Sample Category Title

Daily Technical Analysis: EUR/USD Bounces At 1.1625 And Breaks Resistance Within Wave-3

Currency pair EUR/USD

The EUR/USD is building a minor correction within the larger uptrend (blue line). A bullish continuation is likely to see price test the 1.1750 round resistance level. The momentum is part of a wave 3 (orange) which is part of larger wave 5 (purple) of wave 3 (green).

The EUR/USD broke the support trend line (dotted blue) of the rising wedge chart pattern mentioned in yesterday's analysis. Price retraced back to the 38.2% Fibonacci level of wave 4 (purple) and bounced at the support level. The bullish breakout above the correction and resistance trend line (dotted red) could price move towards the Fibonacci targets of wave 5 vs 1+3.

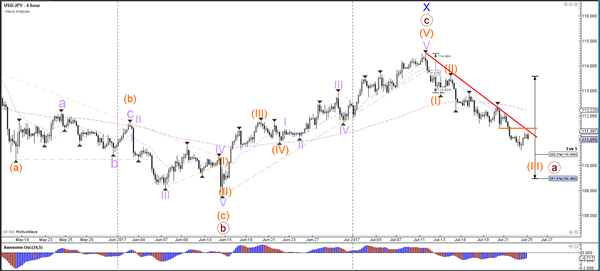

Currency pair USD/JPY

The USD/JPY has bounced the 200% Fibonacci target of wave 3 vs 1 (orange) but the retracement could stop at the resistance trend lines (red and orange).

The USD/JPY completed a wave 3 (green) and made a retracement to the 50% Fibonacci level of wave 4 vs 3. Price turned at the resistance and broke below the support trend line (dotted blue) which could indicate a bearish breakout towards the Fibonacci targets of wave 5 vs 1+3.

Currency pair GBP/USD

The GBP/USD could be building a correction via a WXY (purple) wave pattern. A break below the small channel (blue) would indicate the potential for price to retrace lower towards the 61.8% Fibonacci target of wave Y vs W.

The GBP/USD is completing an ABC (grey) correction within wave X (purple) unless price manages to break above the channel, which could see price test the previous top and Fibonacci levels.

European Open Briefing: AUD Demand Remains Strong

Global Markets:

- Asian stock markets: Nikkei down 0.10 %, Shanghai Composite lost 0.15 %, Hang Seng rose 0.05 %, ASX 200 rallied 0.90 %

- Commodities: Gold at $1255 (+0.10 %), Silver at $16.45 (+0.05 %), WTI Oil at $46.60 (+0.60 %), Brent Oil at $48.90 (+0.55 %)

- Rates: US 10-year yield at 2.25, UK 10-year yield at 1.19, German 10-year yield at 0.51

News & Data:

- Dollar recovers from 13-month low on strong PMI readings, Asia stocks tread water – RTRS

Markets Update:

The US Dollar recovered slightly yesterday, following stronger than expected US economic data. However, the currency quickly lost momentum and came again under pressure in Asia.

EUR/USD bounced off 1.1620 support and is heading again towards 1.17. The Euro remained well bid despite the disappointing PMI numbers out of the Euro Zone countries, which shows that demand is still high.

GBP/USD rose from 1.3015 to 1.3035 in Asia. The Pound is likely to struggle in the near-term amid uncertainty around Brexit and a reluctant Bank of England. Heavy resistance is seen in the area between 1.31 and 1.3120.

USD/JPY is testing 111 support again, and the outlook is negative. A test of 110 should follow soon, and downside momentum will increase should the pair break below that level.

AUD demand remains strong. AUD/USD bounced ahead of 0.79 and reached a high of 0.7945 in Asia. The pair should test 0.80 soon, and a break above that level would then signal an extension of the rally to 0.82. The main risk for the AUD rally are the inflation numbers which will be released on Wednesday. Disappointing figures could put the Australian Dollar under some pressure, although losses are likely to be limited to 0.7840.

Upcoming Events:

- 09:00 BST – German IFO Business Climate

- 14:00 BST – US House Price Index

- 15:00 BST – US CB Consumer Confidence

Aussie Dollar Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.13% against the USD and closed at 0.7925.

Yesterday, the IMF slightly upgraded China's growth forecast to 6.7% for 2017, up from 6.6% estimated earlier.

LME Copper prices declined 0.02% or $1.5/MT to $6000.0/MT. Aluminium prices declined 0.6% or $11.0/MT to $1890.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7933, with the AUD trading 0.1% higher against the USD from yesterday's close.

The pair is expected to find support at 0.7901, and a fall through could take it to the next support level of 0.7870. The pair is expected to find its first resistance at 0.7966, and a rise through could take it to the next resistance level of 0.8000.

Moving ahead, Australia's consumer price index for 2Q, slated to release in the early hours' tomorrow, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Manufacturing Sector Across The Euro-Zone Grew At Its Slowest Pace In 3 Months In July

For the 24 hours to 23:00 GMT, the EUR declined 0.26% against the USD and closed at 1.1640, after data indicated that manufacturing sector growth across the Euro-zone moderated at the start of the third quarter.

The Euro-zone's preliminary Markit manufacturing PMI dropped more-than-expected to a level of 56.8 in July, hitting its lowest level in three months and compared to a reading of 57.4 in the prior month. Markets were anticipating the PMI to fall to a level of 57.2. Meanwhile, the region's flash Markit services PMI remained steady at a level of 55.4 in July, in line with market expectations.

Separately, Germany's manufacturing sector expanded at its weakest pace in three months in July, after it dropped more-than-anticipated to a level of 58.3, compared to a reading of 59.6 registered in the prior month, while investors had envisaged the PMI to drop to a level of 59.2. Moreover, activity in the nation's services sector unexpectedly slowed to a six-month low level of 53.5 in July, defying market consensus for an advance to a level of 54.3. In the prior month, the PMI had registered a reading of 54.0.

Separately, the International Monetary Fund (IMF), in an updated World Economic Outlook, upgraded the Euro-zone's economic growth projection for 2017 to 1.9%, up from 1.7% estimated earlier in April, citing solid growth momentum in the single currency region. Meanwhile, the Fund kept its growth forecasts for the world economy unchanged for this year and next.

In the US, data revealed that the flash Markit manufacturing PMI advanced to a four-month high level of 53.2 in July, surpassing market expectations for a rise to a level of 52.3 and compared to a reading of 52.0 in the prior month. Further, the nation's preliminary Markit services PMI remained steady at a level of 54.2 in July, meeting market expectations.

On the other hand, existing home sales in the US unexpectedly eased 1.8% on a monthly basis, to a level of 5.52 million in June, declining to its lowest level since February 2017. Existing home sales registered a reading of 5.62 million in the prior month, while markets were expecting it to remain unchanged at 5.57 million.

Meanwhile, the IMF revised down US economic growth forecast to 2.1% for this year and next, citing the US President, Donald Trump's struggle to deliver on policy and stimulus.

In the Asian session, at GMT0300, the pair is trading at 1.1653, with the EUR trading 0.11% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1628, and a fall through could take it to the next support level of 1.1602. The pair is expected to find its first resistance at 1.1677, and a rise through could take it to the next resistance level of 1.1700.

Moving ahead, investors will focus on Germany's Ifo business climate and expectations indices for July, slated to release in a few hours. Moreover, the US consumer confidence index for July, due to release later in the day, will pique significant amount of investor attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

IMF Lowered Britain’s 2017 Growth Forecasts Amid Tepid First Quarter Growth

For the 24 hours to 23:00 GMT, the GBP rose 0.11% against the USD and closed at 1.3023.

Yesterday, the IMF slashed Britain's growth forecast for 2017 by 0.3% to 1.7%, factoring in a weaker-than-expected first quarter economic growth.

In the Asian session, at GMT0300, the pair is trading at 1.3027, with the GBP trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.2991, and a fall through could take it to the next support level of 1.2956. The pair is expected to find its first resistance at 1.3060, and a rise through could take it to the next resistance level of 1.3094.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

IMF Slightly Revised Up Japan’s Growth Forecast For 2017

For the 24 hours to 23:00 GMT, the USD rose 0.22% against the JPY and closed at 111.17.

Yesterday, the IMF stated that it expects Japanese economy to expand by 1.3% this year, buoyed by stronger private consumption, investment and exports. The organisation had projected a growth of 1.2% in April.

On the data front, Japan's final leading economic index rose to a level of 104.6 in May, compared to a reading of 104.2 in the prior month, while the preliminary figures had indicated an advance to a level of 104.7. On the other hand, the nation's final coincident index fell less than initially estimated to a level of 115.8 in May, compared to a reading of 117.1 in the prior month. The index had registered a drop to a level of 115.5 in the flash estimate.

In the Asian session, at GMT0300, the pair is trading at 111.07, with the USD trading 0.09% lower against the JPY from yesterday's close.

Earlier today, minutes of the Bank of Japan (BoJ) showed that board members were divided on how much information they should disclose to the public about a possible exit from ultra-loose monetary policy.

The pair is expected to find support at 110.68, and a fall through could take it to the next support level of 110.29. The pair is expected to find its first resistance at 111.4, and a rise through could take it to the next resistance level of 111.73.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Swiss Franc Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.11% against the CHF and closed at 0.9472.

In economic news, Switzerland's total sight deposits rose to a level of CHF579.1 billion in the week ended 21 July, compared to a level of CHF578.9 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9466, with the USD trading 0.06% lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9448, and a fall through could take it to the next support level of 0.9431. The pair is expected to find its first resistance at 0.9481, and a rise through could take it to the next resistance level of 0.9497.

Amid a lack of any macroeconomic releases in Switzerland today, trading trend in the CHF is expected to be determined by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

IMF Forecasted Stronger Economic Growth For Canada In 2017

For the 24 hours to 23:00 GMT, the USD declined 0.3% against the CAD and closed at 1.2510.

Yesterday, the IMF raised its growth outlook for Canadian economy, now expecting it to grow by 2.5% in 2017, up from its April projection of 1.9%.

On the macro front, Canada's wholesale sales climbed 0.9% MoM in May, higher than market expectations for an advance of 0.5%. Wholesale sales had recorded a revised rise of 0.8% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2505, with the USD trading a tad lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2475, and a fall through could take it to the next support level of 1.2446. The pair is expected to find its first resistance at 1.2543, and a rise through could take it to the next resistance level of 1.2582.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

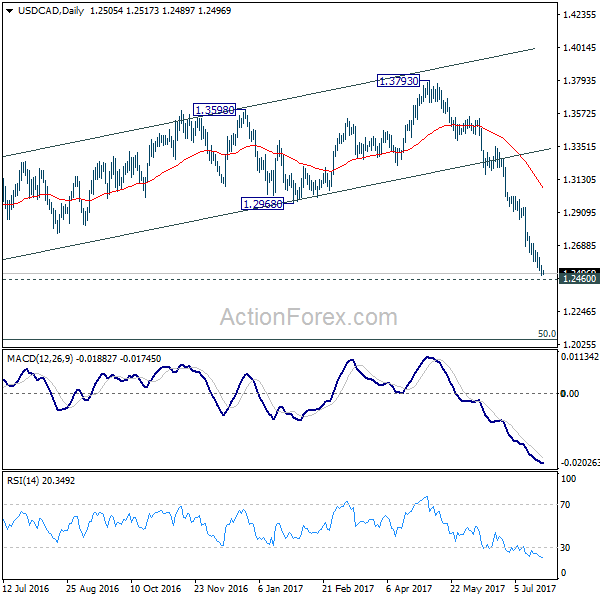

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2478; (P) 1.2514; (R1) 1.2546; More....

Intraday bias in USD/CAD remains on the downside for 1.2460 key support level. Considering bullish convergence condition in 4 hour MACD, we'll be cautious on strong support from there to contain downside and bring rebound. On the upside, break of 1.2608 minor resistance will indicate short term bottoming and turn bias back to the upside for 1.2968 support turned resistance. However, firm break of 1.2460 will target next key fibonacci level at 1.2048.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Fall from 1.3793 is seen as the third leg and should target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Forex Markets Tread Water, Canadian Dollar Firm as Supported by Recovery in Oil Price

The forex markets are treading water in a rather dull start to the week, staying mostly in ranges. Other financial markets are mixed too. NASDAQ hit record high overnight and closed up 0.36% at 6410.81. But DOW and S&P 500 closed down by -0.31% at 21513.17 and -0.11% at 2469.91 respectively. Treasury yield staged a mild recovery with 10 year yield closed up 0.022 at 2.254. Asian markets are trading in tight range with mild loss in Nikkei as it struggles to regain 20,000 handle. In other markets, Gold is losing some upside momentum ahead of 1260 but is staying near term bullish. WTI crude oil is back above 46.6 on recovery and helped keeping USD/CAD below 1.25 handle.

BoJ minutes showed members divided on revealing exit strategy

The minutes of the June 15-16 BoJ meeting showed that board members were divided on how much information about exit strategy should be revealed to the public. The minutes noted that "some members said it was important to thoroughly explain the BOJ's thinking on how it will manage policy and the impact on the central bank's finances to gain understanding." On the other hand, "several members said providing uncertain information before meeting the inflation target could cause market confusion, so it is important to continue internal analysis on this subject." BoJ will released summary of opinions in the July meeting later on Friday, which could more information on the discussions afterwards.

Crude Oil Recovers as Saudi Arabia Promised to Cut Exports in August

Oil price recovered mildly after Saudi Arabia's oil minister Khalid Al-Falih announced that it would cap its exports at 6.6M bpd in August, 1M bpd below that the same period last year. He acknowledged that "the market has turned bearish with several key factors driving these sentiments", admitting that weaker compliance with cuts by some OPEC states and a rise in OPEC exports were one of the factors leading to weaker oil prices. He added that "some countries continue to lag which is a concern we must address head on" and "exports have now become the key matrix to financial markets and we need to find a way to reconcile credible exports data with production data". On the global oil demand outlook, Falih expect growth would reach +1.4- 1.6M bpd in 2018, a rate that should offset US output expansion.

Markets awaiting FOMC

FOMC meeting is the highlight of the week even though Fed is not expected to make any change to its monetary policies. Opinions are divided on what Fed would do in the second half of the year. One more rate hike and an announcement to shrink the balance is still the base case for most analysts. But more are now leaning towards the case for Fed to hike in December, rather than September. Fed fund futures are pricing in less that 10% chance of a September hike, and around 50% chance of December hike.

While Fed officials are seeing the slow down in inflation in Q2 as due to temporary factors, it might take a few more months to convince them that this is the correct view. Also, there are still a lot of uncertainties on what fiscal policies US President Donald Trump would deliver. IMF lowered growth forecasts for US to 2.1% in 2017 and 2.1% in 2018, sharply down from April projection of 2.3% and 2.5% respectively. And, "uncertainty about the timing and nature of U.S. fiscal policy changes" was cited as the key reason behind the downgrade. Hence, Fed could just announce a change in its reinvestment plan in September to start unwinding the balance sheet first.

Looking ahead for today

German Ifo business climate will be the main focus in European session. Germany will release import price index while UK will release CBI trends total orders. US will release house prices and consumer confidence.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2478; (P) 1.2514; (R1) 1.2546; More....

Intraday bias in USD/CAD remains on the downside for 1.2460 key support level. Considering bullish convergence condition in 4 hour MACD, we'll be cautious on strong support from there to contain downside and bring rebound. On the upside, break of 1.2608 minor resistance will indicate short term bottoming and turn bias back to the upside for 1.2968 support turned resistance. However, firm break of 1.2460 will target next key fibonacci level at 1.2048.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Fall from 1.3793 is seen as the third leg and should target 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes June Meeting | ||||

| 06:00 | EUR | German Import Price Index M/M Jun | -0.70% | -1.00% | ||

| 08:00 | EUR | German IFO - Business Climate Jul | 114.9 | 115.1 | ||

| 08:00 | EUR | German IFO - Expectations Jul | 106.5 | 106.8 | ||

| 08:00 | EUR | German IFO - Current Assessment Jul | 123.8 | 124.1 | ||

| 10:00 | GBP | CBI Trends Total Orders Jul | 12 | 16 | ||

| 13:00 | USD | House Price Index M/M May | 0.50% | 0.70% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y May | 5.80% | 5.67% | ||

| 14:00 | USD | Consumer Confidence Jul | 116 | 118.9 |