Sample Category Title

The Aftermath

The Aftermath

The markets will continue to rethink the Tories diminished Brexit directive, and possible party backlash after May's snap election wager ultimately backfired and sent parliament into complete disarray.So we should expect much more discussion about and rethinking of the UK's Brexit position. With May's leadership teetering on the brink, the UK steps ever so closer to the calamitous Brexit cliff edge scenario.

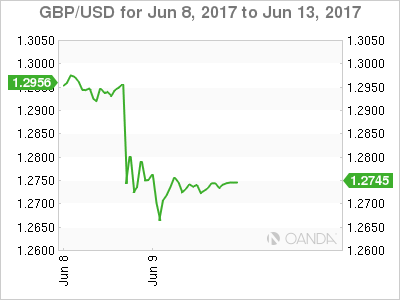

As for the pound, it remains deadlocked in the 1.2700-50 zone as traders muddle through the election aftermath looking for directional clues. Certainly, prolonged uncertainty would argue for a deeper correction on Sterling as May's diminished Brexit mandate scenario plays out. However, there are cooler heads in play suspecting the only real option left is the more market-friendly outcome where the UK adopts a European Economic Area styled agreement. A settlement widely perceived as the least ruinous opportunity for the UK and the rest of the bloc. So, expect markets to struggle in the vortex of near-term possibilities clashing with longer term probabilities.

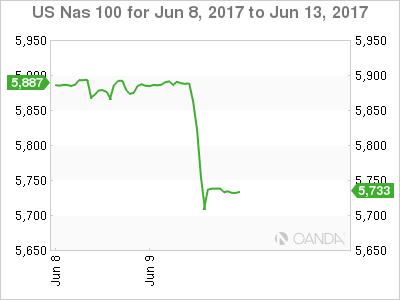

NASDAQ made the Friday afternoon lowlight reel when tech shares pivoted lower driven in part by an apparent flash crash on Amazon shares which dipped nearly 8 % at one point all the while the Dow Jones climbed to record highs. A clear sign of sector rotation in play as opposed to any real shift in fundamentals. While the street was abuzz with talk of a resurgent 'Trump on trade 'as both financial and energy stocks gained by week's end, we remain jaded and pessimistic as that shifting narrative falls a bit too soon and far too optimistic at this stage of the game.

Japanese Yen

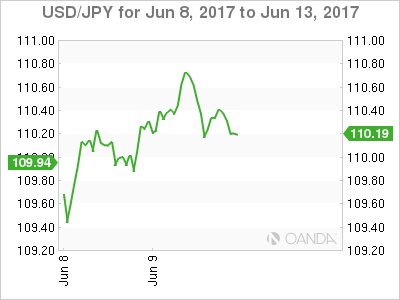

The USDJPY was trading resiliently and showing little signs of post-UK election panic that was until the Friday afternoon swoon on the NASDAQ which .sent the pair toppling over 60 points from intraday highs as risk turned jittery heading into the weekend. I suspect traders opted to play the defensive strategy given weekend headline risk

We‘re left picking up the pieces this morning after Friday's rollercoaster. While some focus remains on last week's BoJ QE exit headlines, we view this little more than the BoJ floating an 'exit” trial balloon.

Risk, on the other hand, has not rebounded in early APAC trade suggesting the markets is sitting tight awaiting more concrete news on the UK political landscape. So far no silver lining in sight as USDJPY trades with an early offered bias and the Nikkei slides

Euro

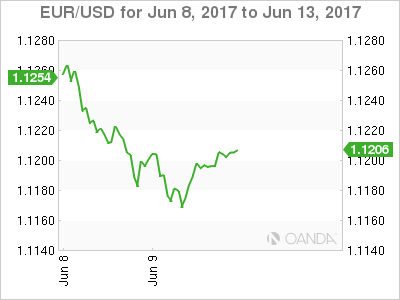

The Euro remains stuck in the mud after the ECB was broadly in line with economists expectations last week. However, with the market anticipating something more on the hawkish side, we could see some more focus on that after the UK election banter fades and EURGBP demand abates.There was a high build up in EURUSD long positioning heading into last week's ECB, so we could see more near-term EURUSD weakness as ECB hawkish narrative continues to unwind

Australian Dollar

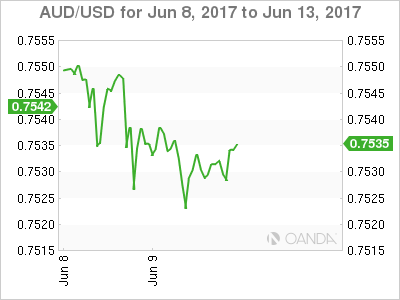

Very tight ranges to close the week as the market's major focus remained on the UK election.But traders are eyeing support holding at .7500-.7525 which bodes will after a solid performance of late. Iron Ore, however, continues to look for a floor which suggests seller will appear on rallies above .7550.

Overall inflation expectations and the employment data have proven supportive of late and another positive print on the Jobs report this week will corroborate the RBA view to look past Q1 weakness and should be supportive for the Aussie.

Macron Maxes Out

Six month ago Macron was an underdog to win the Presidency but his improbable surge has continued after a massive win in the first round of French parliamentary elections. The Australian dollar was the top performer last week while the pound sterling lagged. CFTC positioning data saw GBP shorts pile in ahead of the election. A new Premium video on the existing Premium trades will be posted mid Monday Asia morning.

Macron's La Republique En Marche won 415-455 seats in the first round of voting, out of a total of 577. The vote for the right wing National Front faded to only 1-5 seats and former President Hollande's Socialist party was decimated, winning only 10-20 seats.

The theme of 2016 in elections was a shift to populism but in 2017 it has turned into more of a shift to the fringes and away from establishment parties and candidates. Corbyn's ability to turn out the vote is as shocking as anything over the past year and may inspire leftist candidates elsewhere.

That sets up years of political drama and the specter of wildly divergent policies in a fragmented world. At the moment, a badly wounded May is attempting to hang on with the backing of the DUP but the knives are out. If she's toppled, the uncertainty will be a fresh reason to sell the pound.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

EUR +74K vs +73K prior GBP -37K vs -30K prior JPY -55K vs -52K prior CHF -17K vs -19K prior CAD -94K vs -98K prior AUD 0K vs +3K prior NZD -2K vs -5K prior

The moves of committment of traders were modest this week but at least a few traders got short GBP ahead of Thursday's election and rode that to a quick profit. EUR longs inched to a fresh high dating back to 2007 and CAD shorts remain near a record, highlighting to vulnerability of the pair after another strong jobs report on Friday.

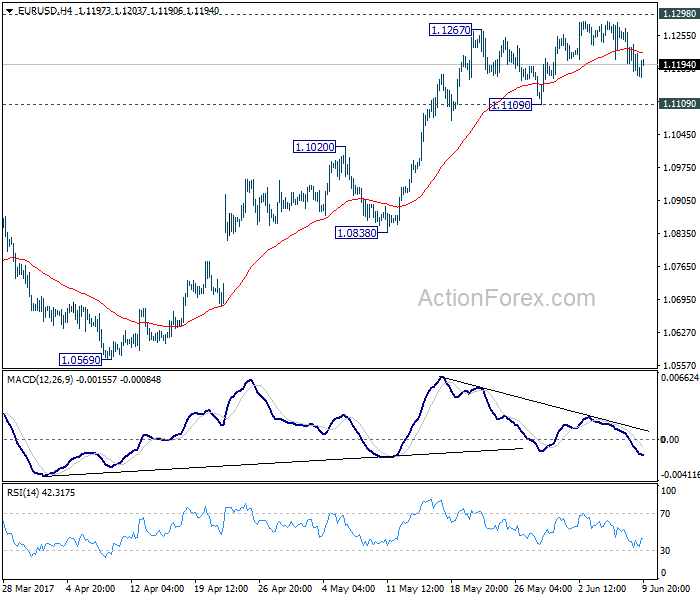

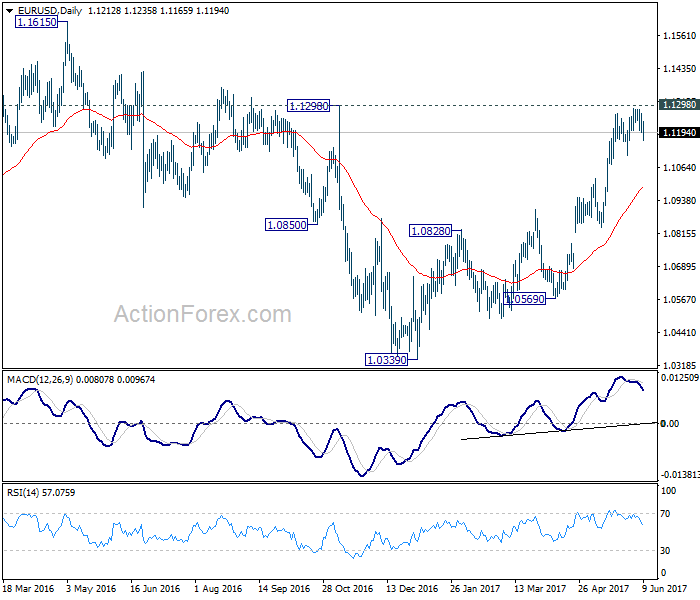

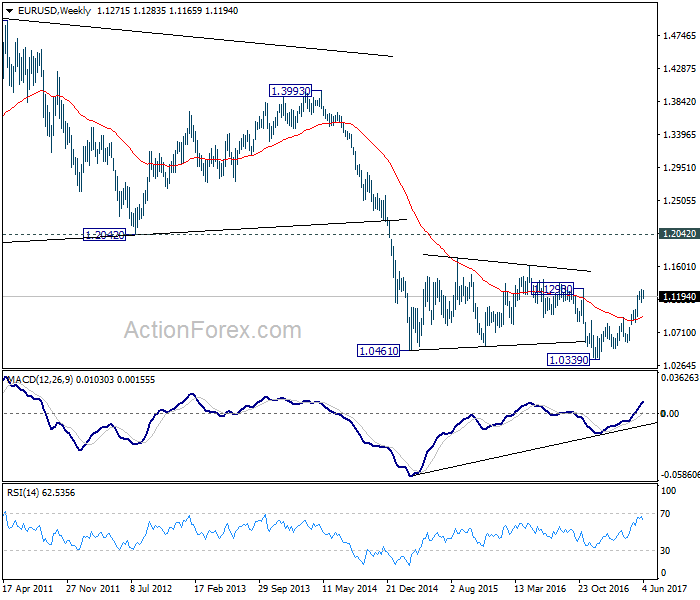

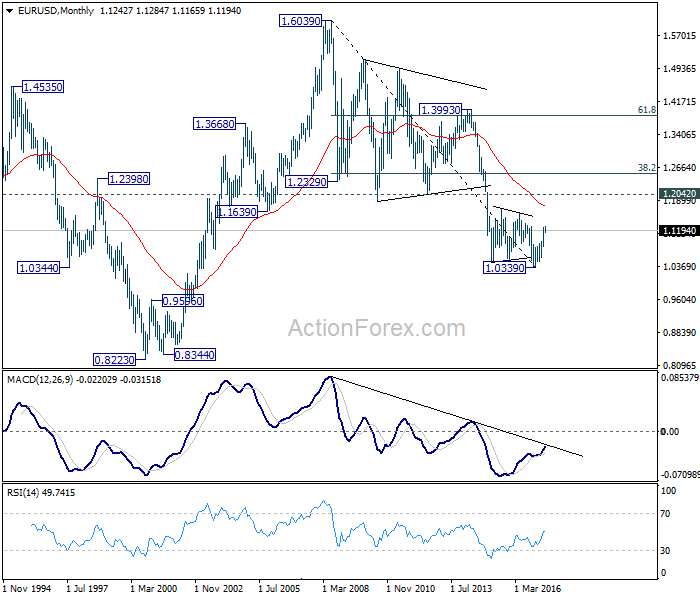

EUR/USD Weekly Outlook

EUR/USD stays in consolidation below 1.1298 key resistance last week. Retreat was so far shallow and contained above 1.1109 support. Outlook is unchanged. Initial bias remains neutral this week first, with focus on 1.1298. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. On the downside, break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0922). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

In the long term picture, the case for completion of down trend from 1.6039 (2008 high), and long term bottoming at 1.0339, is starting to build up. Decisive break of 1.1298 will bring rise back to 1.2042 as first resistance. And in that case, we should at least see rally back to 38.2% retracement of 1.6039 to 1.0339 at 1.2516.

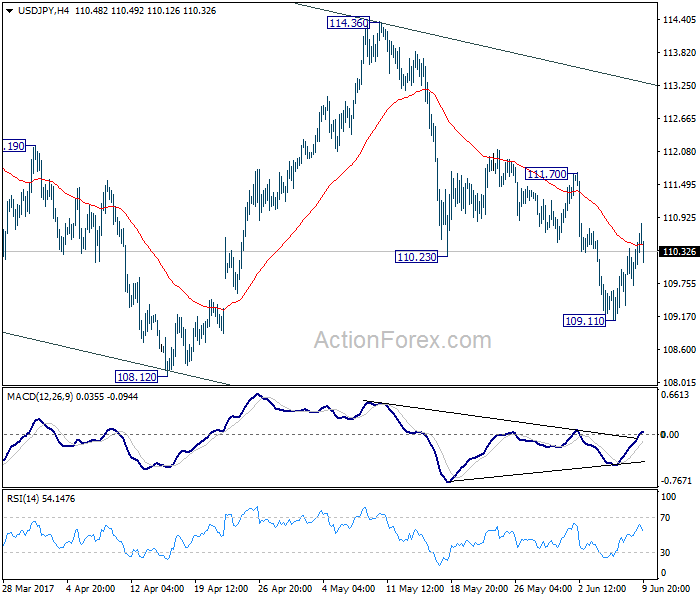

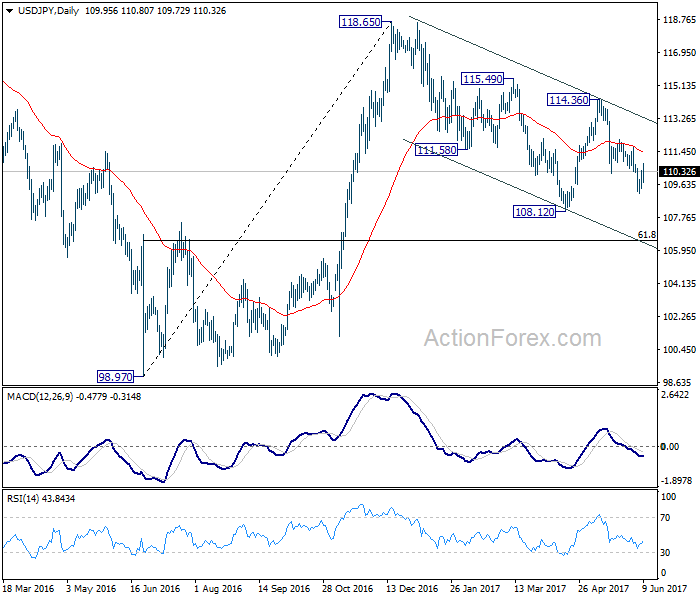

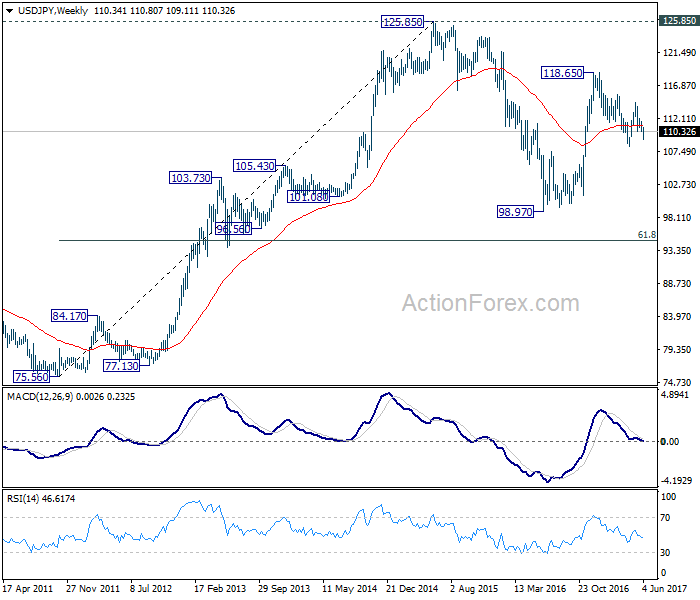

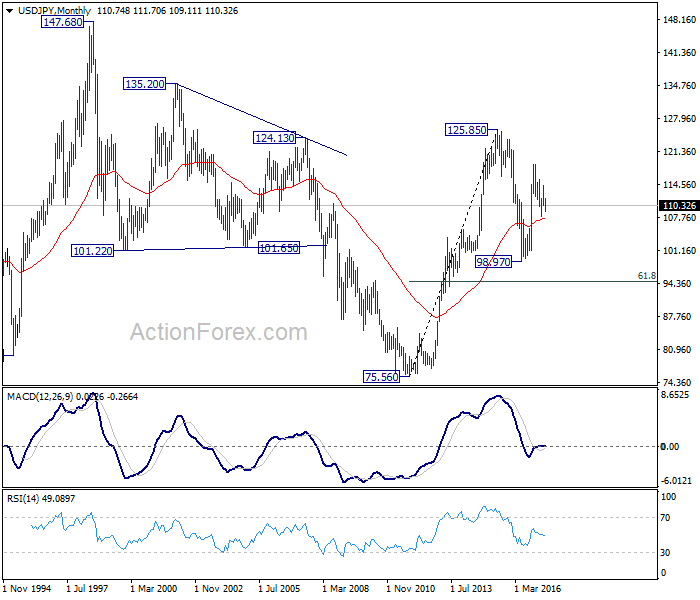

USD/JPY Weekly Outlook

USD/JPY dived to 109.11 last week but rebounded since then. Structure of such rebound is still correctively looking and there is no clear sign of reversal. Initial bias remains neutral this week first. As long as 111.70 resistance holds, near term outlook stays mildly bearish for deeper fall. Below 109.11 will target 108.12 low first. Break will extend the whole corrective fall from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. We will look for bottoming sign there. Meanwhile, break of 110.70 will suggest near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

In the long term picture, the rise from 75.56 long term bottom to 125.85 medium term top is viewed as an impulsive move. Price actions from 125.85 are seen as a corrective move which could still extend. But, up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

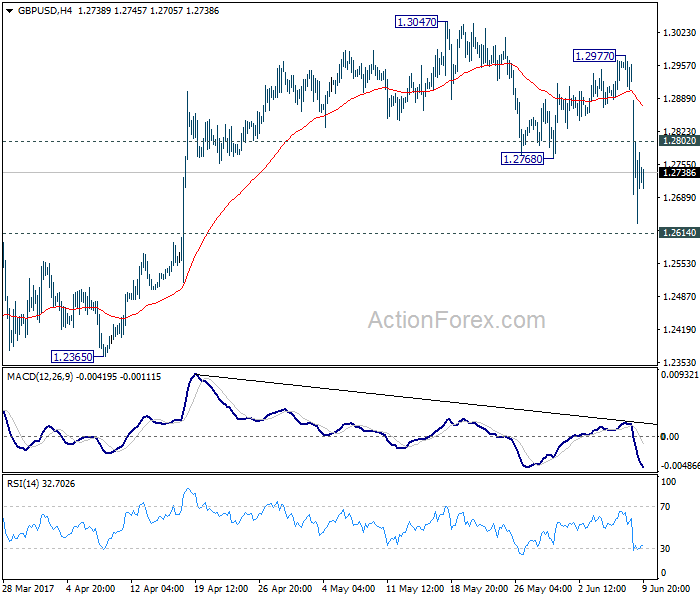

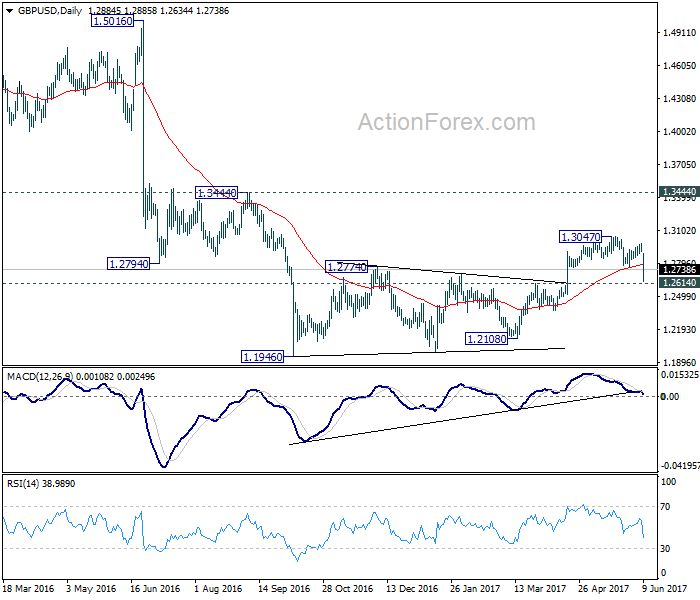

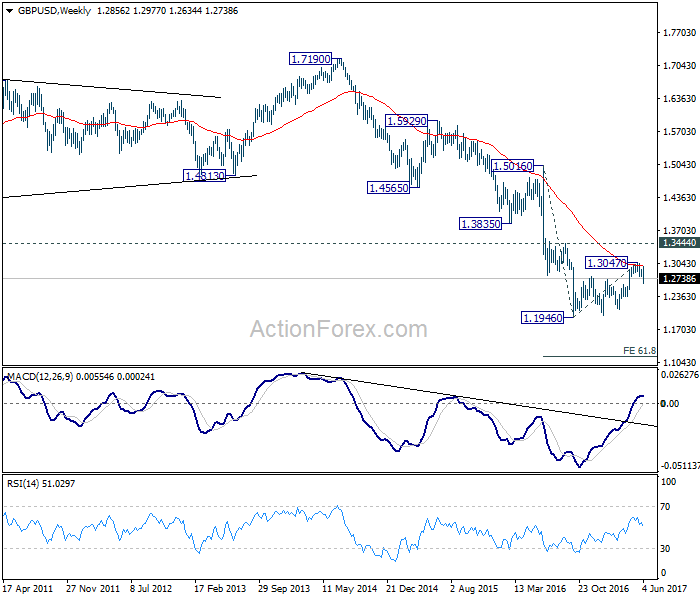

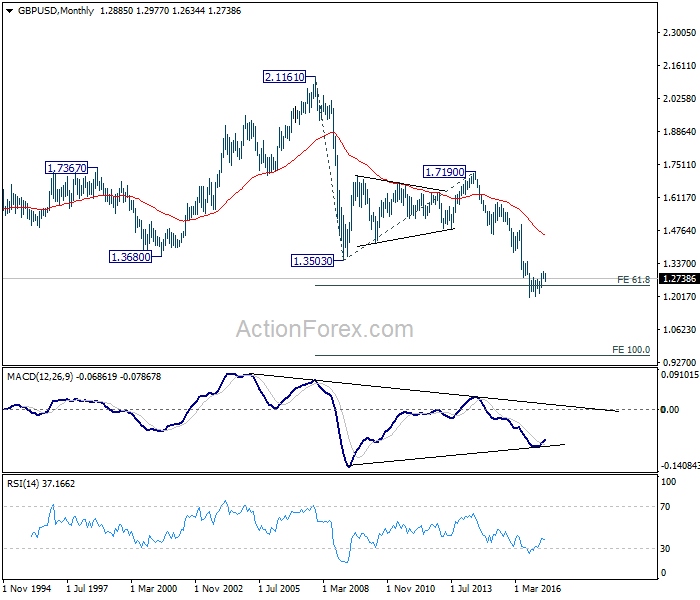

GBP/USD Weekly Outlook

GBP/USD's sharp decline and break of 1.2768 support last week indicates resumption of decline from 1.3047. Also, it affirmed the case that consolidation pattern from 1.1946 has completed at 1.3047 already, well below 1.3444 key resistance. Initial bias stays on the downside this week for 1.2614 key near term support. Break there would confirm our bearish view and target a test on 1.1946 low next. On the upside, above 1.2802 will bring turn bias neutral and bring recovery. But outlook will remain bearish as long as 1.2977 resistance holds.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

In the longer term picture, no change in the view that down trend from 2.1161 is still in progress. On resumption, such decline would extend deeper to 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532.

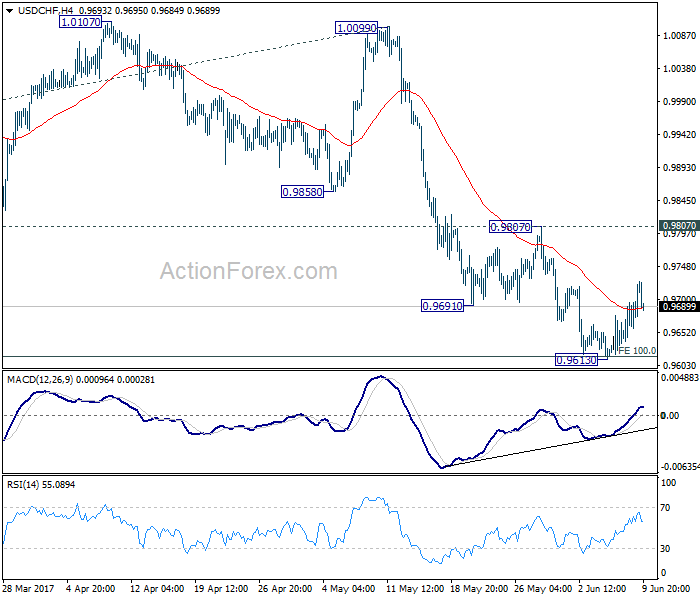

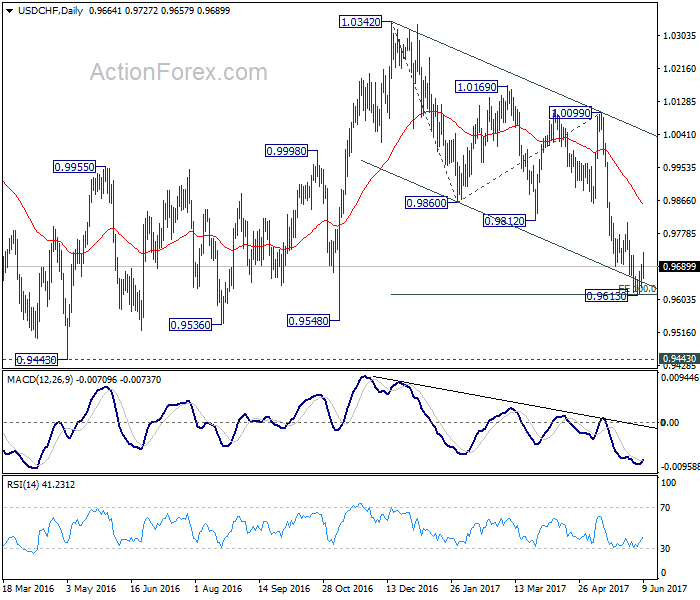

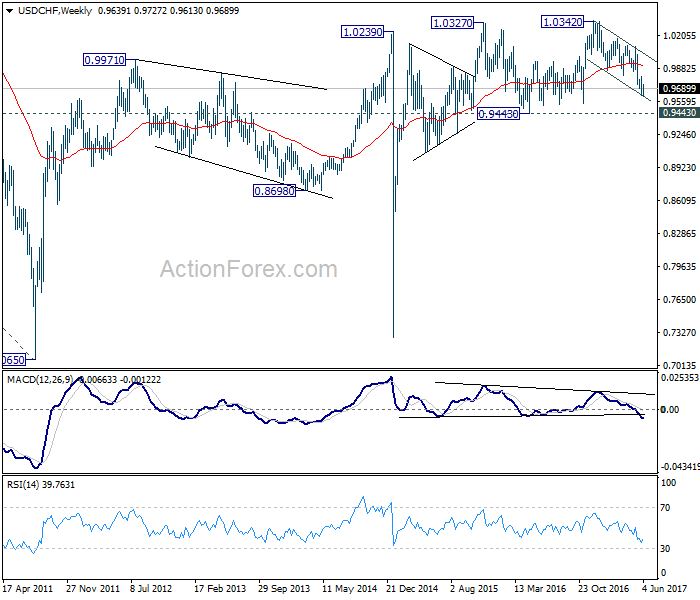

USD/CHF Weekly Outlook

USD/CHF formed a short term bottom at 0.9613 last week and recovered. Such rise is corrective in structure so far and doesn't indicate reversal. Initial bias stays neutral this week first. Outlook will remain bearish as long as 0.9807 resistance holds. Break of 0.9613 will extend the whole fall from 1.0342 to 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

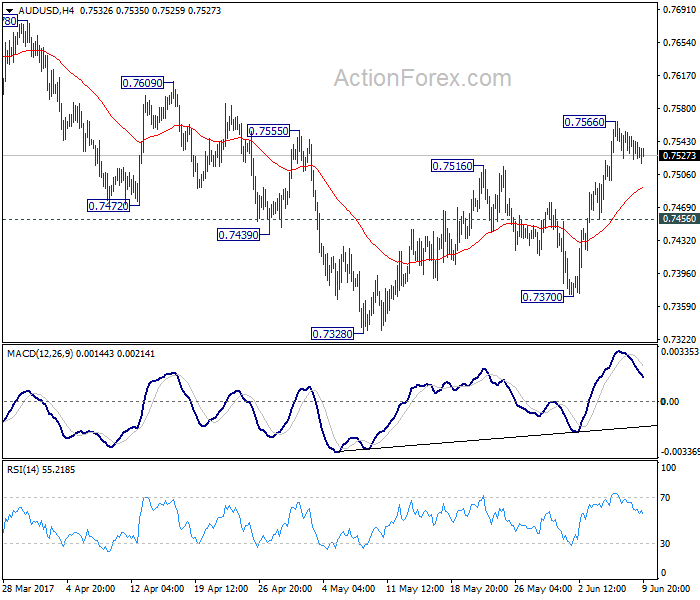

AUD/USD Weekly Outlook

AUD/USD's rise from 0.7328 resumed last week by taking out 0.7516 resistance. But a temporary top was formed at 0.7566. Initial bias is neutral this week first. Further rise is mildly in favor as long as 0.7456 minor support holds. Above 0.7566 will target 0.7748 resistance. In that case, we'll be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7456 minor support will turn bias back to the downside for 0.7328 short term bottom.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8091) and above.

In the longer term picture, while the down trend from 1.1079 might extend lower, we're not anticipating a break of 0.6008 (2008 low) yet. We'll look for bottoming above there to reverse the medium term trend.

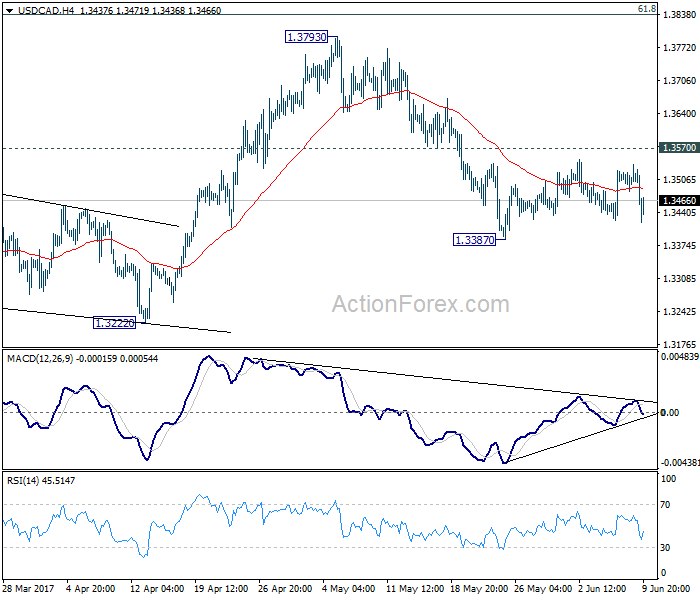

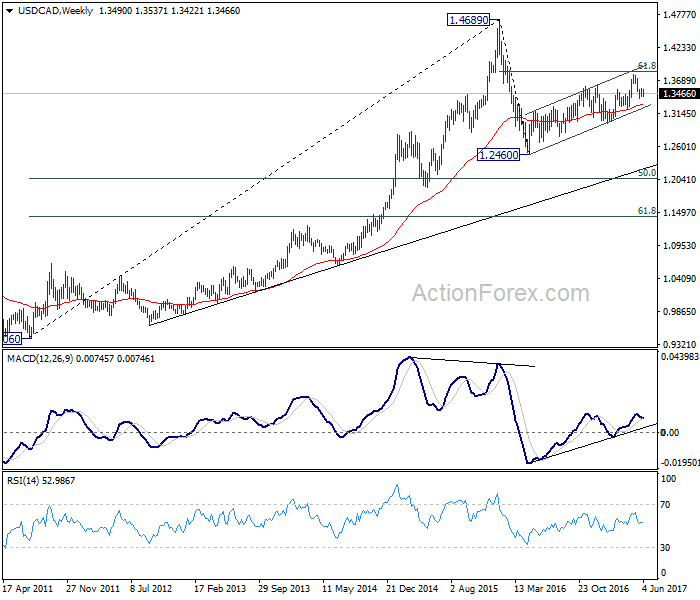

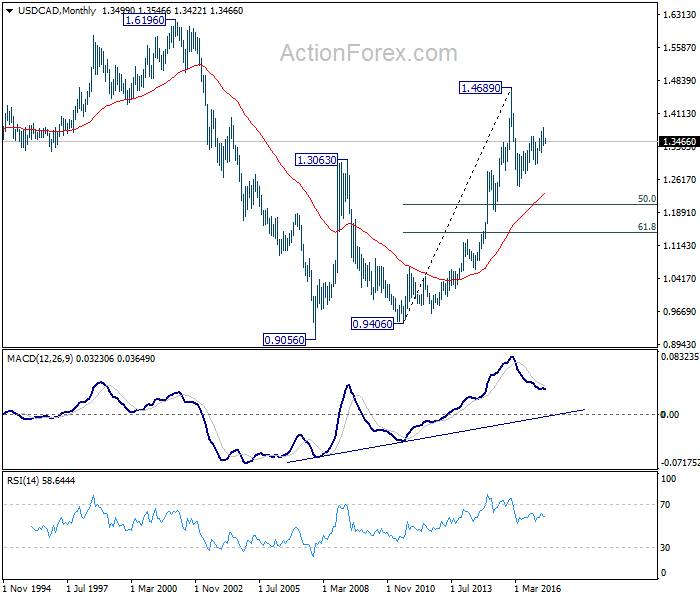

USD/CAD Weekly Outlook

USD/CAD stayed in the consolidation pattern from 1.3387 last week and outlook is unchanged. Initial bias remains neutral this week first. In case of another recovery, upside should be limited by 1.3570 resistance and bring fall resumption. We're holding on to the view that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

In the longer term picture, rise from 0.9056 (2007 low) is viewed as a long term up trend. It's taking a breath after hitting 1.4689. But such rise expected to resume later to test 1.6196 down the road.

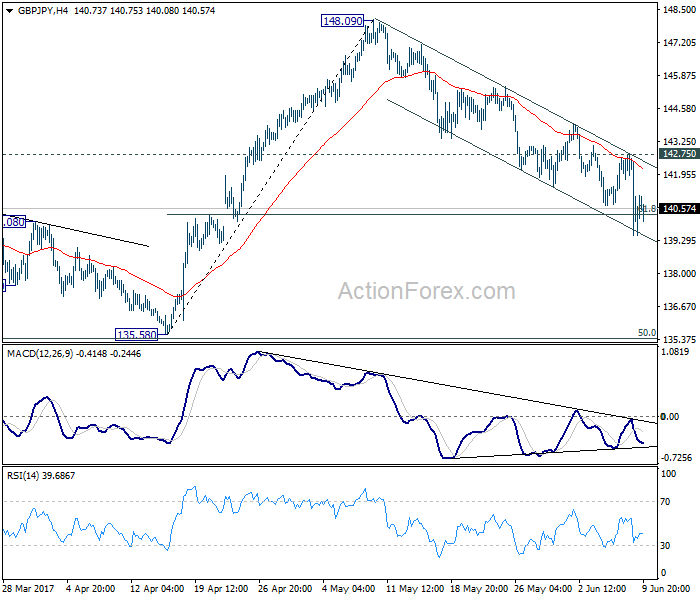

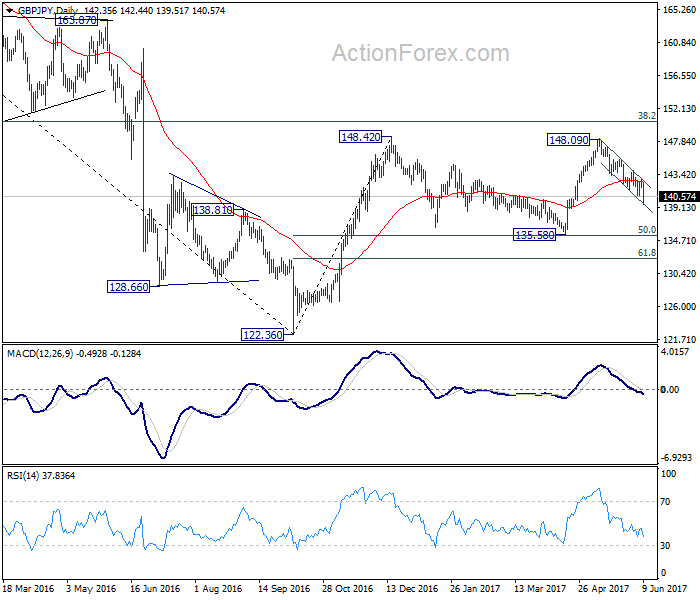

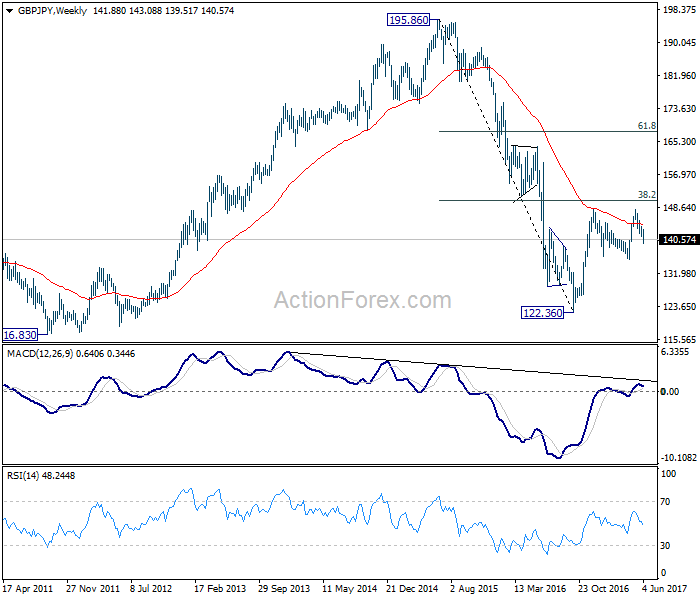

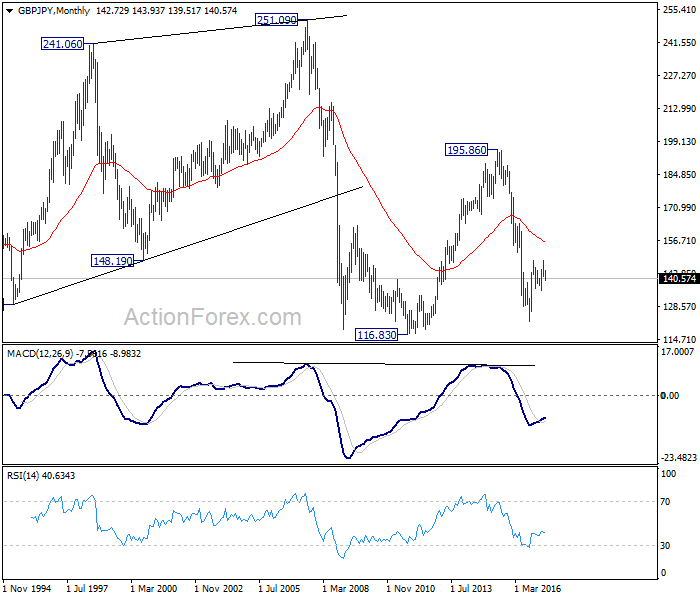

GBP/JPY Weekly Outlook

GBP/JPY's fall from 148.09 extended to as low as 139.52 last week and broke 61.8% retracement of 135.58 to 148.09 at 140.35. The cross is kept well below falling 4 hour 55 EMA and inside near term falling channel. Initial bias stays on the downside this week and current fall would target 135.58 support. We'll look for bottoming sign again around there. On the upside, break of 142.75 resistance is needed to indicate completion of fall from 148.09. Otherwise, near term outlook will say mildly bearish in case of recovery.

In the bigger picture, while the fall from 148.09 is deeper than expected, we're not bearish in the cross yet. Price action from 148.42 is possibly developing into a sideway pattern with fall from 148.09 as the third leg. Deeper decline could be seen but we're looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Rise from 122.36 is still mildly in favor to resume at a later stage. However, sustained break of 135.58/39 will confirm reversal and target a retest on 122.36 low.

In the longer term picture, based on the impulsive structure of the decline from 195.86 to 122.36, such fall should not be completed yet. But we will now pay close attention to the structure of the rise from 122.36 to determine whether it's a corrective move, or an impulsive move. That would decide whether a break of 116.83 low would be seen.

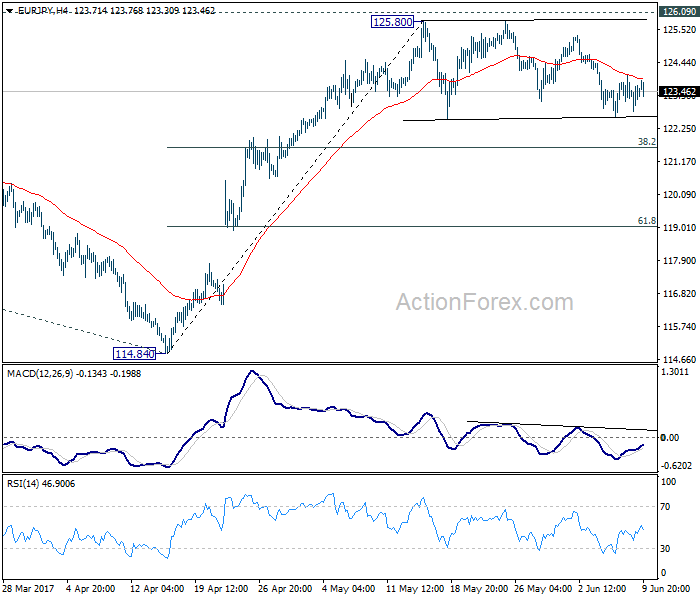

EUR/JPY Weekly Outlook

EUR/JPY stayed in the consolidation pattern from 125.80 last week and outlook remains unchanged. Initial bias stays neutral this week first. In case of another fall, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

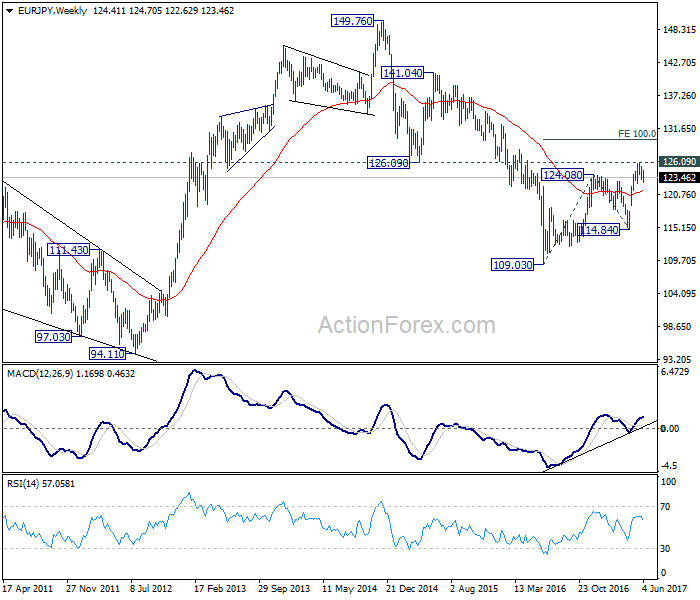

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

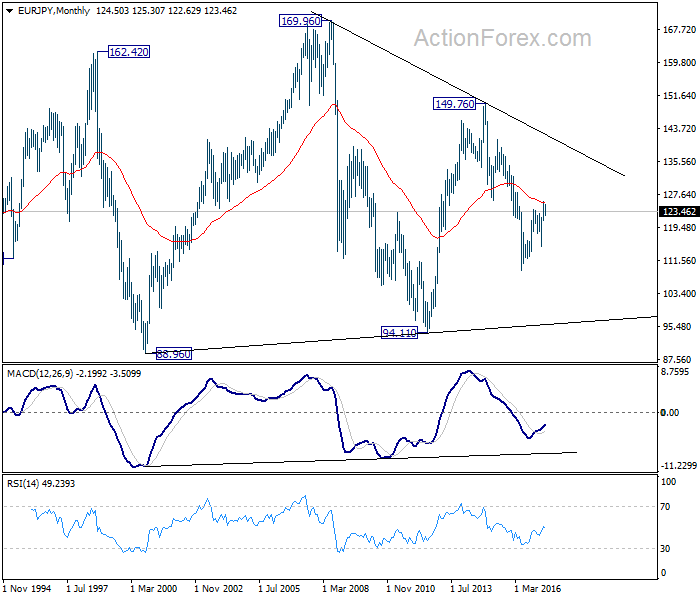

In the long term picture, medium term decline from 149.76 is seen as part of a long term sideway pattern from 88.96. We're not seeing any sign of an established long term trend yet. Hence, we'll be cautious on strong support at 94.11 in case of another fall. Also, there could be strong resistance at 149.76 in case of a medium term rise.