Sample Category Title

GOLD Monitoring Uptrend Channel, SILVER Selling Pressures Continues, CRUDE OIL Testing Support Given At $43.76.

GOLD Monitoring uptrend channel.

Gold is now monitoring the lower bound of the uptrend channel. Hourly support is located at 1249 (intraday low). Stronger support is given at 1214 (09/05/2017 low). Expected to show renewed upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Selling pressures continues.

Silver declines. Closest support is given at 16.44 (18/05/2017 low). Strong support is given at 16.06 (09/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Testing support given at $43.76.

Crude oil is finally continuing its decline since the recent collapse from $52. Support is given at a distance 43.76 (05/05/2017 low). Expected to show further decline.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Short-Term Buying Pressures Are Fading, EUR/GBP Surging, EUR/CHF Pushing Lower.

EUR/JPY Short-term buying pressures are fading.

EUR/JPY has bounced back after breaking hourly support given at 122.56 (18/05/2017 low) has been broken. Hourly resistance can be found at 125.82 (16/05/2017 high). Major support is given at 114.90 (18/04/2017 low).

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Surging.

EUR/GBP is pushing higher towards support given at 0.8866 (12/06/2017 high). Other support can be found at 0.8652 (08/06/2017 low). Expected to further decline.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Pushing lower.

EUR/CHF's bearish pressures are back. Yet, we believe that the medium-term pattern suggests us to see continued bearish pressures towards hourly support that can be found at 1.0792 (03/05/2017 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

Sterling Off As Carney Plays Down Rate Hike Chances

It's shaping up to be another rather quiet session on Tuesday, with US futures pointing marginally higher and the economic calendar very light on notable releases.

The focus remains broadly on the UK, which began negotiations with the EU on its exit on Tuesday, while we've also heard from Chancellor Philip Hammond this morning as well as Bank of England Governor Mark Carney, both of whom spoke at the delayed Mansion House dinner in London.

Sterling is coming under pressure again on Tuesday after BoE Governor Mark Carney defended the need to resist raising interest rates, despite three policy makers voting to do so at the meeting last week. Rising inflation is clearly a concern among certain policy makers, having risen to 2.9% last month which is well above the central banks 2% target, but Carney was keen to stress that other factors have to be considered.

Prior to last week's meeting, markets had not anticipated a rate hike until at least 2019, prompting the pound to rally after the announcement. While the move was quite sharp, it hasn't developed into anything more which would suggest investors are very much on the same page as Carney who argued that against the backdrop of anaemic wage growth and mixed consumer activity and business investment, it would not be appropriate to raise rates. This may mean tolerating higher inflation in the short term but under the circumstances, I think this remains the most suitable and likely response.

With Brexit negotiations now officially underway, it will be interesting to see whether sterling remains as vulnerable to the constant flow of updates and commentary, especially given the friendlier tone that both sides adopted on day one. Perhaps all the fighting talk of the last year was just simply both sides positioning themselves ahead of difficult negotiations and now they've actually started, things may become a little quieter on that front. Still, it's very early days and should the talks turn nasty, I wouldn't be surprised to see both use the media to vent their frustrations which could be bad for the pound at times.

Euro Subdued As German Inflation, Eurozone Current Account Disappoint

The euro is showing little movement in the Tuesday session, as EUR/USD is trading at 1.1150. On the release front, German PPI declined by 0.2%, weaker than the forecast of -0.1%. This marked the first decline since September 2016. Elsewhere, the Eurozone's current account surplus dropped sharply to EUR 22.2 billion, compared to a forecast of EUR 31.3 billion. In the US, today's major event is Current Account. On Wednesday, the US releases Existing Home Sales and Crude Oil Inventories.

The political landscape has finally settled in France, after two months of elections. On Sunday, President Emmanuel Macron easily won a majority in presidential elections. Macron's En March party won about 60% of the seats in the National Assembly. However, voter turnout was very low, at just 42%, as voter fatigue and the expected result contributed to a low turnout. Still, there is no arguing that it's an impressive victory for the young and charismatic Macron, whose party is barely a year old. Macron ran on a pro-business agenda, promising to relax regulations and reform labor laws in order to make the French economy more competitive, but France's powerful trade unions are sure to push back against any legislation that will take away rights or benefits from workers. The unions have not shied away from going on strike or organizing mass protests in past conflicts with the government, so Macron will be hard-pressed to implement reforms while keeping peace on the labor front. Macron is also staunch supporter of the EU, and hopes to raise France's stature and clout in Europe, especially with Britain heading out the door.

One year after the Brexit referendum, which sent shock waves across Britain and the European Union, formal negotiations between the two sides began on Monday in Brussels. Both sides were on their best behavior, and the two chief negotiators even exchanged gifts. The parties published a concise Terms of Reference for the negotiations, which provided an outline of the talks as set by the Europeans. The paper pointedly did not mention trade talks, but rather listed the initial issues that will be discussed: 1) legal status of EU citizens in the UK; (2) Northern Ireland/Ireland border; and (3) financial obligations of the UK to the EU. With Prime Minister May trying to cobble together a minority government, her position is much weaker than before the disastrous election, and the British position has become more flexible. Philip Hammond, the British finance minister, has said that he wants a business-friendly and pragmatic Brexit and that no deal would be bad for the UK. He did, however, warn the Europeans not to craft an agreement that punished the UK for leaving the club. The negotiations are expected to resume on July 10, when the parties will delve into substantial issues.

USD/CHF Riding Higher Within Symmetrical Triangle, USD/CAD Trading Lower, AUD/USD Wide-Open For Another Rally.

USD/CHF Riding higher within symmetrical triangle.

USD/CHF is pushing higher. Hourly resistance can be found at given at 0.9771 (09/06/2017 high). Strong resistance is given at 1.0107 (10/04/2017 high). Expected to show continued short-term bullish pressures.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Trading lower.

USD/CAD has strongly declined and is now consolidating. Hourly support lies at 1.3165 (14/06/2017 high). Expected to show continued weakness towards support given at 1.3010 (16/02/2017 low)

In the longer term, the pair lies in a bullish channel since a year. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Wide-open for another rally.

AUD/USD is pushing higher since the pair has failed to reach hourly support given at 0.7329 (09/05/2017 low). The technical structure is clearly positive and the pair should head towards resistance at 0.7750 (21/03/2017 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Short-Term Weakness, GBP/USD Strong Short-Term Bearish Pressures, USD/JPY Strengthening.

EUR/USD Short-term weakness.

EUR/USD is trading lower. The pair is still trading below strong resistance given at 1.1300 (09/11/2017 high). Hourly support can be found at 1.1076 (18/05/2017 low). Stronger support lies at 1.0842 (11/05/2017 low).

In the longer term, the momentum is clearly negative. We favour a continued bearish bias towards parity. Key resistance holds at 1.1714 (24/08/2015 high) while strong support lies at 1.0341 (03/01/2017 low).

GBP/USD Strong short-term bearish pressures.

GBP/USD is back below former hourly support given at 1.2757 (21/04/2017 low). Hourly resistance lies at 1.3046 (18/05/2017 high). Expected to test hourly support given at 1.2636 (09/06/2017 low). The road is wide-open for further decline.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Strengthening.

USD/JPY continues to trade higher. Hourly support can be found at 108.89 (14/06/2017 high). Strong support is located at 108.13 (17/04/2017 low). Expected to show continued increase towards resistance given at 112.13 (24/05/2017 high)

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Technical Outlook: Spot Gold – Limited Correction Seen Ahead Of Fresh Extension Lower, 200SMA Marks Next Target

Spot Gold corrects Monday's strong fall which found footstep at $1243, with recovery attempts being so far capped by 100SMA ($1247).

Strongly oversold slow stochastic on daily chart warns of further correction, but no firmer bullish signal seen so far.

Extended upticks would face another barrier at $1252 (Fibo 61.8% of $1257/$1243 / falling hourly cloud base) which should ideally cap before larger bears resume.

Repeated close below $1245 (Fibo 61.8% of $1214/$1296 rally) is needed to signal bearish continuation through $1243 towards next strong support at $1238 (200SMA).

Res: 1247, 1252, 1255, 1257

Sup: 1245, 1243, 1238, 1233

Technical Outlook: WTI Oil – Near-Term Action Is Directionless While Holding Within $44.00/$45.00 Range

WTI Oil stays within narrow consolidation for the fourth consecutive day after extended recovery attempts stalled at $45.00 on Monday. Further directionless trading could be expected while the price holds within $44.00 / $45.00 range, with break of either side expected to generate direction signal.

Upside remains limited for now despite strongly oversold daily studies, however, stronger correction cannot be ruled out on firmer bullish signal on reversal of slow stochastic from oversold zone on daily chart.

Bullish scenario needs break above $45.07 (Fibo 38.2% of $46.69/$44.07 downleg) to trigger further recovery.

On the other side, persisting strong bearish sentiment maintains downside pressure and sees final push towards $43.74 target (05 May low) after limited correction.

Res: 44.67, 45.07, 45.38, 45.69

Sup: 44.07, 43.74, 43.06, 42.72

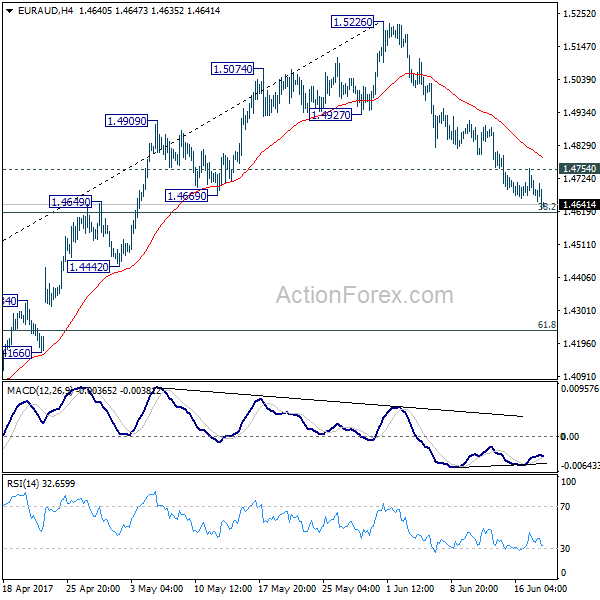

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4643; (P) 1.4699; (R1) 1.4727; More...

EUR/AUD's fall from 1.5226 resumed after brief consolidation. The break of 1.4669 support argues that rise from 1.3624 is completed at 1.5226 already. Intraday bias is back on the downside. Break of 38.2% retracement of 1.3624 to 1.5226 at 4614 will pave the way to 61.8% retracement at 1.4236 and possibly below. On the upside, above 1.4754 minor resistance will turn bias neutral and bring recovery first.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4669 support will dampen this bullish view. We'll assess the outlook later after looking at the structure and depth of the pull back.

USD/BRL Stuck Above 3.28 For Now, SECO Revises Inflation Path Lower

Brazilian real struggles to recover despite easing uncertainties

The Brazilian real was unable to recover completely from the panic sell-off that took place after the alleged corruption of President Michel Temer. After spiking USD/BRL to 3.40, the real stabilised at between 3.25-3.30, far above the 3.10 level prior to the revelations. However, several indicators suggest that the level of uncertainty has decreased substantially.

First, interest rates erased almost completely gains with the 2-year swaps rates easing to 9.22% compared to 11% on May 15th. On the longer end of the curve, the move is similar as the 10-year sovereign yields eased to 10.37% compared to 11.73%. However, the only black mark is on the CDS rates side. CDS rates on Brazilian sovereign debt have not return to their pre-revelation levels yet - the 5-year and 10-year are still higher by 40bps and 46bps, respectively - suggesting that investors are still worried about further turmoil in the political landscape. We believe it is just a matter of time.

Secondly, the level of implied volatility has been decreasing over the last few weeks. 1-month ATM implied volatility on USD/BRL has returned to 12.6% on Monday compared to more than 23.3% a month ago. Furthermore, the 1-month 25-delta risk reversal measure, which measures the difference between the price of a call and a put, has eased to 2.51% from more than 5% in mid-May, suggesting that the market is not anticipating further upside in USD/BRL.

Overall, it seems that the market still needs time to digest the latest political developments in Brazil. We believe that the real has room to appreciate against the greenback and we anticipate that USD/BRL has only one way to go: down.

Swiss economy: Low inflation is still a concern for Bern

A week after the SNB kept rates unchanged, the State Secretariat for Economic Affairs in Bern has issued economic forecasts for Switzerland. The GDP growth in 2018 is expected to reach 1.9% y/y (currently at 0.9%). In the same time, the SECO is forecasting exports to reach 3.7% (currently below 3%). Imports are also expected to take a jump to 3.8%. Consumer prices forecasts are the one weak point and the SECO sees consumer prices declining by 0.3% a year from now.

The strong franc has not prevented the SECO from showing its optimism on the Swiss economy. We tend to believe that current levels are still sustainable for the Helvetic country. In the same time, FX reserves are reaching almost CHF 700 billion which shows the massive effort to stabilise the CHF. We do not believe that the central bank will diminish its intervention and the balance sheet is set to stay very large.

Upside pressures on the CHF will likely continue. The currency is very dependent on the ECB monetary policy. In the medium-term, markets seem to expect the ECB to provide some hints about a further tightening path, which would provide some relief to the currency. For the time being, we remain long CHF.