Murkowski and Collins voted against the amendment

Russia said to have ordered the US to reduce its diplomatic staff in the country to 455 in retaliation for more US sanctions (Staff number will reflect the same level as Russia diplomats in Washington)

Japan PM Abe's Adviser Nakahara: Japan should adopt a policy mix of fiscal and monetary instruments under a new BoJ chief. Govt should spend ¥100T on infrastructure projects by issuing 60-year bonds the next decade and have the BoJ buy some of them through the market

China Foreign Exchange Trade System (CFETS): To increase CNY currency (Yuan) Reference Rates release; effective July 31st (5 times vs. 2 times prior per day)

Currencies

USD was trying to muster more consolidation in the wake of its recent weakness. The spat of better European GDP and inflation data was giving the greenback some headwinds. A batch of European Q2 GDP came in better-than-expected with France, German, Sweden YoY readings all beating expectations

The SEK currency was the session outperformer following its GDP performance. The Kroner shaking off recent political events and firmed against the Euro. EUR/SEK moving from 9.59 to under 9.52 following the GDP beat.

Dealers noted that CHF currency weakness had been the main market theme this week as the SNB remained the lone dove central bank in Europe as its appeared to be drifting away from the stance of most other G10 central banks. USD/CHF above the 0.97 level while EUR/USD was edging closer towards the 1.14 level for its highest reading since the floor was removed back in Jan 2015

Fixed Income

Bund futures trade at 161.70 down 48 ticks extending its drop after the latest round of German regional CPI readings. Resistance lies near the 162.10 level followed by 162.75. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 126.20 lower by 18 ticks as global stock indices slide. Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.51 region, followed by 127.50.

Friday's liquidity report showed use of the marginal lending facility fell to €225M from €1.2B prior.

Corporate issuance saw $26B come to market via 4 issuers headlined by AT&T $22.5B -7part senior unsecured offering and American Express $2.25B senior unsecured note offering. This week's issuance is at $36.4B. For the week ending July 26th Lipper US fund flows reported IG funds net inflows $2.3B bringing YTD inflows to $77.5B, High yield funds reported outflows of $20.8M bringing YTD outflows to $6.7B.

Looking Ahead

(BE) Belgium July CPI M/M: No est v -0.2% prior; Y/Y: No est v 1.6% prior

(MX) Mexico Jun YTD Budget Balance (MXN): No est v 381.7B prior

05:30 (ZA) South Africa to sell combined ZAR650M in 2029, 2033 and 2046 I/L bonds

06:00 (DE) Germany July Preliminary CPI M/M: 0.2%e v 0.2% prior; Y/Y: 1.5%e v 1.6% prior

06:00 (DE) Germany July Preliminary CPI EU Harmonized M/M: 0.3%e v 0.2% prior; Y/Y: 1.4%e v 1.5% prior

06:00 (PT) Portugal Jun Industrial Production M/M: No est v 0.4% prior; Y/Y: No est v 2.4% prior

06:00 (IE) Ireland Jun Retail Sales Volume M/M: No est v 0.8% prior; Y/Y: No est v 3.3% prior

06:00 (UK) DMO to sell combined £2.05B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to leave 1-Week Auction rate unchanged at 9.00%

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil July FGV Inflation IGPM M/M: -0.6%e v -0.7% prior; Y/Y: -1.6%e v -0.8% prior

07:30 (IN) India Weekly Forex Reserves

08:00 (ZA) South Africa Jun Budget Balance (ZAR): +21.9Be v -21.2B prior

08:00 (BR) Brazil Jun National Unemployment Rate: 13.3%e v 13.3% prior

08:00 (UK) Baltic Dry Bulk Index

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming Bond issuance

08:30 (US) Q2 Advance GDP Annualized Q/Q: 2.5%e v 1.4% prior; Personal Consumption: 2.9%e v 1.1% prior (**Note: Revisions: GDP revised from 2014-16; reference yr remains 2009)

08:30 (US) Q2 Advance GDP Price Index: 1.3%e v 1.9% prior; Core PCE Q/Q: 0.7%e v 2.0% prior

08:30 (US) Q2 Employment Cost Index (ECI): 0.6%e v 0.8% prior

08:30 (CA) Canada May GDP M/M: 0.2%e v 0.2% prior; Y/Y: 4.2%e v 3.3% prior

09:00 (CL) Chile Jun Manufacturing Production Y/Y: 1.1%e v 1.9% prior; Industrial Production Y/Y: 1.2%e v 0.1% prior

09:00 (CL) Chile Jun Total Copper Production: No est v 469.2K tons prior

09:30 (BR) Brazil Jun Primary Budget Balance (BRL): -20.0Be v -30.8B prior; Nominal Budget Balance: -54.6 v -67.0B prior; Net Debt to GDP Ratio: 48.5%e v 48.1% prior

10:00 (US) July Final University of Michigan Confidence: 93.1e v 93.1 prelim

11:00 (EU) Potential sovereign ratings after European close

13:00 (US) Weekly Baker Hughes Rig Count data

13:20 (US) Fed's Kashkari (dove, FOMC voter) speaks at Townhall Event

Will US GDP Provide Bright Spark On An Otherwise Downbeat Day

- Amazon earnings weigh on sentiment;

- Obamacare “skinny repeal” fails to get past the Senate, threatening tax reform and spending;

- US and Canadian GDP releases eyed, as well as Kashkari comments.

Financial markets are set to open on a more downbeat note on Friday, with earnings from Amazon on Thursday being blamed for the initial underperformance along with the US Senate's inability to pass the “skinny repeal” of Obamacare.

While Amazon's results may only be responsible for some short term negativity, with the tech sector as a whole still enjoying a remarkable year, the failure in the Senate could pose further problems for President Donald Trump and his growth agenda. It's generally believed that the repeal of Obamacare will unlock the ability to cut taxes, a key policy of Trump's during the campaign and one that was partly responsible for such a strong post-election rally in equities, the dollar and rates.

Equity markets have been rather resilient to the delayed approval of tax cuts and spending measures that were intended to boost growth in the world's largest economy, from the currently below par levels. This has been aided by healthier earnings, as we've once again seen for the second quarter, despite the occasional blip, as we had with Amazon. Today is looking a little quieter but we will get numbers from Exxon Mobil, Merck and American Airlines, among others.

Friday is also looking a little quieter on the economic data side as well, with US and Canadian second quarter GDP the only notable releases. The US will be of particular interest, with expectations currently for quite a sizeable upward revision to 2.5% which would make the first half of the year not the shambles it first appeared. With inflation and jobs data still to come next week, it could also act as another incentive for the Fed to pursue another rate hike this year – although that's unlikely to come until December – with policy makers comfortable with the path the economy is on.

We'll also hear from Neel Kashkari later on today, a voter on the FOMC and arguably its most dovish member. While his comments will be of interest, being one of the few doves among a committee who's consensus is still to tighten does mean his comments possibly carry less weigh, as far as traders are concerned.

Yen Finds Support As Japanese Consumption And Employment Brighten In June

On early Thursday, the yen partially reversed yesterday's losses after statistics out of Japan showed a surprise improvement in domestic consumption and the labour market. This is said to put the BOJ's recent arguments for maintaining current policy into question and will likely encourage policymakers to scale back their ultra-loose stimulus program in the future.

In June, the unemployment rate in Japan beat forecasts according to the Japan Institute for Labour, falling from 3.1% in May to 2.8%, while analysts anticipated the figure to slip to 3% instead. The availability of jobs which is measured by the jobs to applications ratio rose slightly to 1.51, exceeding the 1.49 observed in the previous month and the 1.50 forecasted. Despite the marginal increase, the ratio climbed for the fourth consecutive month reaching the highest on record in 43 years.

Concerning consumption, household spending continued expanding in June, rising by 1.5% month-on-month, which was more than double the previous reading of 0.7%. The positive figure was a surprise, as based on forecasts, household expenditure was anticipated to decline by 0.1%. On a yearly basis, consumer spending turned positive for the first time in a year, climbing unexpectedly by 2.3%. The reading in May was down by 0.1%, whereas for the month of June, analysts expected a rise of 0.6%.

Separate data showed that retail sales experienced an increase as well, climbing by 0.1 percentage points to 2.1% and missing the forecast of 2.3%.

Looking at prices, national CPI was in line with expectations, remaining steady at 0.4% in June on an annual basis. Note that, CPI has followed an upward path since the beginning of the year. Excluding energy and food products, national core CPI did not change from 0.4% seen in May.

Last week, the BOJ decided to maintain its ultra-easy monetary policy under concerns that inflation will take more time to approach the target of 2%. However, the above data on employment conditions and consumption will likely motivate companies to raise prices sooner than anticipated and therefore increase stubbornly low wage growth. This would give a signal to BOJ policymakers to rethink their recent conclusions as inflation might not delay hitting the desired target after all.

In the forex markets, the data drove the yen higher against the greenback by 0.22%, with dollar/yen falling from 111.22, before the data release, to 110.98.

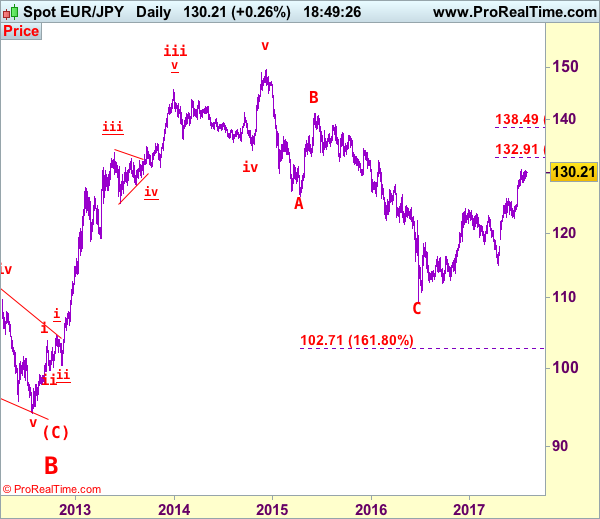

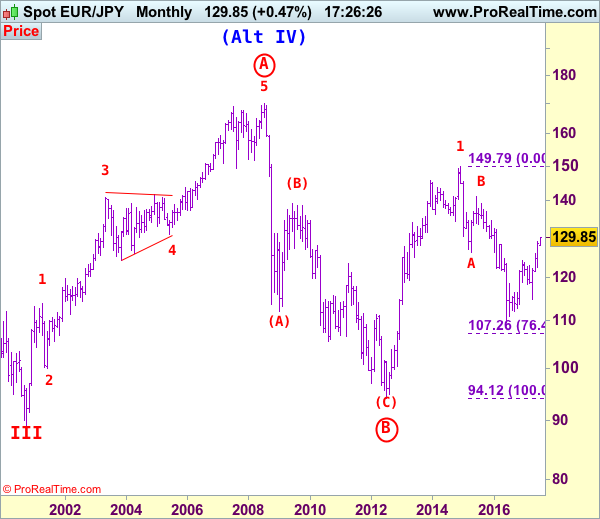

EUR/JPY Elliott Wave Analysis

EUR/JPY - 130.21

EUR/JPY: Wave v as well as larger degree wave (C) ended at 94.11 and first leg of larger degree wave C upmove has possibly ended at 149.79 and wave 2 correction has possibly ended at 109.49.

The single currency has maintained a firm undertone after surging to 130.77 earlier this month, bullishness remains for medium term upmove from 109.49 low (2016 low) to resume after consolidation, above said resistance at 130.77 would extend this move to 131.00, then 132.00-10, however, near term overbought condition should prevent sharp move beyond 132.90-00 (1.236 times projection of 109.49-124.10 measuring from 114.85) and price should falter well below previous chart resistance at 134.59, risk from there has increased for a retreat to take place later.

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, above 126.00 would add credence to this view, then headway to 130.00 would follow.

On the downside, although initial pullback to 129.30-40 cannot be ruled out, reckon 128.85-90 would limit downside and bring another rise to aforesaid upside targets. A daily close below support at 128.49 would bring test of support at 127.44 but break of latter level is needed to suggest a temporary top is possibly formed, bring retracement of recent upmove to 126.45-50 but price should stay above previous resistance at 125.82 (now support) and euro may head north again from there. Only a sustained breach below this level would signal correction of recent upmove has commenced for further fall to 125.15-20 but previous resistance at 124.65 would hold from here.

Recommendation: Buy at 128.85 for 130.85 with stop below 127.85.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

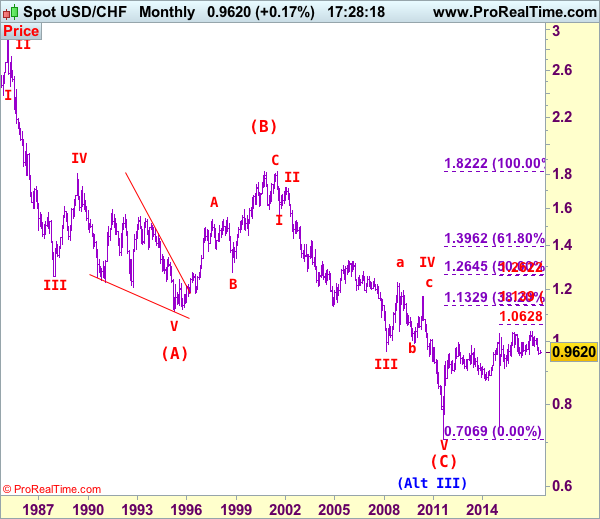

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9693

USD/CHF – Wave IV ended at 1.1730 and wave V has possibly ended at 0.7068

Although the greenback fell to as low as 0.9438 late last week, the subsequent strong rebound suggests a temporary low is possibly formed there and consolidation with mild upside bias is seen for gain to 0.9701 resistance, however, a daily close above there is needed to add credence to this view, bring retracement of recent decline towards resistance at 0.9771 but only a sustained breach above this level would provide confirmation and signal correction of recent selloff has commended, then headway to 0.9808 resistance would follow but upside should be limited to 0.9890-00 and price should falter well below psychological resistance at 1.0000.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the downside, whilst pullback to 0.9550-60 cannot be ruled out, reckon 0.9490 support would remain intact and bring another rebound to aforesaid upside targets. Only a drop below said recent low at 0.9438 would revive bearishness and signal the erratic decline from 1.0344 top (formed back in late 2016) is still in progress and downside bias remains for this move to extend weakness to 0.9390-00, however, loss of downward momentum should prevent sharp fall below 0.9300-10, risk from there has increased for a rebound to take place probably later.

Recommendation: Buy at 0.9550 for 0.9750 with stop below 0.9450

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

Technical Outlook: EURCHF Hits The Highest Levels Since Jan 2015 On Steep Rally In Past Few Days

The Euro surged against Swiss Franc this week, marking gains of over 3% so far in the biggest weekly advance since late Jan 2015. The Swiss Franc hit the lowest level since the SNB unpegged the national currency on Jan 15 2015.

Market participants suspect that the SNB might be behind the move, as central bank's president Jordan warned about significantly overvalued franc.

Strong rally so far doesn't show signs of fatigue, despite strongly overextended daily studies, but some corrective action could be anticipated in the near term.

The pair hit fresh high at 1.1379 on Friday, the highest since 15 Jan 2015 fall, signaling further advance.

Immediate target lies at 1.1418 (Fibo 138.2% projection) and rally may extend towards 1.1554 (Fibo 161.8% projection.

Res: 1.1379, 1.1418, 1.1500, 1.1554

Sup: 1.1300, 1.1260, 1.1180, 1.1105

Euro At 30-Month Highs, US Advance GDP Next

The sparkling euro climbed to 1.1777 on Thursday, its highest level since January 2015. On Friday, EUR/USD has inched higher, as the pair is trading at the 1.17 line, up 0.23% on the day. On the release front, German Preliminary CPI is expected to remain unchanged at 0.2%. Later in the day, the US releases Advance GDP, with the estimate standing at 2.5%. If GDP surprises, we can expect movement from the euro. We’ll also get a look at UoM Consumer Sentiment, with is expected to dip to 93.2 points.

The German consumer remains optimistic about the economy, and economic barometers certainly bear out the positive sentiment. With German exports in high demand, the manufacturing sector is strong. GfK German Consumer Climate strengthened for a fourth straight month, improving to 10.8 in the July report. This edged above the estimate of 10.7 points. Importantly, strong consumer confidence has translated into increased consumer spending, a key driver of economic growth. However, the fly in the ointment remains inflation, which is stuck at low levels. The lack of inflation is a pressing concern for ECB policymakers, and there is little chance that the bank will end its quantitative easing program before December, if inflation levels don’t move upwards.

The Federal Reserve maintained the benchmark rate at 1.25% on Wednesday. The highly-anticipated rate statement was cautiously optimistic in tone, saying that the economy was growing at a moderate pace and that the labor market remained strong. The statement made note of low inflation, but said that the Fed expected the economy to continue to expand. Another key issue on the Fed’s plate is the $4.2 trillion balance sheet. The rate statement said that the Fed plans to taper asset purchases “relatively soon”, which is a likely nod at September as the start date. This would involve the Fed tapering its purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Although the Fed continues to talk about another rate hike in 2017, investors remain skeptical. The rate statement did not change many minds, as the odds of rate increase in December stand at 47%, according to the CME Group.