Sample Category Title

GBPUSD – Recovers Higher Within Trading Range

GBPUSD - The pair continues to face upside pressure but within its established range. Support lies at the 1.2700 level where a break will turn attention to the 1.2650 level. Further down, support lies at the 1.2600 level. Below here will set the stage for more weakness towards the 1.2550 level. Conversely, resistance stands at the 1.2800 levels with a turn above here allowing more strength to build up towards the 1.2850 level. Further out, resistance resides at the 1.2900 level followed by the 1.2950 level. On the whole, GBPUSD continues to face upside threats.

DAX Slips As Oil Prices Remain Under Pressure

The DAX index has posted losses in the Friday session. Currently, the index is at 12,730.25 points, down 0.50%. There was positive news on the manufacturing front, as German and Eurozone Manufacturing PMIs beat their estimates. However, data from the services sector failed to keep pace, as German and Eurozone Services PMIs both missed expectations.

Global stock markets continued to contend with low oil prices, which are weighing on investor confidence. Brent crude has plunged 10.8% in June, as crude trades around $45 a barrel. As crude prices continue to fall, there are rising concerns of disinflation. The US, Japan and much of Europe are struggling with low inflation, and lower levels could hamper growth. OPEC members continue to discuss lowering production, but the markets do not seem impressed. OPEC is already bound by a production agreement and compliance is over 100%, yet this has failed to prevent the collapse in oil prices. Another headache for major producers is the increase in production from the US, Libya and Nigeria.

A stronger global economy has spurred demand for exports from the euro-area, and this has boosted the manufacturing sectors in Germany and the eurozone. German Manufacturing PMI ticked lower to 59.3 in May, above the forecast of 59.1 points. Germany's manufacturing sector continues to show strong growth, and the April reading of 59.4 was the highest since March 2011. The news was also positive in the eurozone, as Manufacturing PMI improved for a tenth straight month, climbing to 57.3 points. This beat the estimate of 56.9 points. On Thursday, the ECB's economic bulletin projected solid growth in the euro-area in the second quarter, buoyed by low inflation rates and stronger domestic demand.

The German economy remains robust, with a strong labor market and stronger consumer and state spending. As well, the manufacturing and export sectors are booming due to increased global demand for German products. There were cries of despair in political and business circles in Europe when Donald Trump was elected, as Trump campaigned on a protectionist, 'America first' agenda. However, these concerns have largely died down, as the eurozone economy has improved and Trump has been in damage control mode, as he focuses on domestic scandals. Earlier this week, the well-respected German BDI Federation of Industry added its voice to the chorus of accolades for the German economy. The BDI said that Germany's economic output would increase by 1.5% this year. At the same time, the BDI counseled caution, noting that the economy had been buoyed by a weaker euro, lower oil prices and the ECB's accommodative monetary policy. All three are ‘external factors', in the sense that Germany has limited influence on them, and a significant change in any one factor could weigh on economic growth.

US 30 Index Declines To Reach One-Week Low, Medium-Term Outlook Remains Bullish

The US 30 index is on its fourth day of declines after reaching an all-time high of 21,539.10 on Monday. Today's decline has led the index to record a one-week low of 21,340.70.

Technical indicators such as the RSI and stochastics are pointing to a change in short-term momentum for the index. The RSI is theoretically in bullish territory at 60, but it has steeply fallen from overbought territory to reach its current level. In addition, the indicator remains downward sloping. Meanwhile, the stochastics are projecting a similar picture with the %K line in bearish territory (after recording a steep fall) and below the slow %D line.

On the upside, Monday's all-time high of 21,539.10 is likely to act as a point of resistance. Further up, the 21,600.00 level might act as psychological barrier to upside movements as well.

On the downside, today's decline violated the Tenkan-sen line (red), which was providing intra-day support at 21,378.00. The 21,300.00 handle, a potential psychological level, could provide some support. Another likely important support area is the one formed by the Kijun-sen line (blue) at 21,089.10 and the 21,000.00 psychological mark. Notice that the 50-day moving average (MA) at 21,020.00 is also in between these two points.

As regards the medium-term outlook, it remains bullish given the significant advancing by the index since the start of the year. Further supporting this is the fact that the index level is comfortably above the 50- and 200-day MAs as well as the Ichimoku cloud top, while both MAs are currently upward sloping. A note of caution though as the considerable divergence from the 200-day MA might be indicative of an overextended rally.

Overall, the near-term momentum is currently looking negative and the medium-term is bullish.

Technical Outlook: Spot Gold – Extended Recovery Eyes $1262/64 Barriers

Spot Gold extends recovery from week’s low at $1240 and took out initial barrier at $1254 (Fibo 23.6% of $1296/$1240 descend / 10SMA).

Correction may extend through $1259 (55SMA / daily Tenkan-sen) towards strong resistance at $1262/64 (Fibo 38.2% / 20SMA) as slow stochastic on daily chart is heading north after reversal from O/B territory and showing more room at the upside.

Close above $1264 is needed to generate strong signal for extended recovery.

Broken 10SMA now acts as initial support at $1255, followed by more significant broken 100SMA at $1248, loss of which would signal an end of corrective phase and shift focus towards $1240 and 200SMA at $1236.

Res: 1259, 1262, 1264, 1268

Sup: 1255, 1248, 1245, 1240

Technical Outlook: WTI Oil – Limited Upside Action Despite Strong Bullish Signals On RSI/Slow Stoch Reversal

WTI oil holds positive tone on Friday but upside attempts remain limited following Thursday's strong upside rejection after brief probe above $43.00 barrier.

Negative technicals and sentiment maintain strong bearish pressure for retest of temporary footstep at $42.04 (21 June low) and extension of bear-leg from $51.98 (25 May high) towards next target at $40.63 (weekly cloud base / 50% retracement of $26.04/$55.22 recovery).

On the other side, strong bullish signal is coming from daily RSI slow stochastic reversal from oversold territory, which may spark fresh recovery rally towards upper pivots at $43.82/$44.13 (Fibo 38.2% of $46.69/$42.04 / falling 10SMA).

Res: 43.14, 43.30, 43.82, 44.13

Sup: 42.67, 42.26, 42.04, 41.09

Fed Talk Provides Little Support For Dollar

Global equities are trading mixed now that this weeks Fed speakers have done little to alter market projections for the path of interest rate. Crude oil is poised for its fifth straight week of declines.

The 'mighty' USD peaked at a one-month high on Tuesday after the Fed did the expected, hiked interest rates last week and left the door ajar for further monetary tightening later in the year.

However, with fed fund futures odds of that happening straddling atop of +41%, the greenback has been stuck in a tight range ever since, pending fresh catalysts.

Nonetheless, the market is waiting on U.S data due next week – which include the June consumer confidence indicator, pending home sales, crude oil inventories, revised Q1 GDP and the PCE price index – for direction.

Yet, for a stronger conviction, what really matters for the dollar are wages and inflation-related data which occurs in a fortnight with non-farm payrolls (NFP).

This market snooze fest, aside from the commodity currency moves this week – CAD in particular – investors have to be patient and pick their moments now that central banks again have a stranglehold on currency markets.

Note: Today, the Fed's Bullard, Mester and Powell cap a busy week for speeches from U.S policy makers.

1. Global stocks keep their head above water

Global equities, helped by a rebound in tech shares in particular, remain resilient despite investor concerns about a policy misstep from the Fed – inflation is lagging – and a rout in the oil market that extended for a fifth-week.

In Japan, the Nikkei share average finished this week little changed as dollar-yen levels steadied (¥111.28). The broader Topix added less than +0.1%, while down-under, Australia's S&P/ASX 200 Index gained +0.2%.

In Hong Kong, the Hang Seng China Enterprises Index added +0.3%, while the Hang Seng Index rose less than +0.1%.

In China, blue chips stocks ended at an 18-month high, buoyed by MSCI inclusion of mainland shares in its key index. The blue-chip CSI300 index settled up +0.9%, while the Shanghai Composite Index added +0.3%.

In Europe, indices are trading modestly lower across the board with continued weaker oil prices weighing.

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx600 -0.1% at 388, FTSE -0.3% at 7416, DAX -0.3% at 12757, CAC-40 -0.2% at 5271, IBEX-35 -0.5% at 10656, FTSE MIB -0.3% at 20862, SMI -0.2% at 9034, S&P 500 Futures +0.1%.

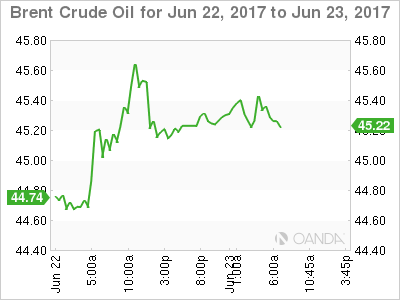

2. Oil edges up, but still set for biggest H1 fall in 20-years, gold shines

Overnight, oil prices have edged a tad higher, but remains on course for its worst first-half decline in almost two decades as production cuts have failed to sufficiently reduce oversupply.

Brent crude futures are up +28c at +$45.50 a barrel, while West Texas Intermediate (WTI) crude futures are trading at +$43.04 a barrel, up +30c from yesterday's close.

Since peaking in late February, crude has dropped around -20% in the wake of the initial OPEC-led production cut.

Note: OPEC and non-OPEC oil producers' compliance with the output deal reached 106 percent in May. However, a number of producers – notably Iraq, Saudi Arabia and Russia – aggressively ramped up output in the run-up to the deal, while U.S producers, Libya and Nigeria are exempt from the cuts.

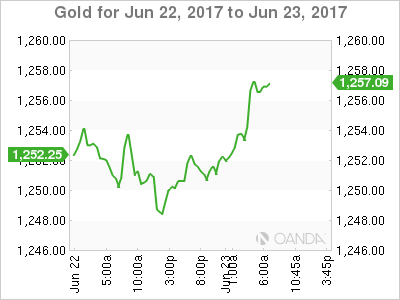

Ahead of the U.S open, gold prices (+0.6% at +$1,257.1 an ounce) have climbed to a weekly high, supported by a lower dollar and economic and political uncertainty around the world. However, the prospect of further interest rate hikes by the Fed is expected to limit gains.

3. German Yield Spreads Poised to Reach Pre-Trump Levels

The Treasury/Bund 10-year gap currently stands at +191.3 bps, down from +233.38 bps in late December.

Some dealers believe that the risk that the Fed may be moving ahead of the curve in its interest rate-rise path, given declining inflation rates and a shift in political risk from Europe into the U.S, argues for a tighter yield spread between the two bonds (U.S 10's to outperform German debt product). For many, the technical target is around +165 bps, a level last seen before Trumps U.S presidential win.

Overnight, the yield on 10-year Treasuries has backed up +1 bps to +2.16%. In the U.K 10-year yields have added +3 bps to +1.05%, while French OAT's and German Bund yields are little changed.

Note: The Fed has raised interest rates four times since late 2015, and three times since the U.S election last November. U.S Treasury yields have fallen around -50 bps since the March rate hike.

4. The 'Big' dollar under pressure

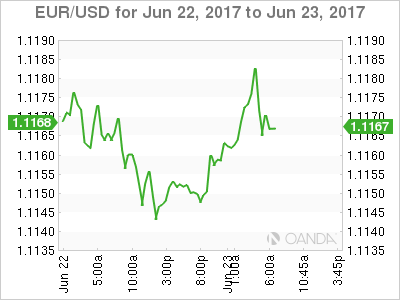

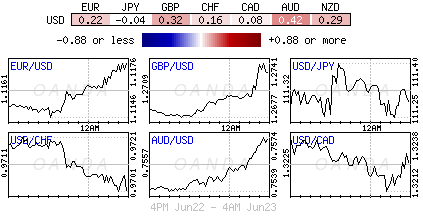

Overnight, the U.S dollar has traded mostly on the back foot. The EUR (€1.1174) has found support following better-than-expected manufacturing data in the eurozone (see below).

Sterling (£1.2727) rises after outgoing BoE member Kristin Forbes said in a speech yesterday that there were “compelling” reasons why a U.K interest rate rise should not be delayed. Ms. Forbes leaves the MPC next week, but the comment carries weight, as she is not a lone voice, with three out of eight members voting to raise rates at this month's BoE meeting. The pound 'bear' expect gains to be limited due to political and Brexit uncertainty.

Note: It's exactly a year today since Britain voted to leave the E.U – in the past 12-months the pound has fallen more than -15% outright, and almost -13% versus the EUR.

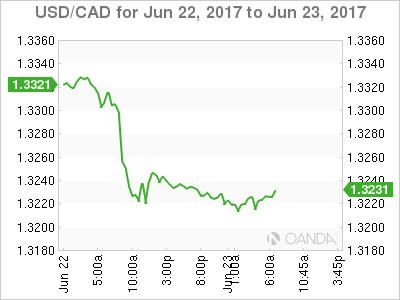

Commodity-linked currencies continue to hold onto their significant gains made yesterday following a rebound in crude oil prices from 10-month lows – CAD in particular is trading flat (C$1.3232).

5. Eurozone economy slows, but

Data this morning showed that the eurozone's economy slowed slightly this month, but it still had its strongest quarter in more than six years, according to a survey of activity in the manufacturing and services sectors.

The composite PMI fell to 55.7 from 56.8 in May, a five-month low. The market was expecting it to fall to 56.6; however, it still leaves the eurozone economy growing at its fastest rate since the start of 2011.

Market Update – European Session: European Data Continues To Improve, Building Case For ECB Policy Normalization

Notes/Observations

European data continues to improve, building case for ECB policy normalization,

France Q1 GDP revised higher

Major European PMI Manufacturing data beats expectations and extent further into expansion territory (France, Germany and Euro Zone all improve)

Overnight

Asia:

Japan Jun Preliminary PMI Manufacturing registered its 9th month of expansion but the lowest pace in 6-months (52.0 v 53.1 prior);

North Korea said to have carried out another rocket engine test, likely for small stage of 3-stage ICBM type rocket engine

Europe:

PM May stated that EU citizens who currently live in the UK would not be forced to leave after Brexit; had no intention of breaking up families. Proposal was "fair and serious" offer that ~3M EU citizens living in the UK for 5 years would be offered a new UK settled status with rights to stay and access to health, education plus other benefits; proposal is dependent on EU guaranteeing Britons same rights

German Chancellor Merkel noted that the UK offer on citizens' rights was a good start, but many issues were still to be resolved including finances and relationship with Ireland

BOE's Forbes (outgoing dissenter) saws some urgency to tighten monetary policy; liftoff of UK rates shouldn't be delayed longer

SNB's Maechler reiterated view that SNB has the ability to intervene in the forex market if necessary

Americas:

Senate healthcare bill text released. GOP Sens Paul, Lee, Johnson and Cruz release joint statement that they were not ready to support healthcare bill; currently open to negotiation and obtaining more information

Congressional Budget office (CBO) planned to release scoring on Senate healthcare bill early next week

Mexico Central Bank (Banxico) raised the Overnight Rate by 25bps to 7.00% (as expected). Vote was not unanimous with one member voted to keep rates unchanged. Current rate was consistent with 3% inflation target

Economic Data

(NL) Netherlands Q1 Final GDP Q/Q: 0.4% v 0.4%e; Y/Y: 3,.2% v 3.4% prelim

(SG) Singapore May CPI M/M: 0.3% v 0.1%e; Y/Y: 1.4% v 1.3%e; CPI Core Y/Y: 1.6% v 1.7%e (highest annual pace in nearly three years)

(FR) France Q1 Final GDP Q/Q: 0.5% v 0.4%e; Y/Y: 1.1% v 1.0%e

(FR) France Jun Preliminary Manufacturing PMI: 55.0 v 54.0e (9th month of expansion), Services PMI: 55.3 v 57.0e, Composite PMI: 55.3 v 56.7e

(DE) Germany Jun Preliminary Manufacturing PMI: 59.3 v 59.0e (31st month of expansion), Services PMI: 53.7 v 55.4e, Composite PMI: 56.1 v 57.2e

(TW) Taiwan May Industrial Production Y/Y: 0.8% v 0.5%e

EU) Euro Zone Jun Preliminary Manufacturing PMI: 57.3 v 56.8e (47th month of expansion), Services PMI: 54.7 v 56.1e, Composite PMI: 55.7 v 56.6

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2029, 2033 and 2051 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 388, FTSE -0.3% at 7416, DAX -0.3% at 12757, CAC-40 -0.2% at 5271, IBEX-35 -0.5% at 10656, FTSE MIB -0.3% at 20862, SMI -0.2% at 9034, S&P 500 Futures +0.1%]]

Market Focal Points/Key Themes European Indices trade modestly lower across the board with continued weaker Oil prices weighing. Activity has been fairly lackluster with little in the way of market moving news and a quiet corporate calendar. Gambling stocks in the UK have been under pressure after the CMA launched enforcement action against the firms, whilst Imagination Technologies continued to see upside momentum after yesterday announcing that its started a formal sale process. Meanwhile Zumtobel reported full year results, with a dip in Rev causing weakness in shares, whilst NN Group trade over 3% lower after Dutch Watchdog says NN Group must compensate customers based on estimate of losses due to misinformation. Looking ahead to the US morning session, notable earners include Blackberry and Finish Line.

Equities

Consumer discretionary [GVC [GVC.UK] -1.1% 888 [888.UK] -0.9%, William Hill [WMH.UK] -0.9%, Ladbrokes Coral [LCL.UK] -0.5% (CMA launches enforcement action against gambling firms), - Zumtobel [ZAG.AT] -4.3% (Earnings)]

Technology: [ Imagination Tech [IMG.UK] +10% (Follow through)]

Healthcare: [Genfit [GNFT.FR] -1.8% (Reaches a critical milestone towards the development of a non-invasive IVD test for Nash), - Gensight [SIGHT.FR] -2.8% (Placing), - Diasorin [DIA.IT] +2.9%, Tecan [TECN.CH] -1.0% (To collaborate with Tecan in new platform development)]

Speakers

ECB said to recommend amending article 22 of Statute to enable Eurosystem to fulfill mandate and become a Euro clearer regulator EU Leaders commented ahead of final day Summit in Brussels

UK PM May reiterated view that had a very constructive start to Brexit negotiations and presented a fair proposal on citizen rights

EU's Juncker noted that the UK proposal on citizen rights was a 1st step but was not sufficient

YouGov/Times poll: 35% of survey respondents would prefer Corbyn (opposition) as PM vs. 34% for May (Corbyn overtaking May for first time). 30% were unsure when asked who make the best prime minister

Brazil Central Bank (BCB) Gov Goldfajn: Inflation was under control

Currencies

FX markets were little phased by improve European economic data. France Q1 GDP was revised higher while the major European PMI Manufacturing data beat expectations and extented further into expansion territory (France, Germany and Euro Zone all improve)

Dealers noted that the USD in a holding pattern as the summer doldrums appeared to begin early. Federal Reserve has raised interest rates four times since late 2015, and three times since the US election last November. US Treasury yields have fallen around 50 bp since the March rate hike.

Fixed Income

Bund futures trade at 164.99 down 9 ticks, near the session highs as markets try to figure out when the ECB will announce its tapering schedule. Resistance lies near the 165.52 level, followed by 166.21. A break of the 163.89 support level could see lows target 162.05 followed by 160.30.

Gilt futures trade at 128.82 down 40 ticks as MPC-dated SONIAs are showing increased bets on 2017 BOE rate hikes this morning. Price is pulling back towards the lower third the June trading range. If price becomes bearish and drops below the noted 128.53 level, initial support lies at the 127.96 level, with key support at the 126.70 support level. Resistance lies at the 129.14 level, followed by the 129.80 level. Major resistance lies at the 132.65. region.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.6099T a gain of €8.3B from €1.6016T prior. Use of the marginal lending facility rose to €253M from €203M prior.

Corporate issuance saw $0.5B come to market via 1 issues headlined by Adani Ports 10-year fixed note offering. This week's issuance is at $19.2B, lower than the analysts' issuance target to come in around $20B. For the week ending Jun 22nd Lipper US fund flows reported IG funds net inflows $1.55B bringing YTD inflows to $65.84B, High yield funds reported outflows of $0.1B bringing YTD outflows to $4.83B.

Looking Ahead

(ZA) South Africa to sell combined ZAR650M in 2025, 2029 and 2033 bonds

06:00 (UK) DMO to sell combined £2.5B in 1-month, 3-month and 6-month bills (£0.5B, £1.0B and £1.0B respectively)

06:45 (US) Daily Libor Fixing

07:30 (IN) India Weekly Forex Reserves

07:30 (TR) Turkey Jun Real Sector Confidence (Seasonally Adj): No est v 104.8 prior; Real Sector Confidence (unadj): No est v 109.2 prior

07:30 (TR) Turkey Jun Capacity Utilization: No est v 78.8% prior

08:00 (BR) Brazil Mid-Jun IBGE Inflation IPCA-15 M/M: 0.1%e v 0.2% prior; Y/Y: 3.5%e v 3.8% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces details of upcoming auctions

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada May CPI M/M: 0.2%e v 0.4% prior; Y/Y: 1.5%e v 1.6% prior; Consumer Price Index: 131.0e v 130.4 prior

08:30 (CA) Canada May CPI Core- Common Y/Y: 1.4%e v 1.3% prior, CPI Core- Trim Y/Y: No est v 1.3% prior; CPI Core- Median Y/Y: No est v 1.6% prior

09:00 (BE) Belgium Jun Business Confidence: -0.8e v -1.1 prior

09:00 (MX) Mexico Apr Retail Sales M/M: +1.0%e v -1.3% prior; Y/Y: 2.4%e v 6.1% prior

09:00 (CL) Chile May PPI M/M: No est v -1.1% prior

09:45 (US) Jun Preliminary Markit Manufacturing PMI: 53.0e v 52.7 prior, Services PMI: 53.5e v 53.6 prior, Composite PMI: No est v 53.6 prior

10:00 (US) May New Home Sales: 600Ke v 569K prior

11:00 (EU) Potential sovereign ratings after EU close

(AT) Austria Sovereign Debt to Be Rated by Moody's

(FR) France Sovereign Debt to be rated by Moody's

(DE) Germany Sovereign Debt to be rated by Moody's

(GR) Greece Sovereign Debt to be rated by Moody's

(US) United States Sovereign Debt to be rated by Moody's

(BE) Belgium Sovereign Debt to be rated by Fitch

11:15 (US) Fed's Bullard (non-voter, hawk) in Cleveland

12:00 (US) Fed's Mester speaks in Cleveland

13:00 (US) Weekly Baker Hughes Rig Count data:

13:30 (DE) German Fin Min Schaeuble participates on panel regarding Europe

14:15 (US) Fed's Powell (voter, neutral) in Chicago

Can Rig Data Deal Another Blow To Oil?

- US PMI and housing data in focus as quiet week draws to a close;

- US oil rig data of interest as dead cat bounce in WTI and Brent signals possible further downside;

- GBP gains as BoE commentary turns increasingly hawkish;

- EUR higher as eurozone manufacturing PMI hits multi-year high.

US equity markets are expected to open a little higher on Friday after three days of small losses, with the focus on an otherwise quiet day falling on the PMI data for June and comments from a few Federal Reserve officials.

It's been a relatively quiet week on the whole so far from an economic data perspective. The flash manufacturing, services and composite PMIs will give us something to look out for, with all three expected to notch up moderate improvements while doing little to convince people that the economy is recovering from its slow start to the year. Should the soft data continue into the third quarter, it may force the Fed into considering slowing the pace of tightening – as markets already appear to be pricing in – which they seem very reluctant to do.

We'll also get new home sales data which has been on a nice uptrend since the start of last year and comes after a decent beat on existing sales earlier in the week. Three Fed officials are lined up to appear today including Jerome Powell – a permanent voter on the FOMC – Loretta Mester and James Bullard. Mester and Bullard are both non-voters this year and the latter, as was evident by comments on Thursday, is among the more dovish officials. Still, it will be interesting to see how they interpret the recent data and whether they see any downside risks that will influence the pace of tightening.

Late on in the day we'll get the latest rig count data from Baker Hughes, which comes as oil claws back some of the substantial losses suffered earlier in the week. Brent and WTI may be higher for a second day but as it is, there's little reason to believe this is anything more than a dead cat bounce and that next week may be another painful one. Traders are clearly unconvinced by the cuts that are intended to bring inventories down to their five year average, particularly against the backdrop of rising output from the US, Libya and Nigeria. A clear break below $44.50 in Brent and $42 in WTI could trigger further downside for oil, with $40 being the next big test.

Sterling is making small gains again this morning, aided once again by hawkish comments from Kristin Forbes who supports a rate hike but will leave the Bank of England at the end of the month. While traders still appear at ease with the recent hawkish turn but with Andy Haldane voicing his concerns on inflation this week, perhaps they shouldn't be. Still, even with recent gains, the pound remains range-bound against the dollar with 1.26 providing solid support below and 1.28 resistance above.

The euro is also trading a little higher today, supported by good PMI numbers from the eurozone, Germany and France. While some of the numbers have come off their recent highs, they still remain well above 50 – the level that separates growth from contraction – and point to stronger growth for the region. It's also encouraging that the manufacturing PMI for the euro area hit a multi-year high in June, which bodes well heading into the second half of the year.

Brexit One-Year On….. What Next?

It's remarkable thattoday marks exactly one year since Britain voted to leave the European Union,yetSterling still remains at depressed levels with the currency struggling to nurse the deep Brexit wounds. Although there was some optimism in the latter half of 2016 when economic data unexpectedly displayed resilience against Brexit, the visible signs of slowing growth in the first quarter of 2017 were a massive wakeup call. Since then, the Pound has found itself pressured from all directions as the ongoing Brexit developments, political instability in Westminster and influx of depressing economic data weigh heavily on the currency.

As we move deeper into the year, the horrible combination of rising inflation and tepid growth are likely to place the Bank of England in a complicated position. The interest rate tug of war between Bank of England policymakers has already started with expectations constantly fluctuating over when, or if, rates will be hiked. Although leaving interest rates unchanged seems like a safe bet amid the uncertainty, there is a risk of inflation rising uncontrollably which may aggravate the fall in real wages while punishing savers. On the other hand, raising US interest rates could negatively impact growth, dent business confidence and hit consumers even further. It will be interesting to see how the Bank of England solves this complicated jigsaw and while the end result remains uncertain, there is some certainty that Sterling will be impacted.

Brexit negotiations and UK politics will also heavily impact Sterling this year which can already be seen in the currency's price action. The growing uncertainty at home and abroad should leave the Pound highly vulnerable to losses with bears exploiting the technical bounce to drive prices lower.

From a technical standpoint, the GBPUSD currently trades within a bearish channel on the daily charts. Previous support around 1.2775 could transform into a dynamic resistance that opens a path lower towards 1.2600.

Gold glitters once again

Gold bulls received inspiration this week in the form of plunging oil prices which weighed on global sentiment and soured risk appetite. A weakening Dollar coupled with mixed messages from policymakers on US rate hike timings supported the metal further as prices lurchedtowards $1258 during Friday's trading session. With the zero-yielding metal notoriously known for being dictated by US rate hike expectations, there is a possibility of gold venturing higher if speculations of the Federal Reserve taking action this year decline. Due to Brexit developments, political risk in Washington and oil's oversupply woes stimulating risk aversion, safe-haven assets are likely to remain supported moving forward. From a technical standpoint, Gold is currently trading within a bullish channel on the daily charts and there is a visible reluctance to break below $1240. A decisive breakout and daily close above $1260 could bring bulls back into the game.

WTI Crude limps into Friday

WTI Crude edged higher during Friday's trading session on the back of profit-taking, but sentiment remained heavily bearish amid the oversupply concerns. With Oil prices officially in a “bear market,” investors will be paying close attention to how OPEC responds and if further cuts are put in place to reduce the global glut. The bias towards the commodity remains tilted to the downside with price action displaying doubts over OPEC's ability to trim global inventories to their five-year average in 2018. I believe this may be a critical period for oil especially when considering how prolonged periods of low prices and US Shale resurgence could cause OPEC's output-cut deal to collapse. From a technical standpoint, WTI Crude is under intense selling pressure on the daily charts. A technical bounce may be on the cards before prices trade back towards $42.

Gold Medium-Term Bullish, Silver Short-Term Bullish Consolidation, Crude Oil Strong Bearish Pressures.

Gold Medium-term bullish.

Gold's medium-term momentum is positive. Hourly support is located at 1240 (yesterday low). Stronger support is given at 1214 (09/05/2017 low). Expected to show short-term upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

Silver Short-term bullish consolidation.

Silver's selling pressures are strong despite ongoing bullish consolidation. Closest support is given at 16.36 (21/06/2017 low). Strong support is given at 16.06 (09/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude oil Strong bearish pressures.

Crude oil is finally continuing its decline since the recent collapse from $52. Support given at a 42.20 (14/11/2017 low) has been broken. Expected to show further decline.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).