Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.92; (P) 113.22; (R1) 113.58; More...

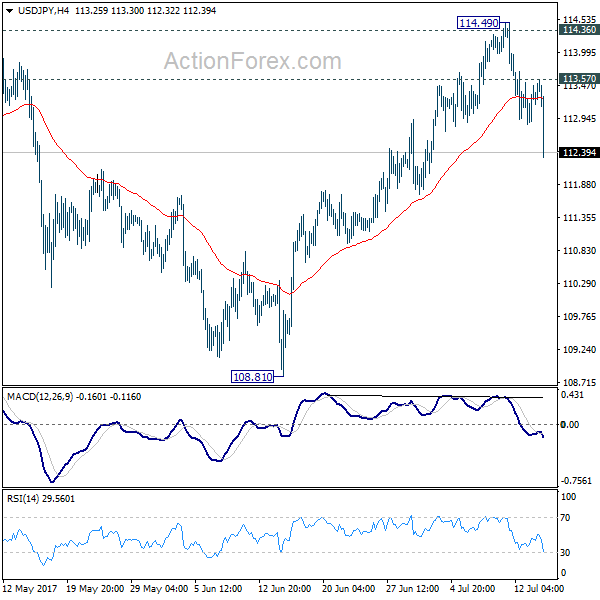

USD/JPY's decline resumes in early US session and reaches as low as 112.44 so far. The break of 112.88 support indicates rejection from 114.36 resistance. And, rise from 108.81 should be completed at 114.49. More importantly, the corrective pattern from 118.65 is likely still in progress. Intraday bias is now back on the downside for 55 day EMA (now at 111.98). Firm break there will target 108.12 low and below. Above 113.57 minor resistance will turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Dollar Selloff Extends after Weak CPI and Retail Sales

Dollar's decline accelerates in early US session after weak economic data. Headline CPI slowed to 1.6% yoy in June, down from 1.9% yoy and below expectation of of 1.7% yoy. Core CPI was unchanged at 1.7% yoy, in line with consensus. Meanwhile, headline retail sales dropped -0.2% in June, below expectation of 0.2%. Ex-auto sales dropped -0.2%, also missed expectation of 0.2%.

Technically, USD/JPY finally takes out 112.88 support firmly, which indicates near term reversal. The pair could now be heading back to 108.81. GBP/USD breaches 1.3 handle and this week's rebound extends. Focus will now be on 1.3029 resistance. USD/CAD took a break after BoC inspired decline but is now gathering momentum again.

Euro is the relatively weaker currency this week as markets are reassessing ECB policy path. Reuters quoted unnamed sources saying that ECB could indicate in the future that there is no fixed end to its asset purchase program. One source said regarding stimulus exit is that "the important thing is not to pre-commit and keep it very gradual." Another source said that "it's got to be data-dependent and we need to preserve the flexibility."

Meanwhile, according to a Reuters of economists, 47% of respondents expect ECB to announce tapering in September meeting. 25% expect ECB to extend QE at a reduced pace. 18% expects the decision to be made in October instead.

Released earlier today, Eurozone trade surplus widened to EUR 19.7b in May. New Zealand business manufacturing index dropped to 56.2 in June.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.92; (P) 113.22; (R1) 113.58; More...

USD/JPY's decline resumes in early US session and reaches as low as 112.44 so far. The break of 112.88 support indicates rejection from 114.36 resistance. And, rise from 108.81 should be completed at 114.49. More importantly, the corrective pattern from 118.65 is likely still in progress. Intraday bias is now back on the downside for 55 day EMA (now at 111.98). Firm break there will target 108.12 low and below. Above 113.57 minor resistance will turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business Manufacturing Index Jun | 56.2 | 58.5 | 58.2 | |

| 04:30 | JPY | Industrial Production M/M May F | -3.60% | -3.30% | -3.30% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 19.7B | 20.3B | 19.6B | 18.6B |

| 12:30 | USD | CPI M/M Jun | 0.00% | 0.10% | -0.10% | |

| 12:30 | USD | CPI Y/Y Jun | 1.60% | 1.70% | 1.90% | |

| 12:30 | USD | CPI Core M/M Jun | 0.10% | 0.20% | 0.10% | |

| 12:30 | USD | CPI Core Y/Y Jun | 1.70% | 1.70% | 1.70% | |

| 12:30 | USD | Advance Retail Sales Jun | -0.20% | 0.20% | -0.30% | -0.10% |

| 12:30 | USD | Retail Sales Less Autos Jun | -0.20% | 0.20% | -0.30% | |

| 13:15 | USD | Industrial Production Jun | 0.30% | 0.00% | ||

| 13:15 | USD | Capacity Utilization Jun | 76.80% | 76.60% | ||

| 14:00 | USD | U. of Michigan Confidence Jul P | 95 | 95.1 | ||

| 14:00 | USD | Business Inventories May | 0.30% | -0.20% |

USD/CAD Posted Humble Gains, USD/CHF Breakout Needs Confirmation, AUD/USD Seems Unstoppable

USD/CAD Posted Humble Gains

The Loonie has lost little ground versus the greenback in the morning, the minor increase was somehow expected after the amazing drop. Has found temporary and now is struggling to recover, but is still under immense selling pressure.

Right now we don't have a reversal sign, but we may have one in the upcoming days if the United States economic data will come in line with expectations or better. USD/CAD is trading right above two important support level and above the 1.2700 psychological level.

Is trading near 1.2730 level, but is losing altitude again after the morning increase, we'll see what will happen in the upcoming hours because the US is to release high impact data. The fundamental factors will take the lead, so you should be careful because we may have a high volatility.

The US CPI could increase by 0.1% in June and could jump in the positive territory after the 0.1% drop in May, while the Core CPI may increase by 0.2% in the previous month and could beat the 0.1% in the former reading period. Moreover, the greenback could receive support also from the Retail Sales, which could increase by 0.1%, the indicator dropped by 0.3% in the previous reading period, the Core Retail Sales are expected to increase by 0.2% and could boost the greenback, which could dominate the currency market on the short term.

The Capacity Utilization Rate and the Industrial Production will be released as well later, you should keep and eye on the economic calendar because the high impact data could shake the markets. A disappointment will send the USD tumbling, so maybe will be better to stay away during the data release.

USD/CHF Breakout Needs Confirmation

The USD/CHF managed to jump above a dynamic resistance, even if the USDX is trading in the red right now. USDX moves in range, but remains to see if this will be an accumulation or a distribution movement.

Has resumed the minor rebound, but the breakout needs confirmation, the next upside targets are at the median line (ml) of the minor ascending pitchfork and higher at the median line (ML) of the descending pitchfork. Right now we don't have a any trading opportunity, we'll have a buying opportunity only if the rate will come back down to retest the lower median line (lml) of the minor ascending pitchfork.

AUD/USD Seems Unstoppable

AUD/USD extends the latest gains and climbed above a major static resistance, remains to see if this will be a valid one because the US numbers could force the rate to decrease in the upcoming hours. Price is strongly bullish and looks determined to hit fresh new highs. Technically should increase further, but a USDX's rally will help the sellers to take the lead again.

Is trading above the 0.7755 major static resistance, but is premature to say that will have a valid breakout. I've drawn an up sloping red line where he could find resistance again. A failure to climb above the red line will signal an exhaustion and a reversal on the short term.

US Inflation And Consumer Numbers Eyed

It's been a sluggish start to trading on Friday as traders await inflation and consumer spending numbers from the US that could add a further dovish layer to Janet Yellen's comments on Wednesday.

It's become very clear in recent weeks that an increasing number of Federal Reserve policy makers are becoming concerned about persistent subdued inflation despite evidence suggesting that the labour market is tightening, typically a trigger for stronger wage growth and higher prices. Fed Chair Yellen highlighted this herself to the Senate Banking Committee on Wednesday, an admission that weighed on US Treasury yields and the greenback while supporting stocks in the process.

We don't have the plethora of policy makers making appearances today, with only Robert Kaplan scheduled to appear, but the US data that is due should fill that void quite nicely. Given Yellen, and many others', comments in recent weeks, the CPI data will clearly attract a lot of attention, even if it isn't the Fed's preferred measure of inflation. The core PCE price index – the preferred report – typically comes a few weeks after the CPI and while the numbers tend to differ a little, the direction of travel is generally similar so the latter does offer value.

While headline CPI is expected to fall to 1.7% in June, from 1.9% in May, core CPI is seen unchanged also at 1.7%. This isn't going to put policy makers fears at ease at all, particularly given that PCE is lower again. Should we see a larger decline then the yields and the dollar could be prone to slipping again, with the probability of another rate hike this year likely taking another hit, despite only sitting marginally above 50% currently.

The retail sales release, coming at the same time, is also a huge number given the importance of the consumer to the US economy. Markets could therefore become very volatile prior to the open, particularly if both numbers disappoint. We'll also get earnings from JP Morgan, Wells Fargo and Citigroup today which could make it quite a lively end to the week.

A Cautious Fed Sends Equities To Record Highs, Dollar dips

Friday July 14: five things the markets are talking about

Today's U.S consumer inflation is forecast to have rallied only +1.7% y/y last month. On a month-on-month basis, the core-CPI is expected to rise +0.2% after a +0.1% increase the previous month. Expect the data (08:30 am EDT) to be highly scrutinized, especially since Fed Chief Yellen this week indicated that it's premature to conclude that the underlying trend of prices is falling short of the Fed's +2% target.

The 'big' dollar continues to remain under pressure in the wake of dovish comments this week from U.S. policy makers, while U.S equities record fresh highs as Ms. Yellen reiterated yesterday her intention to Congress to tighten only gradually. Her 'less hawkish' comments also have U.S treasury prices climbing.

Also today, the market will also get a better understanding on how variable data during Q2 translated into corporate earnings when a number of Tier 1 financials stateside (JP Morgan and Citi) report their results.

U.S retail sales (08:30 am EDT) and industrial production figures (09:15 am EDT) are also due this morning.

1. Stocks print new highs

Overnight, Asian equity markets again traded with a positive tone, in line with what was seen with U.S bourses. Nevertheless, trading remains somewhat cautious ahead of this morning's U.S data.

In Japan, the Nikkei share average edged a tad higher (+0.1%) overnight as disappointing earnings from the world's third largest apparel retailer, offset gains made after Wall Street pushed higher. The broader Topix added +0.4%, for a +1.1% rise for the week.

Note: Markets in Japan will be closed for a holiday on Monday.

In Hong Kong, stocks rallied for the fifth consecutive session, their best weekly gain in a year, as last week's correction attracted more bargain hunting from China. The Hang Seng index rose +0.2%, while the China Enterprises Index gained +0.5%.

In China, equities ended mixed for the week, with the blue-chip index closing at a 19-month high, while start-ups had their worst week in 12-months. The blue-chip CSI300 index rose +0.4%, while the Shanghai Composite Index added +0.1%.

In Europe, stocks have opened a tad higher. Flat oil and commodity prices are having little impetus for materials and energy stocks on the FTSE 100. Markets will take their cues from today's U.S data.

U.S stocks are set to open little changed.

Indices: Stoxx50 flat at 3,527, FTSE -0.3% at 7,388, DAX -0.1% at 12,637, CAC-40 -0.1% at 5,240, IBEX-35 +0.2% at 10,677, FTSE MIB flat at 21.531, SMI %+0.2 at 9.026, S&P futures -0.1%

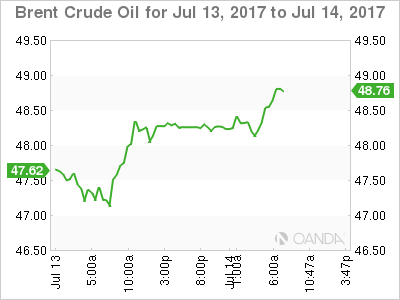

2. Oil edges lower on high fuel inventories, industry adeptness

Oil prices have edged lower overnight amid high fuel inventories, but remain on track for a solid weekly gain.

Brent crude futures are down -19c, or -0.4%, at +$48.23 per barrel. Week-to-date it's up +3.5%. U.S West Texas Intermediate (WTI) crude futures are at +$45.93 per barrel, down -15c but heading for a +3.8% gain over the week.

The IEA this week warned that a long-awaited market rebalancing could be delayed due to weak compliance with production cuts among OPEC members.

In its monthly report the IEA issued a stronger outlook for global oil demand, however, with consumption in Germany and the United States increasing in recent months.

But, the report also noted a dramatic recovery in oil production from Libya and Nigeria and a lower rate of compliance by OPEC with its own output agreement.

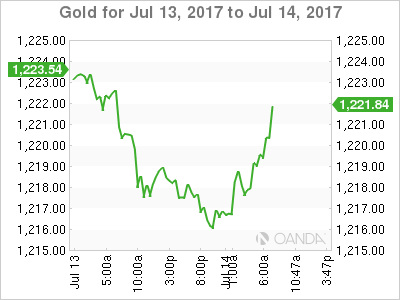

Gold prices (+0.1% to +$1,218.99 an ounce) are holding steady ahead of the U.S open, as the Fed seems set to only gradually tighten monetary policy, curbing speculation that interest rates would rise more than once this year.

3. Sovereign yields fall on Yellen's comments

The recent caution from the Fed has managed to take the sting out of a sell-off in the bond market, which had been gathering steam over the past few weeks on rising expectations that the ECB is set to wind down its asset purchase program.

Fed fund futures are now only pricing a 50-50 chance of a rise by December.

Yellen's 'less hawkish' comments this week has seen U.S Treasuries rally in reaction, clawing back a third of their selloff with yields on two-year notes falling to three-week lows, while U.S 10's is down another -1 bps overnight at +2.32%.

In Europe, Germany's benchmark 10-year Bund yield is flat, trading atop of its psychological +0.5% and has now given back a quarter of the rise (+0.585%) triggered by last month's hint from ECB's Draghi that it was readying to scale back stimulus.

Today's U.S CPI and retail sales data will be key for fixed income traders in shaping their curves.

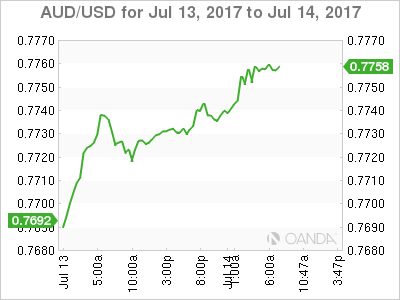

4. Dollar losing support

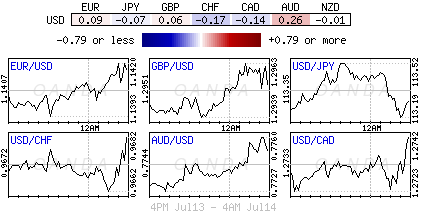

The signal from the Fed this week has managed to drive the 'mighty' buck to fresh nine-month lows against G10 pairs.

The latest comments from Yellen and others suggest that interest rates will rise very gently, and that is supportive for high-yielding currencies or 'carry' trades. The AUD has rallied +0.3% to a nine-month peak of A$0.7760 and the NZD little changed at NZ$0.7320.

Naturally, the yen (¥113.24) is underperforming against higher yielding currencies.

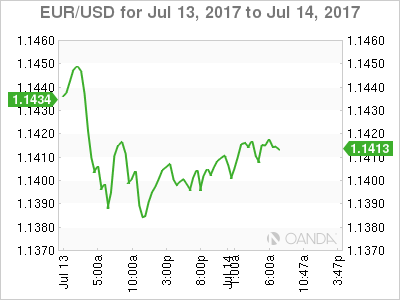

Currently, the EUR trades little changed at €1.1415, while sterling is up +0.1% at £1.2963 and the loonie is holding steady at C$1.2738 after gaining +1.5% outright after the Bank of Canada (BoC) rate hike Wednesday.

Note: There has been a lot of interest from Europe to own CAD on the crosses, especially against EUR (€1.4546).

5. ECB in preparation phase for tapering

Next week will be a big week for the ECB.

To date, the ECB has been focusing on preparing the markets for a tapering decision – they begun the process by tightening its communication at its June meeting.

The market believes President Draghi will take the next step at the upcoming meeting on July 20. But given the very sensitive market reaction, the ECB is expected to communicate their plans 'very' carefully.

Expect Euro policy makers to stress the recent better economic data to justify the policy switch, and to indicate that they would reassess its policy stance in early September, based on new staff macro forecasts.

DAX Unchanged Ahead Of US Retail Sales, Inflation

The DAX index is almost unchanged in the Friday session. Currently, the DAX is at 12,637.00, down 0.07%. In economic news, the eurozone trade surplus edged up to EUR 19.7 billion, falling short of EUR 20.3 billion. The US will release CPI and retail sales, with both indicators expected to post a weak gain of 0.1%.

A robust German economy has spurred the eurozone's recovery this year, but Germany is also grappling with persistently weak inflation levels. German Final CPI, a key gauge of consumer spending, improved to 0.2% in June, compared to -0.2% in May. Final CPI remains soft, managing just one reading above 0.2% in 2017. Earlier in the week, the wholesale price index came in at a flat 0.0%, rebounding from a decline of 0.7% a month earlier. The ECB has set an inflation target of 2%, but German and eurozone inflation numbers remain well below that threshold. The ECB has acknowledged that economic conditions have improved, but insists that it has no plans to taper its ultra-loose monetary policy unless inflation levels move higher. The current asset-purchase plan is scheduled to wind up in December, and we're unlikely to see any changes in monetary policy unless inflation moves considerably higher in the second half of the year.

The US economy has slowed in 2017, with GDP in the first quarter of 1.4%. Despite a labor market that remains close to capacity, consumer spending has not kept up. Wage growth remains weak, and inflation levels are well below the Fed's target of 2 percent. Later on Friday, the markets will get a look at consumer spending and inflation indicators. The markets are expecting weak gains, which could disappoint investors and hurt the US dollar.

Janet Yellen testified twice on Capitol Hill this week, but her comments didn't contain anything new, and the markets didn't show much reaction to her cautious message. Yellen reiterated that the Fed planned to raise rates “gradually”, and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair didn't provide any timelines, but the most likely timelines are September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and may not need another rate hike. In her testimony before a congressional committee, Yellen reiterated said that she believes the factors weighing on inflation are temporary. However, she acknowledged that with inflation well below the Fed's target of 2%, “there could be more going on there”. Early in the year, the Fed all but signed on the dotted line that it would raise rates three times in 2017, but a third rate hike has become a serious question mark, with the odds of a December hike continuing to dip. According to the CME Group, the current odds for a December increase are just 43%.

Euro Subdued, Eurozone Trade Surplus Misses Estimate

The euro has ticked higher in the Friday session. Currently, EUR/USD is trading just above the 1.14 level. On the release front, the eurozone trade surplus edged up to EUR 19.7 billion, falling short of EUR 20.3 billion. The US will release CPI and retail sales, with both indicators expected to post a weak gain of 0.1%.

Germany may be the catalyst of the eurozone's economic recovery, but the bloc's largest economy has not been immune to low inflation. Final CPI improved to 0.2% in June, compared to -0.2% in May. CPI has managed just one reading above 0.2% in 2017, and earlier in the week, WPI came in at 0.0%. German and eurozone inflation levels remain well below the ECB's target of 2%, and with no indication that inflation levels will move higher anytime soon, the cautious ECB is unlikely to taper its aggressive stimulus package.

The US economy has slowed in 2017, with GDP in the first quarter of 1.4%. Despite a labor market that remains close to capacity, consumer spending has not kept up. Wage growth remains weak, and inflation levels are well below the Fed's target of 2 percent. Later on Friday, the markets will get a look at consumer spending and inflation indicators. The markets are expecting weak gains, which could disappoint investors and hurt the US dollar.

Janet Yellen's testimony on Capitol Hill this week was cautious and the markets didn't show much reaction to her comments. Yellen's message didn't veer from what the markets have already heard from other Fed policy makers. Yellen reiterated that the Fed planned to raise rates “gradually”, and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair didn't provide any timelines, but the most likely timelines are September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and may not need another rate hike. In her testimony before a congressional committee, Yellen reiterated said that she believes the factors weighing on inflation are temporary. However, she acknowledged that with inflation well below the Fed's target of 2%, “there could be more going on there”. Early in the year, the Fed all but signed on the dotted line that it would raise rates three times in 2017, but a third rate hike has become a serious question mark, with the odds of a December hike continuing to dip. According to the CME Group, the current odds for a December increase are just 43%.

Daily Technical Analysis: GBP/JPY Technical Zig-Zag Uptrend

Global Equities were given a boost the past few days, which has been bullish for the GJ pair. Japanese data has been solid the past week, and its major trading partner in China has posted strong data for the week. Whereas, US data has largely been meeting expectations. At this point we can spot 2 POC zones where the price could reject as the pair is making a technical zig-zag pattern. POC1 (D H3, 23.6, EMA89, ATR pivot) comes within 146.65-80 zone. POC1 rejection should be a sign of a strong trend due to technical confluence it makes within the POC itself. If it rejects from this zone the pair should target 147.80 where the doors for 148.50 might be open next week. Deeper retracement targets 145.55-75 zone (D L4, trend line, ATR low, W L4) and rejection from this zone targets 146.80 and 147.80 if the pair makes 4h close above the level.

Buy GBP On Brexit Bill

Buy GBP on Brexit bill

In an important step forward for Brexit, Britain formally acknowledged that there will be a cost to separation from the EU. The media is framing the existing financial obligations as a “bill” which clearly has a punitive and negative connotation. However, owning up to commitments it's the logical and legal action that must occur. The GBP rallied on the news against the USD and EUR. The development is bullish in our view as the glimmer of honestly (in a sea of cloudy Brexit rhetoric) sets up a constructive dialog at next week negotiations. In addition, that acknowledgement of existing and future liability highlight the complexity of executing a “hard” Brexit.

If nothing less a “soft” Brexit will been a necessary for the UK in order to monitor capital allocations and usage. Foreign Minister Boris Johnson has stated that EU must avoid insisting on “extortionate sums.” For the long game we suspect cooler heads will prevail in UK-EU relations proving GBP room for further appreciations. However, our ideal strategy around the sterling remains buy on panic Brexit selling. We are long the bullish reversal off 1.2831 pivot targeting 1.3048 resistance.

Balancing Act at the ECB

At next Thursday's meeting of the ECB's Governing Council (20 July), we expect the Governors to continue their monetary tightening, but to do so in a ‘kind and gentle' way. That is, they will try to soften the blow so as not to roil markets more than necessary.

Next Thursday, we expect ECB Chairman Mario Draghi to act hawkish while trying not to sound hawkish. We believe he will begin plans for a tapering of Quantitative Easing to start on 26 October. We expect QE to end in mid-2018 (depending on market reaction and economic data), and we look for an ECB rate increase by the end of 2018.

Central banks worldwide are shifting toward normalization of interest rates, and this is sending shockwaves through financial markets, pushing yields up 25bp across the yield curve. Draghi recently smashed conventional (dovish) wisdom with hawkish comments, sending the EUR on a bullish tear. He seems inspired by the Eurozone's solid growth and not too fearful of inflation.

GOLD Trading Mixed, SILVER Renewed Bearish Pressures, CRUDE OIL Stalling Below Resistance Area At 46.

GOLD Trading mixed.

Gold's is trading mixed after the precious metal reached the $1200 level. Hourly support is now given at $1204 (10/07/2017 high). Hourly resistance can be found at 1229 (06/07/2017 high). Expected to show renewed bearish pressures in case the resistance level at 1229 holds.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

SILVER Renewed bearish pressures.

Silver's bearish pressures are important. The metal is heading towards hourly support given at 15.18 (10/07/2017 low). Key resistance is given at a distance at 17.75 (06/06/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Stalling below resistance area at 46.

Crude oil is trading above $44. The volatility is declining. Hourly support is given at 43.65 (10/07/2017 low). Expected to show renewed bearish pressures as the black gold is stalling below 46.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).