Sample Category Title

Technical Outlook: EURUSD – Correction To Precede Fresh Upside

The Euro is holding in extended consolidation under fresh one-year high at 1.1445wher renewed upside attempts on Friday were rejected. Consolidation is so far holding within narrow range, but deeper correction of last week's strong rally is likely. Slow stochastic is turning south in deep overbought territory on daily chart and RSI is also reversing after brief probe into overbought zone. Firm break below 1.1400 handle is needed to signal pullback and expose supports at 1.1368 (Fibo 23.6% of 1.1188/1.1445/hourly cloud base) and more significant 1.1320 (Fibo 38.2%) and 1.1300 (former tops). Dip-buying scenario remains in play, as broader uptrend from 1.0340 (2017 low) is looking for further extension higher. Deeper pullback would face next supports at 1.1280 zone (converged daily Tenkan-sen/Kijun-sen) and needs to find ground above 1.1243 (20SMA/Fibo 61.8%) to keep bulls in play.

Res: 1.1426, 1.1445, 1.1500, 1.1550

Sup: 1.1368, 1.1320, 1.1300, 1.1280

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

USD/JPY – 112.84

The greenback has continued trading with a firm undertone, suggesting the rebound from 108.82 low is still in progress, hence upside risk remains for marginal gain from there, however, loss of upward momentum should prevent sharp move beyond 113.00 and bring retreat later, below 111.73 support (Friday’s low) would suggest top is possibly formed, bring weakness towards 110.95 support but a daily close below the Kijun-Sen (now at 110.88) is needed to add credence to this view, bring subsequent weakness to 110.65 and later towards 110.00.

On the upside, above 113.10-20 would signals the fall from 114.39 has ended at 108.82 and upside risk remains for the rebound from there to extend further gain to 113.50 and later towards 114.00. Having said that, as broad outlook remains consolidative, upside should be limited and said resistance at 114.39 should hold. Only a break above said resistance at 114.39 would shift risk to upside and signal another leg of rise from 108.13 low is underway for headway to 114.60-65, then towards resistance at 115.51.

Recommendation : Hold short enter at 112.25 for 110.25 with stop above 113.25.

On the weekly chart, last week’s rise formed another white candlestick (3rd in a row), suggesting the rebound from 108.82 is still in progress and further gain from here cannot be rule out, however, as broad outlook remains consolidative, reckon upside would be limited to 113.85 and resistance at 114.39 should hold. Only a break above resistance at 114.39 would signal another leg of rebound from 108.13 low is underway for test of resistance at 115.51 but a weekly close above there is needed to signal the fall from 118.66 top has ended at 108.13, then headway to 116.00-10 would follow but resistance at 117.53 should hold from here.

On the downside, whilst pullback to 111.90-95 cannot be ruled out, support at 110.95 should hold and bring another rebound. Below 110.95 would suggest the rebound from 108.82 has ended, bring weakness to 110.00 and possibly towards the lower Kumo (now at 109.51) but support at 108.82 should remain intact, bring further consolidation. Below 108.82 would bring retest of 108.13 but break there is needed to retain bearishness and signal the fall from 118.66 top has resumed and extend decline towards previous resistance at 107.49.

EURUSD Bullish Bias Intact But Rally Takes A Breather

EURUSD maintains the strong bullish phase that took place in the final week of June. The pair paused its rally after reaching its highest level since early May 2016 at 1.1444 on June 29. The 50-day moving average is still heading north after a bullish crossover that took place on May 22 at 1.0816.

Following the strong upside move last week, the market reached overbought conditions, as indicated by the RSI. It is currently showing that momentum has retreated slightly below 70 but is within sight of overbought territory. The fading upside momentum suggests that a consolidation phase is likely for EURUSD in the short term. A move back below 1.1130 would indicate that the short-term bullish phase has ended.

Any upside moves would target 1.1615, the high from May 2016. A break of this major resistance level would open the way towards the August 2015 high at 1.1713.

Since the market is quite overextended, a pullback is possible. In this case, support is located around 1.1280. This level has acted as a resistance area in the past and is thus considered to be an important level to the downside. Below this, the levels at 1.1130 and 1.1015 are expected to provide support. Finally, the level at 1.0816 is important support since it converges with the 200-day MA.

After such a sharp rally in recent days, EURUSD is likely to take a breather, providing more risk to the downside than to the upside in the near term. But looking at the bigger picture, the uptrend that started from the January 3 low at 1.0340 to the June 29 high of 1.1444 is still intact. Trend indicators are giving a bullish market structure, as prices are above the daily Ichimoku cloud and there was a bullish crossover of the 50-day MA with the 200-day MA. Meanwhile, the 50-day MA is still rising.

Gold Holds Bearish Bias, Scope For Further Downside

Gold is holding a negative bias in the short-term as prices approach the June 26 low of 1235.74. The market has been making lower highs and lower lows since falling from the June 6 peak of 1295.97.

The 20-period moving average has crossed below the 50-period MA, giving a bearish signal. The short-term moving average is pointing down, highlighting the bearish view. Meanwhile, the RSI is below 50 in bearish territory, indicating there is a negative bias in the market. The oscillator has not crossed below 30, so gold is not oversold yet, leaving room for further downside.

The immediate target is the June 26 low of 1235.74. Breaking below this level would extend the downside move towards 1226.42 as the next support level. This was an area of congestion in the past. The next main support is located at the May 9 low of 1214.17

Overall, downside pressure is expected to remain strong in the near term as long as the market is trading below the 50-perdiod MA. Only a move above 1248.14 would weaken the bearish bias. This level is an important resistance area as it provided both resistance and support in the past. This is also where the 50-period MA converges. The next main resistance level comes in at 1258.73, a previous high (June 23) and also a support level in the past.

A move above the June 14 high of 1280.82 would cancel the short-term bearish view and this would open the way to re-test the June 6 high of 1295.97. From here, there is scope to resume the uptrend that took place from 1214.17 to 1295.97.

Dollar Modestly Up, Euro Falls Below 1.14

Today's Asian session saw the dollar broadly advancing relative to other majors, though its gains were limited in nature. China's Caixin manufacturing PMI positively surprised, pushing the yuan higher, while a negative backdrop could potentially form for the yen after Prime Minister Shinzo Abe's Liberal Democratic Party lost an election in Tokyo.

As Asian traders were completing their day, the dollar index was up two-tenths of a percent at 95.79. The index, which gauges the greenback against a basket of major currencies, hit a nine-month low of 95.47 during Friday's trading. The US currency suffered sizable losses last week against the euro, pound and the loonie after relatively hawkish comments by the European Central Bank, Bank of England and Bank of Canada heads.

Dollar/yen was last up four-tenths of a percent on the day at 112.81. Euro/dollar and pound/dollar were both down two-tenths of a percent with euro/dollar marginally below the 1.14 handle and pound/dollar at the 1.30 mark. Dollar/loonie was up more than two-tenths of a percent, eyeing the 1.30 handle.

The yen could be under pressure today after Prime Minister Shinzo Abe's party suffered a defeat in an election yesterday in Tokyo, the nation's capital. Tokyo elections have on occasion served as bellwethers for the outcome in the upcoming general elections. Adding to that the fact that the Bank of Japan is one of the few major central banks which has not yet signaled scaling back on its ultra-loose monetary policy, and a weaker yen further ahead has a greater probability of materializing.

In positive news out of Japan, its Tankan large manufactures and non-manufacturers indices both showed an improvement during the second quarter of the year. The yen posted some minor gains relative to the greenback as the data became public.

The June Caixin manufacturing PMI out of China added to last week's upbeat official PMI figures. Specifically, it came in at 50.4, beating forecasts for a reading of 49.5, while it was above May's 49.6. The Chinese currency benefitted upon the release of the figures. Dollar/yuan last traded slightly up on the day at 6.78. The pair contracted (yuan has been strengthening during the past) in the previous four days.

China and Hong Kong are today launching a 'Bond Connect' scheme is an effort to develop mutual capital markets access.

The commodity-linked Australian and New Zealand dollars were both trading down two-tenths of percent versus their US counterpart with the close of Asian markets at $0.7674 and $0.7314 respectively. The aussie failed to receive a boost after the positive figure for Chinese manufacturing PMI. Australia and China trade heavily with each other.

In other Australian news, the country's central bank will be holding its monthly policy meeting tomorrow during which it is expected to maintain its key benchmark rate at the record low of 1.5%.

Turning to commodities, gold hit a one-and-a-half-month low of $1234.72 an ounce in today's trading. It was last down two-tenths of a percent, just shy of the $1235 level. WTI and Brent crude last traded at $46.29 and $48.99 a barrel respectively, both up five-tenths of a percent.

As regards the rest of the day, manufacturing PMI figures out of the US, eurozone and the UK will be gathering the forex market participants' attention. Bank of England Governor Mark Carney is also scheduled to speak at 12:00 GMT.

Market Update – Asian Session: Major PMI’s For The Region Remain In Expansion Territory, Japan LDP Suffers Defeat In...

Summary

Asian markets were generally higher, but with little to push the markets, they drifted a bit directionless into mid-day break. USD/JPY started the day with a gap open at 112.06 after PM Abe’s LDP party suffered a blow in the Tokyo Governor elections. Chatter is there will be a re-shuffle of his cabinet by August and he may have to push back planned sales tax hike from Oct of 2019. The Q2 Tankan survey did little to shift the yen, as data came in a bit better than expected and improved from Q1. Japan’s final manufacturing PMI also confirmed expansion.

The China/Hong Kong bond connected opened today. China Caixin manufacturing reached a 3-month higher which helped to bring the Shanghai Composite back into positive territory. PBOC again skipped open market operations for the 7th consecutive day. Financial press speculated on the $7.2B in dividends that offshore Chinese companies will payout in July and its impact on the yuan. Former PBOC member Yu Yongding commented thathigh domestic savings rates, overwhelming concentration of debt among state-owned enterprises, large FX reserves and the largely closed capital account as factors preventing crisis scenarios.

Economic data in Australia showed a dip in May building approvals, even lower than expectations. PMI manufacturing rose to 55 remaining in expansion territory. AUD/USD remained in a tight range; with the next big catalyst on July 4th when the RBA will hold is interest rate decision. They are expected to keep rates on hold at 1.5%.

Politics

(JP) Incumbent Tokyo Gov Yuriko Koike won landslide victory in election with her Tokyo Residents First Party securing 49 out of the 127 seats, and will hold a majority 79 along with its allies including the Komeito party

(JP) Japan PM Abe may reshuffle cabinet as early as August - Japan press

Key economic data

(JP) JAPAN Q2 TANKAN LARGE MANUFACTURING INDEX: 17 V 15E; MANUFACTURERS OUTLOOK: 15 V 14E; ALL-INDUSTRY CAPEX: 8.0% V 7.2%E

(CN) CHINA JUN CAIXIN PMI MANUFACTURING: 50.4 V 49.8E (3-month high)

(AU) AUSTRALIA JUN AIG MANUFACTURING INDEX: 55.0 V 54.8 PRIOR (9TH CONSECUTIVE MONTH OF EXPANSION

(AU) AUSTRALIA JUN CORELOGIC HOUSE PRICES M/M: 1.8% V -1.1% PRIOR

(AU) AUSTRALIA MAY BUILDING APPROVALS M/M: -5.6% V -1.3%E; Y/Y: -19.7% (9TH CONSECUTIVE DECLINE) V -14.1%E

(JP) JAPAN JUN FINAL PMI MANUFACTURING: 52.4 V 52.0 PRELIM

(KR) SOUTH KOREA JUN PMI MANUFACTURING: 50.1 V 49.2 PRIOR

(AU) AUSTRALIA JUN MELBOURNE INSTITUTE INFLATION M/M: 0.1% V 0.0% PRIOR; Y/Y: 2.3% V 2.8% PRIOR

Speakers and Press

China

(CN) Former PBOC member Yu Yongding: Deleveraging poses more of a risk of deflation to China than financial crisis

(CN) PBOC Vice Gov Pan Gongsheng: Bond link shows China's will to enhance Hong Kong as a financial hub; foreign issuers have strong interest in yuan bonds in China

Japan

(JP) Japan Fin Min Aso may be in violation of minister code for purchasing golf membership - Japan press

(JP) Japan Chief Cabinet Sec Suga: Abe administration to continue prioritizing the economy

(JP) Nikkei explores BOJ outlook report expected on July 20th: inflation forecasts could be revised down to around 1% for FY17 from 1.4% in the April report, while FY18 could be lowered to ~1.5% from 1.7%

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.2%, Hang Seng +0.1%, Shanghai Composite +0.0%, ASX200 -0.3%, Kospi -0.3%

Equity Futures: S&P500 +0.2%; Nasdaq +0.3%, Dax +0.2%, FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1426-1.1403; JPY 112.57-111.97; AUD 0.7695-0.7667; NZD 0.7345-0.7315

Aug Gold -0.3% at 1,238/oz; Aug Crude Oil +0.3% at $46.19/brl; Sept Copper -0.1% at $2.70/lb

(CN) PBOC skips open market operations (7th straight skip)

(CN) PBOC SETS YUAN MID POINT AT 6.7772 V 6.7744 PRIOR

(KR) Bank of Korea (BOK) sells KRW0.70T in 6-month monetary stabilization bonds; avg yield 1.33% v 1.30% prior

USD/CNY Analysts suggest the $7.8B in dividend payments due by China's offshore listed companies in July will put downward pressure on the yuan

Asia equities notable movers

Australia

Fairfax Media, FXJ.AU Confirms it has ended private equity talks and plans to proceed with domain separation; Guides FY17 EBITDA A$262-266M; -10.3%

Japan

Daiichi Sankyo, 4568.JP Top-line results from Phase 3 Global Clinical Development Program evaluating Mirogabalin in pain syndromes met primary endpoint; -2.3%

Hong Kong/China

Casino names all lower after June Macau gaming rev was lower than expected, attributed to China President Xi’s visit to Hong Kong the last week of the month

China Jicheng Holdings,1027.HK Names in David Webb's "50 HK stocks not to own"; -23%

Hangzhou Tigermed Consulting,300347.CN Guides H1 Net CNY109-125M, +40-60% y/y; +10%

Currencies: US Data To Help The Dollar

Sunrise Market Commentary

- Rates: Will the sell-off take a pause or will strong US data hit especially US bonds?

The US ISM could be stronger than expected today, but traders might be hesitant to react ahead of tomorrow's holiday. We do expect strong US labour market data later this week, which might give US Treasuries the lead in the global sell-off. German bonds face tough resistance. A sell-on-upticks might therefore be appropriate, unless a break occurs. - Currencies: US data to help the dollar

US data will be key this week. Today, the US manufacturing ISM is expected at a decent level. An upward surprise might restore confidence on the US recovery and on the dollar. If so, last week's EUR/USD top might become a first resistance.

The Sunrise Headlines

- US stocks closed Friday with slight gains (S&P 500 at +0.15%). Asian stock markets continue on this path as they also struggle to gain traction in early trading.

- Japanese PM Abe's Liberal Democratic Party suffered an historic defeat in an election in Tokyo (losing half of its seats), signalling trouble ahead for the Abe, who has suffered from slumping support because of a favouritism scandal.

- Japan's Tankan survey of business conditions at Japan's large manufacturers jumped to 17 in Q2 from 12 in Q1, besting a median forecast of 15. Business conditions also improved more than predicted for SME manufacturers

- The Japanese Nikkei-Markit PMI increased to 52.4 in June from 52 in May. Manufacturers upped their purchasing activity on new orders and higher production requirements. Employment rose too.

- The China Caixin-Markit manufacturing PMI rose to 50.4 in June after falling into contraction in May (49.6 in May, consensus of 49.8). Growth in output and new orders rose marginally, while employment continued to contract.

- China and Hong Kong have launched a bond trading link that allows foreign fund managers to trade in China's $9 trillion government, agency and corporate debt markets without the need for an onshore account.

- The eco-calendar's most interesting releases are the UK's manufacturing PMI, the US manufacturing ISM and the Eurozone unemployment rate

Currencies: US Data To Help The Dollar

US data to help the dollar?

The strong three-day EUR/USD rally ran into resistance Friday, but there was also no real USD rebound. Yield differentials widened slightly in favour of the dollar. US equities outperformed European ones. EUR/USD closed at 1.1426 versus 1.1440 on Thursday. USD/JPY traded in a small band. The yen started strong, but USD/JPY closed with a small gain at 112.39 as US equities kept up well. Appetite to take additional positions was clearly missing, as it was the final the day of the quarter and as many US traders prepared for a long weekend with US markets closed for the 4th of July holiday tomorrow.

Overnight, Asian equities are trading mixed. The Japan Tankan business sentiment was stronger than expected (see headlines). The Caixin China manufacturing PMI also improved slightly. Decent regional data don't help the yen this morning. USD/JPY opened slightly in the red, but reversed the initial loss. A further rise in the oil price and a rise in US yields are supporting the dollar. USD/JPY trades in the 112.50 area. EUR/USD dropped slightly to the low 1.14 area and trades currently at 1.1415.

The attention turns this week to the US eco data. We expect an improvement after the lacklustre performance of late. EMU data are less important with today the final June manufacturing PMI and the unemployment rate. The US manufacturing ISM is expected to rise slightly, but we see risks to the upside of consensus. Further out this week the US labour market data will be of paramount interest. We see upward risks. The Minutes of the FOMC meeting might also be interesting to get a better take on the start of the balance sheet tapering and on the different value the Fed attributes to a strong labour market on the one hand and lower inflation on the other hand. The EMU data are less important, but after the bond sell off, it will be interesting whether ECB speakers will try to change market views on the outlook for policy.

In a daily perspective, we look out whether the US ISM might be strong enough to help a USD rebound against the euro. A decent report, which we expect, should help a topping out process after the recent EUR/USD rally. In case of good US labour data, we see also room for a re-widening of the USD/EMU interest rate differential as the recent rise in German/EMU yields was quite impressive. That said, the dollar remains vulnerable in case of a negative surprise. We start the week with a tentative USD-positive bias and look out whether last week's top in EUR/USD might become a more solid resistance. A decent US ISM and a constructive equity sentiment might also be a USD/JPY positive. However, it will be difficult to take out the recent top just below 113. For that to happen, as strong Payrolls report is probably needed.

Technical picture: USD looking for a bottom

A combination of hawkish ECB comments and weaker US eco data pushed EUR/USD last week above the 1.1300/66 resistance area with a new high at 1.1448. The next resistance is now the 1.15 area. Further out LT correction tops are coming in at the 1.1616/1.1714. A break would end the long consolidation period that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area will be difficult to break for now. A drop below 1.1119 would suggest the pair enters calmer waters.

The USD/JPY rally ran into resistance in early May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair the 112.13 correction top early this week, but there were no real follow-through gains , So, the break isn't confirmed yet. A break would improve the ST-picture. Even so, were remain cautious on further USD/JPY gains.

EUR/USD Will good US data support the dollar and cap the EUR/USD rally?

EUR/GBP

Sterling extends rebound

On Friday, cable approached key 1.3044 resistance in Asia, but a real test didn't occur, sending GBP/USD temporary lower again. UK data made no difference: Outdated Q1 GDP was confirmed at a weak 0.2% Q/Q. Trading in Cable and EUR/GBP was mostly technical in nature. Some sterling short-covering prevailed at the end of the month/quarter. EUR/GGBP closed the session at 0.8771 (from 0.876). Cable finished the day on a strong bid at 1.3030.

Today, the UK Manufacturing PMI is expected little changed at 56.3 from 56.7. This is still a healthy level and other UK data were not too bad of late. So, we assume that the report might be considered constructive in the markets. The past weakening of sterling is a positive for the UK manufacturing sector. So, the report might support a further technical comeback of sterling. The Brexit negotiations are on ongoing issue. Any progress on the rights of EU/UK citizens might suggested a less hard Brexit. All in all, we see EUR/GBP staying below the key resistance of 0.8866/80 and cable's fate will depend on EUR/USD. If the cross would move higher, cable may test the 1.3048 resistance but a break looks unlikely.

From a technical point of view, EUR/GBP set a minor top north of the 0.8854/66 resistance (2017 top), but a sustained break didn't occur. Recent setbacks will probably block further gains ST. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach remains favoured.

EUR/GBP topside test rejected. A modes/temporary sterling comeback might be on the cards

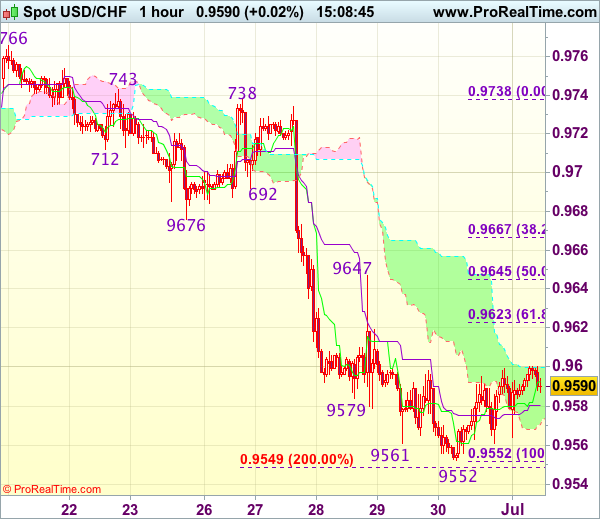

Trade Idea : USD/CHF – Sell at 0.9645

USD/CHF - 0.9595

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9593

Kijun-Sen level : 0.9581

Ichimoku cloud top : 0.9600

Ichimoku cloud bottom : 0.9571

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

Dollar’s recovery after falling to 0.9552 last week suggests minor consolidation would be seen and corrective bounce to 0.9620-25 (38.2% Fibonacci retracement of 0.9738-0.9552) is likely, however, reckon resistance at 0.9647 would limit upside and bring another decline later, below said support would signal recent decline from 0.9771 top is still in progress, hence further weakness to 0.9545-49 (2 times extension of 0.9771-0.9676 measuring from 0.9738) would follow but reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on recovery as resistance at 0.9647 should limit upside. Only above previous support at 0.9676 (now resistance) would defer and suggest a temporary low is formed, risk test of another previous support at 0.9692.

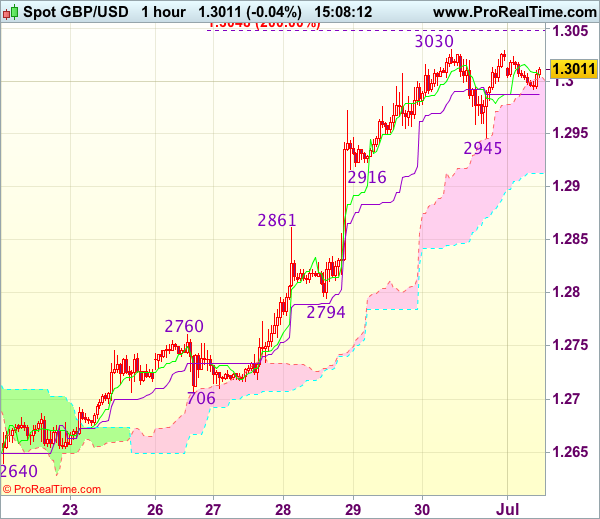

Trade Idea : GBP/USD – Buy at 1.2920

GBP/USD - 1.3013

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3008

Kijun-Sen level : 1.2987

Ichimoku cloud top : 1.3003

Ichimoku cloud bottom : 1.2912

Original strategy :

Buy at 1.2920, Target: 1.3020, Stop: 1.2885

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2920, Target: 1.3020, Stop: 1.2885

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after last week’s rally, adding credence to our bullish view that recent upmove is still in progress and may extend further gain towards recent high 1.3048, however, loss of near term upward momentum should prevent sharp move beyond 1.3075-80 today and reckon 1.3100 would hold on first testing, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy cable again on pullback as support at 1.2916 should limit downside and bring another rally. Below 1.2890-95 would defer and risk test of previous resistance at 1.2861, break there would suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

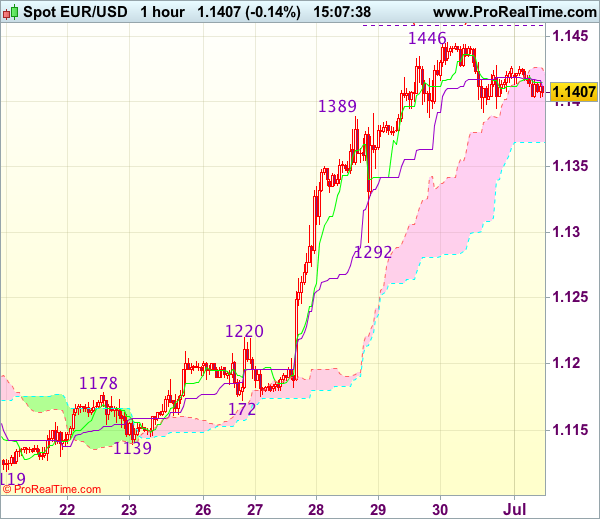

Trade Idea : EUR/USD – Buy at 1.1330

EUR/USD - 1.1405

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1413

Kijun-Sen level : 1.1411

Ichimoku cloud top : 1.1425

Ichimoku cloud bottom : 1.1369

Original strategy :

Buy at 1.1350, Target: 1.1450, Stop: 1.1315

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1330, Target: 1.1440, Stop: 1.1295

Position : -

Target : -

Stop : -

As the single currency met resistance at 1.1446 late last week and has eased, suggesting consolidation below this level would be seen and pullback to the lower Kumo (now at 1.1369) cannot be ruled out, however, reckon 1.1325-30 (38.2% Fibonacci retracement of 1.1139-1.1446) would limit downside and bring another rise later, above said resistance at 1.1446 would extend recent rise to 1.1455-60 (61.8% projection of 1.1119-1.1389 measuring from 1.1292), then 1.1480 but overbought condition should prevent sharp move beyond 1.1500, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1325-30 should limit upside. Below 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446) would abort and signal a temporary top is formed, bring correction to 1.1255-60 later.