Sample Category Title

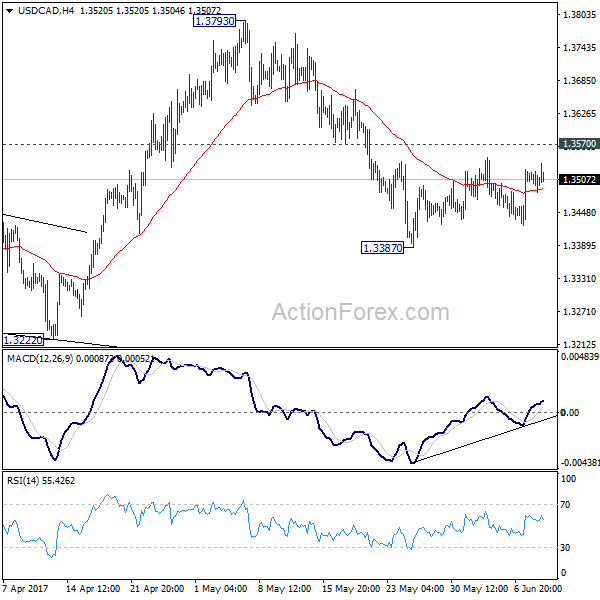

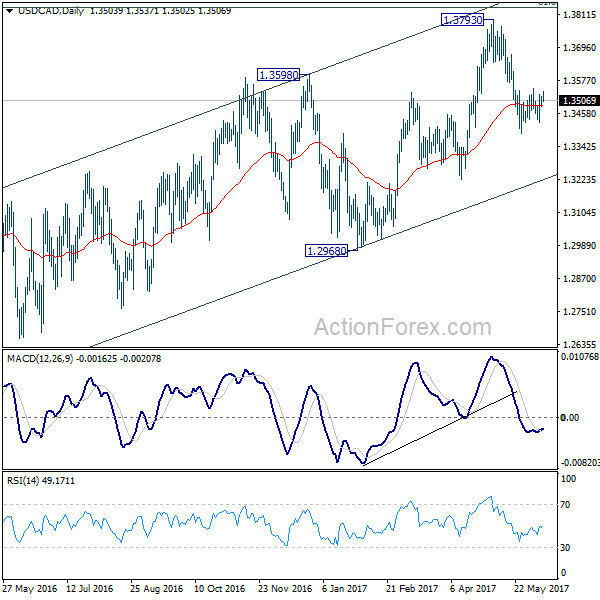

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3486; (P) 1.3503; (R1) 1.3523; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.3387 extends. Upside should be limited by 1.3570 resistance and bring fall resumption. We're holding on to the view that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

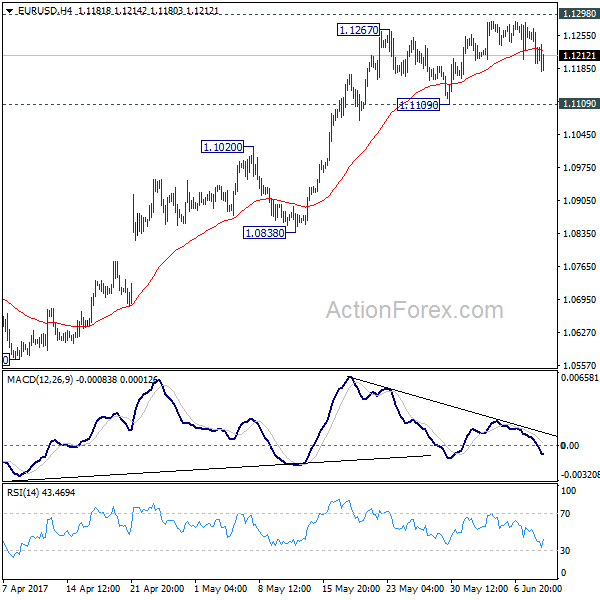

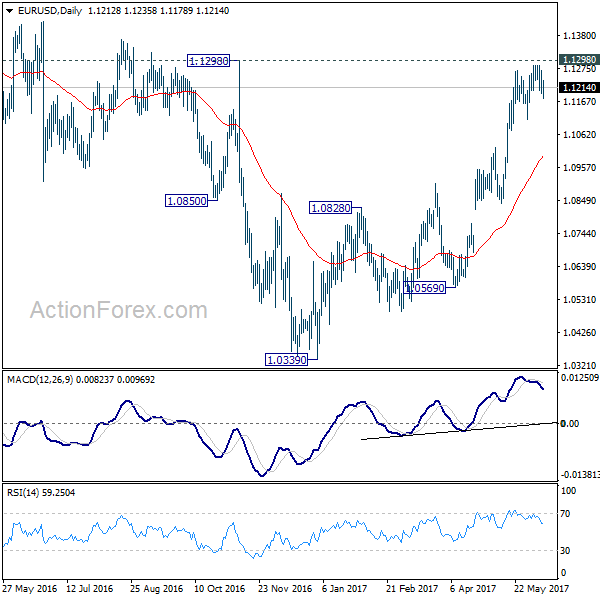

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1181; (P) 1.1225 (R1) 1.1256; More....

Intraday bias in EUR/USD remains neutral with focus on 1.1298 key resistance. Decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. However, break of 1.1109 will indicate short term topping and rejection from 1.1298. In that case, intraday bias will be turned back to the downside for 1.0838 support first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Is The Worst Over For GBP As May Suffers Humiliating Defeat?

It's been quite a memorable night in the UK where once again an election has come and gone and results have come as quite a surprise to both voters and the markets, alike.

Only a month ago, with Theresa May's poll lead at around 20 points, it appeared that the election was going to be a landslide leading to questions about the future of Jeremy Corbyn as Labour leader. One month on and the reality is that the Conservative campaign is being labelled a shambles, it's on course to lose its majority and Corbyn is being praised for a quite remarkable comeback.

While Labour voters may be celebrating, the markets are not in such a bright mood. A hung parliament – as looks very likely now – could be devastating for the preparation of Brexit negotiations which is due to begin in little over a week. A hung parliament was the worst outcome for the markets and yet, under the circumstances the response has been fairly mild. While the reason for this will only become apparent in the coming hours or days, the prospect of a coalition with the DUP or SNP which would take them above the threshold may be what markets are banking on.

Should that fail to materialise, then the moves which we've already seen overnight in the pound may get much worse. The drop in GBPUSD after the exit polls was very significant but even then, it remains slightly above the level that it was trading at prior to May calling the election back in April. Clearly there is no panic yet but should coalition talks fail and the prospect of another election prevail, I struggle to see it maintaining these levels and it would seriously harm the UK's position in Brexit talks and create huge uncertainty.

While the election may remain the focus as we see out the week, UK data will also attract some attention throughout the morning. Manufacturing and industrial production figures, along with trade balance data and an estimate of GDP for the three months to the end of May from NIESR will all be released.

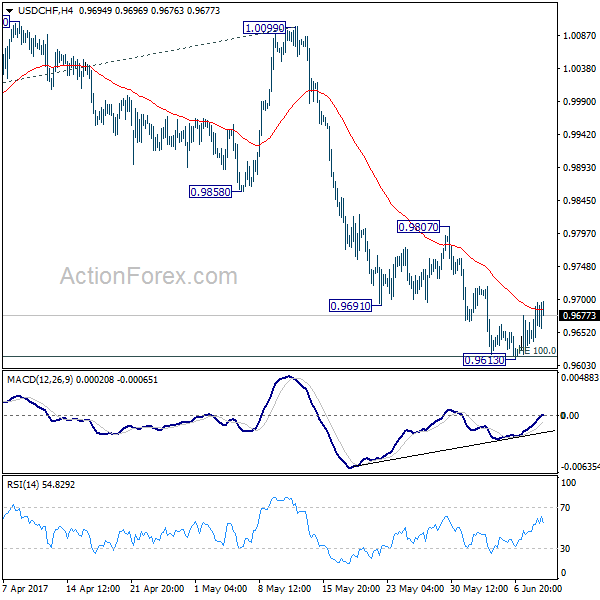

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9635; (P) 0.9666; (R1) 0.9703; More.....

Intraday bias in USD/CHF remains neutral as the corrective recovery from 0.9613 is still in progress. Near term outlook stays bearish as long as 0.9807 resistance holds. When decline from 1.0342 resumes, we'd tart to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

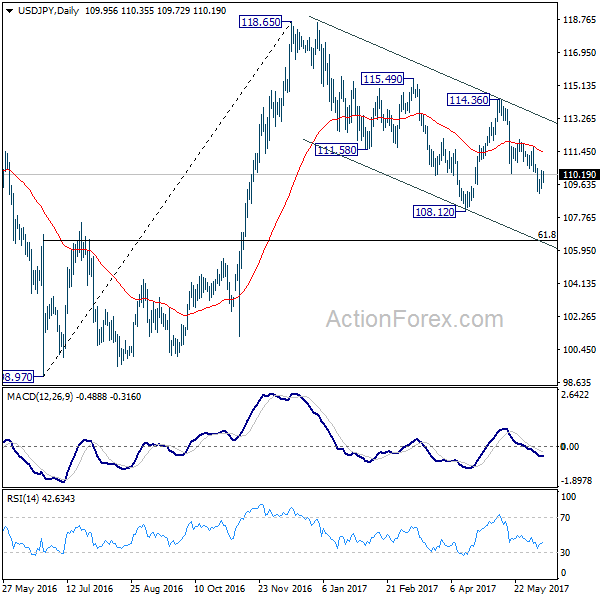

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.47; (P) 109.92; (R1) 110.48; More...

Intraday bias in USD/JPY remains neutral as the corrective recovery from 109.11 is still in progress. Near term outlook remains bearish with 111.70 resistance intact and deeper decline is expected. Below 109.11 will target 108.12 low first. Break will extend whole decline from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. As such decline is seen as a correction, we'll looking for bottoming signal around 106.48. Meanwhile, break of 110.70 will suggest near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

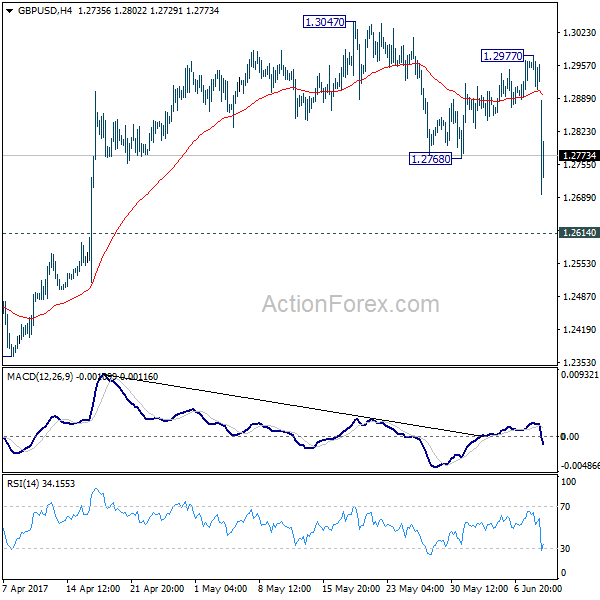

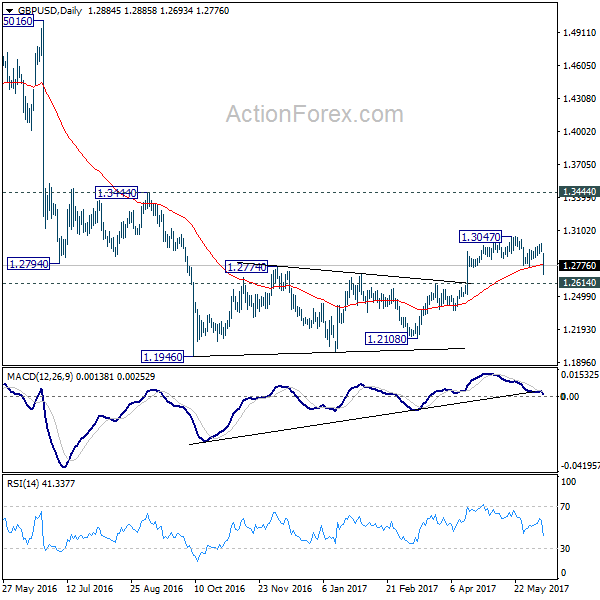

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2944; (R1) 1.2982; More...

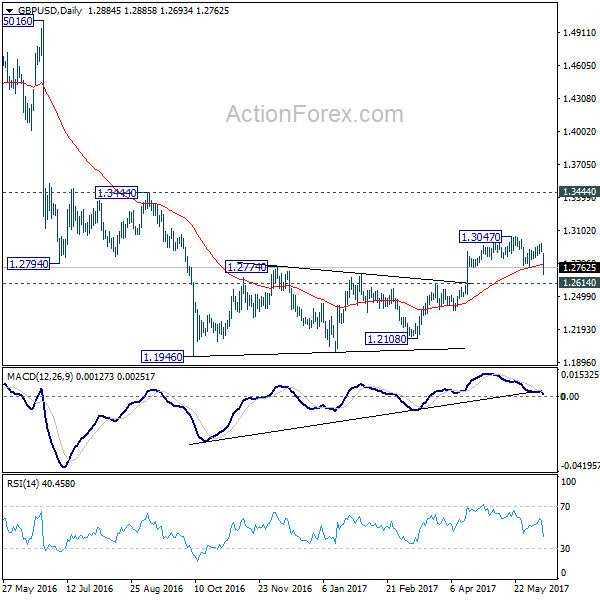

GBP/USD's decline from 1.3047 resumed by diving through 1.2768 to as low as 1.2693 so far. Intraday bias is turned back to the downside for 1.2614 resistance turned support now. Decisive break should confirm the completion of consolidation pattern from 1.1946. In such case, larger down trend should be resuming for a new low below 1.1946. On the upside, break of 1.2977 resistance is now needed to indicate completion of the fall from 1.3047. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

British Pound in Free Fall as May’s Election Gamble Backfires

Sterling tumbles sharply and broadly as the UK election is now very likely proved to be a serious blow to Prime Minister Theresa May and the Conservatives. While the Tories would still get the most seats, exit polls showed that it's going to lose majority and get only 318 seats, down -13 from prior parliament. On the other hand, Labour would probably set 267 seats, up 35. That means UK is now heading to a hung parliament and that is seen by many market participants as the worst case scenario. Much uncertainty would be injected into UK politics, economic policies and most importantly, the Brexit negotiation with EU. And it clearly showed that May's bold decision for a snap election has backfired and it's now even uncertain how long May will stay as Prime Minister.

Technically, GBP/USD's break of 1.2768 support now revived the case of near term reversal. That is rise from 1.2108 has completed at 1.3047 and deeper fall would be seen to 1.2614 key support level. Decisive break there will affirm the view that consolidation pattern from 1.1946 has completed at 1.3047. In such case, the larger down trend from would be resuming for a new low below 1.1946.

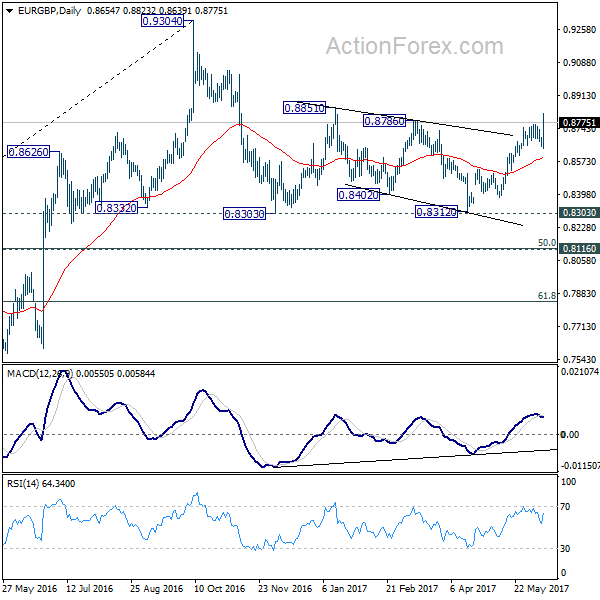

EUR/GBP also resumed recent rise from 0.8312 and took out 0.8786 resistance. Next near term focus is 0.8851 and decisive break there will bring further rally to 0.9304 key resistance. It's too early to say whether the larger up trend from 2015 low of 0.6935 is resuming. We'll monitor the structure of the current rise to assess the outlook.

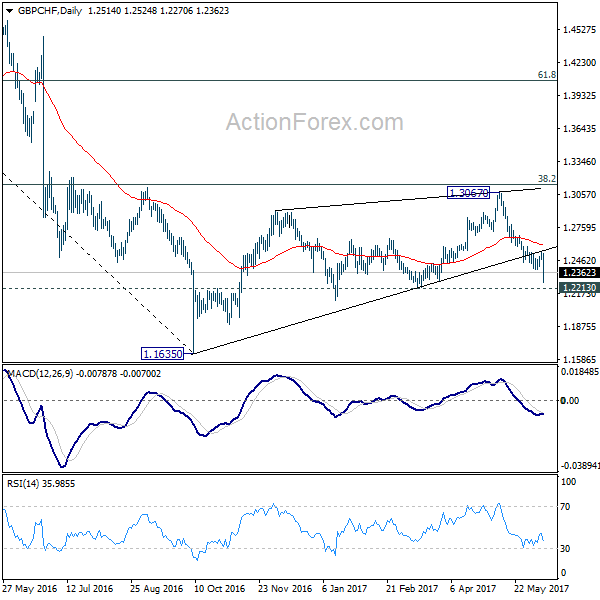

GBP/CHF also resumed the fall from 1.3067 and is now heading to 1.2213 key support level. The medium term consolidation pattern from 1.1635 should be finished at 1.3067, ahead of 38.2% retracement of 1.5570 to 1.1635. Sustained break of 1.2213 should confirm this case and would likely resume the larger down trend through 1.1635 low.

Markets shrugged Comey hearing

The US markets have taken former FBI Director James Comey's hearing in Senate Intelligence Committee rather well. DOW edged to new record high at 21265.69 before paring much of the gain to close at 21182.53, up 0.0%. S&P 500 ended up 0.03% at 2433.79 while NASDAQ rose 0.39% to close at 6321.76. 10 year yield also rose 0.016 to close at 2.194. Without going into the details of the testimony, it's generally perceived that there was no "smoking gun" in the testimony that would trigger impeachment for US President Donald Trump.

ECB took tiny step twoards exit

In Eurozone yesterday, ECB President Mario Draghi poured cold water onto hawks who had anticipated a more upbeat policy statement following recent improvement in macroeconomic data. However, the central bank downgraded the inflation forecasts for three years despite upward revision on GDP growth. The forward guidance was slightly less dovish with the reference "or lower" removed. Honestly, all of us understand that, at the currently exceptionally low (some are negative) interest rates, further rate cuts would offer little help to the economy. Notwithstanding expectations that the ECB would begin preparing the market over QE tapering, the central bank maintained the easing bias, reiterating the commitment to accelerate its monthly asset purchases if necessary. More in ECB Refrained from Talking about Tapering, though Noted that Interest Rates Unlikely Lower.

BoJ Kuroda: Intellectual journey not yet completed

BoJ Governor Haruhiko Kuroda said in a speech at the University of Oxford yesterday that "while the policy approach has steered Japan's economy in the right direction, our intellectual journey has not yet been completed." He pointed out that "the rate of change in the consumer price index recently has been around 0 percent and there is still a long way to go until the price stability target of 2 percent is achieved." A major reason is that inflation expectations have declined and "have continued to be subdued.

On the data front...

Japan M2 rose 3.9% yoy in May. China CPI accelerated to 1.5% yoy in May, PPI slowed to 5.5% yoy. Australia home loans dropped -1.9% in April. German trade balance UK productions and trade balance will be the main focus in European session. Canada will release employment data in US session.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2944; (R1) 1.2982; More...

GBP/USD's decline from 1.3047 resumed by diving through 1.2768 to as low as 1.2693 so far. Intraday bias is turned back to the downside for 1.2614 resistance turned support now. Decisive break should confirm the completion of consolidation pattern from 1.1946. IN such case, larger down trend should be resuming for a new low below 1.1946. On the upside, break of 1.2977 resistance is now needed to indicate completion of the fall from 1.3047. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y May | 3.90% | 4.30% | 4.30% | 4.00% |

| 1:30 | CNY | CPI Y/Y May | 1.50% | 1.50% | 1.20% | |

| 1:30 | CNY | PPI Y/Y May | 5.50% | 5.70% | 6.40% | |

| 1:30 | AUD | Home Loans Apr | -1.90% | -1.00% | -0.50% | |

| 4:30 | JPY | Tertiary Industry Index M/M Apr | 0.50% | -0.20% | ||

| 6:00 | EUR | German Trade Balance (EUR) Apr | 20.3B | 19.6B | ||

| 8:30 | GBP | Industrial Production M/M Apr | 0.70% | -0.50% | ||

| 8:30 | GBP | Industrial Production Y/Y Apr | -0.30% | 1.40% | ||

| 8:30 | GBP | Manufacturing Production M/M Apr | 0.80% | -0.60% | ||

| 8:30 | GBP | Manufacturing Production Y/Y Apr | 0.70% | 2.30% | ||

| 8:30 | GBP | Construction Output M/M Apr | 0.40% | -0.70% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) Apr | -12.0B | -13.4B | ||

| 12:00 | GBP | NIESR GDP Estimate May | 0.20% | |||

| 12:30 | CAD | Capacity Utilization Rate Q1 | 82.40% | 82.20% | ||

| 12:30 | CAD | Net Change in Employment May | 17.0k | 3.2k | ||

| 12:30 | CAD | Unemployment Rate May | 6.60% | 6.50% | ||

| 14:00 | USD | Wholesale Inventories Apr F | -0.30% | -0.30% |

Pound Volatility As Conservatives Look To Lose Their Seat Majority

All eyes are on the British Pound, and there has already been a shock in the early hours of trading on Friday that led to the Pound taking a dive all the way from 1.2950 to below 1.27 following increasing concerns that the UK is heading for a hung parliament.

The Pound is looking under severe pressure with polls indicating that the Conservatives will lose their parliament majority, which looks like another example of traders being on the wrong side of the trade after heavily stacking their cards in favour of a landslide victory for Theresa May when pricing in the UK election.

From a market perspective, a hung parliament is seen as one of the worst possible outcomes to this election because it just injects further uncertainty into the United Kingdom as it heads into Brexit negotiations with the European Union. The whole reason for the unexpected announcement of a snap election from Theresa May was to gain a more dominant hand when representing the UK in negotiations, but this outcome would suggest it has backfired and ultimately will result in the door being opened even wider when it comes to the UK entering further political uncertainty.

If the momentum of the votes begins to shift in favour of what the preliminary polls have suggested will be a hung parliament, the Pound will be at risk to retracing all of its gains that has made since Theresa May unexpectedly called the election. This ultimately means that the Pound could drift to 1.25 within the next few hours if market uncertainty heats up.

Crude Oil Plumbing Depths As 3-Drive Pattern Completes

Key Points:

- RSI Oscillator flirts with oversold levels.

- 3-Drive pattern completes on 4-hour timeframe.

- Watch for a break higher in the coming days.

Crude Oil has been on a wild ride the past few weeks as the commodity has reacted to increased geopolitical risk in the Middle East, as well as rising U.S. Inventory stockpiles. In fact, as I compile this summary the WTI selling is coming strongly in waves as the fragile war of words over Qatar, and their engagement with Iran, seemingly threatens to boil over into actual conflict. However, the technical indicators are telling a different story and we could be just about ready to see a reversal.

In particular, the decline of the past few days has seen the completion of a relatively clear 3-drive pattern on the 4-hour timeframe. Coincidently, the pattern's completion has occurred right on the 78.6 retracement level of the overall bullish wave which seemingly adds to its relevance. In addition, the RSI Oscillator is right on the edge of oversold territory and is now trending sideways which suggests that price action's momentum might be about to change. Finally, WTI prices are currently resting upon a key level of support from early May so it would seem that there are plenty of indicators of a potential turnaround for crude oil in the week ahead

However, any speculative trades to the upside certainly come with plenty of fundamental risk given the ongoing glut of global supply and the risk of a break down in OPEC's supply cap agreement.

There is a real risk that the current argument flooding the Gulf Council members over Qatar's connection with Iran could lead to a break in OPEC's supply cut agreement. However, equally valid is the risk of the current tensions causing military action which would cause crude oil prices to skyrocket.

Ultimately, there are plenty of factors, both fundamental and technical, to suggest that crude oil's decline might have reached its limits. However, the prudent trader would await confirmation of a reversal before countenancing an entry. The most likely scenario involves WTI prices moderating in a sideways direction before turning sharply to rally back towards resistance at $47.73. However, be aware of the risk of volatility from both action in the Gulf States, as well as action from OPEC.

Can The Dollar Yen Recover Despite The Comey Drama?

Key Points:

- The pair could make back some modest ground over the coming sessions.

- Our technical bias remains bullish on a number of fronts.

- Comey saga is still worth bearing in mind.

The Dollar Yen has slowed the pace of its recent downtrend and, in fact, it has actually begun to recover modestly. However, given the ongoing Trump/Comey saga, the fundamental outlook isn't looking so hot for the pair which means we may have to turn to the technical bias for guidance.

First and foremost, the technicals largely indicate that we can expect to see some (if not a lot of) upside action in the near-term. This comes primarily as a result of the medium-term pennant structure that has kept price action contained over the past number of weeks. Specifically, the Dollar Yen’s recent retreat has brought it into conflict with the downside of the pennant which would typically necessitate at least a modest recovery moving ahead.

Furthermore, whilst they have trended out of oversold territory, the stochastics should put a dampener on any additional attempts to push the pair lower in the immediate future. This is largely due to the fact that the oscillator is still flirting with that key 20.0 level which should act as a deterrent to any bears seeking to spark another sell-off.

Another deceptive technical reading that, on the face of things, looks particularly bearish but is actually rather bullish is the parabolic SAR. As shown, if the USDJPY can advance above the 110.40 mark over the next few sessions, the currently bearish indicator will invert — typically a signal that a decent shift in momentum has occurred.

Once the upswing has begun, we expect to see the pair climb to around the 112.00 handle before encountering significant resistance. At this level, the joint influence of the 38.2% Fibonacci retracement, the 100 day EMA, and the central tendency of the overarching structure should present a rather difficult obstacle for the bulls to overcome. What’s more, the pair is already likely to be battling against fundamental headwinds which could mean that this is a medium-term cap on gains.

Ultimately, this forecast is somewhat contingent on the market’s ever unpredictable response to Trump-related drama. However, given the rather sedate reaction to Comey’s scathing testimony, we may have to wait for the case to progress before traders begin to act on the news. In the meantime, the technicals have a fairly firm bias suggesting that some buying pressure is now warranted which could see the pair end the week on a high note.