Sample Category Title

Week Ahead Dollar Weaker After Hawkish Comments From Central Banks

US jobs report and Fed minutes to guide markets

The US dollar is lower against most majors amid hawkish rhetoric from central banks and improving economic conditions around the globe. The U.S. Federal Reserve has raised interest rates twice in 2017 and continues to hint at more tightening measures before the end of the year. American fundamentals have been mixed and the rising concerns about the Trump administration's ability to get to pass pro-growth policies are weighing on the dollar despite the efforts of the central bank.

The Fourth of July holiday in the United States will make an already packed economic calendar even more compressed. The notes from the Federal Open Market Committee (FOMC) meeting in June will be released on Wednesday, July 5 at 2:00 pm EDT. Employment data out of the US will start pouring in on Thursday with the release of the ADP private payrolls report at 8:15 am EDT and the weekly Unemployment claims. The main event will be the release of the U.S. non farm payrolls (NFP) report on Friday, July 7 at 8:30 am EDT with investors looking for signs of inflation in the wages component to reaffirm the Fed's hawkish view.

The EUR/USD gained 1.859 percent in the last five trading days. The single currency is higher against the USD as central bank rhetoric from the Bank of Canada (BoC), the Bank of England (BoE) and the European Central Bank (ECB) came in too close to each other and are signalling an end to low rates. The Fed has done its part with two rate hikes this year and a balance sheet reduction plan expected to kick off in the fourth quarter, but political risk in the US has impaired the dollar with uncertainty on major policies being introduced as promised after the presidential elections.

The European Central Bank (ECB) Forum in Portugal served as the perfect stage for the central bank to join the Bank of Canada and the Bank of England in their hawkish views as it appears the Fed will not be alone in tightening monetary policy in the coming months.

Employment data out of the US next week will be pivotal for the direction of the USD if there is significant improvement in wage growth. The US has posted solid job gains, but the quality of those positions is being questioned, in order to make a dent in the market perception the inflation signals have to be strong to further validate the current rate hike path of the central bank.

The USD/CAD lost 2.213 in the last five days. The currency pair is trading at 1.2966 as economic indicators and hawkish rhetoric has boosted the loonie while the political uncertainty in the US has impacted the US dollar. The pair has decisively broken through the 1.30 price level and the loonie rally will keep going as the market heads into next week's US employment data on a short trading week due to the Fourth of July holiday.

The Fed will release the notes from its latest Federal Open Market Committee (FOMC). The US central bank hiked rates by 25 basis points as expected but with inflation remaining low and some obvious dissenters like Minnesota's Fed Kashkari it will be insightful to learn what form the debate took shape as it helps forecasters model the upcoming decisions from the central bank regarding rates and the reduction of the balance sheet which seems to be a more agreeable subject amongst policy makers.

Canadian economic output rose in April by 0.2 percent as expected. On a yearly basis the economy is growing at a 3.3 percent rate, the biggest gain since 2014. Services are leading the way with an improvement in commodities and a slowdown in manufacturing the major highlights. Next week CAD traders will be tracking the release of the Canadian Trade Balance on Thursday, July 6 at 8:30 am EDT and the employment report on Friday, July 7 at 8:30 am EDT for guidance on the path of the loonie.

Oil gained 7.114 on the last week. The price of West Texas Intermediate is trading at $45.11 amid some financial institutions are buying at what they think is the bottom. Citibank is calling for a rebound of crude after two weeks were oil inventories have been subdued. There has not been any evidence of improvement in demand and the tug of war between the Organization of the Petroleum Exporting Countries (OPEC) and the US shale producers will continue to keep the black stuff trading in a range as data supports one side over the other.

Goldman Sachs was less bullish and issued a note reducing the oil prices forecast for next quarter after Nigeria and Libya productions ended their disruptions and continue to be exempt from the OPEC oil cut agreement. GS is pointing to a $47.50 price per barrel of WTI, which was a significant downgrade from the previous $55 price level.

Crude has advanced 6.2 percent in the last week as the downward pressure due to the oversupply concerns has eased. OPEC members will meet with other producers in Russia to discuss the next steps to stabilize energy prices after they have already agreed to extend the crude production cut until March of 2018. Maintenance and disruptions due to a storm in the Gulf of Mexico reduced the level of US inventories and gave oil a chance to record its best rally of the year and yet prices will be net negative in June. The start of the driving season in the US has not been too favourable for crude addressing the biggest issue yet to be tackled by producers, the apparent lack of demand worldwide.

Market events to watch this week:

Sunday, July 2

- 9:45 pm CNY Caixin Manufacturing PMI

Monday, July 3

- 4:30 am GBP Manufacturing PMI

- 10:00 am USD ISM Manufacturing PMI

- 9:30 pm AUD Retail Sales m/m

Tuesday, July 4

- 12:30 am AUD RBA Rate Statement

- 4:30 am GBP Construction PMI

- Tentative GBP Inflation Report Hearings

Wednesday, July 5

- 4:30 am GBP Services PMI

- 2:00 pm USD FOMC Meeting Minutes

- 9:30 pm AUD Trade Balance

Thursday, July 6

- 8:15 am USD ADP Non-Farm Employment Change

- 8:30 am CAD Trade Balance

- 8:30 am USD Unemployment Claims

- 10:00 am USD ISM Non-Manufacturing PMI

- 11:30 am USD Crude Oil Inventories

Friday, July 7

- 4:30 am GBP Manufacturing Production m/m

- 8:30 am CAD Employment Change

- 8:30 am CAD Unemployment Rate

- 8:30 am USD Average Hourly Earnings m/m

- 8:30 am USD Non-Farm Employment Change

*All times EDT

Q2 Business Outlook Survey Confirms Firming Canadian Economy

Highlights:

- Expected future sales and employment intentions both rose sharply. Investment intentions ticked lower but from elevated Q1 levels and with a more optimistic tone to the accompanying commentary.

- Indicators of capacity pressures rose sharply. The share of businesses reporting difficulty meeting demand rose to its highest since Q2/2015.

- Most respondents expect inflation in the Bank of Canada's 1-3% target range although with an increase in those expecting something in the bottom-half of that range.

Our Take:

The Bank of Canada's Q2 Business Outlook Survey showed improved Canadian business optimism once again in Q2 and will reinforce now widely-held expectations that the Bank of Canada could hike interest rates as soon as the July 12th policy announcement. Expected future sales growth and hiring intentions both rose with the latter easily hitting a record high. Investment intentions dipped but from a very high Q1 reading that matched the second-highest on record. Comments from the bank - which often reflect underlying details not reported in the 'standard' data release - suggested that firms have, encouragingly, "become more focused on expanding capacity to accommodate stronger demand." Consistent with the need to expand capacity, the share of businesses reporting difficulties meeting demand rose sharply as did the reported intensity of labour shortages.

A report from Bank of Canada researchers earlier this week argued that 'soft' indicators like the BOS have been a better predictor of official monetary policy decisions than 'hard' indicators, like GDP growth. Even that distinction, though, is becoming increasingly unnecessary given another strong April GDP report this morning. Thus, both 'soft' and 'hard' data increasingly argue that the current extremely low level of interest rates is no longer needed to support the economy.

Canadian Dollar Higher After Steady Growth And Central Bank Survey

The Canadian dollar continued to rally versus the US dollar after the release of the gross domestic product (GDP) earlier today showed a monthly gain of 0.2 percent in line with expectations. The USD/CAD lost 0.29 percent in the last 24 hours as the loonie advanced against its US counterpart after the positive GDP and Bank of Canada (BoC) business survey validate the hawkish rhetoric launched two weeks ago that has put a rate hike firmly on the table. Senior monetary policy members have said that the rate cuts from 2015 have done their job and the central bank could be ready to remove some stimulus. The market was taken by surprise by the change of tune, and is now pricing in a 70 percent chance of an interest rate hike in July.

The USD is having the worst quarter since 2010 despite the hawkish rhetoric from the U.S. Federal Reserve. Political uncertainty in the White House and a divisive healthcare reform delayed to after the Fourth of July Senate recess have put downward pressure on the dollar. The Fed does not have a monopoly on optimism as other central bank have joined the chorus as economic growth has improved in Canada, the United Kingdom and Europe. Central bankers are pointing to an end of stimulus, but with little details or actions as of yet. The Fed remains the most proactive central bank with four 25 basis points rate hikes (two this year) and the end of its quantitative easing program. the next step is the reduction of its massive balance sheet which could happen before the end of the year.

The Bank of Canada is a special case as the European Central Bank (ECB) and the Bank of England (BoE) have quantitive easing programs that will have to be gradually wound down whereas Stephen Poloz can jump on the rate hike bandwagon with relative speed. The BoC governor also does not have to worry about a vote as there is no monetary policy committee.

The timing of the first rate hike will be challenging. The three factors driving the loonie will have to be taken into consideration. Oil prices have been stable but the showdown between the US shale producers and the OPEC output deal nations is not addressing the tepid demand for energy around the world. Nafta renegotiations starting in August could change the economic landscape for Canada and that is something the central bank will have to address. The third factor is the Fed itself. The American economy has been softer in 2017 raising questions about what impact a third rate hike and a lower Fed balance sheet could have in the second half of the year.

The USD/CAD lost 0.379 in the last 24 hours. The currency pair is trading at 1.2966 as economic indicators and hawkish rhetoric has boosted the loonie while the political uncertainty in the US has impacted the US dollar. The pair has decisively broken through the 1.30 price level and the loonie rally will keep going as the market heads into next week's US employment data on a short trading week due to the Fourth of July holiday.

The Fed will release the notes from its latest Federal Open Market Committee (FOMC). The US central bank hiked rates by 25 basis points as expected but with inflation remaining low and some obvious dissenters like Minnesota's Fed Kashkari it will be insightful to learn what form the debate took shape as it helps forecasters model the upcoming decisions from the central bank regarding rates and the reduction of the balance sheet which seems to be a more agreeable subject amongst policy makers.

Canadian economic output rose in April by 0.2 percent as expected. On a yearly basis the economy is growing at a 3.3 percent rate, the biggest gain since 2014. Services are leading the way with an improvement in commodities and a slowdown in manufacturing the major highlights. Next week CAD traders will be tracking the release of the Canadian Trade Balance on Thursday, July 6 at 8:30 am EDT and the employment report on Friday, July 7 at 8:30 am EDT for guidance on the path of the loonie.

Oil gained 0.372 on Friday. The price of West Texas Intermediate is trading at $45.11 amid some financial institutions are buying at what they think is the bottom. Citibank is calling for a rebound of crude after two weeks were oil inventories have been subdued. There has not been any evidence of improvement in demand and the tug of war between the Organization of the Petroleum Exporting Countries (OPEC) and the US shale producers will continue to keep the black stuff trading in a range as data supports one side over the other.

Goldman Sachs was less bullish and issued a note reducing the oil prices forecast for next quarter after Nigeria and Libya productions ended their disruptions and continue to be exempt from the OPEC oil cut agreement. GS is pointing to a $47.50 price per barrel of WTI, which was a significant downgrade from the previous $55 price level.

Crude has advanced 6.2 percent in the last week as the downward pressure due to the oversupply concerns has eased. OPEC members will meet with other producers in Russia to discuss the next steps to stabilize energy prices after they have already agreed to extend the crude production cut until March of 2018. Maintenance and disruptions due to a storm in the Gulf of Mexico reduced the level of US inventories and gave oil a chance to record its best rally of the year and yet prices will be net negative in June. The start of the driving season in the US has not been too favourable for crude addressing the biggest issue yet to be tackled by producers, the apparent lack of demand worldwide.

Market events to watch this week:o

Sunday, July 2

- 9:45 pm CNY Caixin Manufacturing PMI

Monday, July 3

- 4:30 am GBP Manufacturing PMI

- 10:00 am USD ISM Manufacturing PMI

- 9:30 pm AUD Retail Sales m/m

Tuesday, July 4

- 12:30 am AUD RBA Rate Statement

- 4:30 am GBP Construction PMI

- Tentative GBP Inflation Report Hearings

Wednesday, July 5

- 4:30 am GBP Services PMI

- 2:00 pm USD FOMC Meeting Minutes

- 9:30 pm AUD Trade Balance

Thursday, July 6

- 8:15 am USD ADP Non-Farm Employment Change

- 8:30 am CAD Trade Balance

- 8:30 am USD Unemployment Claims

- 10:00 am USD ISM Non-Manufacturing PMI

- 11:30 am USD Crude Oil Inventories

Friday, July 7

- 4:30 am GBP Manufacturing Production m/m

- 8:30 am CAD Employment Change

- 8:30 am CAD Unemployment Rate

- 8:30 am USD Average Hourly Earnings m/m

- 8:30 am USD Non-Farm Employment Change

*All times EDT

RBA & Riksbank Meetings, US Jobs Report & FOMC Minutes, Other Key Data in Focus

Next week's market movers

- In Australia, the RBA is expected to keep its policy unchanged. In light of recent encouraging developments in the economy, we see the case for a more upbeat message by policymakers.

- Sweden's Riksbank is also likely to stand pat. We expect officials to shift to a more optimistic bias, following in the footsteps of the Norges Bank and the ECB.

- In the US, employment data for June and the minutes from the latest FOMC meeting will keep investors busy.

- We also get key economic data from Japan, the UK, the US, and Canada.

On Monday, during the Asian morning, the Bank of Japan will release its Tankan business confidence survey for Q2. The forecast is for all of the survey's indices to have risen, something supported by the Reuters Tankan Diffusion Index, which rose notably from the previous quarter on average. An increase in all of these prints would signal that both large and small Japanese firms are feeling more optimistic about current conditions as well as their future outlook. We expect Japanese equity markets to benefit from such an upbeat report, as it could be a signal that GDP growth is set to pick up more steam moving forward. Turning to monetary policy, such strong Tankan prints could add fuel to recent speculation that the BoJ may begin to communicate a plan for its eventual exit from QQE. However, as inflationary pressures remain subdued in Japan, we maintain our view that the Bank is unlikely to alter its current QQE framework any time soon.

In the US, the ISM manufacturing PMI for June is expected to have ticked up. However, taking a look at the preliminary Markit manufacturing PMI for the month, we believe that the risks surrounding the ISM index are tilted to the downside. The Markit index slid to 52.1 from 52.7 in May, pointing to the slowest improvement in overall business conditions since September 2016.

From the UK, we get the manufacturing PMI for June. Then on Tuesday we get the construction index for the same month and subsequently on Wednesday, the service-sector print. The forecast is for all of these indices to have declined. Should these prints show that the UK ended Q2 on a soft footing, and that economic growth may have slowed further, that would likely pour some cold water on market expectations regarding a BoE rate hike at one of the upcoming meetings.

Turning to the political spectrum, Monday marks the end of the 10-day deadline given to Qatar to comply with a list of 13 demands issued by Saudi Arabia, the UAE, Bahrain and Egypt. Qatar is required to shut down the Turkish military base in the country, shut down the Al-Jazeera news network, curb diplomatic ties with Iran, sever all ties to "terrorist organizations", pay reparations for damages caused by Qatari policies in recent years, and more. If Qatar agrees to comply, the four Arab nations will lift the sanctions they imposed earlier in June. However, it is not clear what happens if Qatar fails to meet these demands. In the optimistic scenario, the four Arab nations could simply keep their sanctions in place, which is likely to have little market impact. This is supported by recent comments from the UAE Foreign Minister, who said that "the alternative is not escalation, the alternative is parting of ways". In the unlikely event that the situation does escalate though, investors' risk appetite may be impacted, with safe haven assets likely to be the main beneficiary. Oil prices could gain in the short-term as well, as the risk of supply disruptions would likely increase.

Markets will stay closed in Canada in Celebration of Canada Day, and will close early in the US ahead of Independence Day.

On Tuesday, during the Asian day, the RBA will announce its rate decision and the forecast is for no change in policy. In recent gatherings, officials maintained a neutral tone overall, but appeared somewhat worried with regards to the labor and housing markets, indicating that developments in these two sectors warrant careful monitoring. The two most recent employment reports from Australia have been stellar, while the house price inflation has begun to cool according to the latest Residential Property Index. As such, we think that policymakers are likely to tone down their concerns at this meeting. Having said that though, we don't expect any dramatic shift in rhetoric, but rather a slightly more upbeat tone, as the RBA will probably want to examine more than a couple of months' worth of data before making material changes to its bias.

During the European day, the Riksbank will announce its own policy decision. Without a forecast available, we see the case for the world's oldest central bank to remain on hold. At its latest gathering back in April, the Riksbank extended the duration of its QE program by 6 months to December 2017 and pushed somewhat further out the timing for its first planned rate hike. The tone of the meeting statement was quite cautious, indicating that it will take longer before inflation stabilizes around 2%, and citing considerable uncertainty over political developments abroad. A few weeks after that meeting, the Bank announced plans to move away from its strict 2% inflation target and to introduce a target range of ±1% from 2%. This implies that policymakers may be more tolerant of subdued inflation, which reduces the likelihood for any further easing measures. What's more, European political risks have dissipated notably following the French election, something that could be reflected in the meeting statement. The combination of these factors makes us believe that the Bank is likely to appear more optimistic this time. In fact, we would not rule out the prospect that the Riksbank follows in the recent footsteps of the Norges Bank and the ECB, by also removing its interest rate easing bias.

Markets will remain closed in the US for Independence Day.

On Wednesday, the Fed releases the minutes of its June policy gathering, where the Committee raised the Federal funds rate by 25bps. In the statement accompanying the decision, Fed officials noted that they expect to begin normalizing the Bank's balance sheet later this year in a slow and predictable manner. Meanwhile, they kept the "dot plot" largely unchanged, signaling that one more rate hike is on the cards for this year. In our view, market participants will dig into the minutes for more details on the timing of the balance sheet normalization, as well as any discussion with regards to the timing of the next rate increase. At the time of writing, the market is anticipating the next hike to come in May 2018. This shows that the dot plot has not convinced the financial community, which may need stronger hints before it prices in another hike for 2017.

Our own view is that the Fed will indeed proceed with another hike this year. The Committee has repeatedly pointed out that the softness in the economic data for Q1 is transitory. Indeed, the Atlanta Fed GDPNow model adds credibility to that scenario by indicating that GDP growth rebounded to 2.9% in Q2, while the June employment report is expected to show that the labor market continues to tighten. The key risks to our view are a second quarter of soft GDP and/or further slowdown in the nation's core inflation.

On Thursday, from the US, we get the ADP employment report for June and the ISM non-manufacturing index for the same month. Getting the ball rolling with the ADP report, the forecast is for the private sector to have added 178k, much less than the 253k print in May. Nevertheless, this would still be a decent print and if met, it may increase speculation that Friday's NFP will also meet its forecast of 183k. Nonetheless, we have to sound a note of caution. Even though this is the only major gauge of the NFP, the correlation the two numbers has fallen notably during the last few months.

Now, let's pass the torch to the ISM index. Expectations are for the index to have slid somewhat, but to have remained well above the 50 mark that separates expansion from contraction. The case for a decline in the ISM index is supported by a similar move in the Markit services index for the month, which signaled the slowest upturn in service sector output since March.

On Friday, all eyes will be on the US employment report for June. The forecast is for nonfarm payrolls to have risen by 183k, more than the 138k in May. The unemployment rate is expected to have remained unchanged at 4.3%, while average hourly earnings are expected to have accelerated in monthly terms. Overall, this would be another employment report consistent with further tightening in the labor market, which will be pleasant news for FOMC policymakers. The financial world is currently anticipating the next increase in the Federal funds rate to come in May 2018, while the Fed's "dot plot" points to such a move coming by the end of this year. Therefore, if the June jobs report is indeed as robust as expected, it could confirm the Fed's view that the recent softness in economic data is transitory and could bring forth market expectations with regards to the next hike. Having said that though, we believe that the economic indicators that will play the biggest role on the timing of the next move are the nation's CPIs. Following three months of declining inflation rates, a decent rebound is needed to materially increase the probability for a hike this year.

We also get employment data for June from Canada, though no forecast is yet available. Neither the Markit nor the Ivey PMIs for the month have been released yet, implying that we do not have any gauges of how the labor market fared in June. In any case, these data will be closely tracked amid recent signals from BoC policymakers that a tightening move may be on the cards soon. Another month of solid employment gains could add fuel to such speculation. Having said that, even though the BoC may indeed appear more hawkish soon, we doubt that an actual rate hike is looming. We would need to see a significant pickup in the nation's core CPI rate that has declined for 3 consecutive months now before we join those who are calling for an immediate rate increase.

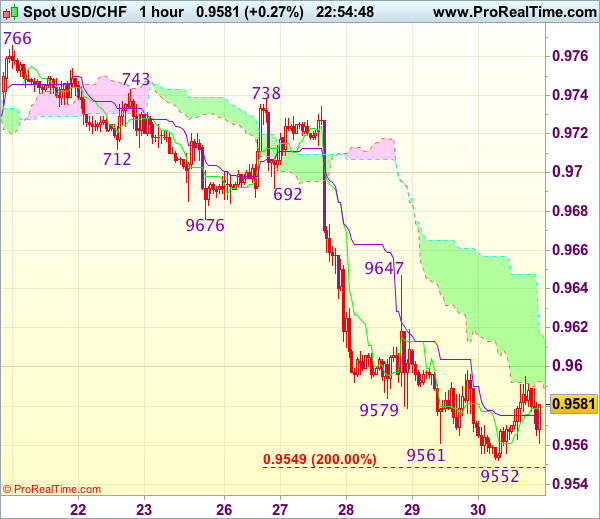

Trade Idea Wrap-up: USD/CHF – Sell at 0.9645

USD/CHF - 0.9572

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9578

Kijun-Sen level : 0.9574

Ichimoku cloud top : 0.9617

Ichimoku cloud bottom : 0.9593

Original strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

As the greenback has recovered after marginal fall to 0.9552, suggesting minor consolidation would be seen and recovery to 0.9600-10 is likely, however, reckon resistance at 0.9647 would limit upside and bring another decline later, below said support would signal recent decline from 0.9771 top is still in progress, hence further weakness to 0.9545-49 (2 times extension of 0.9771-0.9676 measuring from 0.9738) would follow but reckon downside would be limited to 0.9525-30 (50% projection of 1.10100-0.9613 measuring from 0.9771) and 0.9500 should hold, price should stay above 0.9470 (61.8% projection), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on recovery as resistance at 0.9647 should limit upside. Only above previous support at 0.9676 (now resistance) would defer and suggest a temporary low is formed, risk test of another previous support at 0.9692.

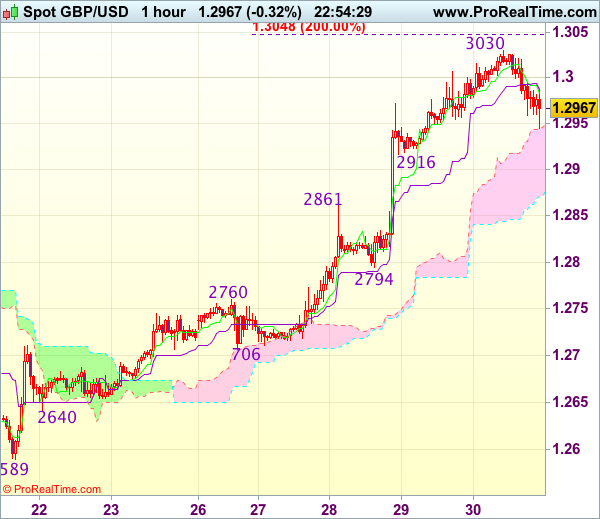

Trade Idea Wrap-up: GBP/USD – Buy at 1.2920

GBP/USD - 1.2978

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2983

Kijun-Sen level : 1.2988

Ichimoku cloud top : 1.2946

Ichimoku cloud bottom : 1.2871

Original strategy :

Buy at 1.2920, Target: 1.3020, Stop: 1.2885

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2920, Target: 1.3020, Stop: 1.2885

Position : -

Target : -

Stop : -

As cable has continued trading with a firm undertone after this week’s rally, adding credence to our bullish view that recent upmove is still in progress and may extend further gain towards recent high 1.3048, however, loss of near term upward momentum should prevent sharp move beyond 1.3075-80 today and reckon 1.4100 would hold on first testing, risk from there has increased for a retreat to take place later.

In view of this, we are looking to buy cable again on pullback as support at 1.2916 should limit downside and bring another rally. Below 1.2890-95 would defer and risk test of previous resistance at 1.2861, break there would suggest a temporary top is formed instead, risk weakness to 1.2830-35 but support at 1.2794 should remain intact.

Trump Target Of 3% Growth Looks Less Unattainable

- Watch for a RBI Hawkish Cut - Peter Rosenstreich

- Oil Outlook Remains Clouded - Arnaud Masset

- Trump Target Of 3% Growth Looks Less Unattainable - Yann Quelenn

- Time For A Recovery In Oil Prices?

Economics - Watch For A RBI Hawkish Cut

This month we have seen a bunch on central banks unexpectedly shift towards an unexpectedly hawkish strategy. Yet despite this U-turn we suspect rates rises will be slow with reduction in balance sheet over interest rates to be the primary tool for tightening. A current exception judging from market expectations is the Reserve Bank of India. Next week's RBI rate decision is likely to bring a 25bp policy rate cut. However, given the uncertainty around determining if the slowdown has been generating by cyclical issues or government interventions should probably delay any central bank action. It remains difficult to determine if India current weakness in growth and inflation is only the result of demonetization or application of the goods and services tax (GST). Currently inflation in India remains soft, due to a mix of transitory and structural factors, driving politicians to overlook potential of midterm higher inflation prices, for short-term growth gains. CPI inflation has dropped quickly, to 2.2% in May from 5.0% in 2016. RBI cut is likely to be a one off before shifting back to a tightening stance as we suspect inflation will pick up in 2H.

Leading economic indicators are signaling that economic activity is improving; led by consumer demand. The consumer already boosted by GDP growth above 6.0% is also support by loose credit conditions and improving external demand. Disruptions cause by demonetizations are still filtering through the system effecting consumer spending and slowing inflation, distorting recent readings. Yet strong rural wage growth and state government pay increases will kick in and drive growth and inflation higher. We could envision growth heading toward 7.5% by the years end.

In broader terms, the external environment remains supportive for EM currencies. Despite some talk of central bank "normalization", global interest rates remain subdued forcing investors to search for yields.

In addition incoming data such as China PMI show that trade demand remains solid supporting our EM story. We remain bullish on the INR heading into the RBI rate decision.

Economics - Oil Outlook Remains Clouded

Crude oil prices struggled to recover from the sharp sell-off that has sent a barrel of West Texas Intermediate to $42.05 a couple of weeks ago, down almost 20% from its peak of May 25th. However, since June 21, the WTI was able to recover marginally thanks to a weaker US dollar and reassessment of the fundamentals by investors. From a technical standpoint, the WTI's sell-off has been stopped by the key support at around $42 (multi lows) and is currently retracing toward the $46.00-50 resistance area (Fibo 38.2% on April-June sell-off and previous highs).

Overall, it seems that investors are negatively skewed about the oil outlook as even the recent political turmoil in the Middle East - several countries cut their diplomatic ties with Qatar, a major oil and gas producer in the region - was unable to stop the debasement in crude oil prices. In addition, the sustained contraction in US crude inventories seems to have no effect either. Despite a marginal increase last week (+118k barrels), US stockpiles (excluding strategy reserves) have been decreasing continuously since the end of March this year, sliding from 535mio barrels to 509mio as of June 23rd.

Market participants have lost faith in OPEC's ability to drive prices as several of its members (mostly Iraq) failed to comply with the deal and did not cut production sufficiently. In addition, Iran declared it had increased the capacity of its main oil terminal, which tends to indicate that the world's fifth largest oil producer is willing to inch up production. Finally, according to the EIA, the US had more than doubled its exports of crude oil and petroleum products over the last six years as exports restrictions were lifted. Furthermore, the US shale industry continues to optimise production and cut costs.

On the medium to long-term we remain cautious on the oil outlook as the fundamentals do not support upside gains. However, in the shortterm, crude oil prices have room to recover somewhat, thanks to a weak dollar and the end of the panic selling. We expect crude oil to return gradually toward the $50 threshold as fears ease.

Economics - Trump Target Of 3% Growth Looks Less Unattainable

Last Monday, no less than four Fed members have provided their views on monetary policy including Janet Yellen whose speech was in London on global economic issues.

Financial markets tried to grab some hints regarding the Fed's path towards normalisation of monetary policy. Markets currently estimate the likelihood of a third rate hike this year below 50%.

We believe the Fed will be very focused on economic data rather than geopolitical development and we consider that recent economic data is not fully supporting a continued normalisation of the economy.

Fed members looked concerned by the level of equities. San Francisco Fed President John Williams declared that the stock market is "running on fumes" while Janet Yellen said that current stock valuation levels are "rich". Both declarations have been made at separate moments and it is clear the Fed underpinned stocks overvaluation.

Earlier last week, non-defense capital goods recorded their highest decline since last December at -0.2% m/m below consensus 0.1 m/m. US Manufacturing PMI came in below expectations at 52.1 vs 52.7 expected. We recall that a level above 50 indicates expansion and we are slowly approaching towards this threshold.

The US GDP came in surprisingly higher than markets estimates despite data for the second quarter is significantly weaker than what has been released during the first quarter. Nonetheless, we believe there are still clear downside risks on the greenback at the moment. Therefore, the EURUSD pair may continue to bounce higher in the short-term.

We also consider that there is other supporting evidence that shows concerns regarding the US growth future. US auto sales have constantly weakened from 18.29 million sales in December 2016 towards 16.58 vehicles sales in May 2017, and this trend illustrates a negative sentiment on the North American economy from consumers. We believe that fundamentals are still soft and we consider the US recovery to be overestimated at the moment.

One explanation is that despite labour data being positive, wage growth remains subdued and this is certainly preventing consumers buying new cars or at least it is making them postpone their purchases. It is definitely not a great sign for the US economy in our view.

On top of that, the IMF in a report has slashed its GDP forecast for yearend by removing the effect of President Trump's fiscal stimulus. Indeed, it looks more and more uncertain that this fiscal plan will ever be implemented at this point. The IMF forecast for US GDP is now 2.1% from 2.3% in April. As a result the Trump target of 3% growth looks less and less unattainable.

As we stated above, there is room for further weakness for the greenback. The Eurodollar pair, which has strengthened out of Draghi's comments, should continue heading higher on markets pricing back in US economic difficulties.

Themes Trading - Time For A Recovery In Oil Prices?

Cuts in crude oil production and growing demand indicate that crude prices should continue to grind higher in 2017. In an unexpected move, OPEC silenced skeptics by orchestrating the first production cut in eight years between OPEC and non-OPEC countries. The agreement sent crude prices soaring. After four years of depressed crude prices as a result of a global supply glut, the group's three largest producers - Saudi Arabia, Iraq and Iran - overcame significant disagreement to move to reduce global oil inventories. The agreement was unprecedented, with Russia and Mexico also joining in to cut output.

While this historic agreement will only begin to address the supply equilibrium, the steady improvement in demand will be the primary driver of higher oil prices in 2017. Steady oil consumption remains constant even during weak economic conditions as the world's consumers demand 95 million barrels of oil a day, up from 86 million in 2008. However, global demand continues to recover, with growth in the USA, Europe and China. Despite efforts for cleaner energy, oil remains the world's primary fuel, driving globalization.

As oil market dynamics continued to tighten, certain companies are better positioned to take advantage of improving oil prices. This Oil Recovery theme is designed to exploit rising prices by selecting companies mostly active in the upstream segment, which would benefit the most from a barrel above $60. To enhance risk diversification, the portfolio is structured using an equally-weighted risk contribution approach. In summary, this means the allocation is calculated in such a way that each stock contributes on an equal basis to the portfolio's total risk.

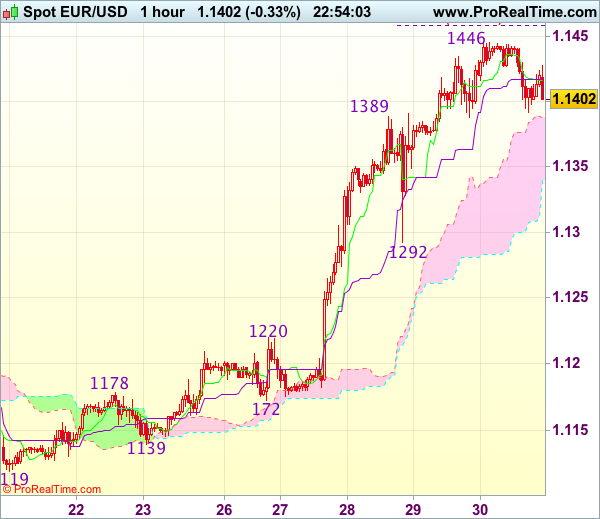

Trade Idea Wrap-up: EUR/USD – Buy at 1.1350

EUR/USD - 1.1412

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1411

Kijun-Sen level : 1.1419

Ichimoku cloud top : 1.1388

Ichimoku cloud bottom : 1.1341

Original strategy :

Buy at 1.1350, Target: 1.1450, Stop: 1.1315

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1350, Target: 1.1450, Stop: 1.1315

Position : -

Target : -

Stop : -

As the single currency has maintained a firm undertone after recent rally, adding credence to our bullish view that recent rise is still in progress and may extend further gain to 1.1455-60 (61.8% projection of 1.1119-1.1389 measuring from 1.1292), then 1.1480, however, overbought condition should prevent sharp move beyond 1.1500, risk from there has increased for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1350-55 should limit upside. Below 1.1315-20 would defer but only break of indicated support at 1.1292 would signal a temporary top is formed, bring correction to 1.1255-60 later.

Trade Idea Wrap-up: USD/JPY – Sell at 112.60

USD/JPY - 112.33

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.09

Kijun-Sen level : 112.33

Ichimoku cloud top : 112.45

Ichimoku cloud bottom : 112.22

Original strategy :

Sell at 112.40, Target: 111.40, Stop: 112.75

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.60, Target: 111.60, Stop: 112.95

Position : -

Target : -

Stop : -

Although the greenback rose to as high as 112.93 yesterday, the subsequent sharp retreat signals top has been formed there and consolidation with downside bias is seen for weakness to 111.46 support, a firm break below there would add credence to this view, brig further fall towards 111.15-20 but support at 110.95 should remain intact, bring rebound later.

In view of this, we are looking to sell dollar on recovery as 112.60-65 should limit upside and bring another decline. Above said resistance at 112.93 is needed to abort and confirm recent upmove has resumed for headway to 113.15-20.

Dollar On Course for Worst Quarter in 7 Years; Loonie at 10-Month High

Today's European session was a rather busy one in terms of data releases. Final UK figures on first quarter economic growth confirmed economic activity slowing down in the nation, while inflation figures out of the eurozone surprised to the upside but failed to boost the euro. Out of the US, consumer spending and the reading for the core PCE index were among the releases attracting attention.

US consumer spending recorded a slight increase in May, rising by 0.1% month-on-month, in line with expectations but falling short of the previous month's 0.4%. Consumption makes up for close to 70% of the US economy. In other US data, the May core PCE price index rose by 0.1% on a monthly basis. Analyst forecasts and April's respective figure also stood at 0.1%. The number for April was the result of a downward revision from 0.2%. The dollar edged higher relative to the yen upon data release, eventually reaching a daily high of 112.24. The pair was last flat at 112.17.

Later in the day, the final reading of the University of Michigan consumer sentiment index for the month of June was released at 95.1. This was above the 94.5 expected but at its lowest since November of last year. Dollar/yen fell on the news.

Looking at the dollar index, which gauges the greenback against the currencies of six major US trading partners, it was last up on the margin after hitting a fresh nine-month low of 95.47 earlier in the day. The measure, which is down 4.8% over the quarter, is on track for its worst quarter in seven years.

In other news, the final figures for first quarter UK GDP were released today. Those showed the economy expanding by a meager 0.2% quarter-on-quarter. This was in line with projections and below the previous quarter's 0.7%. On an annual basis, the economy expanded by 2.0% as expected and slightly above the previous quarter's respective number at 1.9%. It is worrisome that UK consumers' purchasing power is continuing to receive a blow as a result of the weakening sterling since last year's Brexit referendum. Their spending power has contracted the most since the 1970s. If this is combined with the loss in confidence due to political uncertainty, the outlook looks even bleaker. Pound/dollar was on a declining path even before the data hit the markets but extended its fall after the numbers became public. The pair reached a low of 1.2958 during the European session while it last traded 0.2% down on the day.

In terms of data out of the eurozone, the June flash inflation numbers showed the inflation rate at 1.3% year-on-year, exceeding forecasts of 1.2% but slightly below May's 1.4%. Core inflation, which excludes volatile food and energy items, stood at 1.2%, up from May's 1.0% which also coincided with analysts' projections. Headline inflation close to but below 2.0% is the European Central Bank's target for inflation. Euro/dollar did not move much upon data release. The pair last traded above the 1.14 handle, 0.2% down on the day after advancing for three consecutive days.

Turning to Canada, the country saw the release of GDP data for April. Month-on-month, the Canadian economy grew by 0.2%, coinciding with expectations but below March's 0.5%. This marks the sixth straight month of growth for the country and points to a strong start during the second quarter of the year given widespread sector growth. Versus the dollar, the loonie gained upon data release. Today it was lifted by higher oil prices as well, as Canada is a major oil exporter. Dollar/loonie looks set for its fifth straight day of declines after hitting a near ten-month low of 1.2946 earlier in the day.

Diverting from forex markets for a peek at commodities, gold was last close to being flat on the day, trading at $1244.45 an ounce. WTI and Brent crude were up 0.8% and 0.5% on the day, trading at $45.28 and 47.66 a barrel respectively.