Sample Category Title

Forex Technical Analysis: USD/JPY

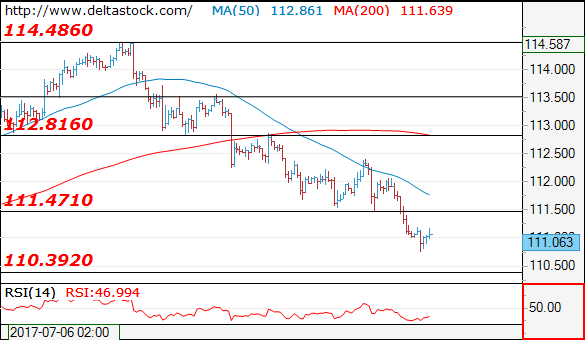

USD/JPY

Current level - 111.06

The downtrend remains absolutely intact and a break through 110.30 support should challenge directly 109.30 dynamic projection. Minor intraday resistance lies at 111.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

111.50 |

114.50 |

110.30 |

110.30 |

|

112.80 |

115.50 |

109.30 |

108.10 |

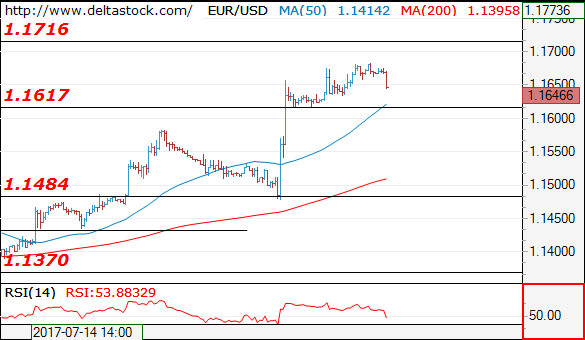

Forex Technical Analysis: EUR/USD

EUR/USD

Current level - 1.1646

The recent peak at 1.1682 has initiated a minor pullback and the intraday bias is negative, for a test of 1.1617 and even 1.1580 area. Major hurdle lies at 1.1720.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1683 |

1.1720 |

1.1580 |

1.1370 |

|

1.1720 |

1.1720 |

1.1480 |

1.1290 |

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

USD/JPY – 110.85

The greenback only recovered to 112.42 late last week before meeting renewed selling interest and the subsequent selloff adds credence to our bearish view that the rebound from 108.82 has ended at 114.50 and the decline from this top is still in progress for further weakness to 110.00, having said that, as broad outlook remains consolidative, reckon downside would be limited to 109.40 and said support at 108.82 should remain intact.

On the upside, whilst initial recovery to 111.40-50 is likely, reckon upside would be limited to resistance at 112.08 and bring another decline later. A daily close above said resistance at 112.42 would defer and suggest low is possibly formed, bring test of the Kijun-Sen (now at 112.60), break there would suggest first leg of decline from 114.50 has ended, bring a stronger rebound to 113,00, however, still reckon upside would be limited to 113.55-60 and 114.00 should hold, bring another decline later.

Recommendation : Sell again at 112.00 for 110.00 with stop above 113.00.

On the weekly chart, as dollar’s retreat from 114.50 has kept price under near term pressure, adding credence to our view that top is possibly formed at 114.50 and consolidation with downside bias remains for weakness to the lower Kumo (now at 110.25), below there would extend fall to 109.40-50, however, reckon indicated support at 108.82 would limit downside and price should stay well above support at 108.13, bring recovery later.

On the upside, although recovery to the Tenkan-Sen (now at 111.66) cannot be ruled out, reckon upside would be limited to 112.05-10 and bring another decline later to aforesaid downside targets. Above 112.42 would bring a strong recovery to 113.00, however, reckon upside would be limited to 113.55-60 and price should falter well below said resistance at 114.50. Only a break above 114.50 would signal the rebound from 108.13 is still in progress for gain towards resistance at 115.51 but a weekly close above there is needed to signal the fall from 118.66 top has ended at 108.13, then headway to 116.00-10 would follow but resistance at 117.53 should hold from here.

Currencies: Dollar Continues Fighting An Uphill Battle

Sunrise Market Commentary

- Rates: New upward potential Bund, especially if German 10y yield drops below 0.5%

Draghi's dovish performance on Thursday, the risk-off correction on European stock markets (Thursday/Friday) and the volatile, but downwardly oriented, oil price (Friday ahead of today's OPEC vs non-OPEC meeting) suggests some more consolidation in the Bund (correction higher). The German 10-yr yield tests important support (0.5%). - Currencies: Dollar continues fighting an uphill battle

Dollar weakness continues to dominate USD trading. Political uncertainty in the US weighs on the US currency and Draghi's comments didn't prevent further by-default euro buying. Today's US and EMU confidence data probably won't change the established USD negative trend. We don't expected a meaningful comeback of the dollar ahead of the Fed policy decision

The Sunrise Headlines

- European equities were hard hit on Friday, as the euro continued to gain ground against the dollar. US equities ended little changed after recouping early losses. Asian equities trade mostly slightly positive overnight with the exception of the Japanese equities which are hit by yen strength.

- Japanese PMI business confidence weakened slightly in July. The headline index fell to 52.2 from 52.4 in June. Levels above 50 suggest expanding activity.

- A new EU competition investigation into Germany's top carmakers threatens the credibility of the entire industry, a German minister has warned, after Brussels confirmed it was probing suspected collusion on technology.

- Better growth in China, the euro zone and Japan is making up for a slower US economy, Trump's stalled economic promises and a faltering UK, the IMF said. 2017/18 global growth was confirmed at 3.5%/3.6%.

- Greece's sovereign credit rating's (B-) outlook was raised to positive by S&P, boosting the government in Athens, as it ponders a return to bond markets. The IMF agreed to a new $1.8B conditional loan for Greece on Thursday.

- Brent oil stabilized around $48/barrel overnight, after dropping sharply on Friday and ahead of a meeting between OPEC and non-OPEC regarding production cuts later today.

- Today, the market calendar contains the EMU and US July PMI business surveys, the US Existing Home sales and speeches of ECB Smets and BoE Brazier. OPEC meets non-OPEC countries to discuss production cuts.

Currencies: Dollar Continues Fighting An Uphill Battle

USD fights an uphill battle

On Friday, overall dollar weakness continued to dominate FX trading. Uncertainty on the potential political fall-out of the investigations against president Trump and people close to him are weighing on the dollar. At the same time, the euro extended a by default rally. Draghi's comments on the ECB press conference can only be considered as soft, but he also didn't seem overly worried on the recent euro strength. EUR/USD closed the session at 1.1683 (from 1.1631). USD/JPY finished the week at 111.13 (from 111.61 on Thursday evening).

Today, attention goes to the business sentiment data (Markit) and to a meeting between OPEC and non-OPEC countries in Russia. The EMU business sentiment indicators showed an unexpected mixed picture (at high levels) in June. The manufacturing PMI still improved, but the services PMI declined. Given the additional euro strength, we see downside risks for the manufacturing sector in July, but maybe some rebound in services confidence, as domestic demand fundamentals remain strong. The EMU data probably won't be a game-changer for euro trading, unless they show a really big surprise. If data would be unexpectedly strong, they might reinforce euro positive momentum. The focus will be on the US side of the story. Political uncertainty is probably here to stay and won't help the dollar short-term. Markets will also look forward to the Fed policy decision on Wednesday. The Fed will confirm its intention to continue policy normalisation and might even give some concrete hints on the start of the reduction of the balance sheet. At the same, time they probably can't ignore the recent softening in inflation. There is already quite some negative news discounted for the dollar after the recent setback, but we see no trigger yet for a positive U-turn on the US dollar. For that to happen, the dollar needs some really positive news. Strong US eco data next week might bring some relief, but that's still far away. For now there is not good reason to try to catch the falling knife.

USD: technical picture worsens further

EUR/USD rebounded above the 1.1300/66 resistance at the end of June. The payrolls and other recent data were not good enough to trigger a sustained USD rebound. Finally EUR/USD broke beyond the 1.1489/1.15 resistance, paving the way to the LT-correction tops at 1.1616/1.1714. A break would end the long consolidation that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area is not easy to break. We don't preposition for a break, but the pressure is mounting. Return action below 1.13 would be a first indication of a loss in upside momentum.

The USD/JPY rally ran into resistance in May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair above the 112.13 correction top, but follow-through gains remain modest. USD/JPY 114.37 resistance was tested, but the test was rejected. The pair is currently drifting lower in the brooder consolidation pattern between 114.50 on the topside and 108.83/13 on the downside. A test of the downside is of the range is becoming ever more likely?. This suggests a pause in the recent USD/JPY uptrend. We stay cautious on USD/JPY long positions despite the recent decent performance

EUR/USD: top MT consolidation pattern under heavy strain

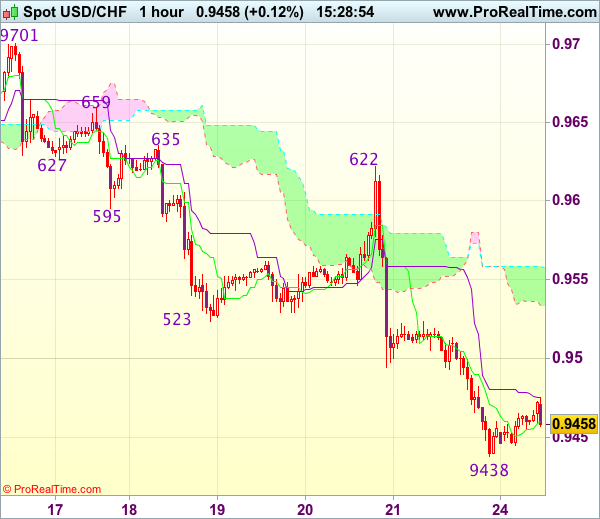

Trade Idea : USD/CHF – Sell at 0.9555

USD/CHF - 0.9475

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9460

Kijun-Sen level : 0.9476

Ichimoku cloud top : 0.9558

Ichimoku cloud bottom : 0.9533

Original strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9555, target: 0.9455, Stop: 0.9590

Position : -

Target : -

Stop : -

The greenback has recovered after falling to 0.9438 on Friday suggesting consolidation above this level would be seen and corrective bounce to 0.9500 and then 0.9520-25 cannot be ruled out, however, reckon the upper Kumo (now at 0.9558) would limit upside and bring another decline later, below said support at 0.9438 would extend recent decline to 0.9405-10 but loss of momentum should limit downside to 0.9375-80, price should stay above 0.9350, risk from there is seen for a rebound later.

In view of this, we are looking to sell dollar on recovery as 0.9550-55 should limit upside and bring another decline. Above 0.9580-85 would suggest a temporary low is formed instead, bring a stronger rebound towards resistance at 0.9622 which is likely to hold from here.

USD/CHF Hit The Critical Support

USD/CHF bounced back from the 0.9440 long term support level, yesterday we had a false breakdown below this level, but only an accumulation could give birth to another leg higher. Moves within an extended sideways movement on the long term, so a valid breakdown below the 0.9440 static support will confirm a further drop in the upcoming months.

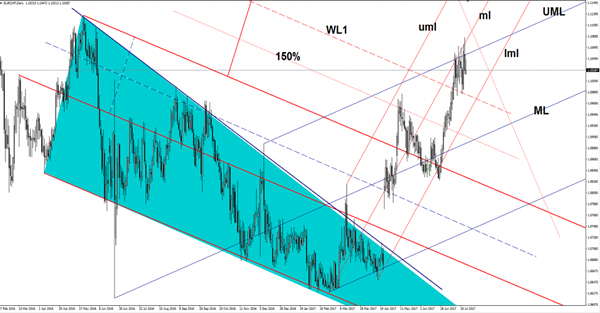

EUR/CHF Further Correction Favored

The EUR/CHFfailed once again to take out a major dynamic resistance and now could go down on the Daily chart.

Price dropped aggressively in the yesterday’s trading session, we had another false breakout above the upper median line (UML) of the major ascending pitchfork and above the median line (ml) of the minor ascending pitchfork. Could drop much deeper in the upcoming days because looks too overbought to climb much higher on the Daily chart at this moment.

Could approach the 1.1000 level in the upcoming days and the lower median line (lml) of the minor ascending pitchfork.Only a breakdown from the minor ascending pitchfork’s body will confirm a larger drop.

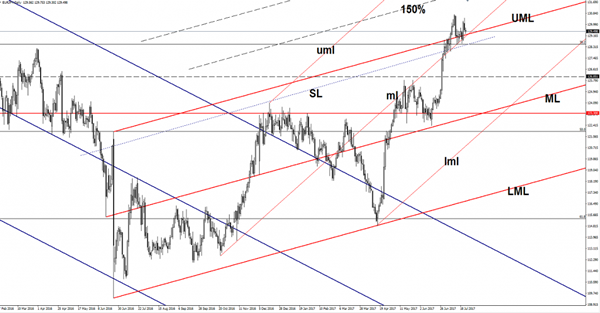

EUR/JPY Buying Opportunity?

The currency pair has decreased since yesterday and could come down to test and retest the support levels before will climb much higher. Is trading much above the 129.50 psychological level and maintains a bullish perspective on the Daily chart.

Looks like that is consolidation because needs to recapture more directional energy before will approach new highs, we have to wait for a confirmation that will continue the upside movement. We have to be careful because the Yen could start another leg higher if the Nikkie stock index will drop further.

The JP225 moves sideways on the short term, remains to see if this will be an accumulation or a distribution movement. The index looks a little exhausted on the Daily chart and failed once again to stay above the 20058 static resistance and could come down to retest the 19700 major static support, a valid breakdown will confirm a major drop in the upcoming period.

Price is expected to retest the upper median line (UML) of the major ascending pitchfork and the median line (ml) of the minor ascending pitchfork, we have a strong confluence between these levels, we’ll see how will react when will hit this zone.

We’ll have a perfect buying opportunity if the support levels will hold and if will reject the price again, only a breakdown through the confluence area will accelerate the sell-off.

Support can be found also at the 38.2% retracement level and at the sliding line (SL), so only a valid breakdown below these levels will confirm a large drop.

The next upside target remains at the 130.76 previous high, could be attracted by the 150% Fibonacci line (ascending dotted line) as well.

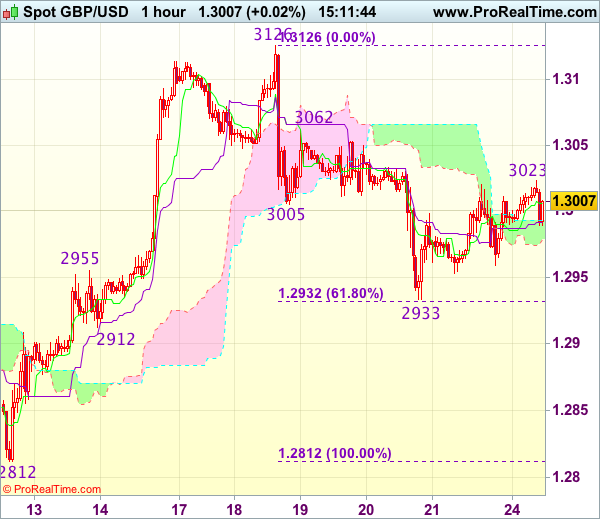

Trade Idea : GBP/USD – Sell at 1.3060

GBP/USD - 1.3010

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3006

Kijun-Sen level : 1.2991

Ichimoku cloud top : 1.2993

Ichimoku cloud bottom : 1.2979

Original strategy :

Sell at 1.3040, Target: 1.2940, Stop: 1.3075

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3060, Target: 1.2960, Stop: 1.3095

Position : -

Target : -

Stop : -

Cable found support at 1.2959 on Friday and has rebounded again, suggesting the recovery from 1.2933 may bring further gain to 1.3040, however, still reckon resistance at 1.3062 would limit upside and bring another decline later, below 1.2950-55 would signal the rebound from 1.2933 has ended, bring weakness to 1.2932-33 (61.8% Fibonacci retracement of 1.2812-1.3126 and said support), break there would extend the fall from 1.3126 top to previous support at 1.2912 but below latter level is needed to retain bearishness and bring subsequent selloff to 1.2880-85.

In view of this, we are looking to sell cable on recovery as resistance at 1.3062 should limit upside. A firm break above resistance at 1.3062 would abort and suggest the fall from 1.3127 has ended instead, bring a stronger rebound towards 1.3090-00 but resistance at 1.3126 should remain intact.

Further USD Weakening

On Friday, US equities were sold off, along with USD, with EURUSD reaching its highest level since January 2015. The markets were concerned to learn that there will be a further investigation into President Trumps' financial dealings that may cause his economic agenda to falter. Further adding to concerns around Trumps administration was the news that senior adviser Jared Kushner will be interviewed by the Senate Intelligence Committee on Monday and Donald Trump Jr., and former Trump campaign Chairman Paul Manafort, will go before Senate committees on Wednesday. USD has further been impacted by the recent downgraded forecast of US growth by the IMF from 2.3% to 2.1% for 2017.

EURUSD gained nearly 1.8% last week, with Friday being the 5th consecutive daily advance. On Friday, EURUSD reached a high of 1.16676 which has been breached in early Monday trading to reach a high of 1.16838. EURUSD is currently trading around 1.1670.

USDJPY touched a 4-week low on Friday of 111.064, a 0.7% drop on the day and JPY strengthening has continued with USDJPY reaching a low of 110.764 in early Monday trading. Currently, USDJPY is trading around 111.10.

GBP traded lower against EUR on Friday, close to an eight-month low and capping its worst week since October trading near to 0.8995. EURGBP is currently trading around 0.8967. GBP fared slightly better against USD on Friday and is currently trading around 1.3017, even with the IMF downgrading its growth forecast for the UK from 2% to 1.7% for 2017. GBPUSD is currently trading around 1.3015.

Gold rose 0.8% on Friday, benefitting from a weaker USD, to trade as high as $1,255.61. Currently Gold is little changed, trading around $1,255.

WTI suffered a loss of 2.4% on Friday, to trade as low as $45.55pb. However, on Sunday, OPEC's Secretary General Mohammad Barkindo stated “We are pretty sure that the rebalancing process may be going at a slower pace than earlier projected, but it is on course. It is bound to accelerate in the second half”. WTI is currently trading around $45.85pb.

At 8:00 BST, The Japanese Cabinet Office will release the Leading Economic Index for June. The index consists of 12 indexes such as account inventory ratios, machinery orders, stock prices and other leading economic indicators, which will give a gauge as to the economic conditions in Japan. If the data release is higher than the previous number of 104.7 it will be considered bullish for JPY, with a poorer number being bearish for JPY.

At 11:00 BST, EUR Market Services PMI Services is due to be released, with the market expecting 55.5, bettering the previous reading of 55.4. So, unless this release is significantly better or worse, the markets will expect EUR to remain unchanged.

At 16:45 BST, US Market Services PMI Services is due to be released, with the market expecting 54.3, bettering the previous reading of 54.2. So, unless this release is significantly better or worse, the markets will expect USD to remain unchanged.