Sample Category Title

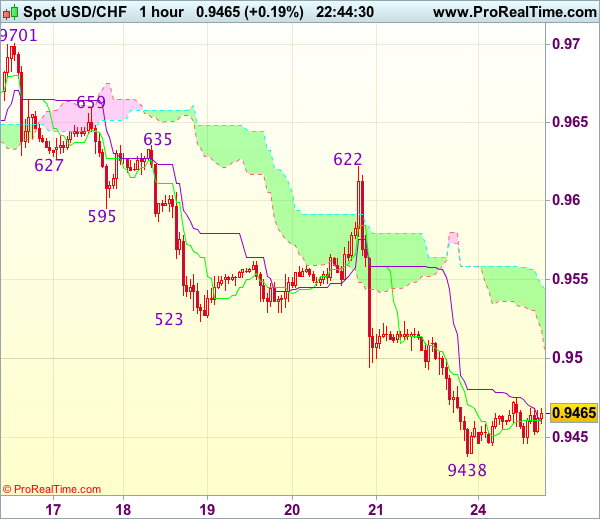

Trade Idea Wrap-up: USD/CHF – Sell at 0.9555

USD/CHF - 0.9461

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9461

Kijun-Sen level : 0.9460

Ichimoku cloud top : 0.9544

Ichimoku cloud bottom : 0.9506

Original strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

The greenback has recovered after falling to 0.9438 on Friday suggesting consolidation above this level would be seen and corrective bounce to 0.9500 and then 0.9520-25 cannot be ruled out, however, reckon the upper Kumo (now at 0.9544) would limit upside and bring another decline later, below said support at 0.9438 would extend recent decline to 0.9405-10 but loss of momentum should limit downside to 0.9375-80, price should stay above 0.9350, risk from there is seen for a rebound later.

In view of this, we are looking to sell dollar on recovery as 0.9550-55 should limit upside and bring another decline. Above 0.9580-85 would suggest a temporary low is formed instead, bring a stronger rebound towards resistance at 0.9622 which is likely to hold from here.

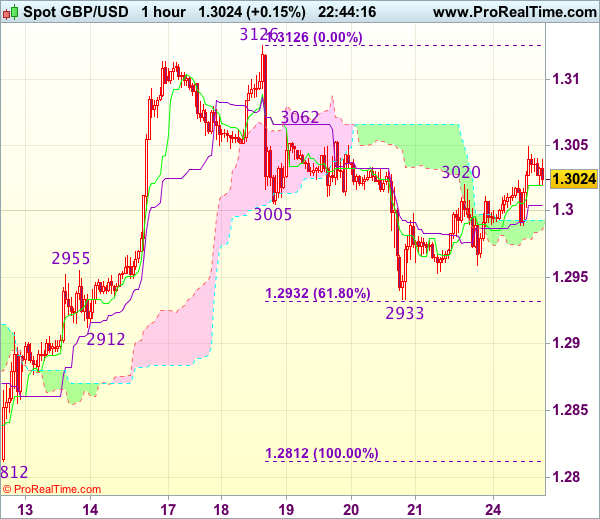

Trade Idea Wrap-up: GBP/USD – Sell at 1.3100

GBP/USD - 1.3043

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3019

Kijun-Sen level : 1.3004

Ichimoku cloud top : 1.2993

Ichimoku cloud bottom : 1.2986

Original strategy :

Sell at 1.3060, Target: 1.2960, Stop: 1.3095

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3100, Target: 1.2980, Stop: 1.3135

Position : -

Target : -

Stop : -

Cable found support at 1.2959 on Friday and has rebounded again, suggesting the recovery from 1.2933 may bring further gain to resistance at 1.3062, however, if our view that top has been formed at 1.3126 is correct, upside would be limited to 1.3100 and bring another decline later, below 1.2985-90 would signal an intra-day top is formed but break of 1.2950-55 is needed to signal the rebound from 1.2933 has ended, bring weakness to 1.2932-33 (61.8% Fibonacci retracement of 1.2812-1.3126 and said support), break there would extend the fall from 1.3126 top to previous support at 1.2912.

In view of this, we are looking to sell cable on further recovery as 1.3100-10 should limit upside. A firm break above 1.3100 would abort and suggest the fall from 1.3127 has ended instead, bring retest of this level but only break there would shift risk back to upside for further gain to 1.3150-60.

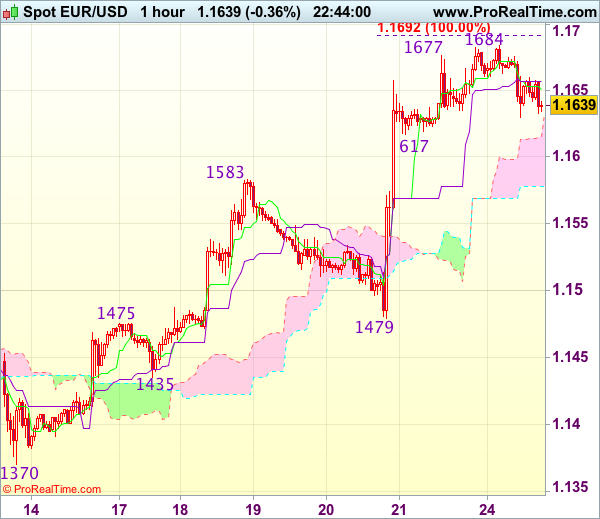

Trade Idea Wrap-up: EUR/USD – Buy at 1.1580

EUR/USD - 1.1643

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1651

Kijun-Sen level : 1.1657

Ichimoku cloud top : 1.1615

Ichimoku cloud bottom : 1.1578

Original strategy :

Buy at 1.1580, Target: 1.1680, Stop: 1.1545

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1580, Target: 1.1680, Stop: 1.1545

Position : -

Target : -

Stop : -

As the single currency has retreated after marginal rise to 1.1684, suggesting consolidation below this level would be seen and pullback to support at 1.1617 is likely, however, reckon previous resistance at 1.1583 would turn into support and contain downside, bring another rise later, above said resistance at 1.1684 would extend recent upmove to previous chart resistance at 1.1714 but break there is needed to retain bullishness for the rise from 1.0340 low to head towards 1.1750.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1583 should limit downside. Below 1.1550 would defer and suggest a temporary top is formed instead, bring correction to 1.1510-15 but support at 1.1479 should remain intact.

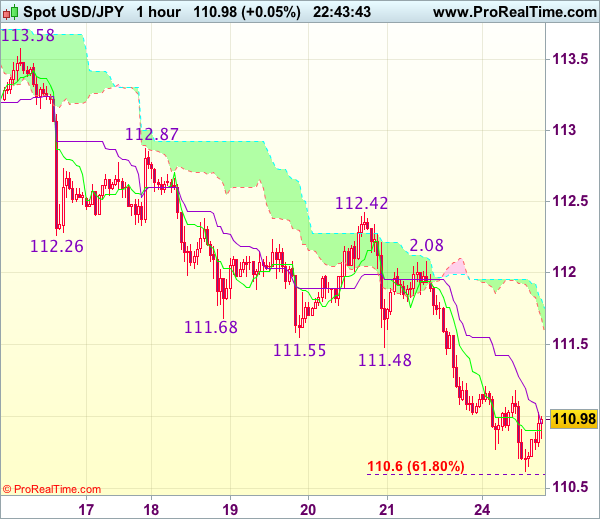

Trade Idea Wrap-up: USD/JPY – Sell at 111.45

USD/JPY - 111.06

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.90

Kijun-Sen level : 110.95

Ichimoku cloud top : 111.81

Ichimoku cloud bottom : 111.68

Original strategy :

Sell at 111.35, Target: 110.35, Stop: 111.70

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.45, Target: 110.45, Stop: 111.80

Position : -

Target : -

Stop : -

As the greenback has recovered after falling to 110.62, suggesting consolidation above this level would be seen, however, reckon upside would be limited to previous support at 111.48 (now resistance) and bring another decline, below said support at 110.62 would signal the selloff from 114.50 top is still in progress and extend to 110.60 (61.8% projection of 114.50-111.55 measuring from 112.42), then 110.30-35 but loss of downward momentum should prevent sharp fall below latter level and reckon 110.00-05 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on further recovery. Above previous support at 111.48-55 would defer and suggest a temporary low is formed, bring retracement of recent decline to 111.75-80, then towards resistance at 112.08.

Oil Traders Focus On St Petersburg Meeting | Bets On CFTC Data

- Oil traders want deeper oil production cut

- CFTC data in line with Central bank's reaction

Oil Traders Focus On St Petersburg Meeting

Oil traders have only one thing on their mind - the meeting between six OPEC and non OPEC ministers in St Petersburg. The hopes were high that perhaps they get some sort of clue or acknowledgement from the cartel that their current strategy is not yielding the outcome they were hoping for. More recently, the cartel was trying to put more pressure on countries like Libya and Nigeria which have ramped up their production as they were not handcuffed by the production cut deal.

Oil prices moved higher as the cartel was effective in brining one more member under their umbrella of the production cut. Nigeria agreed voluntarily to limit its production cut to 1.8 million barrels a day (once it reaches that level). Traders were hoping that they get some good news out of this event and they have it.

The net beneficiary of this will remain the US shale oil producers. Since the OPEC oil production cut, they took no time in taking the full leverage of this opportunity by swelling their production. Sadly for the OPEC, they have no control over them. At the current OPEC oil production, the cartel is not going to achieve the kind of results they are craving for, but the threat remains that any production cut by them would present an opportunity for the US shale oil producers.

Finally, on Monday, the oil traders are also paying attention to the fact that some producers are not adhering to their production cut agreement. For instance, Iraq's OPEC compliance has fallen to a low of 29 percent and this presents a threat to the oil production cut agreement. What we need is a strong statement which should send a rich message that there is no patience for any country not adhering to the rules set during this production cut.

Bets On CFTC Data

The CFTC data released on Friday has confirmed that traders have increased their long euro positions, reduced their sterling short positions and increased their yen short positions. The message is very much clear in this, the institutions are playing a strategy which is in tune with the perspective of the central bank's policies. However, reducing sterling short positions may end up badly as the central bank is not going to push the buttons on changing their monetary policy in the middle of the Brexit negotiation crisis. Even today, the IMF has lowered the growth forecast for the UK's economy although they did say that the economy would fall of the cliff if they leave the EU block. The Prime Minister, Theresa May, may be getting ready for a holiday break but the back benchers may take this opportunity to weaken her position as a leader and before we know it, we will have another election.

As for the dollar, short positions are still increasing and this is mainly due to political gridlock in the US, failure of the Trump administration in delivering anything so far, and the debt ceiling approaching. The Federal Chairwomen was pretty dovish in her last testimony in front of the senate. The upcoming FOMC statement on Wednesday would be very critical when it comes to the inflation part as that is a major denominator. Any change to this agenda could change the game altogether. Also we have the US GDP data due this week and even if the number produces a growth of 3% by any magic for the second quarter, it is not going to change the landscape of the yearly GDP.

Dollar Weighed by White House Turmoil after Sean Spicer Resignation Shakes up Trump’s Inner Circle

Following the recent developments connected with the investigation into Russia's ties with the US presidential election and Trump's failure to pass the health care bill in Congress for the second time, the uncertainty around Trump's administration peaked on Friday after Sean Spicer, the White House press secretary, resigned from his role. The dollar saw little immediate reaction to the news on Friday but last week's events weighed on the currency in forex markets today.

Sean Spicer announced on Friday his decision to leave the position of a press secretary at the White House, which he held for six months. The surprise resignation comes after Trump hired the former Wall Street financier and presidential fundraiser Antony Scaramucci as a director of the communication team. According to people who have an insight knowledge, Spicer refused to stay as secretary, expressing his opposition to the hiring as this would exacerbate uncertainty in the White House. Moreover, other sources suggest that further reshuffles in the media and legal teams have already taken place. Later in the day, Scaramucci, who addressed the daily briefing at the White House, named Sarah Huckabee Sanders as the new press secretary. Previously Sanders served as a deputy press secretary.

Regarding Scarammucci's new responsibilities, he is said to help the White House develop strategies in an attempt to deal with the Russian scandal. Last week, Special Council Rober Muller who was recently appointed to run the investigation into Russian interference in the 2016 election, questioned for the first time the financial relations between Trump's business and the Russian government, adding more confusion to the political turmoil. Besides that, on Saturday, Republican and Democrat leaders agreed on imposing additional sanctions on Russia as a punishment for its 2014 annexation of Crimea and its intervention in the US presidential election, putting Trump into a dilemma as any opposition to this would bring him into suspicion. The vote for the legislation, which also includes extra sanctions against Iran and North Korea, is due to take place on Tuesday.

With Trump's inner-cycle appearing to be falling apart and the president himself facing numerous political obstacles, investors are now far from convinced that Trump's administration will be able to deliver his promised economic agenda.

The latest troubles engulfing Trump drove the dollar to fresh lows in the forex markets. The dollar index hit a 13-month low of 93.82 earlier today, while against the yen, the greenback slid to a 5-week low of 110.60. Euro/dollar also touched fresh highs, rising to a 23-month top of $1.1684 and even the pound managed to post gains, rising back above the $1.30 level.

Japanese Yen Unchanged, BoJ Minutes Next

USD/JPY has ticked lower in Monday trading. In the North American session, the pair is trading slightly below the 109 line. On the release front, Japanese Flash Manufacturing ticked higher to 52.2, above the estimate of 52.3 points. In the US, Existing Home Sales dropped to 5.52 million, well short of the estimate of 5.59 million. Later in the day, the BoJ releases the minutes of its June policy. On Tuesday, the US releases CB Consumer Confidence.

The Japanese economy continues to show improvement, but inflation remains stubbornly low, well below the BoJ's target of 2%. Last week, there were no surprises from the Bank of Japan, which maintained its ultra-loose monetary policy. The bank kept interest rates at 0.10% and maintained its inflation target at 2.0%. However, in light of the low inflation levels, the BoJ extended the timeline for the inflation target by one year, saying it expected inflation to reach 2% by fiscal year 2020. The BoJ has maintained its inflation target since 2013 and has had to postpone the timeline six times, as the bank's radical asset-purchase program has failed to end deflation. BoJ Governor Haruhiko Kuroda has insisted that the inflation target is feasible, blaming low inflation on external factors, such as low oil prices. The bank was more upbeat in its economic forecast than in June, but with the bank stubbornly clinging to its inflation target, the markets don't expect any withdrawal of stimulus until 2018 at the earliest.

It was another bad week for President Trump. Early in the week, Trump's cherished flagship healthcare proposal, which aims to replace Obamacare, stalled in the Senate after two Republican senators said they would not support the bill. Trump has failed to pass any significant legislation so far in his term, and investors are becoming more skeptical as to whether Trump will have any more success with his tax reform and fiscal spending plans. With the Democrats forming a rock-solid wall of opposition, dissension among Republican lawmakers, many of whom are uneasy about Trump, could doom attempts by the White House to get bills through Congress. There was more bad news as Robert Mueller, the special counsel who is investigating alleged collusion between Trump and Russian officials during the US election, said he would review business transactions involving Trump as well as his associates. Trump has said that Mueller's scope is limited to Russia, so the stage could be set for a Nixon-type showdown between the president and the special counsel investigating wrongdoing by the president.

NZDUSD Moving Up on Wave 3, More Upside to Follow

NZDUSD is showing us a three-wave bullish recovery in progress, with current move up from 0.7262 level representing red wave 3). We know wave three is usually the strongest and steepest wave, which means more upside can follow in sessions ahead. Specifically, we see price now trading within sub-wave 4 of three, that can search for a potential base near the Fibonacci ratio of 23.6/38.2, before make another push higher, towards the upper channel line.

NZDUSD, 1H

USDCAD Dented Psychological 1.2500 Support

The pair dented psychological 1.2500 support on fresh extension of broader downtrend on Monday. Loonie received support from better than expected Canada wholesale sales, keeping very firm tone against the greenback. Technical studies remain is strong bearish setup and favor final push towards target and key support at 1.2459 (3 May 2016 low). Meanwhile, bears may show stronger hesitation at important 1.2500 support, although daily indicators continue to point lower despite being in deep oversold territory and lacking any signal of reversal. The pair is riding on extended wave C (commenced from 1.3538)v which approached its FE 261.8% at 2.2484 and may extend to its FE 300% at 1.2330 on sustained break below 1.2459 support. The first solid resistance lies at 1.2659 (falling 10SMA) followed by daily Tenkan-sen (1.2718) with break of these barriers needed to signal stronger recovery. FOMC meeting ends on Wednesday and markets are expecting fresh signals on tone of Fed's post-meeting statement.

Res: 1.2552; 1.2608; 1.2659; 1.2718

Sup: 1.2484; 1.2459; 1.2400; 1.2330

Dollar Rally/Euro Decline Slows

- European equities traded initially lower on euro strength. Later in the session, a fall in euro strength reversed the decline. The German Dax underperformed (around -0.35%) on the back of weak carmakers. US equities open with modest losses.

- The Eurozone PMI fell to 55.8 in July from 56.3 in June. The consensus expected a minor decline to 56.2. Increases in manufacturing costs are starting to slow, with the rise in input costs the lowest since November. Meanwhile, growth in new orders and employment is still strong.

- The Saudi Energy and Industry minister pushed to improve implementation of the production cuts from the nations participating in the deal as compliance dropped from 110% in May to 92% in June. He also said Nigeria and Libya -- both exempt from cutting -- will be allowed to increase output to their targeted levels.

- Poland's president Duda vetoed part of a controversial overhaul of the judiciary that's brought national protest and pitted the nation's government against its partners in the EU and the US. Duda ordered a rewrite of the two bills he rejected and said he'd approve a final piece of legislation giving politicians more control of lower courts.

- According to the Athens Stock exchange filing, Greece is looking to sell five-year bonds on Tuesday. This marks the first return to the debt market since 2014. With the sale, the government of Prime Minister Tsipras is seeking to test the market appetite as the exit from the current bailout program in August 2018 draws nearer.

- In an update to its World Economic Outlook, the IMF changed its annual GDP forecast for the UK to 1.7% this year, compared to a forecast of 2% growth made in April. The 2018 forecast was unchanged at 1.5%. Reasons for the decline are rising inflation, resulting from the weaker pound, which pressures household spending.

- The Republican effort to repeal and replace Obamacare faces a major test this week as the US Senate will decide whether to move forward and vote on a bill whose details and prospects are still uncertain. President Trump, after initially suggesting that he was fine with letting Obamacare collapse, has urged the senators to hash out a deal.

Rates

German 10-yr yield tests key support in dull session

Global core bonds traded mixed today. German Bunds outperformed US Treasuries. This week's US supply operation might be at play. Volumes remained very low though and daily changes small. The Bund gained some ground in European dealings, around the time of comments by ECB governor Nowotny. The Austrian normally has a more hawkish profile, but he said that advances in IT and growing flexibility in the labour market could naturally cap inflation and potentially affect monetary policy. EMU eco data included the important PMI's. National data (France, Germany) pointed at some disappointment for the EMU readings, which eventually manifested in a larger than forecast decline for the EMU manufacturing PMI, while the services PMI stabilized. Both are still at lofty levels. Oil prices recovered somewhat from Friday's weakness as Saudi Arabia and Russia called on smaller oil producers to comply with supply curbs. Most European equity markets stabilized after the sell-off at the end of last week with Germany (car makers) underperforming. The Bund didn't react on the evolution of commodity and stock markets.

At the time of writing, German yield changes range between -0.8 bps (10-yr) and -1.8 bps (2-yr). The German 10-yr yield is still testing key support (0.5%). US yields gain around 1.5 bps across the curve. On intra-EMU bond markets, 10-yr yield spread changes versus Germany are virtually unchanged with Greece underperforming following a supply announcement. Greece has mandated six banks today for its return to the debt market with a new 5-yr bond. It would be the first international transaction since 2014.

The Belgian debt agency tapped three on the run OLO's: 7-yr OLO 79 (€1B 0.2% Oct2023), 10-yr OLO 81 (€1.12B 0.8% Jun2027) and 30-yr OLO 78 (€0.68B 1.6% Jun2047) for a combined €2.8B, the maximum targeted amount. Demand was in line with average with an auction bid cover of 1.6. Belgium already completed 81.4% of this year's stated OLO funding need (€35B).

Currencies

Dollar rally/euro decline slows

Today, the dominant FX trends that ruled trading halted. The decline of the dollar slowed and so did the rise of the euro. The pause in the euro rally was 'justified' by softer than expected EMU PMI's. There was no high profile news to inspire a directional USD move. EUR/USD stabilizes in the mid 1.16 area. USD/JPY failed to sustain north of 111 (currently 110.80).

This morning, the dollar remained in the defensive. EUR/USD held near the recent top in the high 1.16 area, but there were no further follow-through losses. USD/JPY drifted south early in the session but tried to regain the 111 barrier going into the start of the European session.

The euro fell prey to modest profit taking at the start of European dealings. The move gained some traction as the EMU PMI's came out softer than expected. EUR/USD dropped to the 1.1630/40 area. The decline also spilled over into the EUR/JPY and USD/JPY cross rates. It was primarily a technical setback after the recent rally. The "poor" PMI's were nothing more than a good excuse. Interest rate differentials also re-widened marginally in favour of the dollar. Whatever the reason, it all didn't go far. Dollar weakness already resurfaced toward the end of the European morning session.

There was also no high profile news in the US to inspire trading. The dollar continued to trade off the intraday lows, but there is no sign of any significant USD rebound. EUR/USD trades currently in the 1.1640 area. USD/JPY hovers near 111. Conclusion, the dollar decline slowed and the euro rally shifted into a lower gear, but the trends remain in place.

GBP succeeds insignificant comeback

Sterling staged a technical rebound against the dollar and the euro. At the end of last week, the poor results of the first round of negotiations between the UK and the EU weighed on the UK currency. Today's rebound of sterling was primarily technical in nature. The eco news was intrinsically negative for sterling. The IMF downwardly revised the UK 2017 growth forecast to 1.7% Y/Y (from 2.0% in April). IHS markit also reported that its household financial index dropped to the lowest since July 2014 due to rising costs of living. However, all this didn't prevent a modest technical rebound of the sterling. EUR/GBP trades currently in the 0.8945 area. Cable returned north of 1.30. The first estimate of the UK Q2 GDP, to be published on Wednesday, will be the next key factor for sterling trading.