Sample Category Title

USD/JPY Still Sideways

Continues to move sideways on the short term, between the 23.6% and the 50% retracement levels, is trading at the half of this range. We’ll have a clear direction once we’ll have a valid breakout from the extended sideways movement. Remains to see if this is an accumulation or a distribution movement. Personally I’m waiting to see what will happen on the Nikkie, which is narrowing around 20058 static resistance.

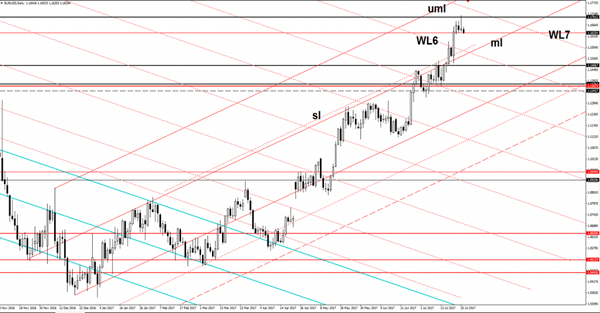

EUR/USD Could Turn To The Downside

Price found temporary resistance right below the 1.1700 level and could lose altitude as the USDX is trying to recover as much as can before the FOMC Statement. However the perspective is bullish as long as is located above the median line (ml) of the ascending pitchfork, only a valid breakdown will signal a reversal.

Technically, is somehow expected to decrease at least till the median line (ml) after the failure to reach the 1.1712 long term resistance and the upper median line (uml) of the ascending pitchfork, but unfortunately the fundamental factors will drive the price.

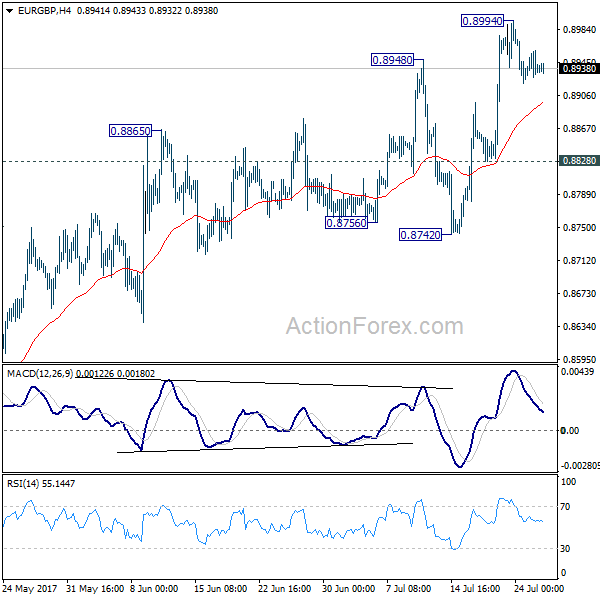

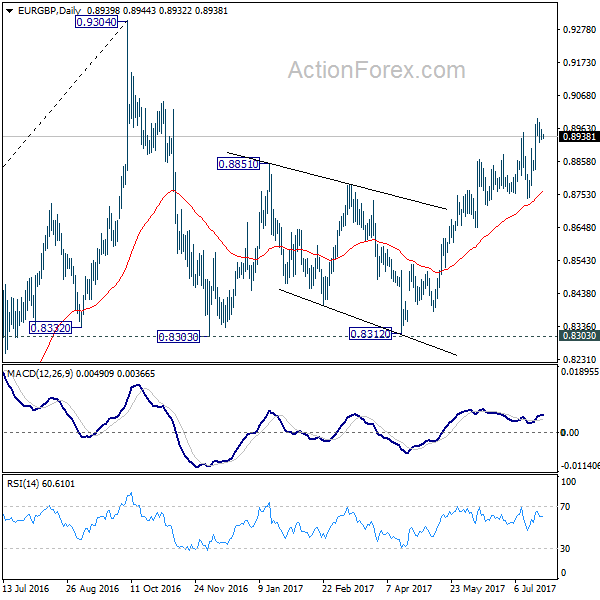

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8924; (P) 0.8942; (R1) 0.8957; More

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8994 temporary top. Downside of retreat should be contained by 0.8828 minor support to bring another rally. Break of 0.8994 will extend the whole rise from 0.8312 towards 0.9304 high. here is no clear sign of up trend resumption yet. Hence, we'll be cautious on strong resistance from 0.9304 to limit upside and bring another fall.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

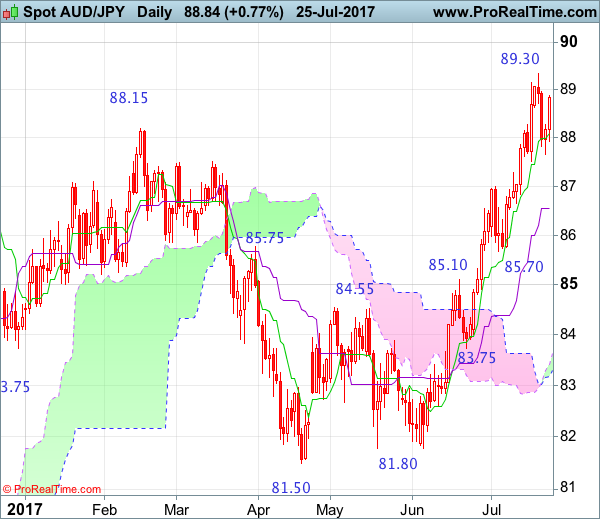

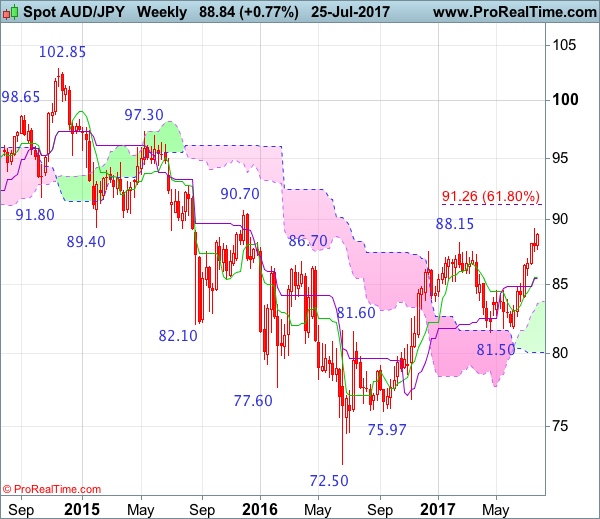

AUD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 13 Mar 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 16 Feb 2017

• Trend bias: Near term down

The Australian dollar continued surging after breaking above previous resistance at 85.10 and the subsequent breach of another previous chart point at 88.15 adds credence to our view that the medium term upmove from 2016 low of 72.50 is still in progress and bullishness is seen for this move to extend further gain to 89.30-35, then towards psychological resistance at 90.00, however, near term overbought condition should prevent sharp move beyond previous chart resistance at 90.70, risk from there is seen for a retreat to take place next month.

On the downside, whilst initial pullback to 87.60-65 is likely, reckon downside would be limited to 87.25-30 and the Kijun-Sen (now at 86.53) should hold, bring another rise later. A daily close below the Kijun-Sen would defer and suggest top is possibly formed, bring correction to 86.00 and then towards previous support at 85.70 but downside should be limited and price should stay well above 85.00-10, bring another upmove probably net week.

Recommendation: Buy at 87.30 for 89.30 with stop below 86.30.

On the weekly chart, aussie has maintained a firm undertone after recent rally above previous resistance at 88.15, adding credence to our bullish view that medium term upmove from 72.50 low (formed back in 2016) is still in progress and upside bias remains for this move to extend headway to psychological resistance at 90.00, then test of previous resistance at 90.70, however, near term overbought condition should limit upside to 91.50-60 and price should falter below another previous chart resistance at 92.70, bring correction later.

On the downside, although pullback to 88.00, then 87,.50-60 cannot be ruled out, reckon 87.00 would limi downside and bring another rise later. Below 86.50-55 would defer and risk test of the Tenkan-Sen (now at 85.55) but a weekly close below the Kijun-Sen (now at 85.41) is needed to signal a temporary top is formed instead, bring retracement of recent rise to 85.00, then 84.60-65, however, still reckon the upper Kumo (now at 83.55) would remain intact.

GBP/USD Bullish Outlook Clouded

Price looks undecided and uninspired on the Daily chart and could decrease again if the USDX will have enough energy to climb much higher on the short term. GBP/USD is trading much above the 1.3000 psychological level, maintaining a bullish perspective as long as this support remains intact.

The buyers seem exhausted on the Daly chart, price failed to reach the 1.3111 previous high, signalling that he could slip lower to test and retest a support level.

The United Kingdom data could bring life on the GBP/USD, the Prelim GDP could increase by 0.3% in the second quarter and could beat the 0.2% growth in the former reading period, while the BBA Mortgage Approvals could decrease from 40.3K to 39.9K. Moreover the Index of Services is expected to increase by 0.4% in May.

You should be careful today because we may have a high volatility after the FOMC Statement and after the Federal Funds Rate will be released. As you already know, the interest rate is expected to remain steady at 1.25% in the upcoming period.

Price decreased a little after the yesterday’s indecision, could come down to retest the upper median line (UML) if the dollar index will resume the minor rebound. Right now is premature to say that we’ll have a broader rebound on the USDX because is trapped below a strong dynamic resistance.

GBP/USD looks too overbought on the short term, so technically should drop towards the warning line (wl1) of the ascending pitchfork, could be attracted by the confluence formed between the upper median line (UML) of the major descending pitchfork with the warning line (wl1). The outlook is bullish as long as is trading above the mentioned support levels, but a valid breakdown below the wl1 and below the UML will open the door for a major drop.

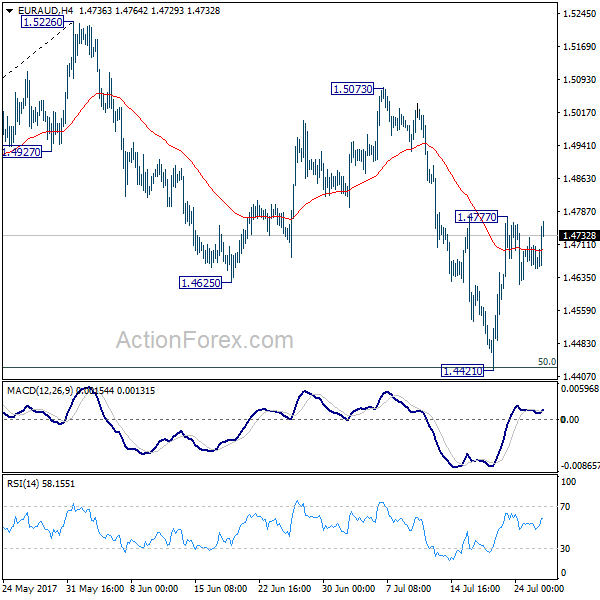

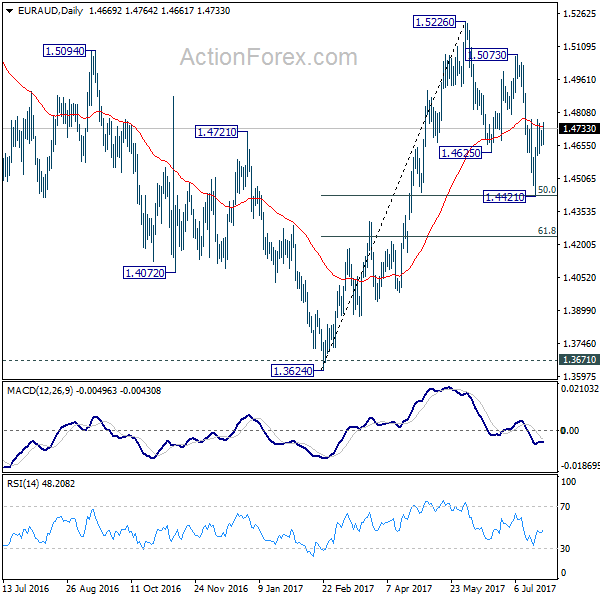

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4645; (P) 1.4685; (R1) 1.4714; More...

Intraday bias in EUR/AUD remains neutral for consolidation below 1.4777 temporary top. We'd holding on to the view that correction from 1.5226 could have completed with three waves down to 1.4421 already. Therefore, another rally is expected in the cross. Break of 1.4777 will turn bias to the upside for 1.5073 resistance first. Break there will indicate resumption of whole rise from 1.3624. However, break of 1.4221 will invalidate our view and extend the decline from 1.5226.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to resume to retest 1.6587. The corrective structure of the fall from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, further downside acceleration will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

AUD/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 10 Jul 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Long white candlestick

• Time of formation: 18 Jul 2017

• Trend bias: Up

As aussie found decent demand at 0.7571 earlier this month and has rallied since, price broke above indicated previous resistance at 0.7835, reinforcing our bullish view that medium term erratic rise from 0.6827 has resumed and upside bias remains for this move to extend headway to psychological resistance at 0.8000, break there would encourage for subsequent rise to 0.8090-00 but near term overbought condition should prevent sharp move beyond 0.8150 and price should falter below 0.8200.

On the downside, whilst initial pullback to 0.7875-80 cannot be ruled out, reckon the Tenkan-Sen (now at 0.7833) would limit downside and the Kijun-Sen (now at 0.7763) should hold, bring another upmove later. A daily close below the Kijun-Sen would dampen this bullish view and suggest a temporary top is possibly formed, risk test of previous resistance at 0.7712 but break there is needed to add credence to this view.

Recommendation: Buy at 0.7840 for 0.8040 with stop below 0.7740.

On the weekly chart, aussie has surged after brief retreat to 0.7571 and the subsequent rally above previous resistance at 0.7835 formed a long white candlestick, signaling the erratic rise from 0.6827 low is still in progress, hence bullishness remains for this move to extend headway to psychological resistance at 0.8000, then 0.8090-00, however, near term overbought condition would limit upside to previous resistance at 0.8163 and price should falter well below resistance at 0.8295, bring retreat later.

On the downside, although pullback to 0.7875 is likely, reckon downside would be limited to previous resistance at 0.7835 (now support) and bring another rise later. Below 0.7785-90 would bring pullback towards previous resistance at 0.7712, break there would suggest top is possibly formed, bring test of the Tenkan-Sen (now at 0.7681) but break of the Kijun-Sen (now at 0.7660) is needed to provide confirmation, bring further fall towards said support at 0.7571 which should remain intact.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, AUD/USD, USD/JPY, USD/CAD, USD/CHF, DOW 30, GOLD

A note on lower timeframe confirming price action...

Waiting for lower timeframe confirmation is our main tool to confirm strength within higher timeframe zones, and has really been the key to our trading success. It takes a little time to understand the subtle nuances, however, as each trade is never the same, but once you master the rhythm so to speak, you will be saved from countless unnecessary losing trades. The following is a list of what we look for:

- A break/retest of supply or demand dependent on which way you're trading.

- A trendline break/retest.

- Buying/selling tails ... essentially we look for a cluster of very obvious spikes off of lower timeframe support and resistance levels within the higher timeframe zone.

- Candlestick patterns. We tend to only stick with pin bars and engulfing bars as these have proven to be the most effective.

We typically search for lower-timeframe confirmation between the M15 and H1 timeframes, since most of our higher-timeframe areas begin with the H4. Stops are usually placed 1-3 pips beyond confirming structures.

EUR/USD

After momentarily surpassing the 1.17 handle on Tuesday and coming within an inch of clipping the underside of a H4 AB=CD 161.8% Fib extension at 1.1713 drawn from the low 1.1370, the single currency (influenced by a much higher-than-expected US consumer confidence report) turned aggressively lower.

What's also notable from a technical perspective is that the daily candles recently connected with an upper channel resistance line extended from the high 1.1263, and chalked in a reasonably strong-looking daily selling wick.

While the above paints a somewhat bearish picture, there are two strong cautionary points to consider here:

Daily support at 1.1615 is hovering nearby current price.

Last week we saw a large weekly supply zone at 1.1533-1.1278 taken out, which had managed to stay intact since mid-May 2015! This suggests that overall the bulls are in control of things for the time being.

Our suggestions: Based on the above findings, our desk is watching the green H4 area marked at 1.16/1.1615 for potential long opportunities. The area is comprised of a psychological band at 1.16, a H4 38.2% Fib support level at 1.1606 pegged from the low 1.1479 and the daily support mentioned above at 1.1615.

To be on the safe side here, we've elected to wait for additional confirmation before pulling the trigger. Preferably, we want to see a full, or near-full-bodied H4 bull candle materialize from the said H4 buy zone. This, of course, will not promise a winning trade, but what it will do is display buyer intent from a high-probability reversal zone.

Data points to consider: US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: 1.16/1.1615 ([waiting for a H4 bull candle to form before entering long is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

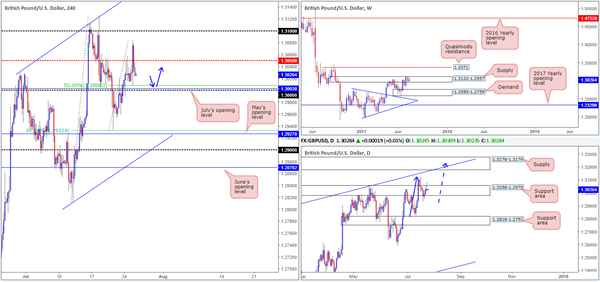

GBP/USD

Kicking this morning's report off with a look at the weekly chart, we can see that the candles remain within the walls of a supply zone pegged at 1.3120-1.2957. In the event that the bears finally regain consciousness here, the next downside target resides at 1.2589-1.2759: a demand base. On the other side of the field, however, the daily chart shows price action to be trading from a support area coming in at 1.3058-1.2979. What's also interesting on this scale is the potential AB=CD bearish pattern that completes within the supply zone marked at 1.3278-1.3179 that converges with a channel resistance line drawn from the high1.2774.

Looking over to the H4 chart, recent action aggressively whipsawed through the mid-level resistance number at 1.3050 after a much higher-than-expected US consumer confidence report. As you can see, this has placed the candles within touching distance of the large psychological level 1.30, which happens to fuse nicely with July's opening level at 1.3003 and a 50.0% support at 1.3008 taken from the low 1.2932.

Our suggestions: Given that the unit is positioned within a daily support area at the moment, and the weekly candles have yet to show much bearish intent within its current supply, we feel longs from the 1.30 region could be an option today in light of the surrounding confluence.

Like the EUR chart above though, we've elected to wait for additional confirmation before pulling the trigger from 1.30. Preferably, we want to see a full, or near-full-bodied H4 bull candle materialize from here. Should this trade come to fruition; the 1.3050 zone will be the first level on our radar for partial profit taking and a reduction in risk.

Data points to consider: UK Prelim GDP q/q at 9.30am. US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: 1.30 region ([waiting for a H4 bull candle to form before entering long is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

AUD/USD

Since the 19th July, the H4 candles have been busy chiseling out a consolidation zone between 0.7969/0.79. A little above this area there is a large psychological band seen sitting at 0.80, whereas a few pips below is a support level marked at 0.7870.

Over on the bigger picture, the weekly resistance area at 0.7849-0.7752 was recently engulfed, potentially opening up the path north to a weekly resistance at 0.8075. Down on the daily timeframe on the other hand, the candles appear to be somewhat indecisive around a channel resistance line taken from the high 0.7732. Should this line eventually give way, the next area on the hit list is a Quasimodo resistance at 0.8030.

Our suggestions: Personally speaking, the current H4 range sparks little interest from us, due to there being no concrete higher-timeframe structure supporting the area. Nevertheless, we have noted the 0.80 level seen just above as a possible option for shorts, given its nearby connection to the daily Quasimodo resistance at 0.8030. Be that as it may, our desk would require additional confirmation before a sell from here would be considered, since there's a good chance weekly price could step in a drag the unit up to 0.8075!

Data points to consider: Australian Inflation figures at 2.30am, RBA Gov. Lowe speaks at 4.05am. US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: 0.8030/0.80 ([waiting for a H4 bear candle to form before entering long is advised] stop loss: ideally beyond the candle's wick).

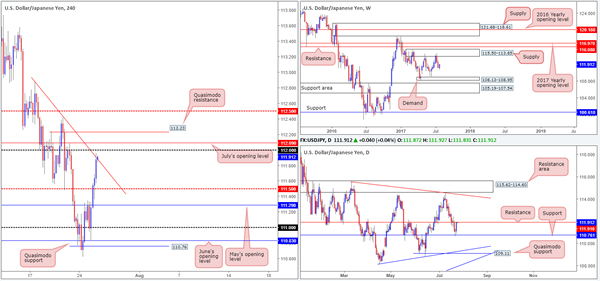

USD/JPY

The USD/JPY bulls, as you can see, went on the offensive amid Tuesday's segment, consequently lifting the pair above May's opening level at 111.29 and a H4 mid-level resistance at 111.50. Intensified by a much higher-than-expected US consumer confidence report, the pair was able to end the day challenging a H4 trendline resistance taken from the high 112.87.

Weekly price is not currently offering much right now, other than that the candles are seen trading mid-range between supply at 115.50-113.85 and demand at 108.13-108.95. The daily chart, nonetheless, reveals that the unit is currently touching gloves with a resistance level coming in at 111.91, after a solid bounce seen from support at 110.76.

Our suggestions: Shorting from the current H4 trendline resistance is tempting, considering that it is linked closely with the aforementioned daily resistance. However, we're a little cautious here. July's opening level at 112.09 and the 112 handle are both located a few pips above the line, and therefore may act as a magnet to price and cause a fakeout. From this, you may be thinking, ‘well, why not just short 112.09/112?' While the point is valid, one would still need to be prepared for this area to also be faked, due to a H4 Quasimodo resistance level lurking just above it at 112.23. Furthermore, by the time H4 price connects with this Quasimodo level, daily price may have already printed a close above the current resistance!

In light of the above notes, we're going to humbly step aside today and reassess structure going into tomorrow's segment.

Data points to consider: US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

USD/CAD

Tuesday's session was incredibly quiet in the USD/CAD market. H4 price spent the day clinging to the 1.25 handle, printing several meaningless candles. This, as you can see by looking over to the daily chart, saw the market chalk up an indecision candle off of a Quasimodo support at 1.2506. Assuming that the bulls remain afloat above this level, we'd be looking for the market to retest 1.2592: a recently broken Quasimodo line. Up on the weekly chart, price recently came into contact with support at 1.2538. Although we have seen little evidence of bullish intent from here, it is far too early to count it out just yet!

Our suggestions: To confirm bullish strength in this market, we would like to see H4 price close above the mid-level resistance at 1.2550. This would, technically speaking, likely clear the runway north up to at least the 1.26 handle, which sits just above the aforementioned broken daily Quasimodo line.

Therefore, a H4 close above 1.2550 followed by a retest and a lower-timeframe confirming buy signal (see the top of this report) would, in our opinion, be enough to validate an intraday long up to at least the 1.26 region.

Data points to consider: US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm. Crude oil inventories at 3.30pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf 1.2550 and then look to trade any retest of this level seen thereafter ([waiting for lower-timeframe confirmation following the retest is advised] stop loss: depends on where one confirms this level).

- Sells: Flat (Stop loss: N/A).

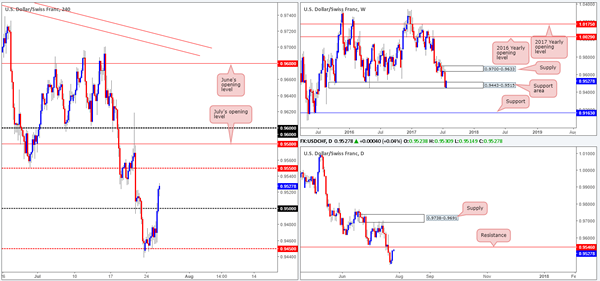

USD/CHF

Influenced by a much higher-than-expected US consumer confidence report on Tuesday, the USD/CHF cleared the 0.95 handle and now looks poised to challenge the H4 mid-level resistance base at 0.9550. From a technical perspective 0.9550 is closely linked with a daily resistance level pegged at 0.9546. Although selling from the 0.9550 region seems reasonable, one has to remain cognizant of the weekly picture that currently shows price trading from a support area drawn in at 0.9443-0.9515.

As such, going short from 0.9550 would entail one selling into potential weekly flow! By the same token, buying would place one against both H4 and daily flow! Therefore, no matter which direction one chooses here, the odds are not really in your favor!

Our suggestions: In the absence of clearer price action, we have decided to remain flat during today's trading and will look to reassess the situation going into tomorrow's open.

Data points to consider: US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Flat (stop loss: N/A).

- Sells: Flat (stop loss: N/A).

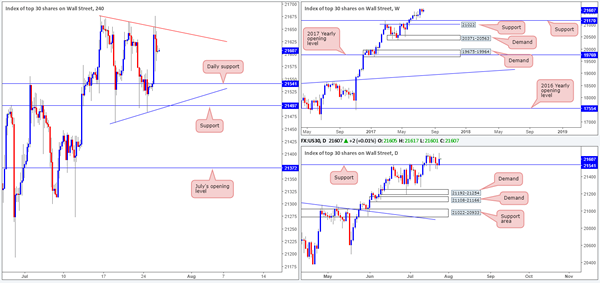

DOW 30

Over the past few weeks, we have been seeing the US equity market chalk up a potential H4 bullish pennant formation (21677/21462). This – coupled with seeing daily price bouncing off of a support level at 21541 and showing absolutely no resistance on the horizon, we feel that this pennant will eventually breakout to the upside. To us, this would be a valid buy signal, however not one that we would personally consider trading on the breakout.

To that end, as long as the daily candles remain above the noted support, our team will continue to favor the upside in this market.

Our suggestions: An ideal situation here would be to see a decisive H4 close above the current H4 pennant formation. Following this, a retest of the broken line in the shape of a full, or near-full-bodied H4 bull candle would be enough for us to enter into a long position with stops pegged below the H4 bull candle's tail. This would, should it come to fruition, be an ideal time to try and join this seemingly undying trend!

Data points to consider: US New home sales at 3pm, FOMC Statement and the Fed funds rate at 7pm GMT+1.

Levels to watch/live orders:

- Buys: Watch for H4 price to engulf the current H4 pennant upper edge and then look to trade any retest seen thereafter ([waiting for a full, or near-full-bodied H4 bull candle to form following the retest is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

GOLD

Since the yellow metal clipped the underside of a daily resistance at 1258.9, the unit has been trading in bearish territory and looks as though it will likely continue doing so until we reach daily support at 1242.0. Fusing closely with this level is a H4 trendline support etched from the low 1204.6 and a H4 38.2% Fib support also taken from the low 1204.6. Weekly price unfortunately offers very little support here as the candles are currently seen loitering mid-range between demand at 1195.1-1228.6 and an area comprised of two Fibonacci extensions 161.8/127.2% at 1312.2/1284.3 taken from the low 1188.1 (green zone).

Our suggestions: While we are seen trading from a daily resistance level at the moment, selling is difficult considering the noted H4/daily supports lurking nearby. In regard to buying, the H4 blue zone which is comprised of the above noted structures highlighted in bold is quite attractive for a bounce long today. With that being said, however, the area does lack weekly support, so in order to trade this area we would need to see additional confirming price action before pulling the trigger.

Levels to watch/live orders:

- Buys: 1238.4/1241.6 ([waiting for a reasonably sized H4 bull candle – preferably a full-bodied candle – to form before pulling the trigger is advised] stop loss: ideally beyond the candle's tail).

- Sells: Flat (stop loss: N/A).

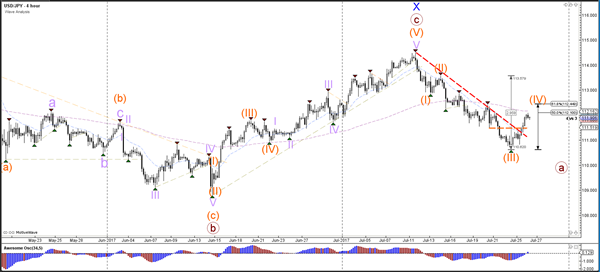

Daily Technical Analysis: USD/JPY Break Or Bounce At 112.50 Resistance Of Wave 4

Currency pair USD/JPY

The USD/JPY has broken above the resistance trend lines (dotted) after completing wave 3 (orange). The bullish price action could still be part of a wave 4 (orange) as long as price stays below the 61.8% Fibonacci level.

The USD/JPY could be building an ABC (purple) correction within wave 4 (orange). The resistance top (red) at 112.50 is a key resistance level for wave 4.

Currency pair EUR/USD

The EUR/USD continued the uptrend and managed to reach 1.17. The new higher high is most likely completing the wave 3 (orange) and starting a wave 4 (orange) correction. Price could use the Fibonacci levels of wave 4 vs 3 as potential bounce spots.

The EUR/USD could be building an ABC (grey) correction within wave 4 (orange).

Currency pair GBP/USD

The GBP/USD respected the 78.6% Fibonacci level of the WXY (purple) pattern. A break below the small channel (blue) would indicate the potential for price to retrace lower towards the 61.8% Fibonacci target of wave Y vs W.

The GBP/USD completed multiple ABC (green) corrections within wave X (purple). Price is now at a new bounce or break spot at the bottom of the channel.

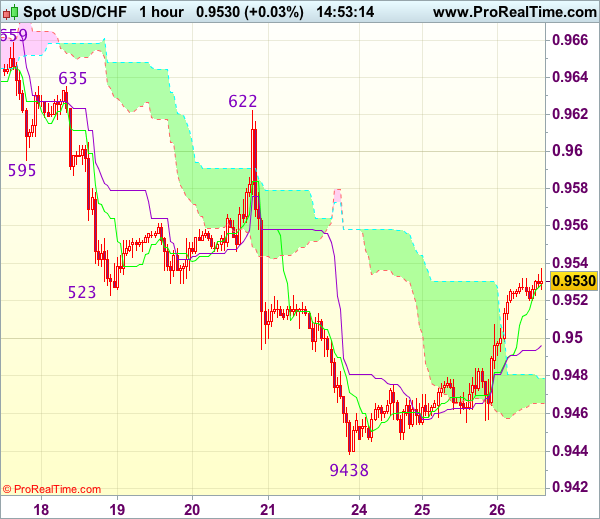

Trade Idea : USD/CHF – Sell at 0.9570

USD/CHF - 0.9532

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9529

Kijun-Sen level : 0.9496

Ichimoku cloud top : 0.9479

Ichimoku cloud bottom : 0.9466

Original strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9570, target: 0.9470, Stop: 0.9605

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after staging a strong rebound from 0.9438 late last week, suggesting near term upside risks remains for this corrective bounce to extend gain to 0.9550-55, however, reckon upside would be limited to 0.9570-75 (50% Fibonacci retracement of 0.9701-0.9438) and bring retreat later, below the Kijun-Sen (now at 0.9496) would suggest an intra-day top is possibly formed but break of 0.9450-55 is needed to signal the rebound from 0.9438 has ended, bring retest of this level first.

In view of this, we are looking to sell dollar on further subsequent recovery as 0.9570 should limit upside and bring another decline. Above 0.9600-05 (61.8% Fibonacci retracement of 0.9701-0.9438) would suggest a temporary low is formed instead, bring a stronger rebound towards resistance at 0.9622.