Sample Category Title

Loonie Suffers on Inflation; Dollar Down; Sterling Maintains Positive Momentum

Among the highlights in today's European session were flash Markit PMI estimates out of the eurozone and the US, Canadian inflation figures and US new home sales data. Beyond economic releases, the pound maintained yesterday's momentum on rising expectations of a rate hike by the Bank of England.

Flash eurozone PMI numbers for the month of June showed the manufacturing sector performing strongly and the services sector surprising to the downside. Specifically, the manufacturing PMI number came in at the more than six-year high of 57.3, exceeding forecasts for a reading of 56.8 and May's 57.0. The respective figure for the services sector stood at 54.7, the lowest since February of this year and below the 56.2 projected by analysts as well as the 56.3 from the previous month. The composite PMI, which blends the two sectors, also fell to its lowest since February, reaching 55.7 and failing to meet expectations for a reading of 56.5 and May's 56.8.

Despite the not so strong composite and services readings, overall the numbers are suggesting that the euro area growth rate would reach 0.7% quarter-on-quarter during the second quarter of the year, its highest since 2015. The euro posted some gains relative to the dollar as the data hit the markets, rising to $1.1187, its highest for the day at the time. Those gains were short-lived though. Euro/dollar gained momentum later in the day, rising above the 1.12 handle. In afternoon European trading hours, the pair was up 0.5% compared to where it started the day.

Weaker inflation figures led the loonie to reverse gains it made versus the US dollar earlier in the day on the back of oil prices picking up. In particular, inflation rose by 0.1% month-on-month in May, below the 0.2% expected and April's 0.4%. On an annual basis, CPI rose by 1.3%, negatively comparing to the projected 1.5% and the 1.6% from the previous month. Annual core inflation, which strips out volatile items in its calculations and which is closely watched by the Bank of Canada, fell to 0.9%, its lowest in almost twenty years. April's respective figure stood at 1.1%. The BoC's target for inflation is 2% annually and today's numbers might pose a challenge to the Bank's recent rate-hike talk, which significantly boosted the loonie.

In terms of reaction in the forex markets to Canadian inflation numbers, dollar/loonie surged, rising to as high as 1.3296 within the first few minutes of data release. The pair was trading at 1.3219 before. As the European trading session is getting closer to its end for the day, dollar/loonie is up 0.3%.

Turning to data out of the US released later in the day, the June flash manufacturing PMI was released at the nine-month low of 52.1. Moreover, this was at a negative surprise compared to the 53.0 expected and below May's 52.7. The services flash PMI was also below expectations, standing at the three-month low of 53.0. Dollar/yen fell as the data hit the markets, though it quickly recovered.

Other data out of the US pertained to new home sales during May. Those rose by a more-than-expected 2.9% to reach 610,000 units from April's upwardly revised 593,000 (from 569,000 before). Dollar/yen experienced volatility upon data release, showing no clear direction. It last traded at 111.26, slightly down on the day. The dollar index looks set to finish the day lower and was last down 0.3% on the day.

Sterling continued gaining versus the dollar today after Kristin Forbes, the Bank of England Monetary Policy Committee (MPC) member who is to complete her term at the MPC by the end of the month, urged fellow MPC members to raise rates immediately. Pound/dollar was last up on the day, reaching a three-day high of 1.2744 at its highest.

A weaker US currency spurred demand for gold which is on track for its third straight day of gains. At its highest for the day, the precious metal hit a one-week high of $1258.73 an ounce. WTI and Brent crude were trading at $42.94 and $45.49 a barrel, up 0.47% and 0.60% on the day respectively.

FOMC voting member Jerome Powell will be giving a speech at a Federal Reserve Bank of Chicago Symposium at 18:15 GMT.

FX Markets Close the Week in Peace

- US stocks slipped somewhat in the opening, but European equities encountered more substantial losses today (between 0.3% and 1%). The dollar lost some minor ground against the euro and was more or less stable against the Yen. Oil failed to rebound and hovers near the sell-off lows around $45/barrel.

- The ECB is pushing for a change to the EU-law as it seeks "clear legal competence in the area of central clearing" of euro-denominated financial contracts, giving it more control over non-EU clearinghouses, also in the UK after brexit, that are deemed systemically important to the bloc's financial markets.

- EC president Tusk said that the UK's offer on citizen's rights was below expectations. "If we compare the current level of citizens' rights to what we have heard from the British prime minister, it's obvious that this is about reducing the citizens' rights --I mean the EU citizens in the U.K.".

- According to a poll, British households are not expecting a major upsurge in inflation over the next 12 months, despite growing rancour within the ranks of the Bank of England over rising prices.

- Unidentified sources close to the matter point out that the growing scarcity of German government bonds makes any major extension of the ECB's asset buying scheme difficult and this will be a key consideration when policymakers decide whether to extend the buys.

- During a joint summit press conference, Macron and Merkel said to be fully committed to a free market economy IF it respects multilateral rules. By September, the two will also present plans to expand their cooperation.

- Eurozone PMI data were mixed today with services surprising to the downside and manufacturing to the upside. General levels stay high however. Combined with the strong consumer confidence figures yesterday, Eurozone economic growth in the second quarter promises to be strong. Price components of the PMI's disappointed.

- French Q1 growth was upgraded again to 0.5% from 0.4% in the second reading and 0.3% in the first. Consumption remained flat over the quarter, but businesses ramped up their investments, with grossed fixed capital formation increasing by 1.2 %. Meanwhile, the PMI surveys indicated French job creation hit near decade highs in June.

Rates

PMI's can't influence bond trading

Global core bond markets ended the week in the same vein as the previous 4 trading sessions: with a range-bound, technically-inspired, neutral trading session. In contrast with previous days, the eco calendar was interesting with the release of EMU PMI's. The composite declined more than forecast in June, driven by a disappointing services PMI. The PMI remained at an elevated level from an absolute point of view though and suggests EMU growth to accelerate in Q2 to 0.7% Q/Q. Price components fell to the lowest level in 5 months and confirm the ECB's reluctance in normalising monetary policy. Markets didn't react on the release and seem to be counting down to the Summer holidays. Brent crude made a second miserable attempt to correct higher, but remains near the sell-off lows. European equity market got off in a swoon around European noon, but didn't trigger safe haven flows. Sources indicated that scarcity of German government bonds is a key consideration for the ECB when deciding on extending its QE-programme. This scarcity limits the possibility of a major extension. Markets didn't react today, but if this idea gains traction it could trigger repositioning higher especially in the German bond market.

At the time of writing, changes on the German yield curve range between +0.3 bps (5-yr) and +1.8 bps (30-yr). The US yield curve shifts up to 1.6 bps (30-yr) higher. On intra-EMU bond markets, 10-yr yield spreads versus Germany were close to unchanged with Portugal (-3 bps) and Greece (-9 bps) outperforming.

Currencies

FX markets close the week in peace

Dollar cross rates didn't show much spirit either today. Traders are already looking forward to next week's more interesting eco calendar with a Yellen speech (Tuesday) and crucial inflation data on both sides of the Atlantic on Friday (US PCE and EMU CPI). USD/JPY kept a perfect tight sideways trading range near 111.30 in the final session of the week, while EUR/USD moved slightly higher, from around 1.1150 to 1.1180. The short term (2y) rate differential moved slightly in favour of the euro this week, explaining the small gains in an uneventful week. The US/German 2-yr yield spread narrowed from 200 bps on Monday to 196 bps today. The above mentioned Reuters rumours could, if reinforced eventually underpin the single currency, but for now it's still a long shot.

Sterling initially profited from BoE Forbes' farewell speech last night. The resigning policy maker tried to boost the hawkish' wing in the central bank's momentum one final time. The recent sequence of events (BoE meeting – Carney comments – Haldane speech) triggered a significant rethinking in rate hike expectation. The probability of a 25 bps hike by the BoE this year rose from 6.5% on June 14 to 50% today. Sterling still has difficulties to gain decent ground though as official Brexit-talks started on a bad note. EU Tusk said that PM May's opening offer on EU nations is below expectations. He added that Brexit took up only very little time at today's EU Summit. Sterling's fortunes changed throughout the day with EUR/GBP returning to opening levels around 0.8790.

Trade Idea Wrap-up: EUR/USD – Stand aside

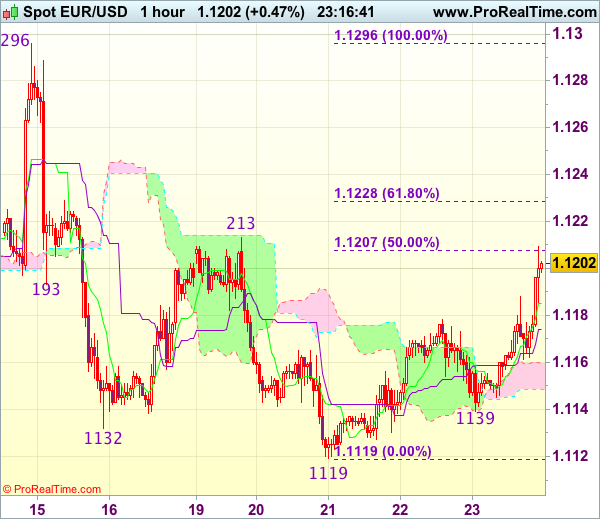

EUR/USD - 1.1202

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1185

Kijun-Sen level : 1.1174

Ichimoku cloud top : 1.1160

Ichimoku cloud bottom : 1.1147

Original strategy :

Sell at 1.1210, Target: 1.1110, Stop: 1.1245

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency has surged again in NY morning, suggesting near term upside risk remains for the rebound from this week’s low of 1.1119 to extend gain to 1.1213 resistance, then towards 1.1228-30 ((61.8% Fibonacci retracement of 1.1296-1.1119), however, reckon upside would e limited to 1.1260-70 and price should falter well below resistance at 1.1296, bring retreat next week.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below the Kijun-Sen (now art 1.1174) would bring weakness towards 1.1139 support but break there is needed to revive bearishness and signal an intra-day top is formed, bring retest of 1.1119.

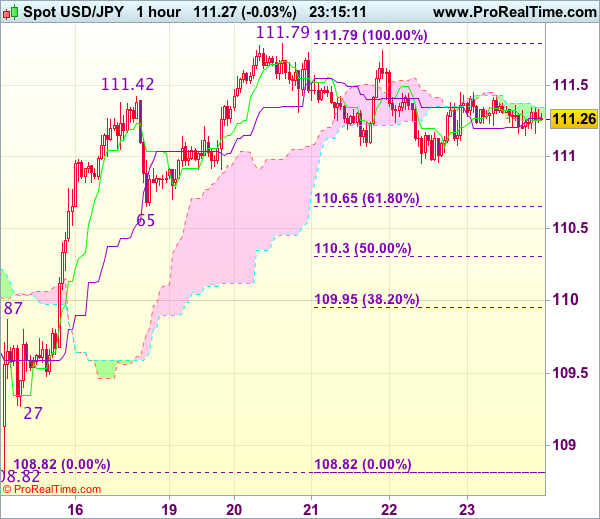

Trade Idea Wrap-up: USD/JPY – Buy at 110.65

USD/JPY - 111.25

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.26

Kijun-Sen level : 111.28

Ichimoku cloud top : 111.35

Ichimoku cloud bottom : 111.26

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

Although the greenback found support just below 111.00 level, near term downside risk remains for the erratic fall from this week’s high of 111.79 to bring retracement of recent rise and weakness to 110.90-95 cannot be ruled out, however, reckon previous support at 110.65 would limit downside and bring another rise later, above 111.45-50 would bring retest of 111.79 but break there is needed to confirm the rise from 108.82 low has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).

Trade Idea: EUR/GBP – Buy at 0.8660

EUR/GBP - 0.8795

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Buy at 0.8660, Target: 0.8860, Stop: 0.8620

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8660, Target: 0.8860, Stop: 0.8620

Position : -

Target : -

Stop : -

Euro’s retreat after meeting resistance at 0.8846 earlier this week has retained our view that further consolidation below recent high at 0.8866 would be seen and another corrective fall to 0.8740-50 cannot be ruled out, however, downside should be limited to support at 0.8652, bring another rise later. Above said resistance at 0.8846 would signal the retreat from 0.8866 has ended, bring retest of this last week’s high but break there is needed to confirm recent erratic upmove from 0.8304 low has resumed and extend further gain to 0.8880, then 0.8900, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

In view of this, we are looking to buy euro on subsequent pullback but one should exit on such rise. Below 0.8650 would defer and risk test of 0.8620, a break below there would signal top is formed instead, bring further fall to 0.8620, then 0.8600 which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Hold short entered at 1.3295

USD/CAD - 1.3284

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Sold at 1.3295, Target: 1.3130, Stop: 1.3355

Position: - Short at 1.3295

Target: - 1.3130

Stop: - 1.3355

New strategy :

Hold short entered at 1.3295, Target: 1.3130, Stop: 1.3355

Position: -

Target: -

Stop:-

Although the greenback has rebounded after finding support at 1.3208 and further consolidation would be seen, as long as indicated resistance at 1.3348 holds, prospect of another retreat remains, below said support would bring test of 1.3191 but break there is needed to signal the rebound from 1.3165 low has ended, bring retest of this support later. Looking ahead, only a break below there would confirm recent decline from 1.3794 top has resumed and extend fall to 1.3100-10 and later towards previous support at 1.3078.

In view of this, we are holding on to our short position entered at 1.3295. Only break of said resistance at 1.3348 would defer and risk a stronger rebound to previous support at 1.3387 (now resistance), however, still reckon upside would be limited to 1.3420-25 and price should falter well below resistance at 1.3471, bring another decline later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Loonie Came Under Pressure on Disappointing CPI Data

Canadian dollar fell back to 1.3300 against the greenback, retracing the largest part of Thursday's rise, inspired by better than expected Canada retail sales. Loonie came under pressure on disappointing CPI data, as Canadian inflation rose less than expected in May. Consumer price index increased in May by 0.1% from the previous month, falling below forecast for a 0.2% increase and 0.4% rise in April. Annualized inflation rose by 1.3% in May, undershooting 1.5% forecast and 1.6% increase in April. Fresh rally improved near-term technicals and left another base at 1.3200 zone which acts as very strong support. Lift above initial barriers at 1.3255 (falling Tenkan-sen / 10SMA), eased downside pressure, turning near-term focus higher and seeing scope for renewed attempt at 1.3340 (200SMA) which repeatedly capped correction from 1.3164 (14 June low).

Res: 1.3306; 1.3340; 1.3351; 1.3387

Sup: 1.3255; 1.3200; 1.3190; 1.3164

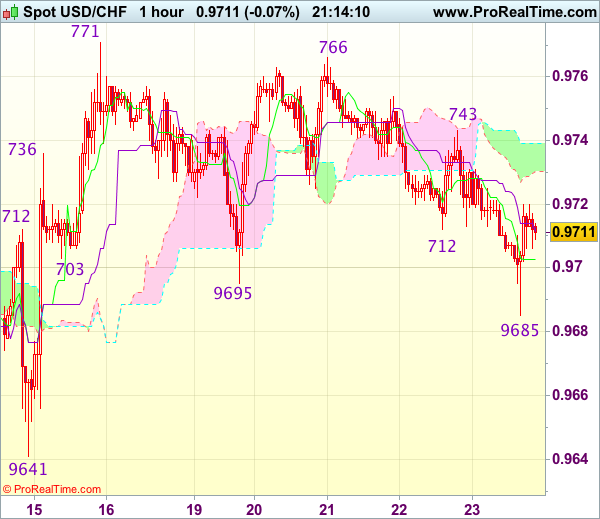

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9708

Original strategy :

Bought at 0.9705, stopped at 0.9690

Position : - Long at 0.9705

Target : -

Stop : - 0.9690

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Dollar’s intra-day breach of previous support at 0.9695 dampened our bullishness and erratic fall from 0.9771 top may extend weakness to 0.9660, however, as broad outlook remains consolidative, still reckon downside would be limited to 0.9641 support, risk from there is seen for another rise to take place next week.

On the upside, expect recovery to be limited to the upper Kumo (now at 0.9739) and bring another decline. Only a firm break above resistance at 0.9743 would revive bullishness and signal an intra-day low is formed, bring test of 0.9766-71 resistance first. Once this resistance is penetrated, this would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808, then towards another previous resistance at 0.9825.

Canadian Inflation Heads Lower in May as Energy Prices Pull Back

Consumer price inflation decelerated to1.3% (year-on-year) in May from 1.6% in April. Prices fell 0.2% month-on-month (seasonally adjusted), following a 0.4% gain in April.

A deceleration in energy prices weighed on the headline number, particularly gasoline prices. Energy prices were up 3.3% year-on-year, slowing from 9.6% in the month prior.

Food prices rose 0.3% (month-on-month) bringing the year-on-year rate to -0.1%, up from -1.1% in April.

The Bank of Canada's core measures were either flat or down, with CPI-median edging down to 1.5 % (from 1.6%), CPI-trim to 1.2% (from 1.3%), and CPI-common unchanged at a feeble 1.3%.

Key Implications

Inflation pressures remain muted in Canada. Even outside of energy prices, core measures show little in the way of burgeoning price pressures. In the past the weakness has been concentrated in goods categories, but even services decelerated in May.

The soft inflation environment is likely enough for the Bank of Canada to hold off on raising interest rates at its next meeting in July. Nonetheless, a continuation of above-trend economic growth should reduce slack and help turn inflation higher over the second half of this year, allowing the Bank of Canada to nudge up the overnight rate in October.

Canadian Inflation Continued to Slow in May

Highlights:

- The year-over-year rate of headline CPI inflation fell to a six-month low of 1.3% in May.

- Expectations were for a modest decline to 1.5% from April's 1.6% reading.

- Electricity prices fell in May as another round of rebates began rolling out in Ontario.

- Gasoline prices declined in the month with the year-over-year increase slipping to 6.8% from as high as 23% in February.

- Food prices rose in May and are now almost flat relative to a year ago following a period of deflation.

- Year-over-year inflation excluding food and energy prices fell for a fourth consecutive month, hitting three-year low of 1.4% in May.

- The BoC's three core measures averaged 1.3% after rounding, down from 1.4% in April and 2.0% a year ago. May's average is the lowest since 1999.

Our Take:

Today's CPI report is the first since the Bank of Canada's hawkish turn last week. Senior Deputy Governor Wilkins's comments put a positive slant on recent economic developments. Additionally, she was somewhat dismissive of recent softer inflation numbers, noting both the transitory impact of lower food prices and the lagged effect of excess capacity on core measures. Nonetheless, another broad-based shortfall in inflation in May will likely have markets re-evaluate the odds of a rate hike as soon as July. Broadening economic growth and progress in the energy sector's adjustment, along with the central bank's acknowledgement that inflation lags the cycle, seem to make rising inflation in the near term less of a precondition for removing accommodation. However, we still think policymakers will want to see some progress toward 2% before raising rates and that was clearly absent in May. Next week's Business Outlook Survey, GDP report and comments from Governing Council members will help firm up expectations around July's policy meeting but we think prospects of a move next month have been dealt a blow today.