Sample Category Title

Canadian Unemployment Rate Hits 6.6% In May

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CAD and closed at 1.3466 on Friday.

Macroeconomic data revealed that Canada’s unemployment rate rose to 6.6% in May, meeting market expectations. In the previous month, the unemployment rate had recorded a reading of 6.5%. Nevertheless, the nation’s net number of people employed climbed more-than-expected by 54.5K in May, rising by the most in eight months and following an increase of 3.2K in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3448, with the USD trading 0.13% lower against the CAD from Friday’s close.

The pair is expected to find support at 1.3405, and a fall through could take it to the next support level of 1.3361. The pair is expected to find its first resistance at 1.3510, and a rise through could take it to the next resistance level of 1.3571.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Market Update – Asian Session: Macron Gets The Mandate To Govern France With Strong Parliament Election Showinges

Asia Mid-Session Market Update: Macron gets the mandate to govern France with strong Parliament election showing; Japan economic data disappoint

Friday US Session Highlights

(US) APR FINAL WHOLESALE INVENTORIES M/M: -0.5% V -0.3%E

(US) House Dem Leader Pelosi: hopes there will be no debate on whether to raise the debt ceiling; hopes for vote by end of July

(UK) PM May: I will now form a government; Brexit talks to start in 10 days as expected; to govern with support of Democratic Unionist Party (DUP) (as speculated)

(UK) Scottish Min Sturgeon (SNP): PM May has lost all credibility and authority following election results

Weekend corporate activity

NOBL.SG: Said to receive approaches for oil business - FT

WDC: Reportedly to make a new offer at over $18B for Toshiba's chip business in final effort to win the assets - press

Politics

(US) Sen Graham (R-SC): Senate will vote on a new round of Russia sanctions this week; Warns Pres Trump not to veto it - press

(RU) Russian opposition leader Navalny organizing protest marches on Monday; Thousands of people expected to take part - press

Key economic data:

(JP) JAPAN APR MACHINE ORDERS M/M: -3.1% (first decline in 3 months) V 0.5%E; Y/Y: 2.7% V 7.3%E

(JP) JAPAN MAY PPI (CGPI) M/M: 0.0% (7-month low) V 0.1%E; Y/Y: 2.1% V 2.2%E

(NZ) NEW ZEALAND MAY CARD SPENDING RETAIL M/M: -0.4% V 0.2%E; TOTAL M/M: -0.2% V +0.4% PRIOR

(NZ) ANZ: New Zealand May non-tradable inflation m/m 0.2% v 0.0% prior, y/y: 2.3% v 2.2% prior

Asia Session Notable Observations

Investors are alarmed going into this week's key Fed meeting this Thursday, with expectations of a rate hike overshadowed by heightened volatility in the tech space on Friday when the Nasdaq plunged over 100 points. Ahead of Monday open, US equity futures are slightly lower while Asian indices start the week under pressure. Hang Seng is particularly vulnerable, falling over 1% to a 1-week low.

FX majors are in narrow range despite some constructive weekend developments overseas. Political risk has been dialed back to a simmer in Europe. French President Macron secured well over 400 seats in the first round of National Assembly elections - well above 330-360 expected - giving him the mandate to govern toward labor reform promised on campaign trail. In Italy too, the euroskeptic 5-Star faction was dealt a blow politically, failing to make the run-off vote in all 7 major cities holding local elections this weekend. Recall Italy presidential elections are expected early next year, but may be called sooner. EUR/USD firmed up marginally above 1.12. GBP/USD was also slightly higher as PM May has survived the first few days of her election disappointment, though there were more reports of Conservative lawmakers looking at a No Confidence vote coup. NZD/USD was down some 20 pips from the highs below $0.72 after NZIER cut New Zealand FY16/17 GDP forecast from 3.4% to 3.0%.

Even though South Korea's new president Moon is increasingly looking more conciliatory with China on the issue of North Korea, Pyongyang's KCNA threatened that it wasn’t far away from test-firing an ICBM w/the potential of hitting the continental US. President Trump has long maintained a test of this magnitude threat would represent crossing a red line.

Ahead of this Friday's BOJ meeting, Japan's 2nd tier data continues to give little justification for rumored discussion about QE exit process. Forward-looking Machine Orders registered its first decline in 3 months, while the corporate goods index did not rise m/m for the first time in 7 months.

Speakers and Press

China

(CN) China Financial News: Slower IPO pace will improve investor sentiment

(CN) China Commerce Ministry reportedly to "substantially" reduce restrictions on foreign access to China market - Chinese press

Australia/New Zealand

(NZ) NZ Institute of Economic Research (NZIER) cuts New Zealand FY16/17 GDP forecast from 3.4% to 3.0%

Korea

(KR) North Korea is close to test-firing an ICBM with potential of reaching US - KCNA (update)

(KR) South Korea Finance Ministry said to submit a 2018 budget plan to Parliament by Sept 1st; Estimated to see 6% increase in spending from 2017 - Korean press

(KR) Bank of Korea Gov Lee: Monetary policy needs to stay accommodative to support the economy, but adjustments should be reviewed if growth remains strong - speech for Bank of Korea's 67th anniversary

Asian Equity Indices/Futures (23:30ET)

Nikkei -0.4%, Hang Seng -1.2%, Shanghai -0.5%, ASX200 closed, Kospi -0.9%

Equity Futures: S&P500 -0.2%; Nasdaq -0.3%, Dax -0.1%, FTSE100 -0.4%

FX ranges/Commodities/Fixed Income (23:30ET)

EUR 1.1195-1.1215; JPY 110.15-110.45; AUD 0.7520-0.7535; NZD 0.7195-0.7215; GBP 1.2725-1.2765

Aug Gold -0.2% at 1,269/oz; July Crude Oil +0.3% at $46.09/brl; July Copper -0.4% at $2.64/lb

(CN) PBOC SETS YUAN MID POINT AT 6.7948 V 6.7971 PRIOR

(US) Weekly Baker Hughes US Rig Count: 927 v 916 w/w (+1.2%) (21st straight weekly rise)

(CN) PBOC to inject combined CNY40B v CNY60B prior

(KR) South Korea sells 5-yr Govt bonds; avg yield 1.885% v 1.925% prior

Asia equities / Notables / movers

Hong Kong

Evergrande (3333) -0.2%; Vanke +0.7%; Evergrade to sell its 14% stake in China Vanke to Shenzhen Motor Group for CNY29.2B

China Resources Land (1109) -1.7%; May sales

Japan

Toshiba (6502) +7.0%; Western Digital to make a new offer at over $18B for Toshiba's chip business in final effort to win the assets - press

FujiFilm (4901) +1.7%; Reports FY17 Net profit ¥131.5B vs ¥112B prior forecast, Op profit ¥172B v ¥192B prior forecast

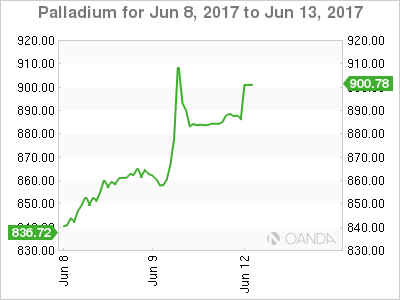

Palladium Puts Oil And Gold To Shame

Incredible scenes in the Palladium market on Friday with a massive squeeze overshadowing continued anaemic price action on precious metals and crude oil.

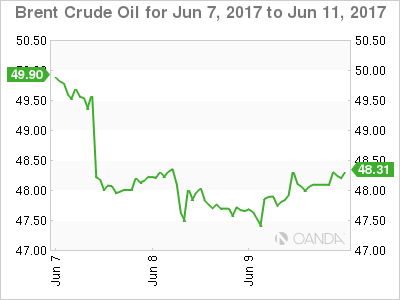

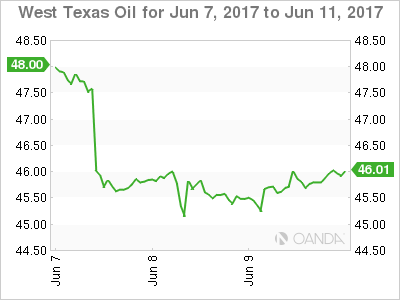

OIL

Crude paused for breath on Friday after a tumultuous week, with both Brent and WTI closing 20 cents higher, even as the Baker Hughes Rig Count showed its mandatory rise by another 11 rigs to 927.

Over the weekend both the Saudi and Russian energy ministers stated they saw no need to revisit the size of the cuts from the OPEC/Non-OPEC production deal. The Saudi’s also went so far as to say the surge in inventories was transitory and that the data should start to see a clear run down sooner rather than later. Hopefully much sooner from OPEC’s point of view, one would think.

It has given both crude contracts a positive start this morning with Brent spot trading 48.25 and WTI spot 45.95.

Brent spot has resistance at 48.50 and then 48.80 with support at 47.25.

WTI spot has resistance at 46.10 and then 46.50 with support at 45.00.

Precious Metals

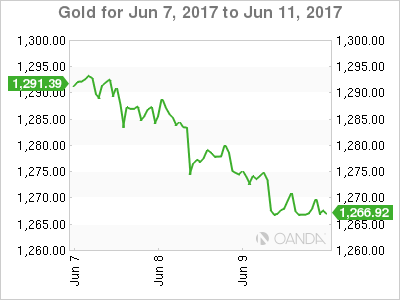

Gold

The weak price action in gold continued into the weeks end with Friday marking the 3rd consecutive lower close of the week. The expected weekend risk hedging did not materialise with gold closing around its lows at 1266.25.

With the U.K. event risk successfully negotiated, it would appear the market is putting more emphasis on this week’s FOMC rate hike, with the street having priced this as an almost 100% certainty. The key to gold’s performance will be the updated Summary of Economic Projections and the long run equilibrium of unemployment. The market will be anxiously watching to see if the Federal Reserve has become more dovish in its outlook. It should support gold, although if the Fed stays on its weaker data is transitory track; this will likely weigh on the yellow metal.

Asia has started the week’s session quietly with gold trading at 1269.40. Gold has resistance at 1271.40 and then 1289.00 with support at 1266.25 and then 1259.00.

Silver

Silver has continued its negative price action having lead gold lower last week. It is trading at 17.1600 in Asia with the important 17.0000 psychological support in sight. A break of this level could see more stop-losses come to the market.

Meanwhile, resistance remains robust above at the 17.5000/17.5500 region. It contains Friday’s pre-sell-off high and the 100 and 200-day moving averages.

Palladium

Palladium was the star of the show on Friday. Exploding higher by 7.30 % to 918.00 at one stage before finishing at 884.00 for a still very respectable gain of 3.35 %.

The emotional scenes play to Palladium’s industrial uses rather than as a pure precious metal play. The futures curve has moved into and aggressive backwardation, meaning that the spot price is much higher than the futures prices. It implies that supplies for immediate delivery are very tight.

The price action itself had the look of panic stop-loss buying by industrial users who had waited for it to follow gold, silver and platinum lower.

Palladium trades quietly at 888.50 this morning in Asia with the region mostly likely awaiting direction from Europe.

Resistance is Friday’s highs around 918.00 with support at 854.00 and 830.00.

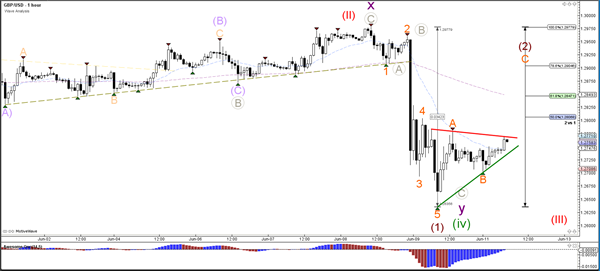

Daily Technical Analysis: GBP/USD Awaits S&R Breakout After UK Election 2017

Currency pair GBP/USD

The GBP/USD has two likely wave scenarios after last week's general parliamentary election in the UK. One variant is bullish where the Cable is completing a retracement within wave 4 (green). The alternative is a bearish reversal as indicated by the impulsive wave 123 (red). A breakout above the solid support and resistance (S&R) trend lines would indicate which direction is more likely.

The GBP/USD could be building an ABC (orange) correction but a break above the 100% level invalidates the bearish wave 2 (brown).

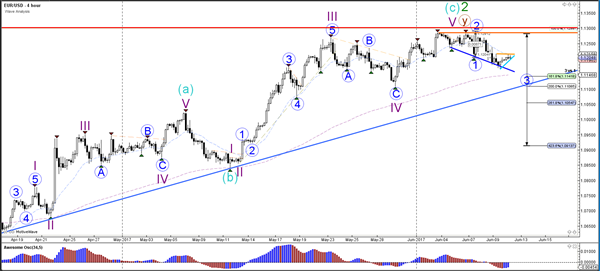

Currency pair EUR/USD

The EUR/USD was unable to break the 100% Fib resistance level at 1.13 (red line) and the failure to break the 1.13 invalidation level keeps the current wave structure intact. A break below support (blue) would increase the chance of a wave 3 (blue).

The EUR/USD invalidates wave 2 (orange) if price manages to break above the 100% Fib level.

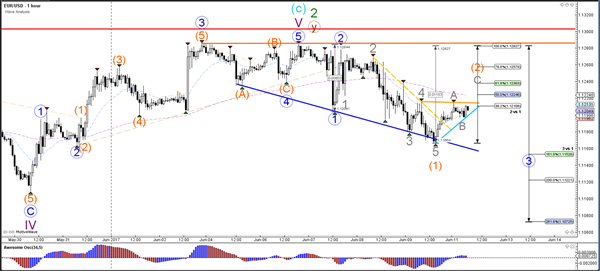

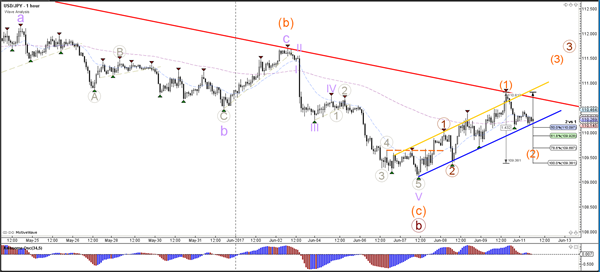

Currency pair USD/JPY

The USD/JPY is testing both support (blue) and resistance (red) trend lines. A break above resistance could see price challenge the Fibs of wave 3 (brown).

The USD/JPY would invalidate the wave 2 (orange) if price breaks below the 100% Fibonacci level.

European Open Briefing: Markets Had A Relatively Quiet Start Into The New Trading Week

Global Markets:

- Asian stock markets: Nikkei down 0.60 %, Shanghai Composite fell 0.45 %, Hang Seng declined 1.05 %

- Commodities: Gold at $1269 (-0.20 %), Silver at $17.12 (-0.60 %), WTI Oil at $46.05 (+0.50 %), Brent Oil at $48.40 (+0.50 %)

- Rates: US 10-year yield at 2.22, UK 10-year yield at 1.00, German 10-year yield at 0.26

News & Data:

- Japan Core Machinery Orders m/m -3.1 % vs 0.5 % expected

- Japan Core Machinery Orders y/y 2.7 % vs 7.3 % expected

- Japan PPI m/m 0.0 % vs 0.1 % expected

- Japan PPI y/y 2.1 % vs 2.2 % expected

- Sterling steadies as British PM scrambles after poll shock, dollar awaits Fed – RTRS

CFTC Positioning Data:

- EUR long 74K vs 73K long last week. Longs increased 1K. Largest long position since 2007

- GBP short 37K vs 30K short last week. Shorts increased by 7K

- JPY short 55K vs 52K short last week. Shorts increased by 3K.

- CHF short 17K vs 19K short last week. Shorts trimmed by 2K

- CAD short 94K vs 98K short. Shorts trimmed by 4K. Near record levels still.

- AUD square vs 3K long. Shorts trimmed 3K

- NZD short 2K vs 5K short last week. Shorts trimmed 3K

Markets Update:

Markets had a relatively quiet start into the new trading week. The Euro consolidated in a 1.1200-10 range, while GBP/USD traded between 1.2710 and 1.2770. The Pound is likely to suffer from the political uncertainty in the near-term, and selling interest on larger rallies will be high. Strong resistance is seen at 1.2820 and ahead of 1.29.

USD/JPY is slightly lower amid a decline in Asian stock markets. The pair fell from 110.45 to 110.15 in Asia. The short-term outlook is mixed. Should USD/JPY fail to break above 111 resistance soon, a retest of 109 seems likely.

AUD/USD consolidated in a 10 pips range overnight. Important support lies at 0.75. A break below would suggest that momentum is still too weak, and that a return to 0.7380 support is likely.

Overall, volatility in the FX market is likely to remain low ahead of the Fed meeting on Wednesday. The central bank is expected to increase interest rates, but the focus will be on the FOMC projections and statement. A cautious Fed could bring the Dollar under additional pressure.

Upcoming Events:

- 09:00 BST – Italian Industrial Production

- 09:30 BST – RBA Assistant Governor Debelle speaks

The Week Ahead:

Tuesday, June 13th

- 02:30 BST – Australian NAB Business Confidence

- 07:00 BST – German WPI

- 09:30 BST – UK CPI

- 10:00 BST – German ZEW Economic Sentiment

- 10:00 BST – Euro Zone ZEW Economic Sentiment

- 13:30 BST – US PPI

- 23:45 BST – New Zealand Current Account

Wednesday, June 14th

- 01:30 BST – Australian Westpac Consumer Sentiment

- 03:00 BST – Chinese Industrial Production

- 03:00 BST – Chinese Retail Sales

- 07:00 BST – German CPI

- 09:30 BST – UK Unemployment Rate

- 09:30 BST – UK Average Earnings

- 09:30 BST – UK Claimant Count Change

- 10:00 BST – Euro Zone Industrial Production

- 13:30 BST – US CPI

- 13:30 BST – US Retail Sales

- 19:00 BST – Fed Interest Rate Decision

- 19:30 BST – FOMC Press Conference

- 23:45 BST – New Zealand GDP

Thursday, June 15th

- 02:30 BST – Australian Employment Change

- 02:30 BST – Australian Unemployment Rate

- 07:45 BST – French CPI

- 08:15 BST – Swiss CPI

- 08:30 BST – SNB Rate Decision

- 08:30 BST – SNB Press Conference

- 09:00 BST – Italian CPI

- 09:30 BST – UK Retail Sales

- 10:00 BST – Euro Zone Trade Balance

- 12:00 BST – Bank of England Rate Decision

- 12:00 BST – Bank of England Meeting Minutes

- 13:30 BST – US Philadelphia Fed Manufacturing Index

- 14:15 BST – US Industrial Production

- 14:15 BST – US Manufacturing Production

- 15:00 BST – US NAHB Housing Market Index

Friday, June 16th

- 07:30 BST – Bank of Japan Press Conference

- 10:00 BST – Euro Zone CPI

- 13:30 BST – US Housing Starts

- 13:30 BST – US Building Permits

- 15:00 BST – US Michigan Consumer Sentiment

The Kiwi Dollar Should Cool-Off This Week

Key Points:

- Buying pressure has been notable but may subside over the coming days.

- Mixed fundamental forecast should see some of last week's rally eroded.

- Near-term losses may not preclude further gains in the medium to long-term.

The Kiwi Dollar had an excellent past week of gains but the longevity of its rally is now coming into question. Specifically, a mixed technical bias and some fundamental uncertainty could prevent the pair from pushing higher over the coming sessions. Indeed, recent upsides already seem to have been pushing the envelope so to speak which might mean a correction or moderation is now in order. Due to this, it may be worth taking a closer look at what caused last week's rally and how this ties in with the fundamental and technical biases moving forward.

Starting with last week's performance, the Kiwi Dollar was in the market's good graces over the past 7 days which resulted in the pair making its way all the way back to the 0.7208 handle by the end of Friday. The rather consistent buying pressure was largely attributable to the disappointing US data sprinkled throughout the week – including both a -0.2% contraction in US Factory Orders and a weaker than expected Unemployment Claims result of 245K. However, one session proved to be particularly bullish as a result of the sixth consecutive uptick in the GDT Price Index (this time of around 0.6%) which saw the NZD claim nearly 50 pips on Tuesday.

Going forward, the question will be whether or not we can expect to see similarly supportive data or if the economic news is going to slap the pair lower. Well, Wednesday will see both the quarterly and yearly NZ GDP figures posted which could provide the necessary buoyancy if they come in on or above targets.

The two prints are forecasted at around 0.7% and 2.7% respectively and, given the general recovery of the nation's dairy industry and the increased tourist arrivals over the past year, we are very likely to see these estimates achieved.

On the face of it, the likelihood of us seeing strong GDP numbers should mean our default bias is going to be bullish. Nevertheless, any positive sentiment could be drowned out by the deluge of US Retail Sales data and the Fed's interest rate decision – both of which are due out just prior to the GDP numbers.

Due to this, we can't quite put forward an argument for further gains purely on fundamental grounds and we may have to take a look at the technicals to get a clearer picture.

When delving into the technical side of things, it becomes clear that the Kiwi Dollar remains broadly bullish but we might begin to see momentum slow as it is now challenging a vital resistance level. Specifically, whilst the EMA bias is highly bullish, the Parabolic SAR remains firmly below price action, and the ADX is signalling that a strong trend is in play, the pair is now highly overbought. Indeed, both stochastics and RSI are signalling that it may be time for the bulls to take a break which might see the historical zone of resistance around the 0.7232 remain intact.

Ultimately, the combination of the mixed technical and fundamental outlooks means that we are likely to see price action moderate this week – potentially leading the NZD to retreat to the 0.7129 mark. However, this may not be the end of the overall uptrend and, instead, it might simply be a bit of a cooling-off period prior to the bulls making another attempt at surging higher. As a result of this, cautious optimism may be well founded in the long-run but the bears may be in the driving seat for the next week at least

Cable Faces Potential Volatility In The Week Ahead

Key Points:

- Cable facing volatility as Bank of England and FOMC decision looms.

- Watch for sharp volatility following the risk events.

- Expect further political risk until Theresa May can form a government.

The Cable had a particularly rough week as the currency pair reacted to a surprising result from the UK election which saw the conservatives lose enough seats to cause a “hung parliament”. Subsequently, the market was shocked and the pair collapsed back below the 1.28 handle to close the week at 1.2741. Subsequently, it makes sense to review last week’s chaotic events with a view to assessing the looming risks as the FOMC gets ready to rule.

Last week was particularly volatile for the Cable as the UK general election result brought with it a sharp surprise for the markets. Rather than a victory for the Theresa May led conservative government, it actually proved to be a veritable rout and resulted in a “Hung Parliament”. This subsequently caused the Cable to decline sharply by around 200 pips and resulted in the pair closing the week well down at 1.2741. Ultimately, it still remains to be seen if Theresa May will be able to form a government in the coming week and this means plenty of volatility for the Cable moving forward.

Looking ahead, besides the ongoing political risk, there is plenty of volatility looming for the Cable in the week ahead. In particular, both the Bank of England and the U.S. Federal Reserve are getting set to determine their interest rates and this could bring with it some surprises. The U.S. Federal Reserve’s FOMC has proved relatively poor at setting expectations ahead of the meeting so it is currently anyone’s guess as to whether the central bank will follow through on their recent rhetoric and lift interest rates. However, given some of the recently poor U.S. economic figures, the risk of further dovishness is relatively high. In contrast, the Bank of England is dealing with rising inflation rates and, although they are unlikely to lift rates, there could be some relatively hawkish rhetoric following the event. Subsequently, it’s highly likely that the Cable will suffer some bouts of volatility as those decisions are released.

From a technical perspective, last week’s sharp fall likely suggests that the consolidation from the 1.30 handle has ceased and we are now moving towards further downside momentum. In addition, the RSI Oscillator still remains within neutral territory and has further space to move before becoming oversold. Subsequently, our initial bias remains on the downside for the coming week with the caveat to watch for volatility from the FOMC decision. Support is currently in place for the pair at 1.2707, 1.2632, and 1.2512. Resistance exists on the upside at 1.2906, 1.2977, and 1.3045.

Ultimately, fundamental and political risk is likely to dictate the Cable’s near term trend as the Fed and BOE both get set to meet to determine their respective interest rates. Subsequently, the pair is likely to have a relatively bumpy week, until these events are ironed out, so monitor the results closely as they are released.

Market Morning Briefing: Euro Has Weakened From The Higher Levels

STOCKS

Dow (21271.97, +0.42%) is trading above 21200 and while that continues, it could be headed towards 21500-21600 in the next few sessions. Near term looks bullish.

Dax (12815.72, +0.80%) indeed tested 12800 last week and if it is able to break above 12850, we could see a sharp rise towards 12900-13000 this week.

Shanghai (3153.55, -0.15%) could possibly dip to 3130-3125 once before again rising up towards 3175-3200 levels. There is enough scope to rise on the upside in the medium term while the long term support near 3020 holds.

Nikkei (19944.14, -0.35%) has bounced from the 21-day MA acting as a god support near 19825. While it acts as immediate support, we could see a bounce towards 20000-20100 again in the coming sessions.

Nifty (9668.25, +0.22%) rose sharply, ending last week on a positive note. We may expect a re-test of 9700 in the next few sessions followed by a sharp break on the upside. Else the consolidation within 9700-9600 may continue for some more time before the upward rally resumes.

COMMODITIES

Gold (1266) remains in a slow corrective move which may take it to the support of 1242 but if the support holds, a quick bounce towards 1307can't be ruled out. Silver (17.14) also continues to weaken and may decline to 16.90 in the coming days. We might see less volatility in the market ahead of FOMC meeting ( on 14th June 2017), which may add further directional clarity.

Copper (2.63) is trading within the narrow range of 2.56-2.67. Only above 2.67, higher resistances of 2.84 can come into consideration. We will remain bullish on copper while it is trading above 2.55 regions.

Brent (48.40) and WTI (46.09) had tested their respective supports of 47.40 and 44.20, and bounced a little, keeping the upside possibility of 50.22 (Brent) and 47.50 (WTI) open. If Brent and WTI manage to close above 50.30 and 47.50 in the next couple of sessions, another attempt for 52 and 49.55 can be seen. Bearish possibilities will come in consideration in case 47.40 for Brent and 44.20 for WTI break down.

FOREX

While keeping the rates unchanged as expected, ECB trimmed Inflation expectations through 2019, driving Euro lower. The Comey testament has been brushed off by the investors, boosting Dollar and UK is headed for a hung parliament, weakening the Pound. Overall Dollar strength.

The initial signal of an upside reversal in Dollar Index (97.30) is visible now and it may rise to 97.60-80 in a day or two. A break above 97.80 may fully confirm a near term reversal and open up higher levels of 98.40 and above. The bias turns bullish now with the support of 96.50 holding firm.

Euro (1.1195) has weakened from the higher levels exactly as discussed for the last few days. Technically it may decline further to the support of 1.1125-15 before any bounce can be considered but the German-US 2Yr (-2.08%) keeps the possibility of a recovery still open (Check Interest Rates section). Bias bearish but not with full conviction yet.

Dollar Yen (110.26) has bounced in line with expectations and may rise to 111.20 but as discussed yesterday, to negate the downside risk, it requires a break above 111.70. Till then, the larger trend remains down.

Pound (1.2746) has taken a major hit from the unexpected UK election results. With the initial shock digested, it may either grind in the range of 1.2700-1.2850 for a few sessions or continue the decline towards 1.2600 immediately. It may take one more trading session which is the more probable path.

Aussie (0.7532) remains indifferent to all the global events and untouched even by the general Dollar strength today. It may end the week in the range of 0.7500-0.7600.

Dollar Rupee (64.21) broke the range of 64.30-70 to the downside and now we have to watch crucial Support at 64.10. If that holds, there could be chances of sharp rise to 64.40-50 again. A break below 64.10, on the other hand, could lead to lower levels near 63.90

INTEREST RATES

The US yields have risen as expected. The 5YR (1.76%), 10Yr (2.20%) and the 30Yr (2.85%) are up from previous levels of 1.74%, 2.18% and 2.84% respectively.

The UK 10YR (1%) is testing support near current levels and could bounce back in the coming sessions to levels near 1.05%.

The Japan 5YR (-0.068%) has been rising sharply compared to the other longer term yields and looks bullish in the near term. The 10Yr (0.06%) could test 0.07-0.08% over today and tomorrow before coming off again in the medium term.

The German-US 10Yr (-1.94%) is almost stable just above immediate support levels and unless that breaks on the downside, there could still be some possibility of a bounce back in euro. But on the other hand if we look at the 2Yr yield spread (-2.11%), it has broken sharply below the support levels indicating a weaker Euro in the coming sessions. We would now have to look closely at the 10Yr yield spread for any indication of a break below support levels to get a better directional cue for the Euro.

USDCHF – Remains Vulnerable But With Caution

USDCHF - With the pair continuing to retain its downside pressure, more decline is envisaged despite price hesitation. However, we a close higher seen the past week, further bullishness is likely. On the downside, support lies at the 0.9650 level. A turn below here will open the door for more weakness towards the 0.600 level and then the 0.9550 level. On the upside, resistance resides at the 0.9750 level where a break will clear the way for more strength to occur towards the 0.9800 level. Further out, resistance comes in at the 0.9850 level. All in all, USDCHF faces further bearishness but with caution

EURUSD – Retains Upside Threats Despite Pullback Risk

EURUSD - With the pair continuing to retain its upside pressure, more strength is envisaged though hesitating the past week. Resistance comes in at 1.1250 level with a cut through here opening the door for more upside towards the 1.1300 level. Further up, resistance lies at the 1.1350 level where a break will expose the 1.1400 level. Conversely, support lies at the 1.1150 level where a violation will aim at the 1.1100 level. A break of here will aim at the 1.1050 level. All in all, EURUSD faces further recovery threats in the new week.