Sample Category Title

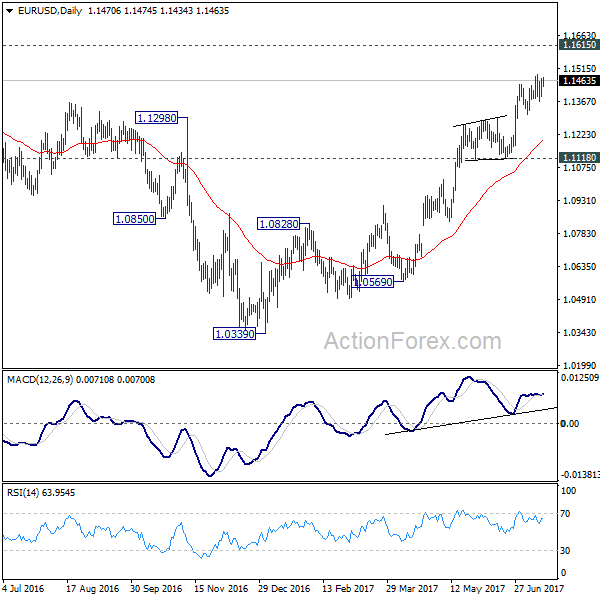

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1415; (P) 1.1443 (R1) 1.1495; More.....

Intraday bias in EUR/USD remains neutral for the moment as consolidation from 1.1489 might extend. Below 1.1312 will bring deeper fall to 55 day EMA (now at 1.1201). In that case, downside should be contained by 1.1118 support to bring rise resumption. On the upside, break of 1.1489 will extend recent rally from 1.0339 to 1.1615 key resistance next.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

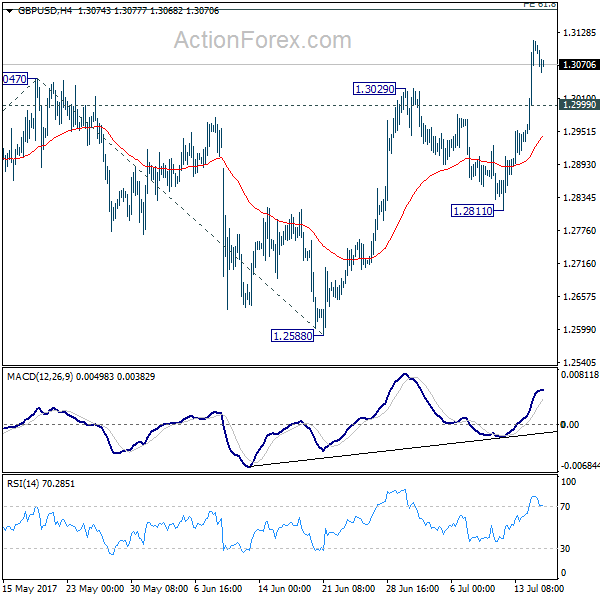

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2986; (P) 1.3049; (R1) 1.3165; More...

Intraday bias in GBP/USD remains on the upside for 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168. Overall, choppy rebound from 1.1946 is seen as a corrective pattern, hence, we'd be cautious on strong resistance from 1.3168 to limit upside. But firm break of 1.3168 will bring further rise towards 1.3444 key resistance. On the downside, below 1.2999 minor support will turn intraday bias neutral first.

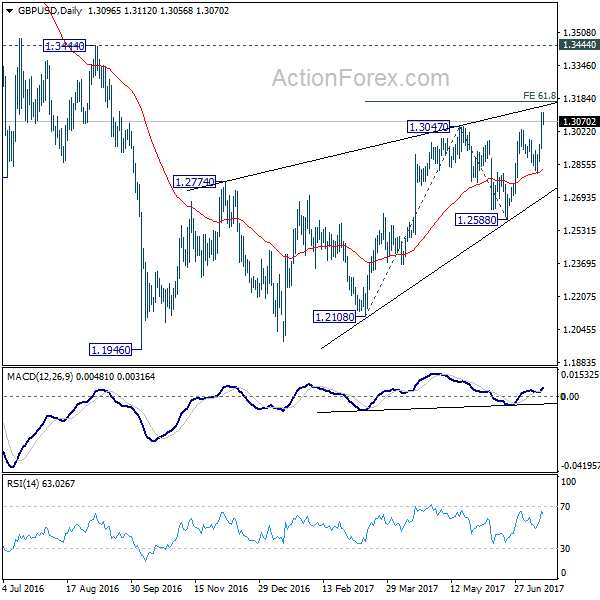

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

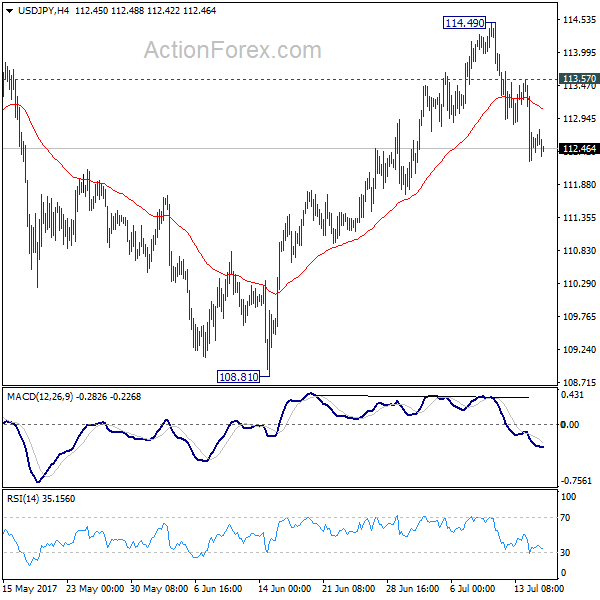

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.98; (P) 112.78; (R1) 113.30; More...

Intraday bias in USD//JPY remains on the downside for 55 day EMA (now at 112.03). The rejection from 114.36 resistance suggests that whole correction from 118.65 is possibly still in progress. Sustained break of 55 day EMA will pave the way to 108.12 and below. On the upside, above 113.57 minor resistance will turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Aussie Stands Tall after Chinese GDP Growth Surpasses Expectations

China, the world's second largest economy and a driver of the emerging markets, has overperformed in terms of growth in the second quarter of the year, proving relief to policymakers who are currently engaged in efforts to limit financial risks from soaring debt levels and a brewing property bubble. Following the statistics, the Australian dollar bounced higher, reaching a more than one-a year high.

According to the National Bureau of Statistics of China, the Chinese economy grew at 6.9% year-on-year in the second quarter, beating the target of 6.5% set by the government and surprising analysts who anticipated that GDP will expand by 6.8%. Quarter-on-quarter, GDP growth was in line with expectations at 1.7% but was higher than the 1.3% estimated in the previous quarter.

Part of the expansion was attributed to the manufacturing sector, where the industrial output rose by 7.6% in June year-on-year, restoring the two-year high level reached in March. The figure was far above the forecast of 6.5% which was set at May's reading.

Other data out of China involved fixed asset investments and retail sales. The former was above the forecast but remained stable at the previous level of 8.6%, while the latter increased by 11%, higher than the 10.6% anticipated and the rate of 10.7% observed in May.

Although the above numbers are evidence of a stabilizing and sustainable economic growth, concerns remain around the high-leveraged housing market, where prices are also rising rapidly. Based on OECD calculations, the debt of non-financial entrepreneurs in China was the highest among major economies at 170% of GDP in 2016. To cool the overheated property market, the People's Bank of China (PBOC) has recently decided to restrict liquidity by tightening monetary policy, following the Fed's rate hike in March. Particularly, the PBOC has mainly targeted the short-term rates, increasing the seven-day repo rate (repurchase agreement rate) to a two-year high of 3.18% in the beginning of May.

In the forex markets, the release of the data lifted the Australian dollar against its US counterpart. The aussie surged immediately by 0.73%, hitting a near 15-month high of $0.7833.

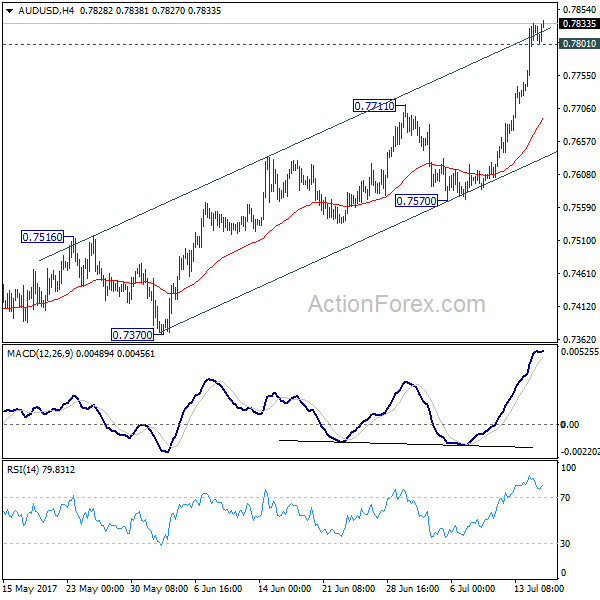

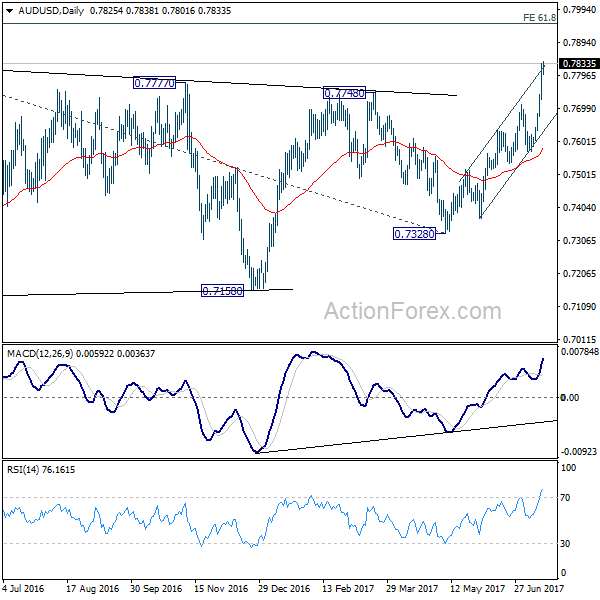

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7755; (P) 0.7794; (R1) 0.7864; More...

AUD/USD's rally is still in progress and edges higher to 0.7838. Intraday bias remains on the upside at this point. Firm break of 0.7833 resistance will confirm resumption of whole rebound from 0.6826 bottom. In such case, AUD/USD would target 61.8% projection of 0.6826 to 0.7833 from 0.7328 at 0.7950 next. On the downside, below 0.7801 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.7570 support holds.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Aussie Firmer as Markets Await RBA Minutes, Markets Rangebound Elsewhere

The forex markets remain generally range-bound except that Swiss is attempting for a recovery. Meanwhile Aussie is extending last week's rally ahead of RBA minutes. Gold rides on Dollar's weakness and is extending last week rebound to 1234.7 so far. On ther other hand WTI crude oil is losing momentum again as it's struggling around 55 day EMA. Economic data released today triggered little reactions. Empire State manufacturing in US dropped to 9.8 in July, down from 19.8, below expectation of 9.8. Canada international securities transactions came in at CAD 29.5, above expectation of CAD 9.78b. Eurozone CPI was confirmed at 1.3% yoy in June while core CPI was unrevised at 1.1% yoy. Trading could remain subdued in US session. But events in upcoming Asian session from Australia and New Zealand might trigger some volatility.

RBA minutes, New Zealand CPI to be released

Minutes of RBA July meeting will be a main focus in the upcoming Asian session. The central bank disaapointed the markets at the meeting by not turning hawkish like other major central banks. Aussie tumbled sharply but the weakness was very brief. Instead Aussie jumped last week on strong iron ore prices as well as dovish Fed messages. The upbeat Chinese dataflow should also give Aussie a boost as China is the world's biggest consumer of iron ore and the largest importer of Australia's iron ores. The strength in the exchange rate could now give RBA some headache. The central bank repeatedly noted that "appreciating exchange rate would complicate" the economic transition from the mining investment boom

New Zealand CPI will be another main focus. CPI is expected to rise a mere 0.2% qoq in Q2, dragging down annual rate from 2.2% yoy to 1.9% yoy. Just when inflation hit the higest level in five years in Q1, there were expectation that RBNZ could turn hawkish. But the central bank disappointed by maintaining that policy would stay accommodative for a "considerable period" of time. The slowdown in inflation would affirm RBNZ's neutral stance.

AUD/NZD's strong rebound last week indcaites that fall from 1.1017 has compelted with a head and shoudler bottom pattern. Further rise could now be seen back to 1.1017 resistance. But after all, larger outlook is neutral as the cross is staying in side range of 1.0234/1.1017. Below 1.0493 minor support will extend the fall from 1.1017 to 1.0234 key supprot.

China GDP grew 6.9% in Q2.

Released from China, GDP expanded 6.9% yoy in Q2, same pace as the prior quarter but above consensus of 6.8%. Economic activities in June continued to improve. Industrial production growth accelerated to 7.6% yoy in June, beating consensus of and May's 6.5%. Retail sales expanded 11% yoy in June, up from 10.7% a month ago. The market had anticipated mild deceleration to 10.6%. Fixed asset investment in urban areas grew 8.6% yoy in the first half of the year, same pace as in the first five months of the year. The government acknowledged that the country's economy continued to improve. It appears that the country's growth is on track to meet the government target of "around 6.5%".

In his first address at the National Financial Work Conference, which is held once every five years, over the weekend, Chinese President Xi Jinping affirmed that the PBOC would play a stronger role in defending against risks, calling for more work on safeguarding the financial system and modernizing its regulatory framework. Interestingly, the word "risk" appeared 31 times in the meeting note, followed by "regulation", which appeared 28 times, signaling that implementation of "regulations" to prevent financial system "risks" is the key direction of the government's policy.

More in China Watch - 2017 Growth Target On Track, Xi Commands To Prevent Risks And Tighten Regulations

Brexit negotiation round 2

The second round of Brexit negotiation starts today in Brussels. UK Brexit Secretary David Davis said ahead of the week long meeting that "we made a good start last month, and this week we'll be getting into the real substance." He noted that "protecting the rights of all our citizens is the priority for me going into this round and I'm clear that it's something we must make real progress on." EU's chief negotiator Michel Barnier said that "we will now delve into the heart of the matter. We need to examine and compare our respective positions in order to make good progress."

There will be working groups focusing on three areas, including citizen's rights, the divorce bill and other loose ends. Another group will focus on the border of Ireland. Three more weeks of talks will be held till early October. By that time, Barnier would hope to show "significant" progress to EU leaders to approve moving the negotiations to trade agreements.

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7755; (P) 0.7794; (R1) 0.7864; More...

AUD/USD's rally is still in progress and edges higher to 0.7838. Intraday bias remains on the upside at this point. Firm break of 0.7833 resistance will confirm resumption of whole rebound from 0.6826 bottom. In such case, AUD/USD would target 61.8% projection of 0.6826 to 0.7833 from 0.7328 at 0.7950 next. On the downside, below 0.7801 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.7570 support holds.

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we'll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Jul | 0.10% | -0.40% | ||

| 02:00 | CNY | Retail Sales Y/Y Jun | 11.00% | 10.60% | 10.70% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Jun | 8.60% | 8.50% | 8.60% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 7.60% | 6.50% | 6.50% | |

| 02:00 | CNY | GDP Y/Y Q2 | 6.90% | 6.80% | 6.90% | |

| 09:00 | EUR | Eurozone CPI M/M Jun | 0.00% | 0.00% | -0.10% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 1.30% | 1.30% | 1.40% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y Jun F | 1.10% | 1.10% | 1.10% | |

| 12:30 | CAD | International Securities Transactions (CAD) May | 29.5B | 9.78B | 10.60B | |

| 12:30 | USD | Empire State Manufacturing Jul | 9.8 | 15 | 19.8 |

CAC Ticks Higher as Eurozone Inflation Matches Forecast

The CAC index has recorded small gains to start off the week. Currently, the index is currently trading at 5240.50 and is up 0.15% on the day. In economic news, it's a quiet day. On the release front, Eurozone Final CPI edged down to 1.3%, matching the forecast. On Tuesday, the eurozone releases ZEW Economic Sentiment, with the markets expecting a strong reading of 37.2 points.

After a break for Bastille Day on July 14, French markets are back in action. President Emmanuel Macron hosted US president Donald Trump during the holiday. Macron is eager to make France an important player on the global stage, and is taking advantage of political and economic developments. Given that Trump and German chancellor Angela Merkel have a frosty relationship, Macron could serve as a go-between, as he has good relations with both Trump and Merkel. As well, France is eyeing Brexit as a golden opportunity to expand its financial sector and attract lucrative financial sector jobs which are leaving London. Many European companies will be downsizing their London operations, and the French are actively courting companies to consider moving to Paris. The first full round of Brexit talks began on Monday in Brussels, with the sides having agreed to first discuss the rights of EU citizens in the UK and Britain's bill for leaving the EU, before talks on a new trade agreement begin. With significant gaps between the parties on both of these issues, the negotiations promise to be difficult.

Although the eurozone economy has shown improvement in 2017, inflation remains at low levels. Eurozone Final CPI edged down from 1.4% to 1.3% in June, marking its weakest gain in 2017. Germany may be the catalyst of the eurozone's economic recovery, but the bloc's largest economy has not been immune to low inflation. Final CPI improved to 0.2% in June, compared to -0.2% in May. The ECB has set an inflation target of 2%, but German and eurozone inflation numbers remain well below that threshold. The ECB has acknowledged that economic conditions have improved, but insists that it has no plans to taper its ultra-loose monetary policy unless inflation levels move higher. The current asset-purchase plan is scheduled to wind up in December, and we're unlikely to see any changes in monetary policy unless inflation moves considerably higher in the second half of the year.

With the US labor market close to capacity and the unemployment rate at just 4.4%, economists are puzzled why this hasn't pushed inflation to higher levels. The Federal Reserve is also at a loss to explain the lack of inflation, but Fed Chair Janet Yellen insists that it's only a matter of time before inflation moves higher. In testimony before a Senate committee last week, Yellen insisted that it was "premature to conclude that the underlying inflation trend is falling well short of 2 percent", and that with a strong labor market "the conditions are in place for inflation to move up". However, the markets remain skeptical that the Fed will make a move before the end of the year, with the odds of a December hike at just 43%, according to the CME Group.

GBP/USD Breakout Needs Confirmation, USD/CHF Turned to the Downside Again, EUR/JPY Eyeing a Crucial Breakdown

GBP/USD Breakout Needs Confirmation

The GBP/USD is trading in the red right now after the failure to resume the upside momentum, a minor decrease is natural after the impressive rally. Failed to climb above the 1.3112 Friday's high, the bears have stepped in and have taken the lead on the short term. Remains to see how long this will be, could come down only to test and retest the broken resistance before will resume the upside movement.

The perspective remains bullish on the Daily chart, personally I'm waiting for a fresh trading signal, that could come in the upcoming days if the broken resistance will hold.

We have a poor economic calendar today, the rate is driven by the technical factors, so the minor decrease is understandable. The US is to release only the Empire State Manufacturing Index, which could decrease from 19.8 to 15.2 points in July.

Price drops after the failure to reach and retest the upside line of the ascending channel, is pressuring the 150% Fibonacci line (ascending dotted line), could come down to test and retest the broken upper median line (UML) of the major descending pitchfork.

Is also approaching the 1.3000 psychological level, we may have a buying opportunity if will stay above the upper median line (UML) and above the first warning line (wl1) of the minor ascending pitchfork.

Personally, I'm still waiting for a confirmation that will increase further, you can see that we had another false breakout above the UML in the past. The sentiment will change drastically on the GBP/USD if the rate will stabilize above the UML, a major rebound will come if this scenario will happen.

Is very important to see what will happen on the USDX these days because is under massive selling pressure on the short term and could approach the 95.00 psychological level in the upcoming days.

USD/CHF Turned to the Downside Again

The currency pair has dropped aggressively since Friday and is targeting new lows on the Daily chart, is strongly bearish as the USDX stay in the seller's territory. Technically should drop further after a false breakout.

USD/CHF goes down after the false breakout above the 50% Fibonacci line (descending dotted line), also failed to stay above the 0.9634 static resistance and now looks determined to approach the 0.9551 previous low.

Support could be found at the lower median line of the descending pitchfork and at the lower median line (lml) of the minor ascending pitchfork, a breakdown below these levels will send the rate towards the second warning line (WL2) of the major ascending pitchfork.

EUR/JPY Eyeing a Crucial Breakdown

EUR/JPY is into a corrective phase on the Daily chart, this is natural after the amazing rally, has come back to test and retest the upper median line (UML) on the major ascending pitchfork, the median line (ml) of the minor ascending pitchfork and the 38.2% retracement level, a valid breakdown below these levels will open the door for more declines. However, we'll have a buying opportunity if will climb above the 129.30 level again.

Chinese GDP Data Overwhelm Investors | Currency Markets Remain A Major Focal Area

- Dollar Doldrums

- ECB May Hold Fire

- New Opening For Pound

Investors over in Europe are sanguine after a more inspiring Chinese GDP reading. The Q2 GDP data came in at 6.9% ahead of the forecast of 6.58%. China is the second biggest economy of the world and the chief concerns were that we may be heading towards more than a soft landing but the recent economic readings have eased off those fears.

Dollar Doldrums

This week is primarily about the currency market. Firstly, investors are going to pick up the momentum where they left off when it comes to the dollar. Factors such as underwhelming US economic data, cautious testimony by the Fed Chairwomen, Janet Yellen and meagre inflation got the dollar bulls worried. We do think that the mighty dollar may be well oversold here and this is due to the fact that traders are questioning the Fed's ability to increase the interest rate one more time this year. They do expect the Fed to reduce the size of their balance sheet rather than to increase the interest rate this year and for many, that has become more significant. Scaling down the size of the balance sheet would make the dollar stronger and we do think that the market is not pricing this at all.

ECB May Hold Fire

The second most vital affair for the markets is the upcoming ECB meeting on Thursday. The speculations are high on both sides of the argument. Some say that the ECB will use this meeting to quench the fire about any rumours that the ECB is going to reduce its monetary stimulus. While the other side is making their argument that it is about time to scale back from the ultra-loose monetary policy. The president of the European central bank would have another opportunity if he thinks that he is not going to utilise this meeting to set the tone for reducing the size of its monetary policy before the next meeting. The central banker's symposium could be just the place where the ECB president lays out his agenda for tapering. A number of various members of the ECB committee do concur with the view that there may be no need for the ECB to keep its patient in the hospital given the recovery we have experienced. Therefore, Draghi may not feel that much pressure to set the foundation for tapering during the upcoming meeting but the market would certainly take its own interpretation

New Opening For Pound

As for the British pound, we broke a major level of 1.31 last week and closed above the 1.30 mark confirming that we are going to start a new trend in a new territory which we have not seen for a while. The inflation data that is due this week remains an important focal point for the economy, and Mark Carney would also add his own colours. If the inflation data confirms further improvement, the bank would find it more difficult to defend its current monetary policy.

DAX Ticks Lower As Eurozone Inflation Edges Lower

The DAX index has started the week with slight losses. In Monday's European session, the DAX is trading at 12,611.50, down 0.18%. On the release front, Eurozone Final CPI edged down to 1.3%, matching the forecast. On Tuesday, Germany and the eurozone release ZEW Economic Sentiment.

One of the key stocks on the DAX, Deutsche Bank, is under pressure, and dropped 0.91% on Friday. Germany's largest bank started off the Monday session with losses as well, after the ECB said it was considering implementing ownership-control procedures against the bank's two largest shareholders, Qatar's royal family and HNA, a Chinese conglomerate. The aim of the review is to ensure that an investor is financially stable and untainted by money-laundering or other crimes. If either shareholder fails the test, Deutsche Bank shares would likely fall.

Eurozone inflation levels have been softening in the second quarter. Eurozone Final CPI edged down from 1.4% to 1.3% in June, marking its weakest gain in 2017. Germany may be the catalyst of the eurozone's economic recovery, but the bloc's largest economy has not been immune to low inflation. Final CPI improved to 0.2% in June, compared to -0.2% in May. The ECB has set an inflation target of 2%, but German and eurozone inflation numbers remain well below that threshold. The ECB has acknowledged that economic conditions have improved, but insists that it has no plans to taper its ultra-loose monetary policy unless inflation levels move higher. The current asset-purchase plan is scheduled to wind up in December, and we're unlikely to see any changes in monetary policy unless inflation moves considerably higher in the second half of the year.

With the US labor market close to capacity and the unemployment rate at just 4.4%, economists are puzzled why this hasn't pushed inflation to higher levels. The Federal Reserve is also at a loss to explain the lack of inflation, but Fed Chair Janet Yellen insists that it's only a matter of time before inflation moves higher. In testimony before a Senate committee last week, Yellen insisted that it was “premature to conclude that the underlying inflation trend is falling well short of 2 percent”, and that with a strong labor market “the conditions are in place for inflation to move up”. However, the markets remain skeptical that the Fed will make a move before the end of the year, with the odds of a December hike at just 43%, according to the CME Group.

Fed policymakers weren't smiling after Friday's consumer inflation and spending numbers. CPI edged up to 0.0%, short of the forecast of 0.1%. There was no relief from Retail Sales, which declined 0.2%, missing the estimate of 0.1%. This marked the third decline in the past four months. Consumer spending accounts for 2/3 of US economic activity, so it's no surprise that weak spending has also meant weak inflation, despite Yellen's claim that low inflation is a temporary phenomenon. The economy had a weak first quarter, with growth of just 1.4%. If the second quarter follows suit, investors could sour on the US dollar in favor of other assets, and the euro could take advantage.