Sample Category Title

Yen Pauses After Ending Week on High Note

USD/JPY has steadied on Monday, following strong losses in the Friday session. In the North American session, the pair is trading quietly at 112.70. On the release front, it's a very quiet start to the day. There are no Japanese events on the schedule. In the US, the sole indicator, the Empire State Manufacturing Index, softened to 9.8 points, much weaker than the forecast of 15.2 points. There are no major US or Japanese events on Tuesday.

It's a light week on the fundamentals front, but we could see some movement from the yen later in the week, as the BoJ meets for a policy meeting. The bank is expected to upgrade its economic growth forecasts in response to the stronger economy. Policymakers have hinted that it will push back its timeline for inflation reaching the 2% target, which currently does not seem a realistic goal, despite years of ultra-loose monetary policy. Will this happen at the July meeting? The markets may not get an answer until the rate statement is released, as the board members are split between those who expect inflation to rise due to the stronger economy, and those who don't think inflation levels will move upwards. If the pessimists prevail, the bank will delay the timing for hitting the 2 percent target from its current forecast of "around fiscal 2018" to a later date. The BoJ has consistently said that it will not reduce its radical stimulus program until inflation levels move closer to the bank's inflation target of 2 percent. However, investors will be looking for any tweaks to current monetary policy, which could trigger some movement from the yen.

The US labor remains close to capacity and the unemployment rate is sparkling, at just 4.4%. So why is inflation mired at low levels? Economists are puzzled, and the Federal Reserve is also at a loss, although Fed Chair Janet Yellen insists that it's only a matter of time before inflation moves higher. In testimony before a Senate committee last week, Yellen insisted that it was "premature to conclude that the underlying inflation trend is falling well short of 2 percent", and that with a strong labor market "the conditions are in place for inflation to move up". However, the markets remain skeptical that the Fed will make a move before the end of the year, with the odds of a December hike at just 43%, according to the CME Group.

Consumer inflation and spending numbers for June were released on Friday, and the data was weak. CPI edged up to 0.0%, short of the forecast of 0.1%. Retail Sales declined 0.2%, missing the estimate of 0.1%. This marked the third decline in the past four months. Consumer spending accounts for 2/3 of US economic activity, so it's no surprise that weak spending has also meant weak inflation, despite Yellen's claim that low inflation is a temporary phenomenon. The US economy had a weak first quarter, with growth of just 1.4%. If the second quarter follows suit, investors could sour on the US dollar in favor of other assets such as the Japanese yen.

Loonie Hits Fresh 14-month High; Dollar Steady after Friday Sell-off

There was limited price action today as investors remained sidelined ahead of three big events this week. Major currencies mostly traded in tight ranges during the European session, while in the absence of major economic releases, the market focus has been on the start of the second round of the Brexit negotiations, the European Central Bank and the Bank of Japan meetings on Thursday.

The greenback managed to slightly recoup against most majors following the sell-off on Friday amid the disappointing inflation and retail sales figures. The Empire State manufacturing index published today added to the negative US story. The New York Fed's barometer on current manufacturing conditions slid in July to 9.8 against expectations of 15.0 and far below the prior month's level of 19.8. The dollar fell slightly against the yen upon the release of the numbers, but managed to recover quickly after. Dollar/yen was last trading at 112.41.

Yearly inflation in the eurozone inched lower in June, the official Eurostat reading confirmed today. Annual consumer prices rose 1.3% in June, in line with expectations, but below the 1.4% gain in May. By contrast, core inflation, which strips out volatile components, rose 1.1% from 0.9% in the prior month. As a result of a slowdown in energy prices (on a monthly basis the prices were down 0.9%), inflation tempered in June from the prior months. However, annual inflation accelerated for the services sector to 1.6% from 1.3%. ECB policymakers are scheduled to discuss monetary policy and make decisions on interest rates and QE on Thursday. The euro was under soft pressure against the US dollar today. Euro/dollar fell to last trade at 1.1466 ahead of the US session.

The uncertainties surrounding the UK's exit from the EU have been putting pressure on sterling against the greenback as the second round of Brexit negotiations starts today. Pound/dollar was last trading at 1.3070.

In Canadian news, home resales fell 6.7% in June from May, the largest monthly drop since 2010. On the other hand, foreign investors increased purchases of Canadian securities in May to reach C$29.5 billion, three times the expected level. The loonie reversed losses against its US counterpart from the Asian session and gained during European trading. Dollar/loonie was last trading at 1.2628, hitting a fresh 14-month high.

Oil prices were gaining for most of the day, but came under pressure as the European session was about to end. The addition of fewer drilling rigs in the US supported earlier gains, however Brent fell below $49 a barrel to last trade at $48.87 while WTI was at $46.45 a barrel.

Following Friday's dollar sell-off, gold prices have been trending upwards. At $1,235.50 an ounce ahead of the European close, the precious metal has been trading above the $1,230 level for most of the day.

Economic Growth in China Holds Steady in Q2

Chinese real GDP growth modestly topped expectations in Q2. Amid an improving outlook for the global economy, Chinese economic growth and capital outflows have stabilized for the time being.

Chinese GDP Growth Steady in Q2

Data released today showed the Chinese economy growing 6.9 percent on a year-ago basis in Q2, topping expectations by 0.1 percentage point and matching the year-over-year pace from Q1 (top chart). Over the past few quarters, China's economy has very modestly accelerated; after three consecutive quarters of 6.7 percent year-over-year growth to start 2016, the year-ago pace ticked up to 6.8 percent to cap the year and has climbed another tick thus far in 2017.

Although a breakdown of GDP into its demand components is not yet available, sector level data indicate that growth was steady in the key sectors of the Chinese economy. Growth in the secondary industry, which includes mining/quarrying, manufacturing, construction and utilities production, held firm at 6.4 percent on a year-over-year, year-to-date basis. Growth in the tertiary industry, or the service sector, was also unchanged at 7.7 percent over this period. The primary sector, which includes agriculture, forestry and fishing, was the sole mover and shaker in Q2, accelerating to a 3.5 percent pace year-over-year, year-to-date.

Economic growth in China has stabilized alongside the brightening outlook for global trade. Indeed, growth in Chinese export volumes has improved from the weak pace seen over the past couple years (middle chart). Separate data released this morning showed Chinese industrial production topping expectations in June on both a year-over-year and year-to-date basis. Investment spending growth, which has accounted for much of the slowdown in the Chinese economy over the past few years, has also leveled out as Chinese policymakers try to thread the needle in challenging areas such as housing; on a year-ago basis, fixed investment spending growth has held steady at 8.6 percent for the past three months.

Although the prospects for the Chinese economy have improved of late, we do not expect a return to the supercharged rates of growth in the global economy experienced over the past couple expansions. As such, we look for a gradual, secular deceleration in the Chinese economy ahead.

Capital Outflows Halted, Gradually Stronger Yuan in the Outlook

Capital outflows plagued the Chinese economy for much of 2014-2016 amid fears about future growth in the world's second largest economy. FX reserves dipped below $3.0 trillion in January 2017 for the first time since 2011 as Chinese policymakers tried to staunch the bleeding. Midway through 2017, however, Chinese policymakers appear to have successfully righted the ship for the time being. Since that low reached in January, FX reserves have modestly increased in each successive month (bottom chart). Our currency strategy team sees a relatively steady renminbi in the near term, and moderate strength in the renminbi versus the U.S. dollar over the medium term amid a broadly softer outlook for the greenback.

Elliott Wave Analysis: AUDUSD Trading Higher

AUDUSD is making an intra-day rally away from 0.7802 level, where sub-wave iv of 3 had potentially ended. If that is the case, the final wave v of three is in motion, that can search for a top around the upper two channel lines. Once the lower channel line gets taken out, a new three wave reversal into black wave 4 can come in play.

AUDUSD, 1H

USD Struggles Not to Lose Further Ground

- European stock markets trade volatile near opening levels today with the German Dax (-0.35%) underperforming. Markets are mainly counting down to Thursday's ECB meeting. US stock markets opened nearly unchanged.

- Eurozone CPI rose 1.3% Y/Y in June (0.0% M/M), according to the final reading which came in line with an initial estimate. Inflation fell back from 1.4% in May having spiked at a three-year high of 1.9% in April. Details showed stronger services inflation was one of the reasons for a rise in core inflation to 1.1% in June (from 0.9% in May).

- A Bloomberg national poll shows that, in nearly every measure of his performance, Trump's presidency is not wearing well with the public. 55% view him unfavourably, up 12 points since December. The American people do however feel fairly optimistic about their jobs, the strength of the economy and their own fortunes.

- The New York Fed Empire manufacturing index disappointed with a reading of 9.8. in July (consensus of 15.0). A decline from the 19.8 in June was expected but the extent of the decline surprised markets. Indexes assessing the six-month outlook suggest that firms remain positive about the future, though less so than in June.

- Bankers with knowledge of the matter stated that Greece is looking, for the first time in three years, to sell five-year government bonds this week or next. This is remarkable given that Athens has received three bailouts in the past seven years and the debate over whether debt write-downs are needed continues as the IMF deems Greece's debt unsustainable and on an "explosive" path.

Rates

Countdown to ECB policy meeting

Global core bonds traded with a minor upward bias in an uneventful European trading session. European stock markets traded volatile, but couldn't influence the Bund's performance. EMU eco data (final CPI inflation) also failed to trigger a market reaction ahead of Thursday's ECB meeting. Many investors turn more cautious ahead of that meeting. Will Draghi downplay some of his hawkishly interpreted comments in Sintra or will he confirm them? The latter could spark unwanted market volatility as an official announcement on QE tapering is only expected in September.

Core bonds painted an intraday topping off pattern during US dealings despite a weaker-than-expected US Empire Manufacturing index. A JPM report arguing in favour of a Fed balance sheet announcement at the July 26 FOMC meeting might have played a role. We only expect such an announcement at the September meeting.

At the time of writing, the German yield curve drops up to 1.5 bps lower with the belly of the curve outperforming the wings. Changes in the US yield curve vary between -0.4 bps (2-yr) and -1.3 bps (10-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between -1 bp and +1 bp.

Currencies

USD struggles not to lose further ground

Trading in the major FX cross rates took a very slow start for the new week. EUR/USD settled close to the recent top, but there was no trigger to kick-start a real test. USD/JPY traded with a slightly negative bias intraday as did core bond yields. The pair trades in the 112.40 area.

Chinese data, including Q2 GDP printed stronger than expected this morning. The impact on regional equity sentiment was mixed given headlines that Chinese authorities considered more regulation and less easy financial conditions. USD/JPY stabilized in the 112.40/70 area after Friday's sell-off. AUD/USD held north of 0.78, maintaining last week's impressive gains. EUR/USD (1.1460/75 area) hovered near the recent top, but no test occurred.

There was absolutely no story to guide USD trading this morning. European equities failed to join the positive momentum from the US on Friday. EUR/USD and EUR/JPY fell prey to short-term profit taking as investors looked forward to Thursday's ECB meeting, but the move didn't go far. Dollar weakness still prevailed going into the open of the USD markets. EUR/USD reversed the earlier dip. USD/JPY struggled not the return below the 112.40/50 area. The EMU CPI was confirmed at 1.3% Y/Y but was largely ignored.

By default dollar softness persisted early in US dealings. The Empire manufacturing survey eased from 19.8 to 9.8 (15.0 was expected). The reaction of the dollar was again negligible. USD/JPY trades in the 112.40/50 area. EUR/USD is still going nowhere in the 1.1465/70 area. The dollar continues to trade weak, but there is still no strong enough trigger to push the pair beyond the 1.1489/1.15 resistance. Will this change before Thursday's ECB meeting?

Sterling rebound slows

Last week's sterling rally slowed this morning and the UK currency fell prey to a modest reversal. Last week, there was no high profile story behind the sterling comeback. This was also the case for today's setback. There were plenty of headlines on discord within the UK government going into the next round of negotiations with the EU. Market doubts the UK government's ability to execute a coherent Brexit-strategy which prevents further sterling gains. Cable dropped off this morning's top north of 1.31 and trades currently again in the 1.3070 area. EUR/GBP shows tentative signs of a bottoming out process. The pair is changing hands in the 0.8770 area. EUR/USD strength is also slowing last week's correction of EUR/GBP.

Japan 225 Index Records 10-day Low; Remains Bullish in the Medium-term

The Japan 225 index has declined in the three previous trading days. In today's trading, it recorded a ten-day low of 19,980. Despite this fall in recent days, the index has been in large part moving sideways over the last number of weeks.

The stochastics are pointing to negative momentum over the short-term. Specifically, the %K line is edging further down into bearish territory, while it crossed below the slow %D line.

If the index rises, the area around the middle Bollinger line - a 20-day moving average (MA) line - at 20,100 could pose a barrier to the upside. Notice that the index briefly rose above this level in today's trading before retreating back below it. Further above, the area around the upper Bollinger band at 20,261 could provide additional resistance.

On the downside, the current level of the 50-day MA and lower Bollinger band, ranging from 19,948 to 19,935, might offer support. Below this territory, the focus would shift to the area around the one-month low of 19,840 for additional support.

Regarding the medium-term, it currently looks bullish mostly due to the significant advancing since mid-April and up to the second half of June - the index hit a twenty-three-month high of 20,322 on June 20. The price is above the 50- and 200-day MAs at the moment, while the 200-day MA is steeply upward sloping.

Spot Gold Moved Higher on Monday

Spot Gold moved higher on Monday, extending last Friday's strong rally when yellow metal rallied, supported by weaker dollar, hit by weak US data.

Recovery rally from $1204 (10 July low) is riding on the third wave which commenced from $1214 (Friday's low) and eyes its 100% Fibonacci expansion at $1236, to validate wave principles.

Next strong barrier lies immediately above at $1239 (double Fibonacci resistance, 38.2% of entire $1296/$1204 descend and 61.8% of $1258/$1204 downleg) and sustained break here would trigger fresh extension of recovery after initial reversal signal was generated on Friday's rally above trendline resistance at $1223 (bear-trendline from $1296 peak).

Broken 200SMA offers immediate support at $1233, followed by $1229 (former highs of 5/6 July / top of thick 4-hr cloud) where dips should be ideally contained.

Res: 1236; 1239; 1242; 1244

Sup: 1233; 1229; 1225; 1220

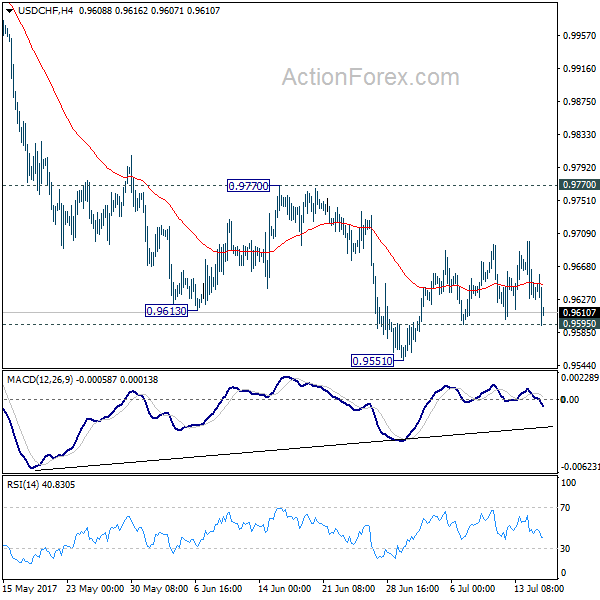

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9609; (P) 0.9654; (R1) 0.9680; More...

Intraday bias in USD/CHF remains neutral as consolidation from 0.9551 continues. In case of another rise, upside should be limited by 0.9770 resistance and bring fall resumption. Below 0.9595 minor support will turn bias to the downside. Break of 0.9551 will extend the whole fall from 1.0342 and target 0.9443 key support level next. At this point, we'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

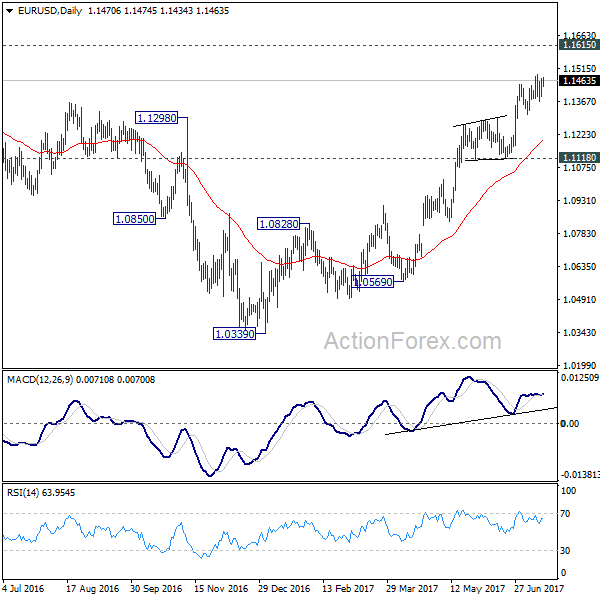

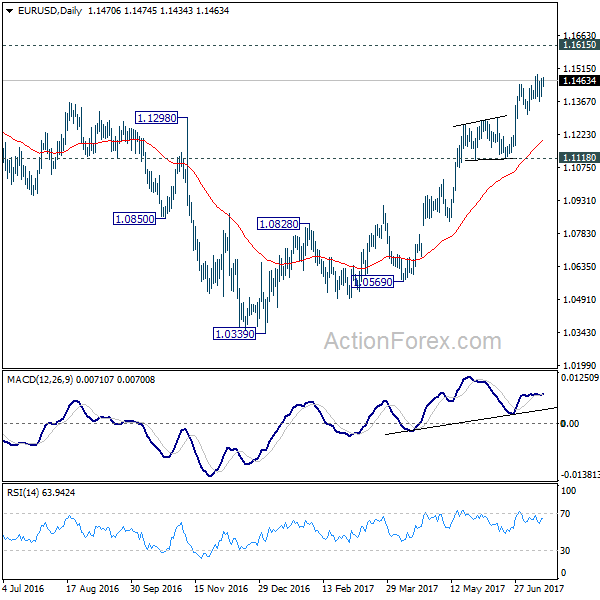

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1415; (P) 1.1443 (R1) 1.1495; More.....

Intraday bias in EUR/USD remains neutral for the moment as consolidation from 1.1489 might extend. Below 1.1312 will bring deeper fall to 55 day EMA (now at 1.1201). In that case, downside should be contained by 1.1118 support to bring rise resumption. On the upside, break of 1.1489 will extend recent rally from 1.0339 to 1.1615 key resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

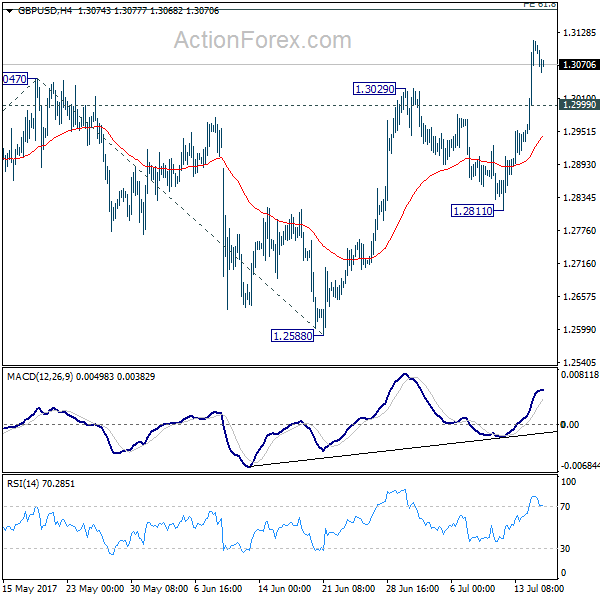

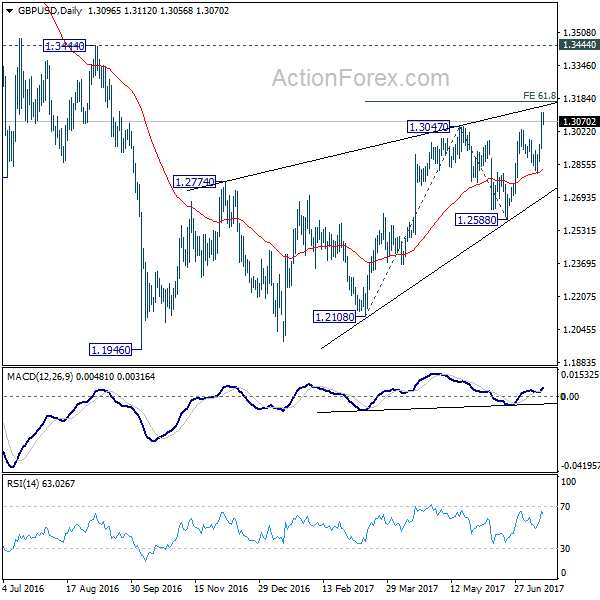

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2986; (P) 1.3049; (R1) 1.3165; More...

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. On the downside, below 1.2999 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.