Sample Category Title

Japan’s core CPI reaccelerates to 2.7%, driven by energy and rice

Japan’s core CPI (excluding food) rose to 2.7% yoy in November, marking the first reacceleration in three months and exceeding market expectations of 2.6% yoy. Core inflation has remained above the BoJ’s 2% target since April 2022, highlighting persistent price pressures. This increase was attributed to reduced government subsidies for utility bills and a sharp rise in rice prices.

Energy prices surged 6.0% yoy, up from October’s 2.3% yoy gain. Within this category, electricity prices jumped 9.9% yoy, and city gas costs climbed 6.4% yoy. Meanwhile, rice prices soared by a staggering 63.6% yoy, the steepest increase since 1971, driven by last year’s unusually hot summer that disrupted production.

Core-core CPI (excluding food and energy) ticked up from 2.3% yoy to 2.4% yoy, while headline CPI rose to 2.9% from October’s 2.3%. Service prices, a key indicator for BOJ as they often reflect wage dynamics, increased 1.5% yoy, unchanged from the prior month.

NZ’s exports rises 9.1% yoy in Nov, imports up 3.9% yoy

New Zealand’s trade data for November showed a significant improvement, with goods exports rising 9.1% yoy to NZD 6.5B, while goods imports increased by a more modest 3.9% yoy to NZD 6.9B. The resulting trade deficit of NZD -437m was much smaller than the expected NZD -1951m.

Exports saw notable gains across key markets. Shipments to China increased 6.3% yoy, adding NZD 106m, while exports to Australia climbed 8.4% yoy (NZD 62m) and to the US by 12% yoy (NZD 85m). Exports to the EU surged the most, rising 27% yoy (NZD 74m), with shipments to Japan also showing strength at 7.2% yoy (NZD 19m).

On the import side, data was more mixed. Imports from China edged down -1.7% yoy (NZD -29m) and from the EU fell sharply by -16% yoy (NZD -163m). Similarly, imports from South Korea dropped -12% yoy (NZD -61m ). However, imports from Australia rose 14% yoy (NZD 101m) and from the US increased 7.2% yoy (NZD 41 m).

Cliff Notes: A Volatile End to the Year

Key insights from the week that was.

As is tradition in Australia, the Federal Government delivered its mid-year economic and fiscal outlook in the lead up to Christmas. As anticipated, this update highlighted a troubling combination of fading revenue windfalls and persistent strength in spending across critical services, infrastructure, cost-of-living measures and state/local grants. While 2024-25 saw a modest improvement in the budget position, future budget deficits and off-budget spending from 2025-26 through 2027-28 were revised up. Current circumstances and the outlook are consistent with a ‘two-speed’ economy, where the public sector drives growth as private demand remains weak, household spending and business investment continuing to be buffeted by tight policy and cost-of-living pressures.

The impetus for further strong growth in public demand is waning, however; and with headwinds for private sector demand only slowly abating, there is a risk of a ‘shaky handover’ of the growth baton from the government to the private sector. This theme is at the heart of our growth forecasts for 2025 and beyond, explored in detail at the national and state level in our latest Coast-to-Coast report.

Focusing on the consumer, the latest evidence from the Westpac-MI Consumer Sentiment survey continues to underscore a marked improvement in confidence through the second half of 2024. During October and November, consumer sentiment staged a rapid recovery from recession-era levels. While December saw a modest pull-back in the headline index (-2.0%), confidence in current conditions improved, particularly with respect to family finances versus a year ago (+6.9%) and whether now is a ‘good time to buy a major household item’ (4.8%). With the stage 3 tax cuts implemented and cost-of-living pressures slowly receding, a foundation for a pick-up in household consumption in Q4 and 2025 is forming, though only time will tell how strong it is.

Turning to New Zealand, the annual revisions to GDP were largely as anticipated, growth revised up through 2022 and 2023 such that, at March 2024, the economy was 2.3% larger than previously estimated. Unexpectedly though, Q2’s contraction was revised down from -0.2% to -1.1% and Q3 saw a further contraction of 1.0% against expectations for a 0.4% fall. In Q3, the decline in activity was spread across numerous sectors, the squeeze on consumers and businesses from the fight against inflation of particular note. However, some of the weakness stems from temporary factors too. Looking ahead, recovery is expected from Q4, Westpac’s GDP nowcast having moved into positive territory since October. Interest rate relief is providing a benefit, and there is more to come, our New Zealand team now expecting a low for this cycle of 3.25% after a 50bp cut in February and a 25bp reduction in April and May. This week also saw the release of the New Zealand Government’s half-year outlook. Much weaker than expected, the fiscal outlook also highlights the need for accommodative monetary policy.

Further afield, it was a strong finish to a big year thanks to three major central bank meetings.

The FOMC delivered another 25bp fed funds rate cut in December as expected, bringing cumulative easing since September to 100bps. That said, the tone of the statement was non-committal on the policy outlook, and the projections slowed the expected pace of easing. September’s 3.4% fed funds forecast for end-2025 is now not seen until end-2026. The FOMC continue to hold a favourable view of growth and the labour market and so, given persistence in inflation through 2024 and nascent risks related to the imposition of tariffs, are keen to bide their time with policy.

That said, it is evident from their forecasts that downside risks for growth are considered as material as those to the upside for inflation. We also believe it is important to keep a close watch on the risks. However, we anticipate downside activity risks are more probable in 2025 and upside risks for inflation from 2026. This leads us to hold an expectation of four cuts in 2025 against the FOMC’s two, but then two hikes in 2026 when they expect continued policy easing. We expect the inflation risks of 2026 to show persistence too, likely justifying a 10-year yield around 4.80% (along with growing fiscal uncertainty).

The Bank of Japan was the next cab off the rank, holding the policy rate at 0.25%, in line with our expectations. The statement indicated that accommodative policy alongside wages growth has supported inflation and above-potential GDP growth. The BoJ will continue monitoring whether businesses persist with robust wage increases and if that feeds through to prices. Union confederation RENGO has indicated they are aiming to negotiate a 5.0% increase in wages for FY25, with a focus on lifting wages amongst small businesses. This, alongside movements in the exchange rate were considered “more likely to affect prices”. Now that businesses feel more comfortable raising prices, future shocks to import prices, in part due to movements in the currency, are more likely to see consumer prices lift as well. A future move in policy will be predicated on whether RENGO can successfully negotiate a third consecutive strong wage increase and if higher import costs, possibly due to Trump’s policies, prompt businesses to raise prices. Evidence for this will be available in early March 2025, and the next rate increase should occur swiftly thereafter at the March 2025 policy meeting. The BoJ is likely to start winding back hawkish rhetoric after that and assess domestic and global conditions over an extended period before deciding if any further change in the policy stance is warranted.

Finally, the Bank of England met overnight and decided to keep the bank rate steady at 4.75% albeit with a bit of dissent – three out of six members voted to reduce it by 25bp. The labour market was considered ‘in balance’ but uncertainties remain around the outlook, partly a result of poor-quality data. While there has been progress on inflation since the start of the year, allowing the MPC to ease rates, concerns about inflation’s persistence are rising. More causes for uncertainty around disinflation were outlined, not limited to the expansionary measures announced in the Autumn budget and geopolitical tensions. These risks led most of the Committee to agree on a ‘gradual approach to reducing monetary policy’. From here, the Committee will want further evidence that the disinflationary pulse remains intact and that will come from signs that demand has eased to meet the constrained supply capacity. We expect the BoE will cut once per quarter in 2025 and end at a neutral rate of 3.50% by March 2026.

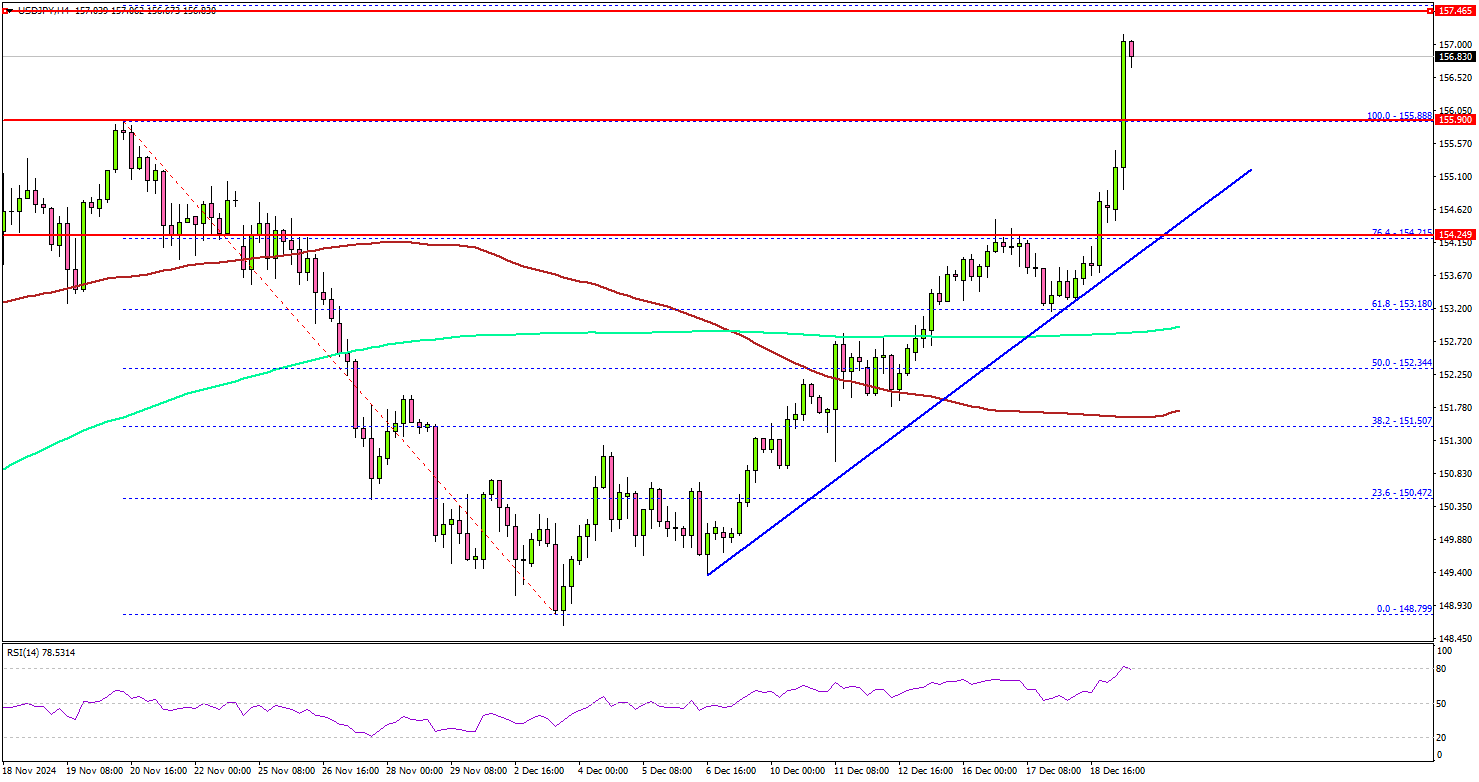

USD/JPY Jumps Post-Fed: Can The Rally Sustain?

Key Highlights

- USD/JPY started a fresh surge above the 154.00 resistance.

- A key bullish trend line is forming with support at 154.50 on the 4-hour chart.

- EUR/USD tumbled toward 1.0350 before correcting some losses.

- AUD/USD and NZD/USD accelerated losses.

USD/JPY Technical Analysis

The US Dollar formed a base above 152.00 against the Japanese Yen. USD/JPY started a fresh surge above the 153.20 and 154.00 levels.

Looking at the 4-hour chart, the pair gained strength above the 154.20 resistance, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It even cleared the 76.4% Fib retracement level of the downward move from the 155.88 swing high to the 148.79 low.

The bulls pushed the pair to a new monthly high above 156.50. On the upside, the pair could face resistance near the 157.40 level. The next major resistance is near the 158.00 level.

A close above the 158.00 level could set the tone for another increase. The next major resistance could be the 159.20 level, above which the price could climb higher toward the 160.00 resistance.

On the downside, immediate support sits near the 155.80 level. The next key support sits near the 155.00 level. Any more losses could send the pair toward the 154.50 level. There is also a key bullish trend line forming with support at 154.50 on the same chart.

Looking at EUR/USD, the pair declined heavily below the 1.0420 support zone before the bulls appeared near the 1.0350 zone.

Upcoming Economic Events:

US Personal Income for Nov 2024 (MoM) - Forecast +0.4%, versus +0.6% previous.

US Core Personal Consumption Expenditure for Nov 2024 (MoM) - Forecast +0.2%, versus +0.3% previous.

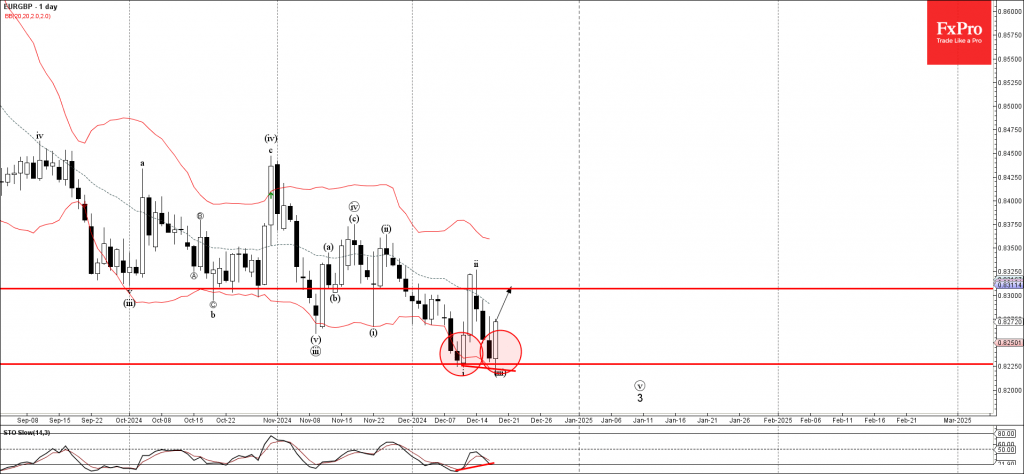

EURGBP Wave Analysis

- EURGBP reversed from support zone

- Likely to rise to resistance level 0.8300

EURGBP currency pair recently reversed up from the support zone located between the key support level 0.8225 (which stopped the previous minor impulse wave i) and the lower daily Bollinger Band.

The upward reversal from this from the support zone is likely to form the daily Japanese candlesticks reversal pattern Bullish Engulfing – of the pair closes today near the current levels.

Given the bullish divergence on the daily Stochastic, EURGBP currency pair can be expected to rise to the next resistance level 0.8300.

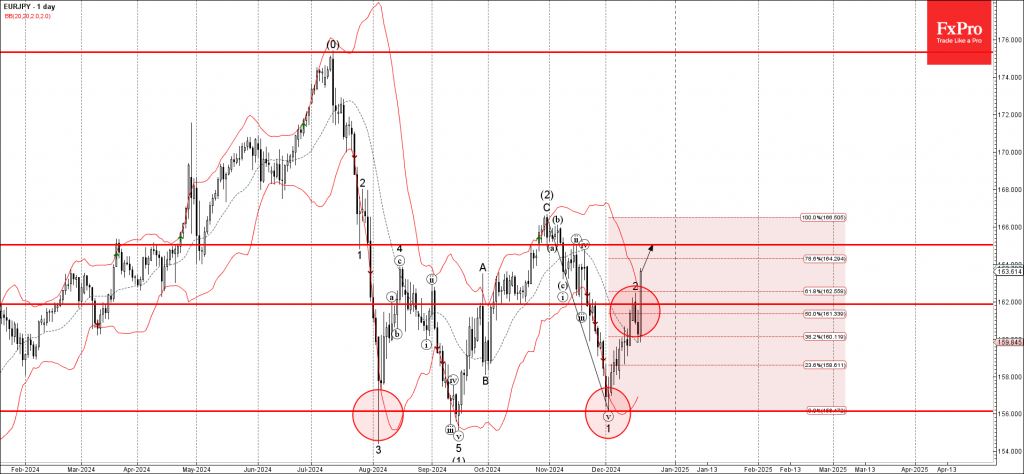

EURJPY Wave Analysis

- EURJPY broke resistance zone

- Likely to rise to resistance level 165.00

EURJPY currency pair recently broke the resistance zone located between the key resistance level 162.00 (which stopped the previous minor wave 2) and the 50% Fibonacci correction of the downward impulse 1 from October.

The breakout of this resistance zone accelerated added to the bullish pressure on this currency pair.

EURJPY currency pair can be expected to rise further to the next resistance level 165.00 (which reversed the price multiple times in November).

Bank of England Review – BoE to Lag Peers in 2025; We Stay Positive GBP

- At today's monetary policy meeting the BoE kept the Bank Rate unchanged at 4.75%, which was widely expected.

- The BoE delivered a dovish vote split but continues to emphasise a gradual approach to reducing the restrictiveness of monetary policy. We think this supports our base case of the next cut coming in February and a quarterly pace thereafter.

- The market reaction was modest with Gilt yields tracking slightly lower and EUR/GBP moving higher.

As expected, the Bank of England (BoE) decided to keep the Bank Rate unchanged at 4.75% today. The vote split had a dovish twist with 6 members voting for an unchanged decision and Dhingra, Ramsden and newcomer Taylor voting for a 25bp cut.

The BoE retained much of its previous guidance noting that "a gradual approach to removing policy restraint remains appropriate" and that "monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further". The MPC now judges that the labour market is "broadly in balance" and has similarly revised its expectation for Q4 growth down from 0.3% q/q to no growth as a reflection of the latest weakening in growth indicators. We also note that in the unchanged camp of the MPC, one member considered that a more "activist strategy" could be warranted, hinting at a more dovish shift in the centrist camp.

Given the recent topside surprises to wage and inflation data combined with an expansionary fiscal stance, we think a continuation of a gradual cutting cycle is warranted. We therefore adjust our call, expecting quarterly cuts in 2025 at the meetings associated with updated economic projections. We expect the next 25bp cut in February with the Bank Rate ending the year at 3.75% (prev. 3.25%). We maintain our terminal rate forecast unchanged at 2.75% but expect it to be reached by Q4 2026 (prev. Q2 2026). However, we highlight that the risk is skewed towards a swifter cutting cycle in the first half of 2025, as highlighted by the MPCs communication today.

Rates. Gilt yields moved lower across the board on the dovish vote split but overall, the reaction was muted. Markets price 18bp worth of cuts for February and 55bp by YE 2025. We highlight the potential for BoE to deliver more easing in 2025 than currently priced, expecting a cut in February and a total of 100bp worth of easing in 2025.

FX. EUR/GBP moved higher on the announcement with the dovish vote split taking centre stage. The still cautious guidance delivered today highlights the more gradual approach of the BoE compared to European peers. We think this supports our case of a continued move lower in EUR/GBP. This is further amplified by relative UK economic outperformance and tight credit spreads. The key risk is a soft BoE.

Sunset Market Commentary

Markets

Yesterday’s hawkish FOMC cut still resonated today. The front end of the curve outperformed slightly after US money markets even outhawked the Fed, looking to only 1 instead 2 rate cuts next year. The US 2-yr yield returns 4.5 bps of yesterday’s 15 bps gain. Long-end US bond yields remain upwardly oriented with the 10-yr and 30-yr yields respectively rising by 3.8 bps (10-yr) to 5.8 bps (30-yr). US president-elect Trump wants to kill a compromise reached between Democrats and Republicans for a three-month stopgap funding extension. Without a deal, the US faces a partial government shutdown by Saturday. He wants to slimdown the package and attach an increase to the debt ceiling (expires in June) to it. NBC even reported that he would support abolishing the debt ceiling altogether. In absence of European numbers, European bonds reacted to the move in US Treasuries yesterday. German yields rise by 4.5 bps (2-yr) to 7.2 bps (10-yr).

The Bank of England kept its policy rate unchanged at 4.75% in a 6-3 majority vote. Three members voted in favour of a 25 bps rate cut (Dhingra, Ramsden and Taylor). We add that one member of the current majority is close to flipping to a more activist approach. Minutes showed him/her arguing that the evolution and prospects for disaggregated measures of activity and inflation could warrant such behavior. Since the previous meeting, inflation rose slightly more than expected (2.6% Y/Y in November), owing in large part to stronger inflation in core goods and food, and is expected to continue to rise slightly in the near term. Bank staff expect GDP growth to have been weaker at the end of the year than projected in November while the labour market is broadly in balance. The outlook is surrounded by more and more domestic (eg impact Autumn budget) and international (geopolitics) uncertainty. A gradual approach to removing monetary policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The market reaction suggests that the split within the board was bigger than expected and that UK money markets took it too far in pricing out 2025 policy rate cuts. UK gilt yields gave away all of the post-FOMC gains with daily changes currently ranging between -2.3 bp (2-yr) and +6.1 bps (30-yr). EUR/GBP bounces off the YtD low at 0.8222 to currently change hands around 0.8260.

News & Views

The Swedish central bank lowered the policy rates by 25 bps to 2.5%. If the economic and inflation outlook holds, it expects to cut rates once again in the first half of 2025. Based on the Riksbank’s own rate forecasts, that would also be the last one of the current cycle: from 2025Q2 on through 2027 it has penciled in a 2.25% policy rate. This is exactly the mid-point of the 1.5-3% neutral rate estimate. After the rapid rate reduction and given the fact that monetary policy works with a lag, the central bank moved to “a more tentative approach when monetary policy is formulated going forward.” Also suggestive of the central bank nearing the end game is the first upward revision to December inflation forecasts since March of this year. The Riksbank expects CPIF to average 1.9%-2%-1.9% over 2024-2025-2026. This compares to 1.7%-1.6%-1.9% in September. The 2027 outcome is seen at 2%. Growth projections were more or less left unchanged at 0.6%-1.8%-2.6%-2.1% over 2025-2027. Swedish swap rates jumped by >10 bps. Gains for the Swedish krone (to EUR/SEK 11.45) could have been bigger if it not were for the risk aversion holding sway on broader financial markets.

The Norwegian central bank stuck to its long-term pledge to keep rates steady at 4.5% through the end of the year. The Norges Bank said that a restrictive monetary policy is still needed but that the time to begin monetary easing is soon approaching, with March 2025 aired as the most likely opportunity to do so. Inflation came in slightly lower than expected, offering some room for rate cuts. That said, it still averages above the 2% target over the policy horizon. GDP would expand at a faster pace next year than expected in September on the back of fiscal policy, consumer spending and higher petroleum investment than previously assumed. One of the key reasons for the Norges Bank to have deviated from major peers by keeping rates steady for so long, was the weak Norwegian currency. It still sees the NOK as a key risk that could derail any rate cutting plans if it were to depreciate further. The NOK loses some marginal ground after today’s decision. EUR/NOK moved to 11.81. Money market expectations were little changed with a first full rate cut priced in by March.

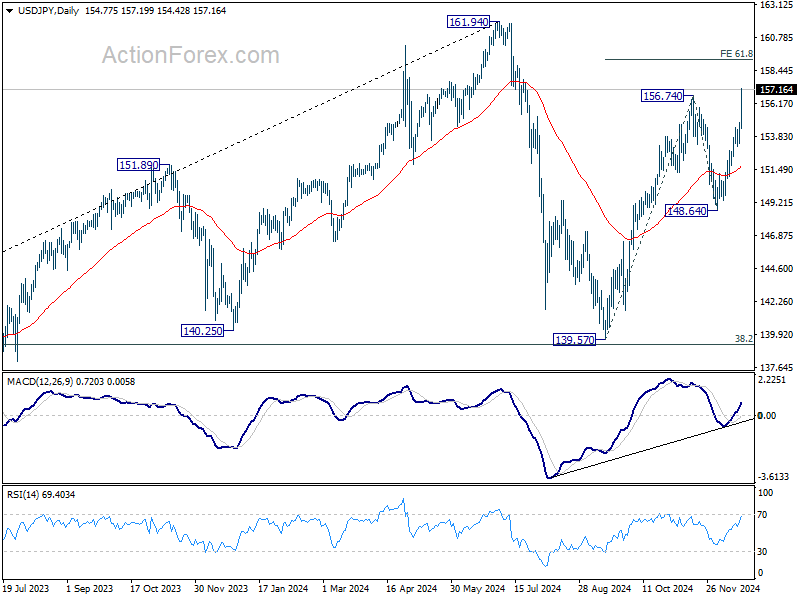

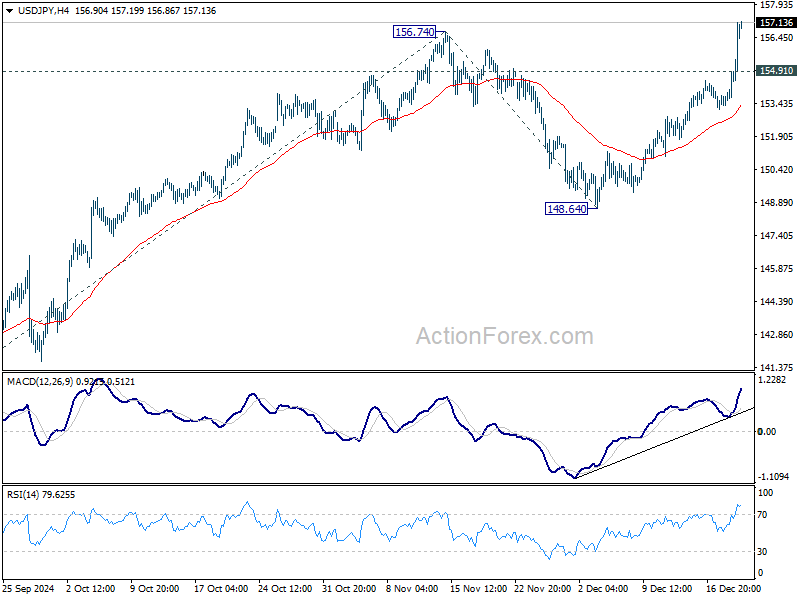

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.78; (P) 154.32; (R1) 155.38; More...

USD/JPY's break of 156.74 resistance confirms resumption of whole rally from 139.57. Intraday bias stays on the upside for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 154.91 minor support will turn intraday bias neutral again first. But outlook will stay bullish as long as 153.15 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.