Sample Category Title

Carney’s Dovish Remarks Pushes GBP Lower

The Bank of England Governor Mark Carney gave a prepared statement yesterday where he said that it was not the right time to raise interest rates. His comments came as the BoE voted to leave interest rates unchanged, but the vote count was split with 5 - 3. The dovish comments pushed the British pound to close weaker on the day.

Price action across the markets was mostly subdued with the lack of any clear economic data to go by. The declining oil prices are also bringing some uncertainty to the markets as the inflation expectations started to fall. This could potentially push the Fed's hawkish plans into doubt. Gold prices remained largely stable, while the US dollar managed to maintain its gains.

Looking ahead, another slow day for the markets but the RBNZ's interest rate decision is coming up later in the evening. Economists polled are expecting to see the RBNZ hold the OCR steady at 1.75%.

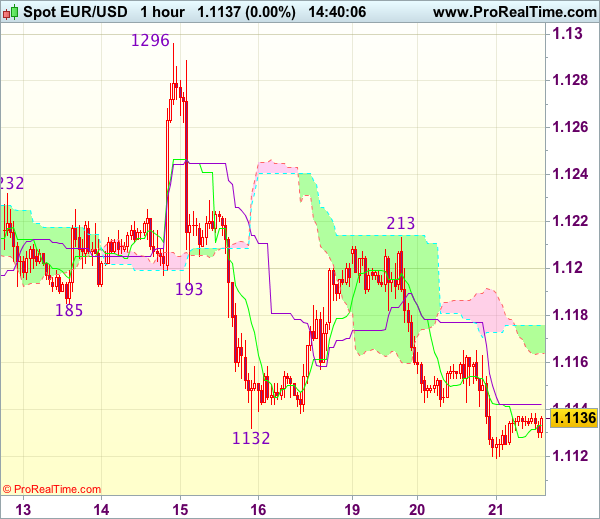

EURUSD intraday analysis

EURUSD (1.1136): EURUSD extended the declines from Monday with price action closing below 1.1200. Further downside could be extended although there seems to be the minor support that is formed at 1.1114. A possible bounce to the upside could result in a formation of a head and shoulders pattern on the daily chart. In the meantime, the minor resistance at 1.1171 could hold the gains in the near term. In either case, the bias in EURUSD is to the downside as we expect to see declines extending towards the lower support at 1.1018 - 1.0995. Price action is also consolidating within a triangle pattern on the 4-hour chart which could signal an upside move in price.

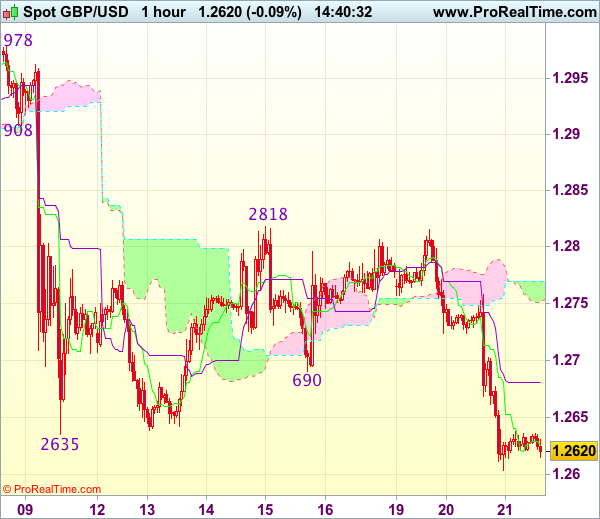

GBPUSD intraday analysis

GBPUSD (1.2634): The British pound fell sharply yesterday following the comments from the BoE Governor, Mark Carney. Price action closed just a few pips away from the first target of 1.2600. The current bounce could result in a short-term retracement on price with further declines likely to come by. GBPUSD could be seen testing the initial support at 1.2600 with the potential to extend the losses to 1.2400. On the 4-hour chart, any retracement is likely to be held near the developing resistance level of 1.2688. A reversal here could signal renewed declines in prices.

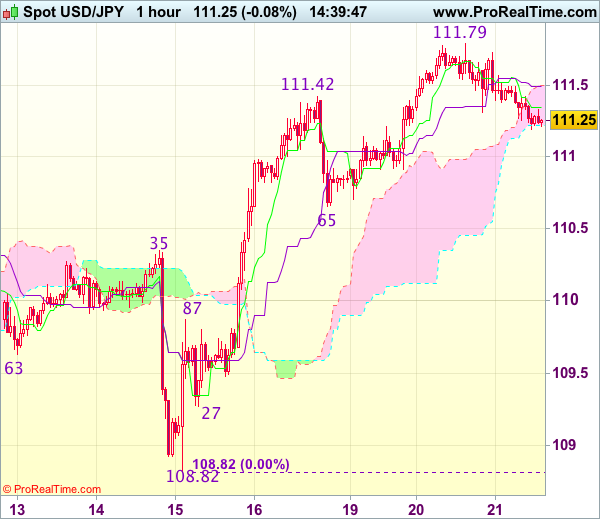

USDJPY intraday analysis

USDJPY (111.27): USDJPY hit resistance at 111.61 yesterday and closed with a doji. The current declines could see USDJPY pushing lower in the near term with support likely to form at 110.80 - 110.52. This will mark a retest of this support level which previously acted as resistance. A reversal off this level will signal further continuation towards the current resistance level at 112.00 - 111.70. A breakout above this resistance will only confirm further upside in price. In the near term, watch for price action at the support. A break down below this support could see USDJPY likely to extend the declines to 109.50 - 109.25 support.

Trade Idea : GBP/USD – Sell at 1.2695

GBP/USD - 1.2610

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2622

Kijun-Sen level : 1.2681

Ichimoku cloud top : 1.2769

Ichimoku cloud bottom : 1.2752

Original strategy :

Sell at 1.2715, Target: 1.2615, Stop: 1.2750

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2695, Target: 1.2585, Stop: 1.2730

Position : -

Target : -

Stop : -

As cable has remained under pressure after breaking below indicated previous support at 1.2635, adding credence to our view that recent decline is still in progress and downside bias remains for further fall towards 1.2575-80, however, near term oversold condition would limit downside to 1.2550 and reckon 1.2520-25 would hold from here, risk from there is seen for a rebound later.

In view of this, we are looking to sell cable on recovery as 1.2695-00 should limit upside. Only above 1.2720-25 would abort and suggest an intra-day low is formed instead, bring a stronger rebound to 1.2755-60 and possibly 1.2780 but price should falter below indicated strong resistance at 1.2818.

Trade Idea : EUR/USD – Sell at 1.1175

EUR/USD - 1.1135

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1133

Kijun-Sen level : 1.1142

Ichimoku cloud top : 1.1176

Ichimoku cloud bottom : 1.1164

Original strategy :

Sell at 1.1185, Target: 1.1085, Stop: 1.1220

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1175, Target: 1.1085, Stop: 1.1210

Position : -

Target : -

Stop : -

Yesterday’s breach of previous support at 1.1132 confirms recent decline has resumed and bearishness remains for further weakness to previous support at 1.1109, however, break there is needed to retain our bearish view and extend subsequent selloff to 1.1075-80 but loss of near term downward momentum should prevent sharp fall below 1.1050, risk from there is seen for a rebound later.

In view of this, we are looking to sell euro on recovery as 1.1175-80 should limit upside. Only above 1.1213 resistance would defer and risk a stronger rebound to 1.1230-35 but upside should be limited to 1.1260-70, bring another decline later.

Oil Prices Are Fairly Stable This Morning In Asian Trading

Market movers today

There are not many data releases in the calendar today. Focus will most likely be on the developments in the oil markets where prices have fallen back significantly over the past month. The sharp falls are weighing on global risk sentiment and therefore have been setting off significant movements in financial markets in the past days.

In the UK, focus remains on the political situation with the Queen's Speech (which out lines the government 's legislative agenda for the coming parliament ary session) taking place today (despite Theresa May not having agreed on a deal with the Democratic Unionist Party (DUP) yet ).

In the Scandi region, focus will be on Norwegian unemployment figures and Swedish economic survey numbers this morning.

Selected market news

U.S. stocks retreated last night from all-time highs as crude oil slid into a bear market on concern the global supply glut will persist. This morning Asian equity markets are also in the red with notably energy dependent Australian equity markets being pushed lower by 1.5%. The only exception being mainland Chinese shares after they were added to MSCI's emerging markets index.

After heavy falls over the past days, oil prices are fairly stable this morning in Asian trading. The Brent oil price is trading just short of USD 46 per barrel which is the lowest level since early November, when US president Trump was just elected. Headlines focus on higher supply from Libya, but in our view the important story in the oil market now is one of weakening demand. Interestingly, API data showed rising gasoline stocks and falling crude stocks. The political turmoil in the Middle East will also be in focus, especially after this morning's news of a reshuffle of the Crown Prince in Saudi Arabia. The weak oil price is also weighing on currency markets, with oil-dependent oil currencies such as the NOK, AUD and RUB feeling the pinch (for more on NOK ahead of the Norges Bank meeting tomorrow, please see the FX section), while the JPY is seeing support on the back of weak global risk sentiment . Meanwhile, the USD is seeing strength overnight as Fed officials yesterday continued to reiterate a moderately hawkish stance on monetary policy.

Focus will also be on the UK today where the Queen's Speech is held in the UK parliament. The speech is given at a time when Theresa May is struggling to strike a deal with the DUP on a new government programme. It will therefore be interesting to see what priorities are highlighted in the speech. Meanwhile, the GBP had a difficult overnight session after BoE Governor Carney said now is not the time to hike, effectively slapping down the three hawkish dissenters who voted for a hike last week and S&P Ratings said they are most likely to cut the UK's rating, and that it will not have to wait to see the terms of the final Brexit deal before doing so. We note that all three ratings agencies have the UK on out look negative. Moody's still assigns a triple-A rating, while S&P and Fitch are two notches below that .

Currencies: Dollar Still Looking For Guidance. Sterling Testing Support

Sunrise Market Commentary

- Rates: Risk sentiment and oil prices key for trading

Today's eco calendar is empty suggesting more low volume trading in tight ranges (both for the Bund and US Note future). There are no scheduled central bank speeches. Risk sentiment and oil prices could guide global trading. Core bonds can profit in a daily perspective if Europe copies yesterday's correction lower on WS and oil extends losses. - Currencies: Dollar still looking for guidance. Sterling testing support

The moves in the dollar were limited yesterday as there were no important data or events. Today's trading pattern might be similar. Sterling reversed the post-BoE rebound on soft Carney comments. Political uncertainty might push EUR/GBP for a test of 0.8854/66 resistance.

The Sunrise Headlines

- Asian stocks weakened after their US peers pulled back from record highs and the oil price fell to a seven month-low. Chinese stocks were the only exception as MSCI decided to add some Mainland A-shares to its global benchmark equity index. Chinese indices reacted by going slightly higher.

- Italy's 5-star movement is trying to shed its Eurosceptic image and called the bid for a euro referendum a “plan B”, only to be executed if negotiations on reforming the euro area are unfruitful.

- Intesa Sanpaolo is in talks with Italy's government and EU regulators about taking control of the good assets of two struggling banks as Italy seeks to head off a renewal of concerns about the solidity of its banking system.

- Angela Merkel says she is open to the idea of giving the eurozone a single finance minister and a common budget, offering conditional support to one of French President Emmanuel Macron's signature policies.

- With no deal in sight between the Conservatives and the DUP party, the government will likely present its legislative programme with no guaranteed majority today for the Queen's speech. The speech votes are planned for the 28th and 29th.

- The only significant items on the eco-calendar are the Queen's speech in the UK, existing home sales in the US, the BoJ Kuroda speech in Tokyo and the sale of German bonds (30-yr).

Currencies: Dollar Still Looking For Guidance. Sterling Testing Support

USD is still looking for guidance

With no important eco data on the agenda, major dollar cross rates traded again uneventful. EUR/USD hovered mostly slightly north of 1.1150, but lost a few ticks later in the session. USD/JPY touched a short-term top in the 111.75/80 area, but reversed earlier gains as core yields and equities declined. EUR/USD finished at 1.1134 (from 1.1149). USD/JPY closed at 111.45 (from 111.53).

Overnight, Asian equities lose ground (0.5%), but less than Wall Street yesterday, which is good. Chinese equities outperform slightly after their inclusion in the MSCI benchmark indices. Oil ($46 p/b for Brent) struggles to prevent further losses, but has currently no direct link with USD trading. USD/JPY is losing a few ticks on the modest risk-off sentiment, currently trading in the 111.30/35 area. EUR/USD is unchanged (1.1135).

The eco calendar remains unattractive today. In the US, existing homes sales and mortgage applications will be published. Housing data are seldom a mover for USD trading. However, of late housing data showed a loss of momentum. Another negative surprise might be slightly negative for the dollar intraday. Technical considerations and equity sentiment will again dominate EUR/USD and USD/JPY trading. Asian equities and the US futures suggest a modest risk-off sentiment. This might be mildly negative for USD/JPY. We take a neutral stance on EUR/USD trading. Yesterday, the pair maintained a cautious negative bias even as sentiment on risk deteriorated throughout the day and yield spreads narrowed. Apparently, the market is still positioned a bit EUR/USD long. Will the pair go for a test of the 1.1110 correction low?

Global context. After last week's relatively hawkish Fed statement, the topside in EUR/USD is better protected and a cautious sell-on upticks approach is advised. However, sustained USD gains need better US eco data, supportive Fed comments and/or higher US yields. With few high profile US data this week, it is doubtful that the US currency will receive this support. If the equity rally slows, so might be the USD rebound

Technical picture

The USD/JPY rally ran into resistance in early May. A mini sell-off mid-May made the short-term picture negative, driving the pair further down in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair beyond a first minor resistance at 110.81. A break beyond the 112.13 correction top would improve the ST-picture. The day-to-day sentiment improved slightly of late, but we remain cautious to forecast a U-turn.

Early May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and US political upheaval propelled EUR/USD north of the 1.1023 range top to a corrective top. The pair tested the 1.1300 area going into the FOMC decision, but the test was rejected. So the Trump top/correction top at 1.1300/1.1366 proved to be a solid resistance. USD sentiment will have to become really negative to clear this hurdle. EUR/USD 1.1110 is a first minor support. A return below 1.1023 would indicate that the upside momentum has eased.

EUR/USD: test off 1.1300/66 resistance rejected, but correction remains modest. First support at 1.1110 within reach

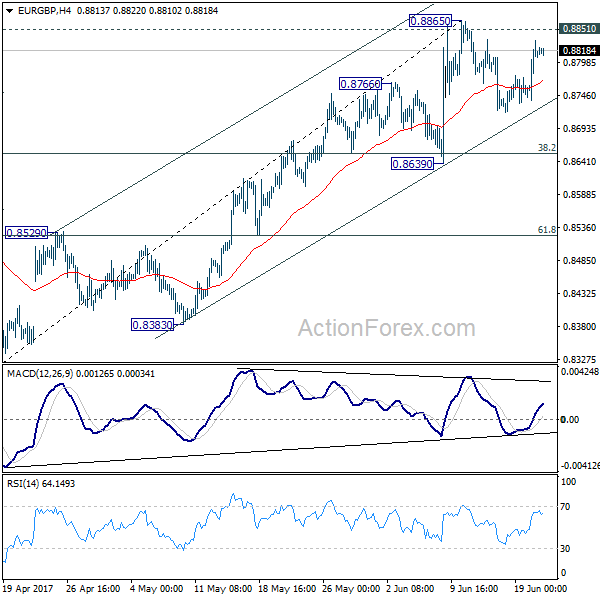

EUR/GBP

EUR/GBP nears recent highs on soft Carney comments

Last week, markets were spooked by an unexpected MPC vote as thee members voted to raise rates to keep inflation in check. Yesterday, BoE governor Carney played another card: ‘Given the mixed signals on consumer spending and business investment, and given the still subdued domestic inflationary pressures, in particular anaemic wage growth, now is not yet the time to begin that adjustment (a rate hike)'. UK bond yields and sterling nosedived. EUR/GBP rebounded north of 0.88. Cable dropped well below the 1.27 barrier.

The UK public finance data will be published today, but the focus will remain on the political scene. The Queen will give her opening speech for the new parliament. However, it is not sure yet that the policy statement can be approved by a political majority as the negotiations between the Conservatives and the DUP are ongoing. The speech as such might not be a big issue for markets, but it illustrates the precarious political situation in the UK. In the wake of yesterday's soft Carney comments, we expect today's context to remain sterling negative.

From a technical point of view, EUR/GBP extensively tested the 0.8854 area (2017 top), but a real break didn't occur. The post-BoE correction halted yesterday. EUR/GBP trades again within reach of the 0.8854/66 resistance. A break would open the way to the 0.90 area. A return below the 0.8655 correction low would indicate easing pressure on sterling. Such a break lower will be difficult. A EUR/GBP buy-on-dips approach is still favoured.

EUR/GBP returns within reach of the 0.8854/66 resistance

Trade Idea : USD/JPY – Buy at 110.65

USD/JPY - 111.29

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.34

Kijun-Sen level : 111.49

Ichimoku cloud top : 111.50

Ichimoku cloud bottom : 111.22

Original strategy :

Buy at 111.10, Target: 112.10, Stop: 110.75

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

As the greenback has retreated after rising marginally to 111.79 yesterday, suggesting consolidation below this level would be seen and pullback to 111.00 cannot be ruled out, however, reckon 110.65 (previous support as well as 38.2% Fibonacci retracement of 108.82-111.79) would limit downside and bring another rise later, only break of said resistance at 111.79 would signal the rise from 108.82 low is still in progress for headway to 111.90-95 (50% projection of 108.82-111.42-110.65) but upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold from here.

In view of this, we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).

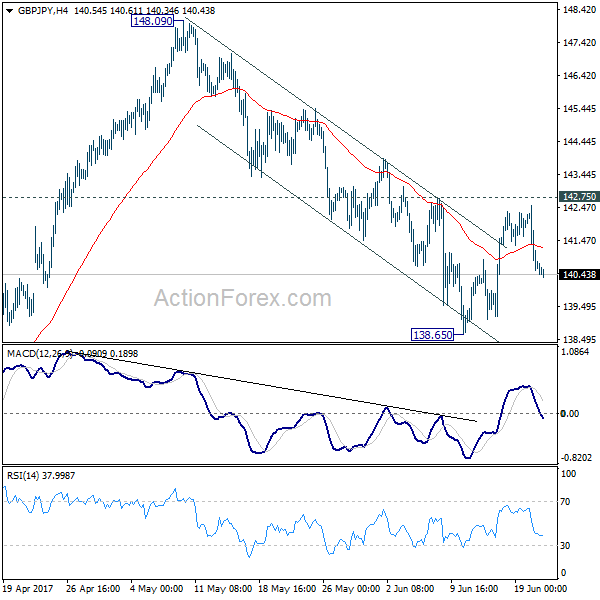

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.01; (P) 141.27; (R1) 141.97; More....

Intraday bias in GBP/JPY remains neutral for the moment. on the downside, break of 138.65 will resume the decline from 148.09. In that case, we'd look for bottoming signal around 135.58, which is close to 135.39 fibonacci level, to bring rebound. On the upside, break of 142.75 should confirm completion of the fall from 148.09 and turn bias back to the upside for this resistance.

In the bigger picture, while the fall from 148.09 is deeper than expected, we're not bearish in the cross yet. Price action from 148.42 is possibly developing into a sideway pattern with fall from 148.09 as the third leg. Deeper decline could be seen but we're looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Rise from 122.36 is still mildly in favor to resume at a later stage. However, sustained break of 135.58/39 will confirm reversal and target a retest on 122.36 low.

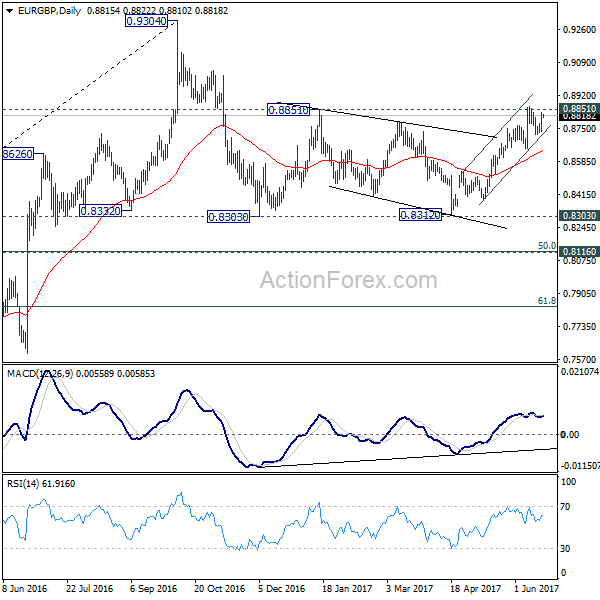

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8731; (P) 0.8755; (R1) 0.8775; More...

EUR/GBP is staying in consolidation from 0.8865 and intraday bias remains neutral at this point. In case of another fall, we'd expect strong support from 0.8639 to contain downside and bring rise resumption. Decisive break of 0.8851 resistance will pave the way to retest 0.9304 high. However, break of 0.8639 support will now indicate near term topping and bring deeper pull back 0.8529 resistance turned support and below.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

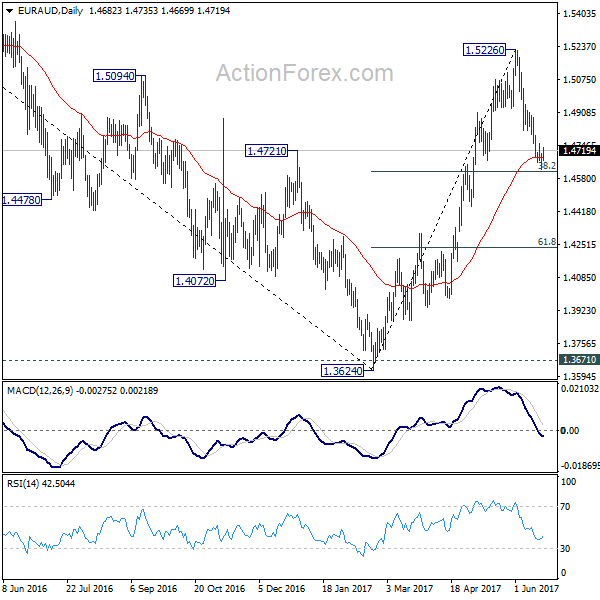

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4641; (P) 1.4673; (R1) 1.4721; More...

Further decline is mildly in favor in EUR/AUD as long as 1.4754 minor resistance holds. Break of 38.2% retracement of 1.3624 to 1.5226 at 1.4614 will pave the way to 61.8% retracement at 1.4236 and possibly below. Meanwhile, break of 1.4754 will indicate that the cross could have defended 1.4669 support. In that case, intraday bias will be turned back to the upside for retesting 1.5226 high.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4669 support will dampen this bullish view. We'll assess the outlook later after looking at the structure and depth of the pull back.

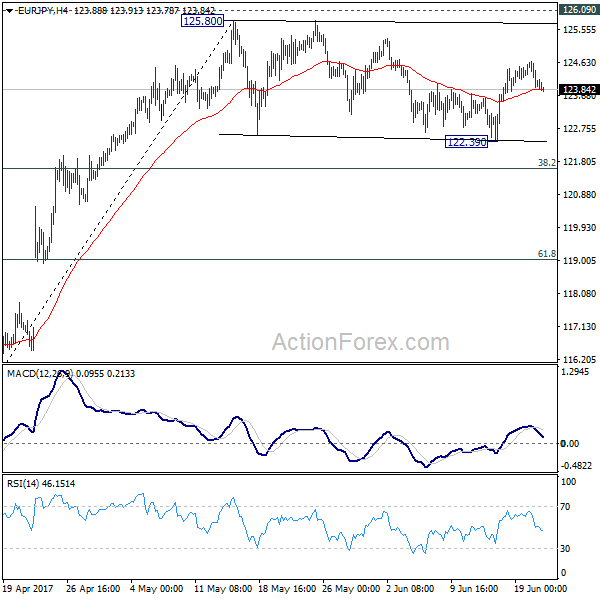

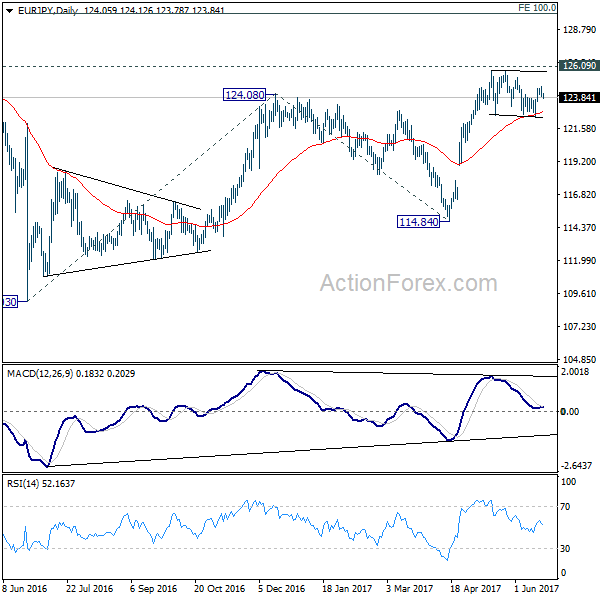

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.79; (P) 124.21; (R1) 124.51; More...

EUR/JPY's consolidation from 125.80 is set to extend further and intraday bias is turned neutral first. In case of another fall, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption. On the upside, decisive break of 126.09 resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.