Sample Category Title

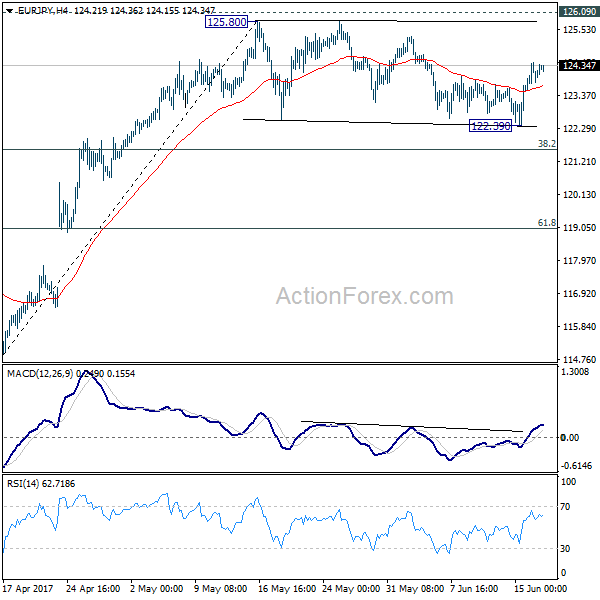

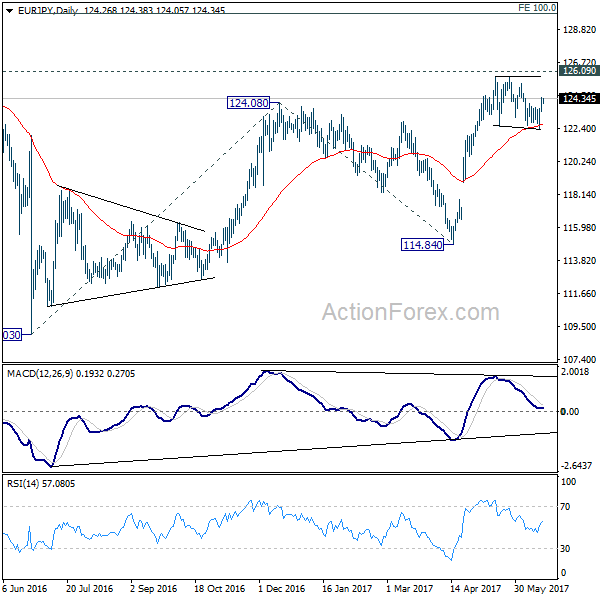

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.61; (P) 124.03; (R1) 124.52; More...

Intraday bias in EUR/JPY remains mildly on the upside for 125.80/126.09 resistance zone. Decisive break of 126.09 will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. In case of another fall as consolidation from 125.80 extends, we'd still expect strong support from 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0877; (P) 1.0890; (R1) 1.0916; More...

Intraday bias in EUR/CHF stays neutral first. We're favoring the case that pull back from 1.0986 has completed at 1.0837 already. Above 1.0907 will turn bias to the upside for retesting 1.0986/0999 resistance zone. Below 1.0836 will extend the correction. Still, we'd expect strong support from 1.0791/0872 support zone to bring rebound.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

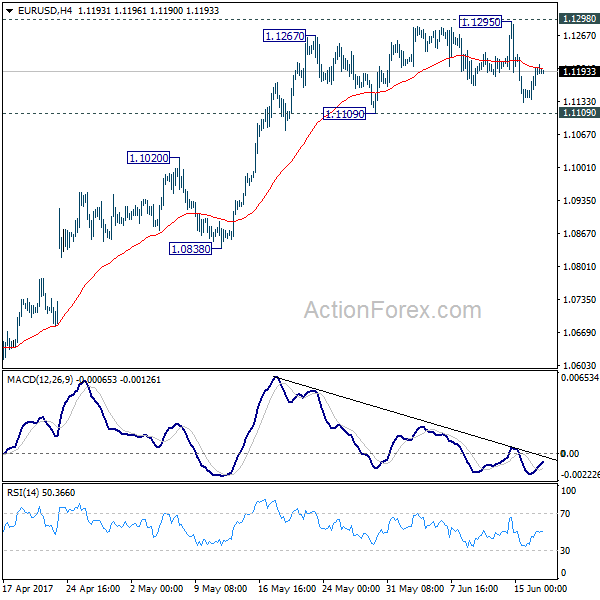

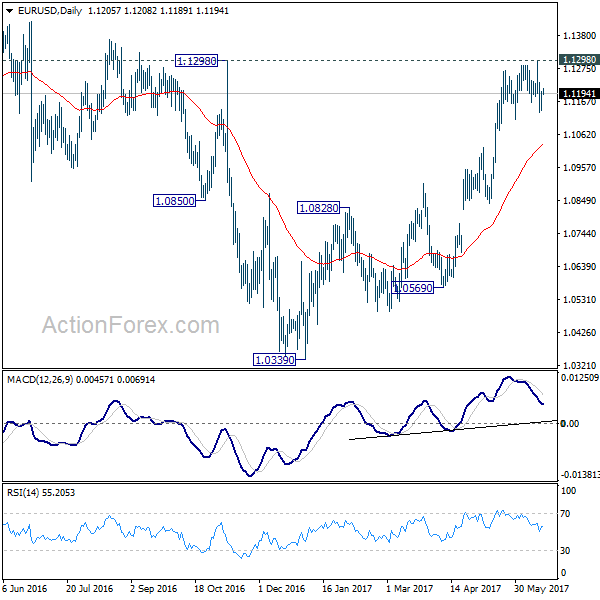

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1154; (P) 1.1177 (R1) 1.1217; More....

Intraday bias in EUR/USD remains neutral for the moment. Focus stays on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0932). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

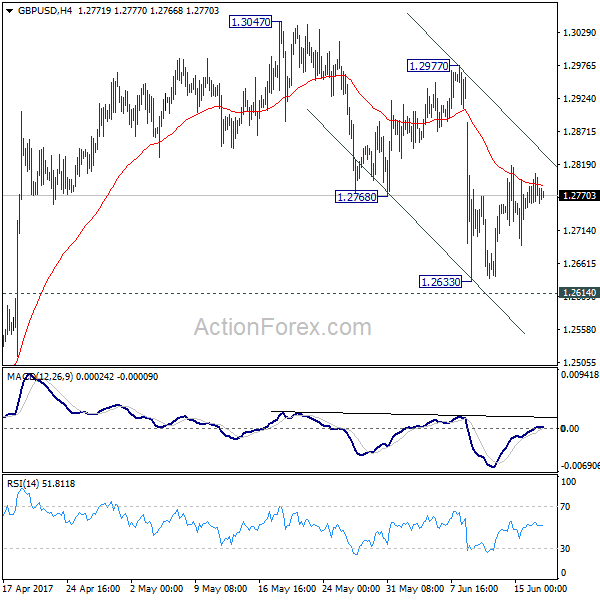

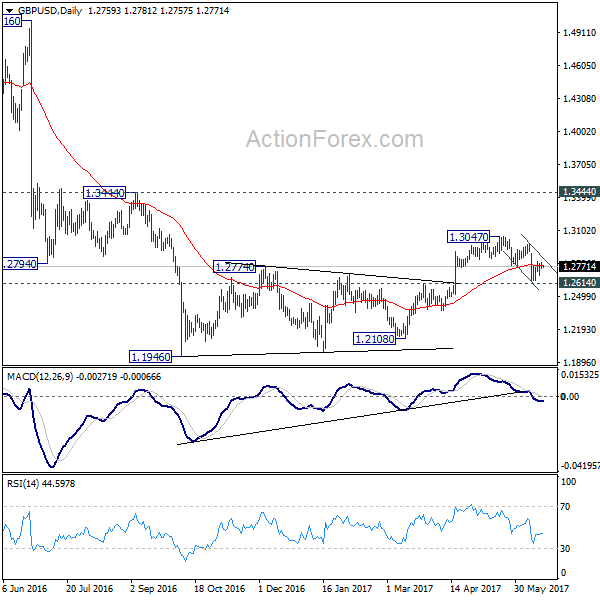

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2746; (P) 1.2775; (R1) 1.2801; More...

Intraday bias in GBP/USD remains neutral for the moment. With 1.2977 resistance intact, we're still favoring the bearish case. That is, consolidation pattern from 1.1946 has completed at 1.3047 already. Break of 1.2614 resistance turned support should confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2977 will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

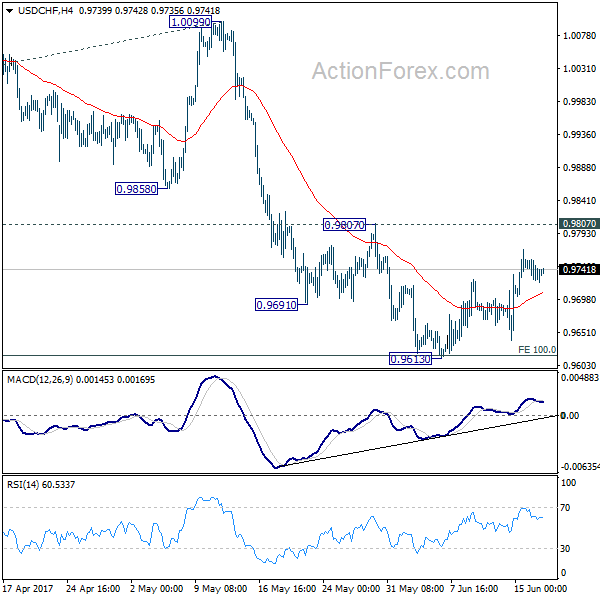

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9724; (P) 0.9740; (R1) 0.9755; More.....

Intraday bias in USD/CHF remains neutral as the consolidation from 0.9613 might extends. still, as long as 0.9807 resistance holds, near term outlook remains bearish as deeper fall is expected. Below 0.9613 will extend the whole decline from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

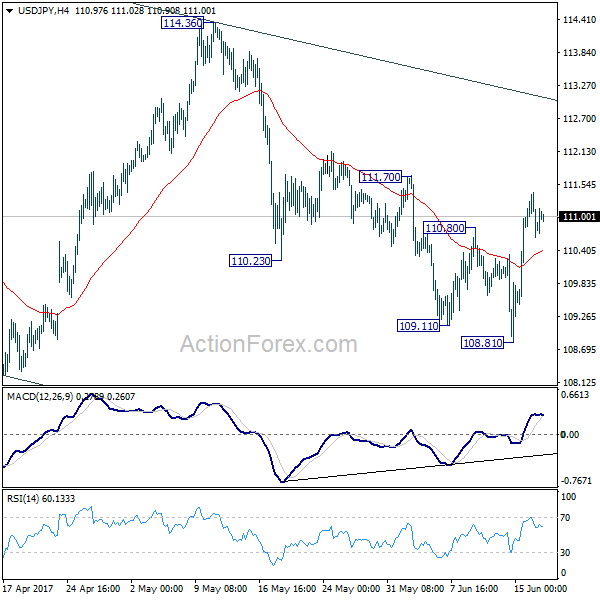

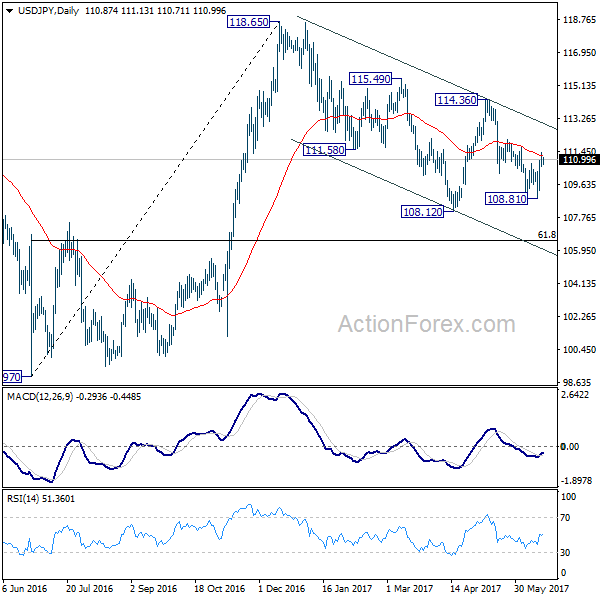

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.52; (P) 110.97; (R1) 111.29; More...

Intraday bias in USD/JPY remains on the upside as rise rebound from 108.81 is expected to continue to near term channel resistance (now at 113.06). Sustained break there will suggest that whole pull back from 118.65 has completed at 108.12 already. In such case, further rise should be seen to 114.36 resistance for confirmation. Nonetheless, break of 108.81 will still extend the fall from 118.65 through 108.12 low before completion.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

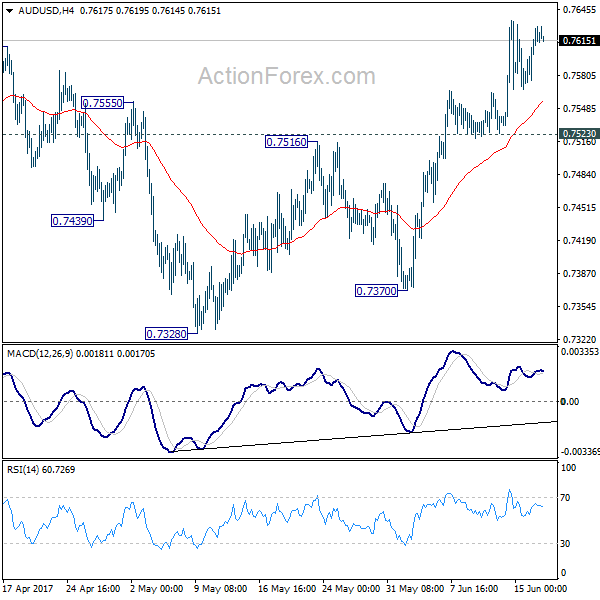

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7584; (P) 0.7607; (R1) 0.7638; More....

With 0.7523 support intact, further rally is seen in AUD/USD for 0.7748 resistance and above. At this point, there is no clear sign of range breakout at. Hence, we'd be cautious on topping again as it approaches medium term fibonacci level at 0.7849. Meanwhile, break of 0.7523 will argue that rebound from 0.7328 is possibly completed. In that case, intraday bias will be turned back to the downside for 0.7370 support.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8116) and above.

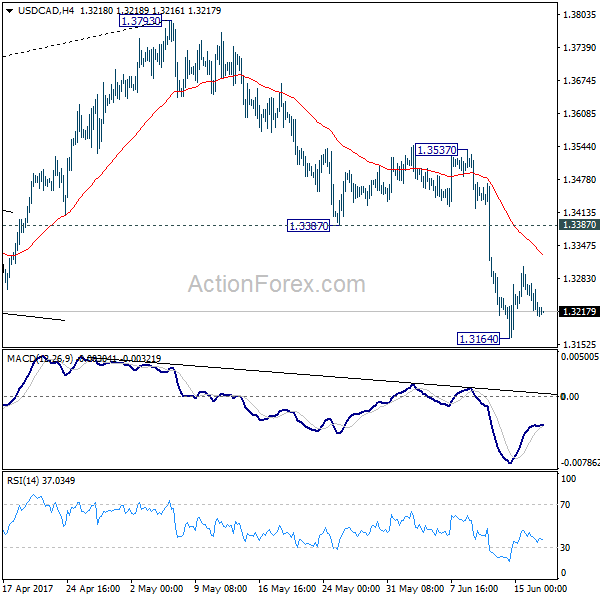

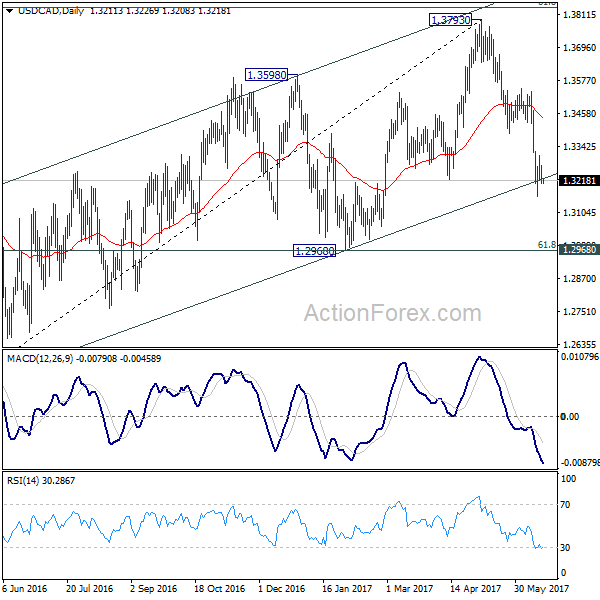

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3190; (P) 1.3231; (R1) 1.3254; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.3164 might extend. In case of another rise, upside should be limited by 1.3387 support turned resistance and bring fall resumption. We're holding on to the view that corrective rise from 1.2460 has completed at 1.3793 already. Below 1.3164 will target 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

Yen Lower after Trade Balance Miss, Sterling Mildly Higher as Markets Eye Day One of Brexit Negotiations

Yen's weakness continue in quiet trading today and trades a touch softer after trade balance release. But overall, the markets are trading in tight range. The only exception is New Zealand Dollar which is resuming this month's broad based rally ahead of RBNZ rate decision on Thursday. Sterling recovers mildly as Brexit negotiations are finally starting today. Dollar and Euro are mixed. In other markets, gold is trading in tight range between 1250/60 for the moment. WTI crude oil is also range bound below 45 handle.

Brexit negotiation finally starts

UK is set to finally start formal Brexit negotiations with EU in European Commission buildings in Brussels today. UK's Brexit Secretary David Davis said that there is a "long road ahead" but that will lead to a "deep and special partnership", "a deal like no other in history". He also pledged to approach the difficulties in a "constructive way". The negotiations would start with EU's top priorities including the divorce bill, rights of citizens and border of Ireland. Meanwhile, EU's chief negotiator Michel Barnier would report in October this year on whether there are sufficient progress to move on to phase two of trade agreements. And it's expected that the whole talks would last until October 2018 before making an agreement. Davis and Barnier would be meeting for one week every month and return to their base to develop the positions.

Yen weakens after trade surplus miss

In Japan, trade surplus narrowed to JPY 0.13% in May, below expectation of 0.35T. Export growth was flat monthly at 0.0% mom. But annually, exports jumped 14.9% yoy, highest since 2015. Nevertheless, that was below expectation of 18.2% yoy. It's also overshadowed by the 0.3% mom, 17.8% yoy rise in imports. Yen trades a touch lower today, accompanying the rise in Asian equities. Nikkei is back above 20000 handle and is trading up 0.6% at the time of writing. Hong Kong HSI is trading up 0.95%. Meanwhile, China SSE composite is up 0.66%.

RBA Lowe expects stronger economy ahead

RBA Governor Philip Lowe said in a speech in Canberra that growth in Australia over the next couple of years will be "a bit stronger than it has been recently". And, the "pick-up in the global economy is helping us". He noted that monetary policy continues to provide support to the economy and "survey-based measures of business conditions have improved noticeably". He also added that "employment growth has also strengthened over recent months." But he also warned that wage growth is "unusually low" and averages hours worked have "declined". Also, the "nature of employment is changing" while there are higher debt levels for households. He emphasized the need to watch these issues carefully.

RBNZ a focus in a light week ahead

The economic calendar is rather light today and the only notable events are speeches of Bundesbank chief Jens Weidmann, New York Fed President William Dudley and Chicago Fed President Charles Evans. Looking ahead, RBNZ rate decision is a key focus this week and it's expected to keep the OCR unchanged at 1.75%. RBA and BoJ will release meeting minutes while ECB will release monthly economic bulletin. The more important economic data are scheduled to release towards the end of the week, including Canada retail sales and CPI and Eurozone PMIs.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3190; (P) 1.3231; (R1) 1.3254; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.3164 might extend. In case of another rise, upside should be limited by 1.3387 support turned resistance and bring fall resumption. We're holding on to the view that corrective rise from 1.2460 has completed at 1.3793 already. Below 1.3164 will target 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Jun | -0.40% | 1.20% | ||

| 23:50 | JPY | Trade Balance (JPY) May | 0.13T | 0.35T | 0.10T | 0.16T |

| 1:30 | AUD | New Motor Vehicle Sales M/M May | 2.90% | 0.30% | ||

| 23:00 | USD | Fed's Evans Speaks in New York |

AUD Bullishness Looking Poised To Extend

Key Points:

- After a strong prior week, the AUD looks ready to extend gains.

- Fundamentals were largely responsible for recent bullishness.

- Technical bias is also rather bullish.

The Aussie Dollar performed rather well last week which came as a surprise to much of the market given the FOMC’s decision to raise rates. As a result, the question is now being raised, can we expect similar gains in the week ahead or will the bears move back into the driving seat? Fortunately, if we take a look into both the week that was and what is next on the agenda, we may be able to establish a bit of a bias.

Starting with last week, the Aussie Dollar shrugged off the news that the FOMC would be increasing rates by around 25bps last week which, in hindsight, isn’t entirely surprising given the broad pricing in of just such adecision. However, just prior to the announcement, a US Core Retail Sales result of -0.3% m/m was posted alongside disappointing CPI figures which also aided in keeping the pair bullish despite the hike. Combined with the fact that the Australian Jobless Rate slipped to 5.5% in the subsequent session, it is actually little wonder that buying pressure remained in place throughout the rest of the week, ultimately, seeing the pair close all the way up at the 0.7618 handle.

However, what about the week ahead? Well, there isn’t a huge amount of Aussie news available which will mean that the US data is largely going to be driving prices for the pair. Nevertheless, the Australian HPI figure is due out early on and is forecasted at around the 2.2% mark which could be worth watching out for. If we see the forecasted result realised, it could set the AUD up for another solid week of gains. However, any real upside potential will be beholden to the US data which is due to posted in much greater volume. Of these postings, the Existing Home Sales and New Home Sales numbers are the two key prints to watch – the latter of which is expected to improve to 600K this time around. Such an uptick might see early gains moderated away as the week draws to a close, potentially leading to a rather flat week overall.

As for the technical front, the AUD is generally bullish but we are beginning to run into some resistance as a result of the pair moving into overbought territory. More precisely, the 12, 20, and 100 day moving averages transitioned into their most bullish configuration last week which is typically a strong signal for additional gains. Furthermore, the Parabolic SAR reinforces this bias as it remains significantly below price action and is in little danger of inverting anytime soon. The one fly in the ointment is the fact that both stochastics and RSI are now overbought which could put a dampener on any further rallies that might be on the cards.

Ultimately, there seems to be some consensus forming that further gains are indeed possible for the AUDUSD but these are likely to be attained at a reduced pace. Nevertheless, this will largely be dependent on the fundamental side of things coming in better than expected as, despite their clear bias, the technicals are unlikely to have the clout to keep the pair rallying on their own.