Sample Category Title

Japanese Yen Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.64% against the JPY and closed at 111.88.

In the Asian session, at GMT0300, the pair is trading at 111.92, with the USD trading marginally higher against the JPY from yesterday’s close.

The pair is expected to find support at 111.14, and a fall through could take it to the next support level of 110.35. The pair is expected to find its first resistance at 112.4, and a rise through could take it to the next resistance level of 112.87.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Higher, Ahead Of Switzerland’s UBS Consumption Indicator Data

For the 24 hours to 23:00 GMT, the USD rose 0.58% against the CHF and closed at 0.9527.

In the Asian session, at GMT0300, the pair is trading at 0.9522, with the USD trading a tad lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9475, and a fall through could take it to the next support level of 0.9427. The pair is expected to find its first resistance at 0.9551, and a rise through could take it to the next resistance level of 0.9579.

Moving ahead, market participants will closely monitor Switzerland's UBS consumption indicator data for June, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

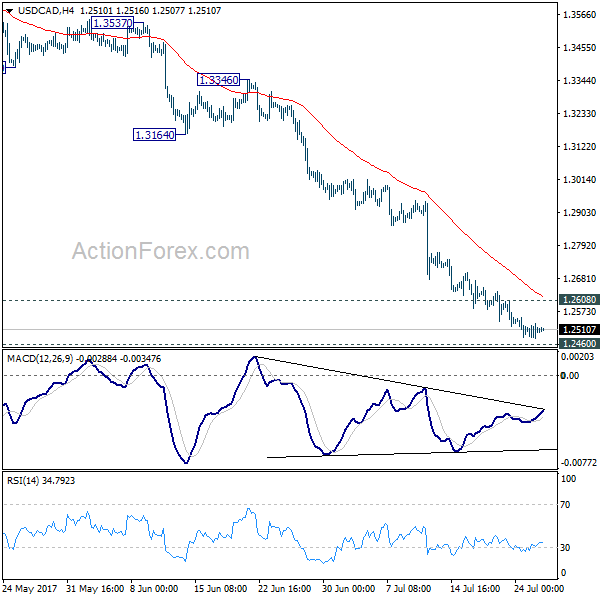

Loonie Trading Slightly Higher This Morning

For the 24 hours to 23:00 GMT, the USD traded flat against the CAD and closed at 1.2510.

In the Asian session, at GMT0300, the pair is trading at 1.2507, with the USD trading marginally lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2481, and a fall through could take it to the next support level of 1.2455. The pair is expected to find its first resistance at 1.2533, and a rise through could take it to the next resistance level of 1.2559.

With no economic releases in Canada today, investor sentiment will be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

UK GDP, The Fed And Oil In Focus

- Will UK get summery boost in GDP data?

- FOMC statement could hold balance sheet clues;

- Brent spikes above $50 on huge inventory draw.

It should be an interesting day for markets on Wednesday, with the UK releasing data on second quarter growth this morning, the US Federal Reserve announcing its latest decision this evening and crude inventory data being released after API reported a substantial reduction.

Data this morning is expected to show growth in the second quarter in the UK improved slightly from the first but remained mediocre, as the consumer squeeze continues to take its toll. Markets are expecting growth of 0.3% in the quarter but I do wonder whether the warmer weather in the quarter and the spike in consumer spending associated with it could spring a surprise on us this morning.

A positive surprise on the GDP report could be what the pound needs to finally break significantly above 1.30 against the dollar, with the pair once again struggling to make any serious move above here.

Another factor here today will be the FOMC decision later, or more likely the statement that accompanies it. The Fed is unlikely to raise interest rates again today having just done so in June, but we could get some insight into whether it will start reducing its balance sheet from September. The Fed has been discussing this for some months now and it may use today's statement to warn markets ahead of the next meeting.

Brent crude surged back above $50 on Tuesday after API reported a 10.23 million barrel drawdown in oil inventories, the biggest decline since September. The drop comes shortly after some of the world's largest oil producers met to discuss progress with the cuts and after data showed Saudi exports to the US have been declining over the last month.

It will be very interesting to see whether EIA reports and similar number today and, if so, whether traders will see this as a sign that the latest cuts are working or just a blip in the data. We'll need to see a few weeks of data to be sure but this coming when the US is importing less from Saudi Arabia may not be a coincidence. The surge through $50 may support this view and further gains could follow if EIA confirms the numbers today.

Oil Tests Resistance But Looks Ready To Retreat

Key Points:

- Selling Pressure is likely to resume in the near-term.

- Long-term downtrend remains intact despite recent upswing.

- Losses should be capped around the 47.20 or 45.32 handles.

Oil prices soared 4.50% higher overnight as a result of a 10.23M drawdown in the US API Crude Oil Stocks – the largest draw in 10 months. Due to this, much of the market will be bracing for another surge in buying pressure just in case the impending US Cushing Inventories data shows a similar outcome. Alternatively, the pessimists will be waiting on a reversal in the event that the next round of data proves disappointing. Whilst only time will truly tell who is in the right, a quick look at the technical bias certainly seems to suggest that the bears may be at a slight advantage.

Indeed, the recent surge has put oil prices into conflict with the upside of a long-term channel which could seriously hamstring further attempts to push oil prices higher. What's more, a number of other technical readings are hinting that the upswing may be short-lived. For instance, stochastics have trended sharply into overbought territory which is likely to encourage a reversal away from resistance. However, we also can't ignore the fact that the long-term trend is definitely slanted to the downside which will be putting pressure on the commodity regardless.

The main counter to a bearish technical biasis the fact that the EMA bias is clearly bullish. Nevertheless, I think this is more likely to act as a near term cap on downsides rather than be a driver of continued gains moving ahead. Specifically, the 100 day EMA should now be a source of dynamic support around the 23.6% Fibonacci level which could be where we now see oil retreat to. However, this is assuming that the next batch of US oil inventories data comes in broadly on target. If we instead see a less extreme draw or even a build, losses could smash back through this support and reach all the way back to the 45.32 handle.

Ultimately, it doesn't appear that oil is going to be out of the woods anytime soon on the technical front. Moreover, the prevailing view that OPEC has failed in its mission to re-float prices is slowly but surely taking its toll on the commodity which is likely to see it travel reliably lower in coming weeks. As a result, our near-term view is that oil reverses and subsequently declines, however, exactly to where is not yet clear.

Australian Inflationary Outlook Softens

Key Points:

- Australian Headline CPI falls to 0.2% q/q.

- Trimmed Mean CPI remains on target at 0.5%.

- Inflation softening likely to only be transitory.

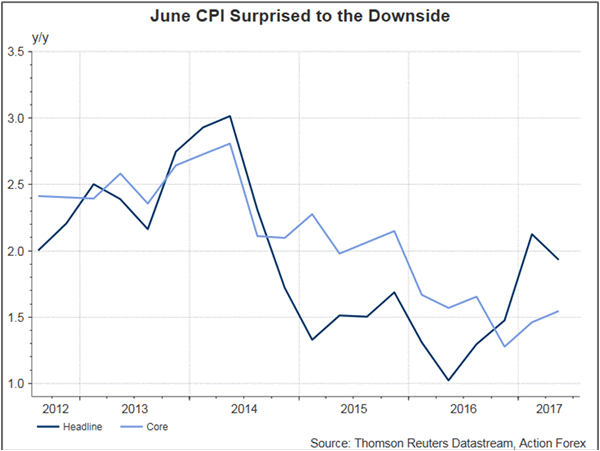

The latest Australian Consumer Price Index (CPI) figures were released earlier today and provided the market with a little surprise, with the headline result declining to 0.2% q/q. This proved to be significantly below the current estimates for inflation with most economists expecting a 0.4% q/q print. Subsequently, the Aussie Dollar has already eased around 30 pips but it remains to be seen what this means for the broader economy.

Certainly, the slip in the Headline CPI figures is interesting but, on its own, it’s not likely to have a great deal of impact on the RBA’s forward direction. In addition, a more important measure, the Trimmed Mean CPI, was actually broadly in line with expectations and returned a result of 0.5% q/q. In fact, this is actually the CPI result that the central bank looks at when they are seeking to set their monetary policy. Subsequently, the view that the recent slip in the headline CPI figure largely removes the pressure for the RBA to act in the medium term is ill-informed.

In fact, the main reason for the slip in the Headline CPI was the overall volatility of petrol and food prices. This largely explains why Core CPI has remained unmoved and, subsequently, suggests that any price effects are expected to be transitory. Subsequently, it would be wise to not read too much into the medium term impacts of a fall in inflation.

However, Australia still faces a challenge with the ongoing rebalancing that is occurring within their economy. Although looser monetary policy has assisted in softening the end of the commodity super cycle there still remains much transition of capital back towards services to occur. Certainly, the recently strength that the AUD has experienced has been relatively unwelcome by the RBA and many have taken the view that the currency is now significantly overvalued.

In fact, many of the reasons for the gain are the ebbing sentiment around the greenback, not the strength of the Australian economy. Subsequently, the AUDUSD is likely to snap lower in due course as broad support for the greenback returns to the fray. This may especially be the case if the market takes a negative view to the current CPI figures, despite the lack of a long-term impact.

Ultimately, the key take away from this commentary is that the slip in the headline CPI rate is relatively unimportant in the scheme of economic variables given that the core inflation rate did not change. However, the current valuation of the Aussie Dollar is more concerning and could be potentially putting a break on export competitiveness that may concern the RBA over the near term.

Market Update – Asian Session: Australia Inflation Remains Below Target

Asia Summary

Asian markets opened mixed, after yesterday’s lackluster session; focus still remains on the Fed. China markets were weaker with some standouts due to H1 guidance. China Cabinet announced all centrally owned firms under state asset regulator to become limited liability firms or joint stock firms by the end of 2017.

Australia Q2 CPI was the main risk event of the session, data showed that core inflation remains well below the 2-3% targeted by the RBA, which means that rates should be kept on hold for some time. Latest survey showed a 54.5% chance that the RBA will keep rates on hold until May 2018. The more muted inflation was attributed to weaker wages and lower fuel costs. The AUD fell 0.5% to session lows of 0.7892, 3-yr govt yield touched 2.037%. Later in the session RBA Govt Lowe warned that there could be financial stability risks from additional easing and affirmed some coverage of the RBA’s discussion of the neutral rate misinterpreted its intention. He also reiterated preference for a weaker currency.

Key economic data

(AU) AUSTRALIA Q2 CONSUMER PRICES (CPI) Q/Q: 0.2% V 0.4%E; Y/Y: 1.9% V 2.2%E; TRIMMED MEAN Q/Q: 0.5% V 0.5%E ; Y/Y: 1.8% V 1.8%E

(NZ) NEW ZEALAND JUN TRADE BALANCE (NZD): 242M V 150ME; 12-MONTH YTD: -3.66B V -3.68BE

(JP) JAPAN JUN PPI SERVICES (CGPI) Y/Y: 0.8% V 0.8%E

(AU) AUSTRALIA JUN SKILLED VACANCIES Q/Q: 0.9% V 1.0% PRIOR

Speakers and Press

China

(CN) China Securities Regulatory Commission (CSRC): to regulate and expand access to China's capital markets

(US) US expected to 'soon' issue new sanctions against China entities for violating UN sanctions against North Korea - US financial press

Australia

(AU) Reserve Bank of Australia (RBA) Gov Lowe: RBA does not need to follow other central banks in policy moves; Q&A: Do not think RBA is overestimating the level of neutral rate, some coverage of neutral rate misinterpreted our intentions

Korea

(KR) Revised assessment from US officials finds North Korea may be able to launch nuclear ICBM sooner than previously anticipated; could achieve capability to strike North America cities next year - Wash Post

Japan

(JP) Bank of Japan Deputy Gov Nakaso: Reiterates still long way to go to meet 2% inflation target and will persistently pursue current powerful easing

Other

(US) Senate Republican plan to repeal and replace Obamacare fails to get votes needed for approval - financial press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.5%, Hang Seng +0.06%, Shanghai Composite -0.37%, ASX200 +0.96%, Kospi -0.29%

Equity Futures: S&P500 -0.05%; Nasdaq -0.08%, Dax -0.09%, FTSE100 -0.10%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1654-1.1638; JPY 112.09-111.86; AUD 0.7941-0.7893; NZD 0.7436-0.7416

Aug Gold +0.38% at 1,247/oz; Sept Crude Oil +1.02% at $48.38/brl; Sept Copper +1.30% at $2.88/lb

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.7529 V 6.7485 PRIOR

(CN) China PBOC OMO injects CNY130B in 7 and 14 day reverse repos v CNY140B prior

(PH) Philippines rejects all bids in 20-yr bond auction; received PHP11.2B in bids v PHP15B offered (1st failed auction this year) –late in yesterday’s session

(CN) China Ministry of Finance (MOFCOM) sells 3-yr bonds at 3.46% v 3.47%e; bid-to-cover ratio 3.86x

(TH) Thailand sells THB6B in 18.89-yr government bonds; avg yield 3.0645%; bid-to-cover ratio 3.47x

Equities notable movers

Australia/New Zealand

Tower New Zealand, TWR.NZ NZ regulators block proposed merger with Suncorp over concerns about reduced competition; -23.8%

Oz Minerals, OZL.AU Reports Q2 gold production 32.1K oz,+23% y/y; copper production 28.2Kt v 27.4Ke, +12% y/y, +8.6%

Hong Kong/China

Evergrande Real Estate, 3333.HK Guides H1 Net to triple y/y; +12.9%

ASM Pacific, 522.HK Reports Q2 (HK$) Net 756.2M v 671Me ; Rev 4.42B v 4.5Be; -10.1%

Japan

Mitsubishi Motors, 7211.JP Reports Q1 Net profit ¥22.97B v loss ¥129.7B y/y; Op ¥20.6B v ¥4.62B y/y; Rev ¥440.9B v ¥428.7B y/y; +5.9%

Other

UBER.IPO Said to narrow short-list for CEO position to less than 6 candidates which include HPE's Meg Whitman; an announcement could come in less than 6 weeks - US financial

US markets on close: Dow +0.5%, S&P500 +0.3%, Nasdaq 0.0%, Russell +0.9%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Healthcare

Biggest gainers: FCX +14.7%; NCM +6.9%; RRC +6.9%

Biggest losers: STX -16.5%; IPG -13.3%; MU -5.6%

At 17:00ET/21:00GMT: VIX 9.43 (+0.00pts); Treasuries: 2-yr 1.39% +1.8%), 10-yr 2.33% (+3.5%), 30-yr 2.91% (+2.8%)

US Market Summary

(US) The Senate managed to pass a vote today to start debate on repeal of Obamacare. The vote was 50-50, with VP Pence vote casting the tie-breaker. The actual makeup of the healthcare bill remains unknown.

(US) Commerce Secretary Ross said global steel overcapacity is quite massive, pointing out that China may account for half of global excess capacity in steel. In a conciliatory note, he said trade and economic ties with China are a work in progress, and that the TPP trade proposal had some very good features that we can try to build on. He hopes to address South Korea free trade agreement shortly, adding that the US economy is in reasonably good shape.

(US) With stocks back in favor, Treasuries paid the price, with a strong sell-off across the curve. 10-year and 30-year yields gained 7 bps a piece, reaching 2.33% and 2.91% respectively; 10s30s spread steady at 58 bps

RBA’s Neutral Rate Rhetoric Overstated, Real Rate Similar To Fed’s

Aussie dropped after the weaker than expected inflation report, as traders took profit after the currency rallied to 2-year against USD and last week. Headline CPI moderated to +1.9% y/y in 2Q17 from +2.1% a quarter ago. The market had anticipated an increase to +2.2%. Key contributors to the weakness were lower automotive fuel prices as global oil prices plunged and the usual seasonal drop in domestic holiday, travel and accommodation prices. RBA's trimmed mean slipped 0.1 percentage point to +1.8%, in line with expectation, while the weighted median CPI climbed +0.1 percentage point to +1.8% in the second quarter. Consumer price levels are an important gauge of central banks' monetary outlook. The dilemma currently facing major central banks worldwide is the continuing economic growth and employment market improvement, alongside subdued inflation. At the July meeting minutes, RBA acknowledged that weak inflation is a global phenomenon with core inflation remaining low while headline inflation turning down..

RBA's Neutral Rate Rhetoric Overstated

Indeed, Aussie's rally last week was a result of market's overreaction to 'neutral rate' rhetoric's by the RBA and Fed Chair Janet Yellen. Recall that RBA suggested that the neutral nominal cash rate is around 3.5%, with medium-term inflation expectations well- anchored around 2.5%'. It also noted that 'a reduction in risk aversion and/or an increase in the potential growth rate could see the neutral real interest rate rise again'. Fed's Yellen noted at the testimony that 'the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance'.

Despite initial impression that RBA's language was implying a tightening stance, RBA's estimated nominal neutral rate, currently at 3.5%, was weaker than the previous projection of 5% (prior to global financial crisis). More importantly, what RBA noted was 'nominal neutral rate' which, if adjusted with medium term inflation expectations of around 2.5%, would bring a real rate of 1%. This is indeed coincident with the Fed's long-run neutral rate in real terms. Meanwhile, Yellen's comments on neutral rate were not more pessimistic than previously. Indeed, the Fed's neutral rate stance over recent years has remained similar, suggesting that the neutral rate had fallen fell sharply after the financial crisis and has remained near zero; r-star would move high should the temporary factors dissipate over time and the long-term level of the neutral rate has permanently shifted downward due primarily to slower potential growth.

RBNZ Assistant Governor John McDermott also talked about the monetary policy outlook earlier today. His stance, while driven muted market reaction, was rather dovish. He suggested that current estimate of the neutral interest rate is around 3.5 % with potential output growth at 2.9% and core inflation at 1.4%. He added that the neutral rate has been slowly falling for some time, due to lower potential output growth. Dating back to early 2015, the central bank noted that the neutral interest rate is around 4.5%

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2481; (P) 1.2506; (R1) 1.2532; More....

No change in USD/CAD's outlook. While deeper fall could be seen, considering bullish convergence condition in 4 hour MACD, we'll be cautious on strong support from 1.2460 key support to contain downside and bring rebound. On the upside, break of 1.2608 minor resistance will indicate short term bottoming and turn bias back to the upside for 1.2968 support turned resistance. However, firm break of 1.2460 will target next key fibonacci level at 1.2048.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Fall from 1.3793 is seen as the third leg and should target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7902; (P) 0.7936; (R1) 0.7970; More...

AUD/USD continues to stay in consolidation below 0.7988 and intraday bias remains neutral. Near term outlook remains bullish as long as 0.7785 support holds and another rise is expected. Break of 0.7988 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next. However, break of 0.7785 will argue that deeper pull back in under way and could target 55 day EMA (now at 0.7658).

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.