Sample Category Title

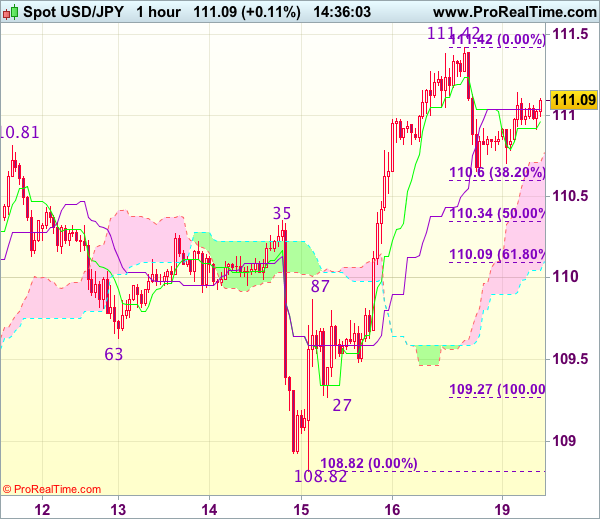

Trade Idea : USD/JPY – Buy at 110.35

USD/JPY - 111.08

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 110.96

Kijun-Sen level : 111.04

Ichimoku cloud top : 110.71

Ichimoku cloud bottom : 110.05

Original strategy :

Buy at 110.35, Target: 111.35, Stop: 110.00

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.35, Target: 111.35, Stop: 110.00

Position : -

Target : -

Stop : -

Dollar’s retreat after meeting resistance at 111.42 has retained our view that consolidation below this level would be seen and pullback to 110.30-35 (50% Fibonacci retracement of 109.27-111.42) cannot be ruled out, however, renewed buying interest should emerge there and bring rebound later, above 111.25-30 would bring retest of 111.42 but break there is needed to confirm the rise from 108.82 low has resumed for retracement of recent decline from 114.37 to 111.60 (50% Fibonacci retracement of 114.37-108.82) and then test of previous resistance at 111.71 but price should falter well below another resistance at 112.13.

In view of this, we are looking to buy dollar on pullback but one should exit on next rise. Below 110.05-10 (61.8% Fibonacci retracement of 109.27-111.42) would abort and signal top has been formed, bring further fall to 109.85-90 and possibly towards 109.50 but support at 109.27 should remain intact.

Swiss Franc Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.23% against the CHF and closed at 0.9728 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9737, with the USD trading 0.09% higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9724, and a fall through could take it to the next support level of 0.9710. The pair is expected to find its first resistance at 0.9754, and a rise through could take it to the next resistance level of 0.9770.

With no major economic releases in Switzerland today, investors will look forward to global events for further direction.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.3% against the CAD and closed at 1.3214 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.3215, with the USD trading marginally higher against the CAD from Friday’s close.

The pair is expected to find support at 1.3192, and a fall through could take it to the next support level of 1.3169. The pair is expected to find its first resistance at 1.3256, and a rise through could take it to the next resistance level of 1.3297.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

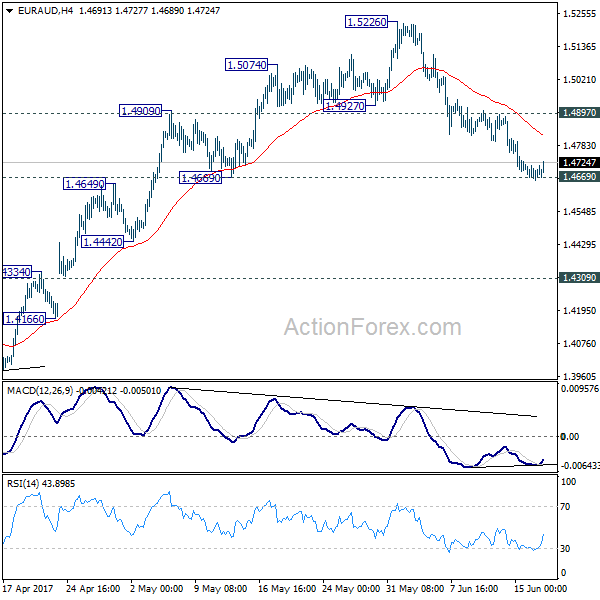

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4664; (P) 1.4730; (R1) 1.4771; More...

No change in EUR/AUD's outlook. We continue to expect strong support from 1.4669, near to 55 days EMA at 1.4689, to contain downside and bring rebound. Break of 1.4897 minor resistance will argue that pull back from 1.5226 has completed and turn bias back to the upside for retesting 1.5226 high first. However, sustained break of 1.4669 will argue that rise from 1.3642 is completed and bring deeper pull back to 1.4309 resistance turned support.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 would extend to 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. However, sustained break of 1.4669 support will dampen this bullish view. We'll assess the outlook later after looking at the structure and depth of the pull back.

The PMI Releases In The Euro Area And The US

Market movers today

The data calendar is fairly thin this week, with the PMI releases in the euro area and the US as the most noteworthy global data releases. The main focus will instead be on political developments in the UK and France in the aftermath of the parliamentary elections in the two count ries on 8 June and yesterday, respectively.

Furthermore, in the UK, Brexit negot iations are bound to begin. We have writ ten intensively about the UK polit ical situat ion since the elect ion, for more see Research UK: May stats (for now) due to Brexit uncertainties, Research UK: Minority government is weak from the beginning and Research UK: Hung parliament adds government risk premium to GBP.

In the US, we will look out for any comments in speeches by FOMC members about what drove the decision on the June rate hike, which in our view was not justified by the data.

Selected market news

Global risk sent iment is solid this morning following a clear win for Emmanuel Macron and his party En Marche in the final round of the parliamentary elect ions in France yesterday. Asian equity markets are most ly up and the typically safe-haven Japanese yen is weaker against the EUR and USD. According to preliminary est imates, Macron’s part y La République en Marche and its cent rist ally Modem secured 355 of the 577 seats in the Nat ional Assembly. Hence, President Macron will enjoy a sizable majority in the French parliament , which will help him in push through an ambit ious reform agenda aimed at reinvigorat ing the French economy. Le Pen and her Party the Nat ional Front secured eight seats in parliament . However, it was also noteworthy that voter turnout was at an historical low at 44%, suggest ing widespread apathy with the current polit ical environment in France.

The Brexit negot iat ions are due to begin between the UK and EU representat ives at 11:00 today in Brussels. The launch of the negot iat ions comes at a time when Theresa May is struggling to hang on to her job. According to the UK newspaper The Times, the PM has 10 days to save her position, as she is facing the threat of rival leadership bids in the Conservat ive party. Some MPs are ready to demand a no-confidence vote, the paper said. Chancellor Philip Hammond told the BBC that Britain will leave the single market , but should aim for a gentle departure. In addition, there is still no power sharing deal with the DUP. Furthermore, the UK may have been hit by yet another terrorist at tack this morning, as a car drove into pedest rians outside a London Mosque, killing one person and injuring 10.

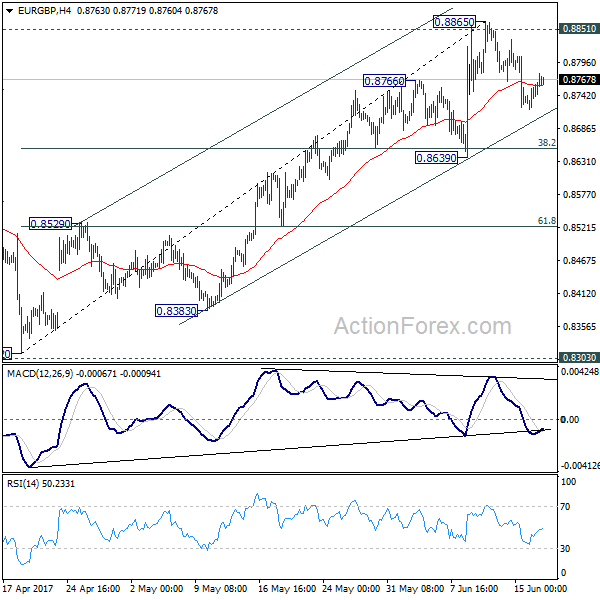

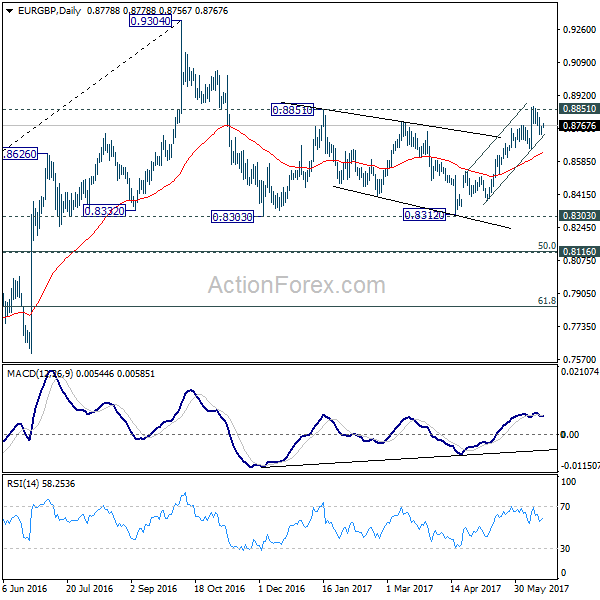

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8732; (P) 0.8748; (R1) 0.8777; More...

Intraday bias in EUR/GBP remains neutral for the moment. While consolidation from 0.8865 might extend, we'd still expect strong support from 0.8639 to contain downside and bring rise resumption. Decisive break of 0.8851 resistance will pave the way to retest 0.9304 high. However, break of 0.8639 support will now indicate near term topping and bring deeper pull back 0.8529 resistance turned support and below.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

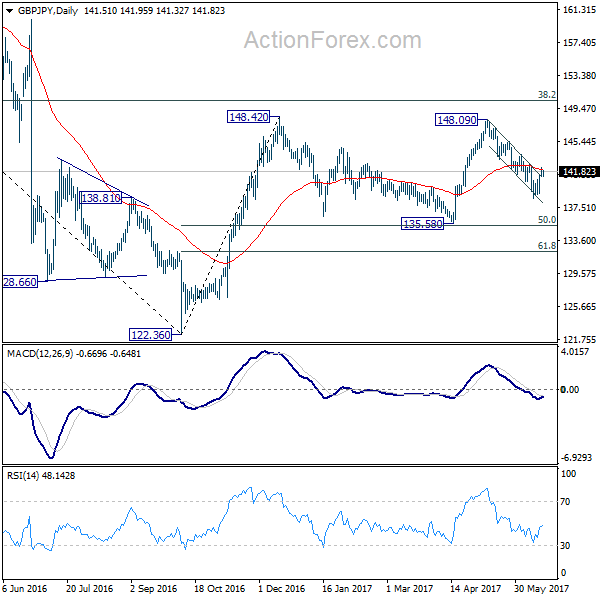

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.17; (P) 141.75; (R1) 142.19; More....

Intraday bias in GBP/JPY remains neutral first. The break of near term falling channel suggests reversal but we're prefer to see break of 142.75 resistance to confirm. In that case, intraday bias will be turned to the upside for 148.09 resistance. On the downside, break of 138.65 will resume the decline from 148.09. But in that case, we'd look for bottoming signal around 135.58, which is close to 135.39 fibonacci level, to bring rebound.

In the bigger picture, while the fall from 148.09 is deeper than expected, we're not bearish in the cross yet. Price action from 148.42 is possibly developing into a sideway pattern with fall from 148.09 as the third leg. Deeper decline could be seen but we're looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Rise from 122.36 is still mildly in favor to resume at a later stage. However, sustained break of 135.58/39 will confirm reversal and target a retest on 122.36 low.

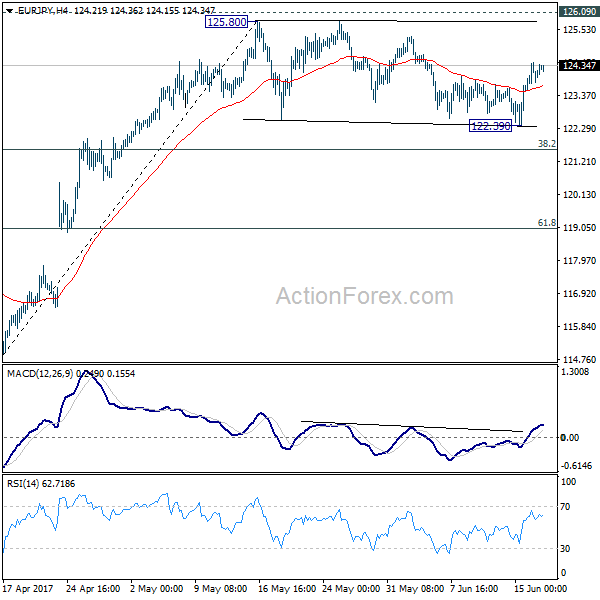

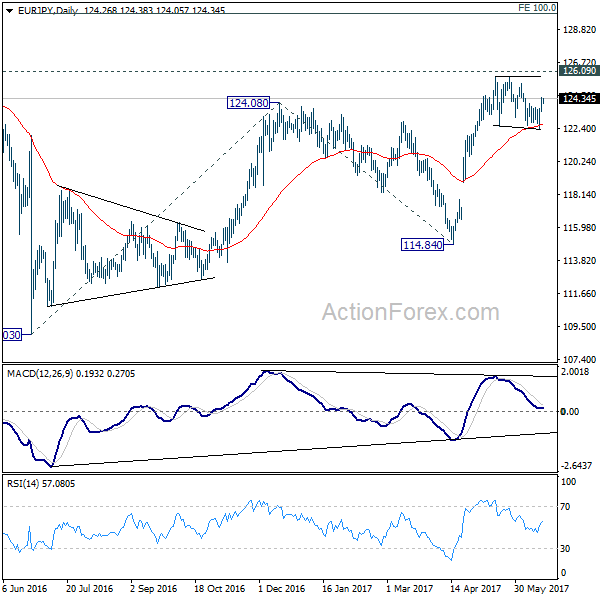

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.61; (P) 124.03; (R1) 124.52; More...

Intraday bias in EUR/JPY remains mildly on the upside for 125.80/126.09 resistance zone. Decisive break of 126.09 will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. In case of another fall as consolidation from 125.80 extends, we'd still expect strong support from 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0877; (P) 1.0890; (R1) 1.0916; More...

Intraday bias in EUR/CHF stays neutral first. We're favoring the case that pull back from 1.0986 has completed at 1.0837 already. Above 1.0907 will turn bias to the upside for retesting 1.0986/0999 resistance zone. Below 1.0836 will extend the correction. Still, we'd expect strong support from 1.0791/0872 support zone to bring rebound.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

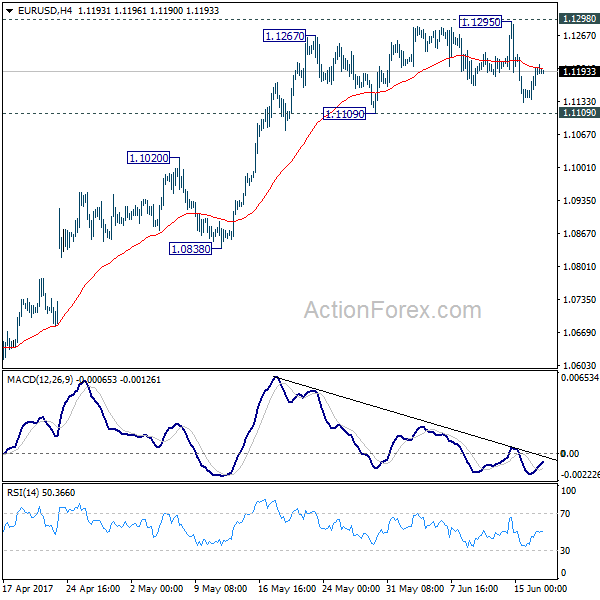

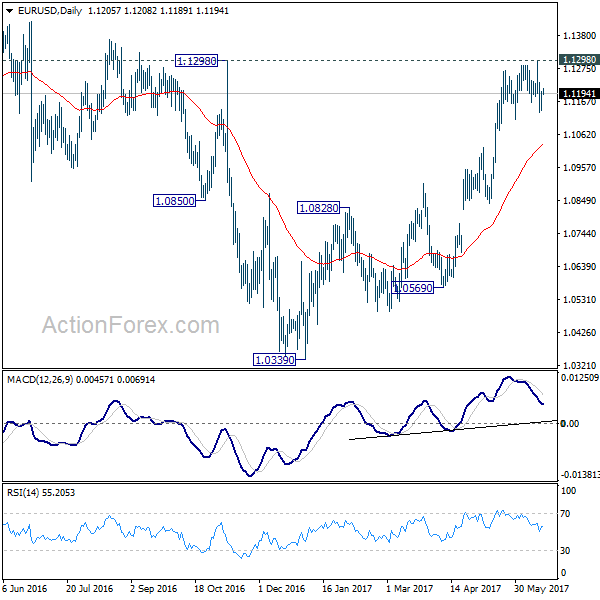

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1154; (P) 1.1177 (R1) 1.1217; More....

Intraday bias in EUR/USD remains neutral for the moment. Focus stays on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0932). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.