Sample Category Title

Trade Idea Update: EUR/USD – Buy at 1.1580

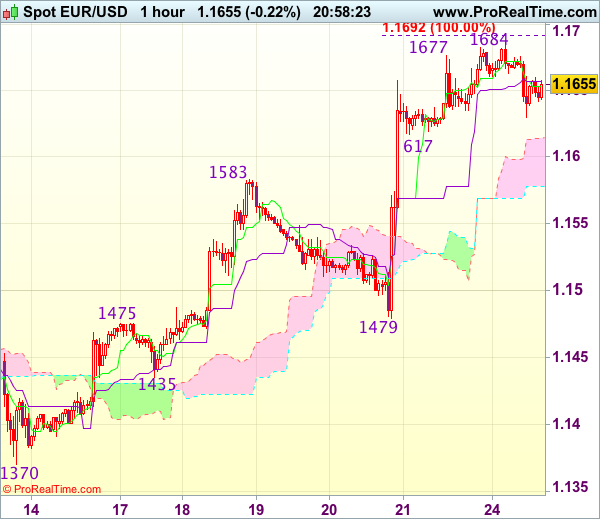

EUR/USD - 1.1649

Original strategy :

Buy at 1.1580, Target: 1.1680, Stop: 1.1545

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1580, Target: 1.1680, Stop: 1.1545

Position : -

Target : -

Stop : -

As the single currency has retreated after marginal rise to 1.1684, suggesting consolidation below this level would be seen and pullback to support at 1.1617 is likely, however, reckon previous resistance at 1.1583 would turn into support and contain downside, bring another rise later, above said resistance at 1.1684 would extend recent upmove to previous chart resistance at 1.1714 but break there is needed to retain bullishness for the rise from 1.0340 low to head towards 1.1750.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1583 should limit downside. Below 1.1550 would defer and suggest a temporary top is formed instead, bring correction to 1.1510-15 but support at 1.1479 should remain intact.

Trade Idea Update: USD/JPY – Sell at 111.35

USD/JPY - 110.82

Original strategy :

Sell at 111.35, Target: 110.35, Stop: 111.70

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.35, Target: 110.35, Stop: 111.70

Position : -

Target : -

Stop : -

As the greenback has resumed recent decline after meeting renewed selling interest at 112.08 on Friday, adding credence to our view that the selloff from 114.50 top is still in progress and downside bias remains for this move to extend weakness to 110.60-65 (61.8% projection of 114.50-111.55 measuring from 112.42), however, loss of downward momentum should prevent sharp fall below 110.30-35 and reckon 110.00-05 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.30-35 should limit upside. Above previous support at 111.48-55 would defer and suggest a temporary low is formed, bring retracement of recent decline to 111.75-80, then towards resistance at 112.08.

Euro Faces Hardened Test

European indices are selling off again, not only due to the prospects of invevitable QE tapering from the ECB, but also due to ongoing declines Europe's auto sector due to allegations of price collusion. Daimler-Benz and BMW are down 15% and 11% year-to-date. On Friday, the Premium Insights locked in 345-pt gain in the Dax short trade opened on Monday. A new note had been issued to indicate the next step (when & where).

The euro surged last week and is now less than 50 pips from the August 2015 high. The Swiss franc narrowly beat the euro last week as the top performer while the pound lagged. CFTC positioning showed increasingly-crowded bets against the yen. The euro has been skidding along the lows for more than two years but is now threatening to break out. Large gains in three of the past four weeks has EUR/USD bumping up against 1.1714 and a break would be a foray into the massive void formed by the drop to 1.05 from 1.40 that started in 2014.

The latest leg of gains comes as the US dollar struggles economically and politically. The non-stop drama and gridlock in Washington increasingly threaten another round of risk aversion.

Inertia should keep a bid in the euro early in the week but the calendar picks up midweek with the FOMC, some higher-tier US data and German CPI on Friday.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +91K vs +84K prior

- GBP -16K vs -24K prior

- JPY -127K vs -112K prior

- CHF -4K vs 0K prior

- CAD +8K vs -9K prior

- AUD +51K vs +37K prior

- NZD +36K vs +32K prior

The yen trade is beginning to look saturated, especially when you factor in the carry trade. The positioning is the kind of thing you might see before a squeeze on risk trades.

The Canadian dollar finally flipped to a net long position. That means the squeeze on the shorts is done but there is still plenty of ammunition if longs want to get involved. In AUD and NZD, meanwhile, the trade is starting to get crowded.

USDJPY: Bearish, Retains Its Downside Pressure

USDJPY: The pair continues to hold on to its downside pressure closing lower the past week. On the downside, support comes in at the 110.50 level where a break if seen will aim at the 110.00 level. A cut through here will turn focus to the 109.50 level and possibly lower towards the 109.00 level. On the upside, resistance resides at the 111.50 level. Further out, we envisage a possible move towards the 112.00 level. Further out, resistance resides at the 112.50 level with a turn above here aiming at the 113.00 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the whole, USDJPY looks to weaken further in the new week.

NZD/USD Much Below the 0.7484 Swing High

NZD/USD stays higher and could hit new highs in the upcoming days if the USDX will stabilize below the 94.00 psychological level. Price rallied aggressively in the last days and jumped above the 0.7375 obstacle, the next upside target is at the 0.7484 swing high. Maintains a bullish perspective as long as is located above the fourth warning line (WL4), could come down to retest the broken resistance (resistance turned into support) before will climb much higher.

USD/CAD Losing Momentum

USD/CAD dropped a little today because is still under massive selling pressure, but most likely will find a strong support in the upcoming days and will start a rebound. Technically, we should have a bounce back on the short term after the massive drop.

Price extends the sell-off as the USDX could slide further, could approach and reach the 1.2460 major static support, where he may find strong support again. A failure to reach the lower median line (lml) will signal an oversold, this situation will send the rate much higher in the upcoming period.

EUR/GBP Still Bullish

The EUR/GBP drops a little after the impressive rally, but maintains a bullish bias despite the minor correction. Is trading near 0.8930 level, much below the 0.8993 yesterday's high, the Euro lost significant ground versus its rivals as the Euro-zone data have disappointed in the morning.

The Euro-zone Flash Services PMI remains steady at the 55.4, but has come below the 55.5 estimate, while the Flash Manufacturing PMI decreased from 57.4 points to 56.8 points in July, even if the estimate was 57.3 points.

Moreover the German Flash Services PMI decreased from 54.0 points to 53.5 points in July, even if the traders have expected to see an increase to 54.4 points, while the Flash Manufacturing PMI plunged from 59.6 to 58.3, much below the 59.1 estimate, signalling that the expansion has slowed down aggressively.

French Flash Services PMI was reported at 55.9 points, much below the 56.6 estimate and below the 56.9 in the former reading period, has received support from Flash Manufacturing PMI, which has increased from 54.8 to 55.4 points, beating the 54.6 estimate.

Price is trading in the red and retreats after the upside momentum, but don't worry because the perspective remains bullish on the Daily chart after the valid breakout from the extended sideways movement and above the warning line (wl2).

The next upside target will be at the 50% Fibonacci line (ascending dotted line), could also be attracted by the upper median line (UML) of the major ascending pitchfork and by the third warning line (wl3) in the upcoming period.

Technically, should increase further as long as is located above the median line (ML) of the major ascending pitchfork, could approach the 0.9226 major static resistance, where he could find strong resistance again.

DAX Drops as German Manufacturing PMI Slows

The DAX index has started the week with losses. In Monday's European session, the DAX is trading at 12,190.00, down 0.40% on the day. On the release front, German and Eurozone Manufacturing PMIs softened in July and missed expectations. On Tuesday, Germany will release Ifo Business Climate.

The new trading week started on a sour note, as Eurozone and German manufacturing PMIs both in July and missed expectations. Still, the soft numbers are unlikely to weigh on the markets, as the PMIs continue to point to expansion in the German and eurozone manufacturing sectors. A stronger global economy has resulted in increased demand for European exports, and domestic consumer consumption has also boosted the manufacturing industry. The German economy continues to perform well in 2017, and this has helped boost the eurozone economy, which is showing stronger growth and lower unemployment. The German finance ministry sounded upbeat on Thursday, saying that "the current picture of economic indicators suggests that the economic upswing continued vigorously in the second quarter". GDP expanded at a strong clip of 0.6% in the first quarter, and Q2 is expected to post another gain of 0.6%. The economy received a thumbs-up from the IMF, which has raised its growth projections to 1.8% in 2017 and 1.6% in 2018. The fly in the ointment has been inflation, as both Germany and the eurozone continue to struggle with inflation levels well below the ECB's inflation target of 2%. German policymakers have long argued that the German economy needs higher interest rates. However, the ECB has to also look after eurozone members who are not doing as well as Germany, and has insisted that it will not withdraw stimulus until inflation in the eurozone moves closer to the bank's inflation target.

There were no surprises from the ECB last week, as policymakers maintained interest rates at 0.00% and the bank's asset-purchase scheme (QE) at EUR 60 billion/month. The ECB has said that it will maintain QE until December "or beyond, if necessary". There had been speculation that the ECB might remove that "wiggle room" phrase, but the bank did not make any changes – perhaps Draghi was being careful not to provide the markets with an excuse to rush on euros, which occurred in June after Draghi left open the door to tapering QE prior to December.

With no news in the rate statement, the markets focused on the ECB President Mario Draghi's press conference. Draghi sounded upbeat about the eurozone economy, noting there were signs of "unquestionable improvement" in the eurozone economy. Draghi acknowledged that inflation remains stubbornly low, and said that it was a question of time until the stronger economic conditions pushed inflation to higher levels. As for monetary policy, Draghi said the bank had not set an exact time for revisiting any changes to the current accommodative policy, but added that the ECB would review policy in September. These comments did not seem to break any new ground, but were perceived as hawkish by the markets and boosted the euro on Thursday.

Daily Technical Analysis: USDCHF

The USDCHF had a bearish momentum last week bottomed at 0.9438. We have a bearish pin bar as you can see on my daily chart below, indicates that price is ready to continue the bearish run after a rejection to move higher. The bias remains bearish in nearest term testing 0.0.9400 – 0.9350 region. Immediate resistance is seen around 0.9500 – 0.9550. A clear break above that area could lead price to neutral zone in nearest term but overall I prefer a bearish scenario at this phase and any upside pullback should be seen as a good opportunity to sell.

Daily Technical Analysis: USDJPY

The USDJPY continued its bearish momentum last week, broke below the daily EMA 200 and 111.45 key support as you can see on my daily chart below. This fact gives us further confirmation of bearish continuation scenario after formed double top formation and bearish pin bar at 114.50 as you can see on my daily chart below. The bias is bearish in nearest term testing 110.25/00 and the major trend line support located around 119.00/50 region. Immediate resistance is seen around 111.45. A clear break back above that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I remain neutral.