Sample Category Title

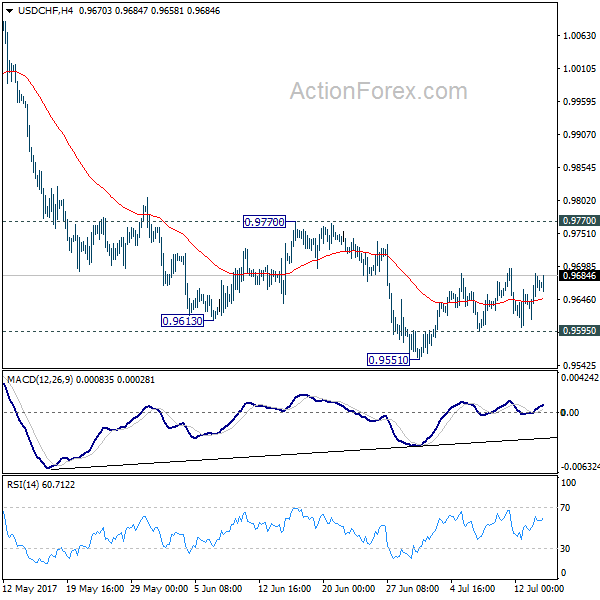

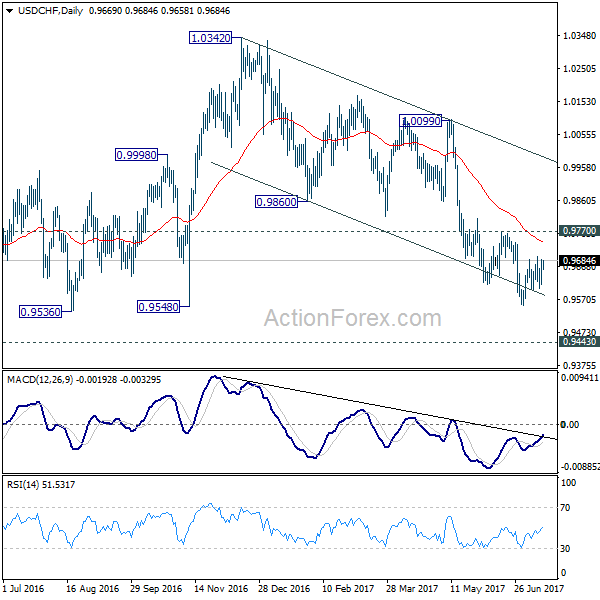

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9629; (P) 0.9657; (R1) 0.9700; More......

USD/CHF is still bounded in the consolidation pattern from 0.9551 and intraday bias remains neutral. Another decline is expected as long as 0.9770 resistance holds. Below 0.9595 minor support will turn intraday bias back to the downside. In such case, USD/CHF should fall through 0.9551 support resume the whole fall from 1.0342 and target 0.9443 key support level next. We'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

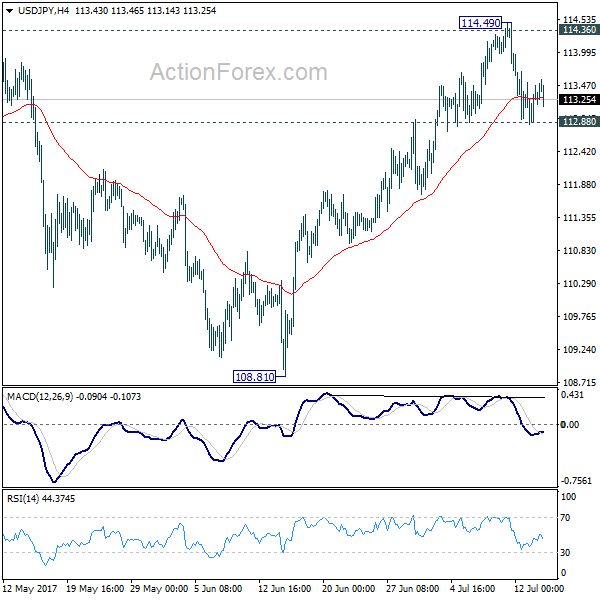

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.92; (P) 113.22; (R1) 113.58; More...

Intraday bias in USD/JPY remain neutral with focus on 112.88 support. Firm break of 112.88 will argue that rebound from 108.81 has completed at 114.49 after being rejected by 114.36 key near term resistance. That would also argue that the correction from 118.65 is still in progress. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 111.98). On the upside, decisive break of 114.36 resistance will confirm that corrective pull back from 118.65 has completed at 108.12. In that case, further rally would be seen to retest 118.65.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85.

Currencies: Key US Data To Decide On Next Directional USD Move

Sunrise Market Commentary

- Rates: US inflation data key with Fed comments in mind

US inflation data will probably be determining for today's trading session. Recent warnings by several Fed governors suggest that a downward surprise could spook markets and question the Fed's tightening intentions. In that case, US Treasuries could profit, outperforming Bunds. - Currencies: Key US data to decide on next directional USD move

The dollar shifted in wait-and-see modus after recent Fed comments on inflation. Today's US data, including CPI and retail sales, might decide on the fate of the US dollar. Strong data are needed for markets to give further credence to the pace of Fed policy normalization and to prevent further USD losses

The Sunrise Headlines

- US stock markets eked out small gains (+0.1%-+0.2%) in an uneventful US trading session. Overnight, Asian stock markets trade mixed with Japan outperforming (+0.5%) and China underperforming (-0.2%).

- Britain has for the first time explicitly acknowledged it has financial obligations to the EU after Brexit, a move that is likely to avert a full-scale clash over the exit bill in talks next week.

- Fed chair Yellen has given the strongest signal yet that regulators are planning to relax a contentious financial safety standard for big banks (eSLR) that executives have complained could perversely encourage them to take more risk.

- Fed Governor Brainard said she's "most focused on getting inflation back up around our 2% target." Dallas Fed Kaplan also said he needs to see inflation moving toward the central bank's goal as he assesses further rate hikes.

- Fitch maintained its A+ rating on China with a stable outlook, citing the strength of the country's external finances and macroeconomic record. ST growth prospects remain favourable, and economic policies have been effective in responding to an array of domestic and external pressures in the past year.

- Republicans launched their latest attempt to secure a longed victory on US healthcare by dropping a planned tax rollback for the wealthy. The new bill already drew criticism from senators on both sides of the political divide.

- Today's eco calendar heats up in the US with CPI inflation, retail sales, industrial production and Michigan consumer confidence. JP Morgan, Citigroup and Wells Fargo publish Q2 earnings.

Currencies: Key US Data To Decide On Next Directional USD Move

US CPI to decide on dollar's fate?

There was no dominant story to guide FX trading yesterday. The dollar remained in the defensive in the wake of Yellen's testimony on Wednesday, but the pressure eased. Markets awaited today's key US data. EUR/USD dropped temporary below 1.14, but rebounded on rumours that ECB's Draghi might herald a policy change at Jackson Hole. EUR/USD closed the session at 1.1398. USD/JPY finished at 113.28.

Asian equities are trading mixed, awaiting key US data later today. Japanese equities outperform as USD/JPY regained the 113 mark. Markets are looking forward to next week's BOJ policy meeting. The BOJ is expected to maintain its cap on the 10-year government bond yield even as rates in other major economies are trending higher. The pair trades in the 113.40 area. The Aussie dollar maintains this week's gain and is near the 0.7750/0.7835 resistance area. EUR/USD remains in wait-and-see modus, holding in the low 1.14 area.

There are again no market moving European eco data today. However, US data might be decisive for the next directional move of the dollar, with June retail sales, CPI & production and July Michigan consumer confidence. Especially the retail sales and CPI are key. Core and headline CPI are both expected at 1.7% (0.2% M/M and 0.1% M/M). Retail sales are expected to regain traction after mediocre May data (but strong readings in March and April). Consensus expectations are not very high, both for the retail sales and the CPI. If inflation drifts further away from the 2%-mark (<1.7 % outcome) , it will almost certainly cause a further loss of interest rate support for the dollar. Consumer confidence from the University of Michigan is expected little changed at a high level (95).

Dollar sentiment remained fragile after Friday's payrolls. Yellen putting the focus on inflation made markets ponder the pace of Fed normalisation and weighed further on the dollar. Yesterday, the dollar decline took a breather, but the picture US currency's technical picture remains fragile. As we see a good chance for the data to meet the consensus, the dollar might start looking for a bottom after the recent setback. However, the is little room for miss, especially not for the CPI.

Technical picture: USD looking for a bottom

A combination of hawkish ECB comments and soft US data pushed EUR/USD above the 1.1300/66 resistance area end June. The payrolls were not good enough to trigger a sustained USD rebound. Next resistance in the 1.15 area is looming. LT-correction tops stand at 1.1616/1.1714. A break would end the long consolidation period that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area will be difficult to break for now. A return below the 1.13 area would be a first indication of a loss in upside momentum. EUR/USD 1.1119/10 is the next important support.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair above the 112.13 correction top, but follow-through gains remain modest. USD/JPY 114.37 resistance was tested, but for now the test is rejected. This at least suggests a pause in the recent USD/JPY uptrend. We stay cautious on USD/JPY long positions despite the recent good performance.

EUR/USD: Today's data to decide on next USD move

EUR/GBP

Sterling rebound to slow?

Sterling regained further ground yesterday, extending the rebound that started after good UK labour data. We see the rebound in the first place as technical in nature. Cable profited from underlying USD softness. A topside test of EUR/GBP was rejected on Wednesday and the broader euro correction also triggered further profit taking on EUR/GBP longs. The UK government published the Brexit ‘Repeal Bill'. It will probably become a source of political noise, but we didn't see a big impact on sterling trading yesterday. BoE's McCafferty further complicated the BoE's monetary policy debate as he raised the issue of reducing the BoE's Balance sheet. His comments might have been slightly supportive for sterling. EUR/GBP closed the session at 0.8809. Cable finished the day at 1.2939.

There are no important eco data in the UK today. There might still be some political noise on the Repeal bill, but we don't expect it to change fortunes for the UK currency right now. So, the gyrations in the dollar might be decisive for sterling trading. The UK currency made a nice ST rebound, especially against the euro. This move might slow.

From a technical point of view, EUR/GBP set a minor top north of 0.8854/66 resistance (2017 top) and finally broke below the 0.8 barrier earlier this week. Quite some sterling negative news should already be discounted at current levels. Even so, the short-term trend remains euro positive/sterling negative. A test of the 0.90 barrier might be on the cards. A break below 0.8720 would suggest that upside momentum is easing.

EUR/GBP topside test rejected, for now

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2705; (P) 1.2738; (R1) 1.2755; More....

Intraday bias in USD/CAD remains on the downside. Current fall is expected to extend to retest 1.2460 low. On the upside, break of 1.2938 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The second leg should have finished at 1.3793. Break of 1.2460 will extend such correction to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. However, firm break there will target 100% projection of 1.4689 to 1.2460 from 1.3793 at 1.1564.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

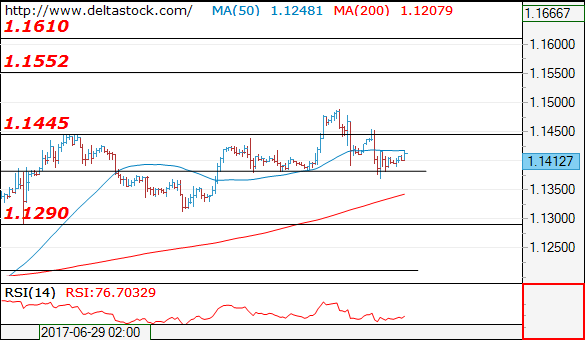

EUR/USD

Current level - 1.1412

With the recent dip below 1.1380 there is a risk of another slide to 1.13+ area, but the overall bias remains positive, for a rise towards 1.1610. trigger on the upside is 1.1452 high.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.1452 |

1.1550 |

1.1380 |

1.1290 |

|

1.1550 |

1.1610 |

1.1290 |

1.1020 |

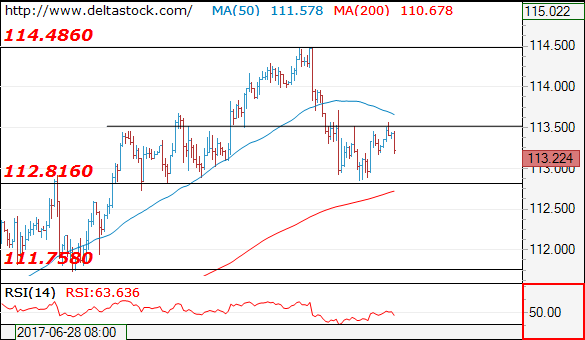

USD/JPY

Current level - 113.22

The rebound above 1.1280 is corrective in nature, thus preceding another leg downwards, to 111.75 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

113.50 |

115.50 |

112.80 |

111.75 |

|

114.50 |

115.50 |

111.75 |

110.20 |

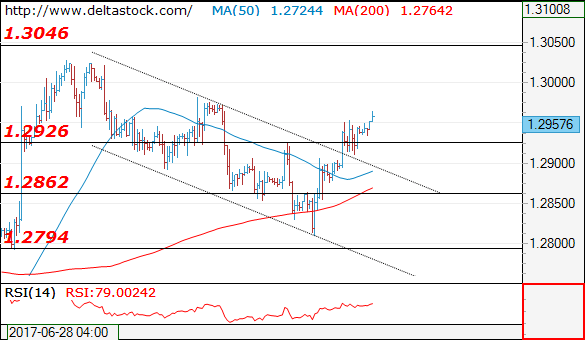

GBP/USD

Current level - 1.2957

Yesterday's break through 1.2920 confirms, that a low is in place at 1.2810 and my outlook remains bullish, for a rise towards 1.3050 area. Initial intraday support lies at 1.2900.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2980 |

1.3050 |

1.2900 |

1.2635 |

|

1.3050 |

1.3500 |

1.2790 |

1.2480 |

US Labour Market Strengthens

The Federal Reserve appears to be on track for a 3rd interest rate increase for the year as recent data releases appear to show US economic policies are on track. The US Labour Department released data that showed Initial claims for unemployment benefits dropped 3K to a seasonally adjusted 247K for the week ended July 8. This is the latest indication that the US labor market strength is sustaining economic growth. Separately, the Producer Price Index rose 0.1% in June, after being unchanged in the previous release. Core PPI increased 2% in the 12 months through June after climbing 2.1% in May. Fed Chair Yellen finished her testimony to Congress and expressed confidence in the US economy and monetary tightening would be a gradual process. This “slow and gradual” process came after indications from Central Bankers that stimulative policies may no longer be required as the overall global market strengthens.

US and European Equities were in striking distance of recent record highs, with some profit taking slowing the upward momentum. Asian equities have also performed strongly with the MSCI Asia Pacific Index up 2.6% and Hong Kong’s Hang Seng posting a 4% rise on the week.

USD is somewhat stagnant against its major counterparts, with little change overnight as the markets wait for today’s economic data releases. Currently EURUSD is trading around 1.1410, GBPUSD: 1.2960, USDJPY: 113.40, AUDUSD: 0.7745 & USDCAD: 1.2730.

Gold bounced from early lows of $1,214.67 to trade currently around $1,218.25.

WTI is trading near the day’s highs around $46.30pb and looks set to have a 4% rise on the week.

At 11:00 BST EUR Trade Balance for May will be released. The consensus calls for a moderate increase to €20.3 Billion from the previous €19.6 Billion. With markets expectations being met, by recent CPI readings from France & Germany, the EUR may stay in demand against its major counterparts.

At 13:30 BST the US will release a plethora of data; Retails Sales, Consumer Price Index & Industrial Production. There may be mixed reactions from the market as Retail Sales (MoM) (Jun) are expected to show a 0.1% rise compared to the previous reading of -0.3% and CPI (YoY) (Jun) is expected to come in at 1.7% down from the previous release of 1.9%. Retail Sales up should provoke USD buying but CPI down would typically result in USD selling. Industrial Production (MoM) (Jun) may help determine the direction of USD, as the market is expecting a release of 0.3% (previously 0.0%) – which may be regarded as inflationary, thereby seeing interest rates rising and USD buying.

Fed Caution Pressures Dollar, Gold Edges Higher

It has certainly been an eventful week for the financial markets, as comments from central bank heavyweights which fueled monetary policy speculations and political uncertainty in Washington, breathed life back into the currency and equity markets. Janet Yellen was the talk of the town after catching investors unaware by adopting a dovish stance in her testimony before Congress. While Yellen reiterated her mantra on how the central bank plans to continue ‘gradually' tightening monetary policy, there were concerns raised over low inflation despite an improving economy. With the Federal Reserve potentially scaling back on its expected pace of monetary policy normalization if inflation fails to pick up, Friday's pending US CPI report is a big deal and will be closely observed.

The main takeaway from Yellen's testimony was that although she remained optimistic over the health of the US economy, this was masked by concerns about persistently low inflation. Dollar bullish investors struggled to find inspiration from Yellen's optimism during Thursday's trading session, with the Dollar Index edging towards 95.75 as of writing. With political risk at home and the appearance of doves enticing bears, the Dollar may find itself vulnerable to further losses.

Commodity spotlight – Gold

Gold prices edged lower on Thursday after Yellen expressed some optimism over the health of the US economy in her testimony before Congress. Although the yellow metal remains bearish on the daily charts, the Feds' concerns of low inflation and continuous focus on ‘gradual' rate hikes may support the zero-yielding metal. With the Dollar under noticeable pressure and political risk in Washington stimulating risk aversion, bulls could be inspired to conquer $1230. From a technical standpoint, although repeated weakness below the $1240 resistance is likely to keep bears in the game, a breakout above $1230 could be early signs of bulls making a comeback.

EUR/USD Setting Up For A Large Move, EUR/GBP False Breakout? EUR/JPY Buying Opportunity?

EUR/USD setting up for a large move

The currency pair posted humble gains in the morning and continues to stay above a major static support. Has signalled an exhaustion in the last days, but maintains a bullish perspective on the short term because is located above some important support levels.

The USDX moves sideways on the Daily chart and is waiting for a bullish spark today from the United States data. Only a dollar index rally could force the EUR/USD to start a broader leg lower in the upcoming weeks.

The Euro-zone is to release the Trade Balance later, the surplus could increase to 20.3B from 19.6B in May, while the Italian Trade Balance is expected to decrease from 3.60B t0 2.43B, but don’t think that will have a significant impact. Everyone is focusing on the US economic numbers, which will bring a high volatility in the afternoon.

Price increased and is trading much above the 1.1376 major static support (resistance turned into support), could move sideways in the upcoming hours. We had a false breakdown below the 1.1376 level, actually has closed much above this downside obstacle, signalling that the bulls are very strong.

Technically the price has shown some overbought signs, but I want to remind you that the fundamental factors will take the lead and will drive the pair, the direction is uncertain.

A valid breakdown below the 1.1376 will open the door for more declines and the Rising Wedge pattern will be confirmed, while a valid breakout above the 1.1466 static resistance will signal a further increase in the upcoming period.

EUR/GBP false breakout?

EUR/GBP dropped aggressively in the last two days and invalidated a breakout above a strong dynamic resistance. Right now is pressuring an important dynamic support, looks determined to ignore this obstacle. Is trading right above the 0.8800 psychological level, a valid breakdown below this level will attract more sellers, which will drive the price towards 0.86, 0.8550 levels.

Is trading in the red after the impressive sell-off, could drop further after the false breakout above the second warning line (wl2) of the minor descending pitchfork. We’ll have a selling opportunity only if will slip below the median line (ML) and if will retest this line.

A valid breakdown below the median line (ML) will invalidate the breakout above the 100% Fibonacci level and from the extended sideways movement. The bullish perspective remains intact as long as the ML is unharmed.

EUR/JPY – buying opportunity?

Looks like that the minor retreat is completed and could jump higher again in the upcoming period. EUR/JPY has found strong support at the upper median line (UML), a rejection here will send it much above the 130.00 psychological level, but personally I’m waiting for a confirmation that will really resume the upside movement. We’ll have a great buying opportunity from the confluence area formed at the intersection between the UML wil the median line (ml) of the minor ascending pitchfork, the first upside target will be at 130.75 previous high.

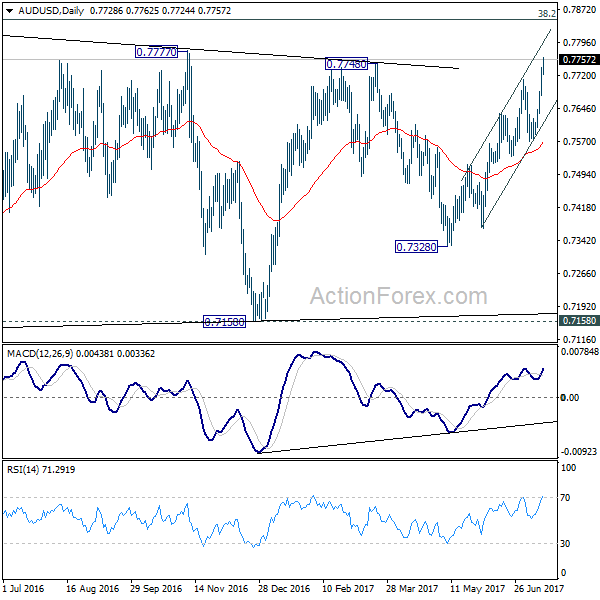

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7688; (P) 0.7713; (R1) 0.7754; More...

AUD/USD's rally continues today and reaches as high as 0.7762. Break of 0.7711 confirms resumption of rise from 0.7328. Intraday bias remains on the upside for 0.7833. Still, there is no clear sign of range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7713 minor support will turn intraday bias neutral first. But near term outlook will remain bullish as long as 0.7570 support holds.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8082) and above.

Dollar Stays Weak ahead of CPI and Retail Sales, Cautious Fed Comments Weigh

Dollar stays soft on cautious comments from Fed officials. Testifying before the Senate Banking Committee, Fed CHair Janet Yellen indicated that risks from inflation are two-sided, and it was premature to conclude that the underlying inflation trend would continue to fall below the 2% target, despite the slowdown in the price gains in recent months. Dallas Fed President Robert Kaplan advocated a cautious approach to rate hike and said that "future removals of accommodation should be done in a gradual and patient manner."

The budget director of White House Mick Mulvaney revealed US President Donald Trump's economic plan in an articled titled "Introducing MAGAnomics". MAGA was from Trump's slogan of "Make America Great Again". A seven-point plan was laid out targeting to boost US GDP growth to 3% on annual basis. Part of the article was published at the White House website here. At the end of the extract, there is a link to read the full op-ed which points to a Wall Street Journal page. Then, the WSJ page requests readers to "subscribe" to read the full story. It's unsure whether the article is for the wealthiests in Wall Street, or those common people you can find on the street.

Instead of looking at the plan, let's look at the response from other professionals. The Congressional Budget Office said in the report that "because details of the proposed policies are not available at this time, CBO cannot provide an analysis of all their macroeconomic effects." Fed chair Janet Yellen said that Trump's 3% growth aspiration is "something that would be wonderful if you can accomplish it". She added, however, that "it would be quite challenging".

In the markets, DOW rose 20.95 points, or 0.1% to close at 21553.09 but it's kept below Wednesday's high at 21580.79. S&P 500 rose 4.58pts or 0.19% to close at 2447.83, below recent high at 2453.82. NASDAQ rose 13.27 pts, or 0.21% to close at 6274.44, well off recent high at 6341.70. 10 year yield rose 0.021 to close at 2.348, well off last week's high at 2.936. The financial markets were not too impressed by the MAGAnomics.

Today's set of economic data from US will be crucial in Dollar's near term trend. Headline CPI is expected to slow to 1.7% yoy in June while core CPI is expected to be unchanged at 1.7% yoy. Retail sales and ex-auto sales are both expected to grow 0.2% in June. Industrial production, business inventories and U of Michigan confidence will also be released. Elsewhere, Eurozone trade balance will be featured in European session.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7688; (P) 0.7713; (R1) 0.7754; More...

AUD/USD's rally continues today and reaches as high as 0.7762. Break of 0.7711 confirms resumption of rise from 0.7328. Intraday bias remains on the upside for 0.7833. Still, there is no clear sign of range breakout yet. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7713 minor support will turn intraday bias neutral first. But near term outlook will remain bullish as long as 0.7570 support holds.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8082) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business Manufacturing Index Jun | 56.2 | 58.5 | 58.2 | |

| 4:30 | JPY | Industrial Production M/M May F | -3.60% | -3.30% | -3.30% | |

| 9:00 | EUR | Eurozone Trade Balance (EUR) May | 20.3B | 19.6B | ||

| 12:30 | USD | CPI M/M Jun | 0.10% | -0.10% | ||

| 12:30 | USD | CPI Y/Y Jun | 1.70% | 1.90% | ||

| 12:30 | USD | CPI Core M/M Jun | 0.20% | 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Jun | 1.70% | 1.70% | ||

| 12:30 | USD | Advance Retail Sales Jun | 0.20% | -0.30% | ||

| 12:30 | USD | Retail Sales Less Autos Jun | 0.20% | -0.30% | ||

| 13:15 | USD | Industrial Production Jun | 0.30% | 0.00% | ||

| 13:15 | USD | Capacity Utilization Jun | 76.80% | 76.60% | ||

| 14:00 | USD | U. of Michigan Confidence Jul P | 95 | 95.1 | ||

| 14:00 | USD | Business Inventories May | 0.30% | -0.20% |