Sample Category Title

Sterling Plunges on Political Uncertainty after Inconclusive UK Election Result; Dollar Steady after Comey Testimony

Sterling plunged on political uncertainty after an inconclusive result in the UK general elections that took place on Thursday, with no single party having a clear claim to power. The dollar moved higher as it was unfazed by former FBI Director James Comey's testimony yesterday.

The British pound lost over 2% against the greenback, touching near a two-month low of $1.2634. The euro surged against sterling to a high of 88.58 pence. Exit polls showed the likelihood of a hung parliament since Prime Minister Theresa May's Conservative party is expected to win without a majority, just days ahead of the Brexit negotiations.

In other currencies, the euro tested the key $1.1200 level and last traded below it at $1.1185. The yen gave up early session gains as the dollar rose back up to 110.46 yen. The aussie traded in a range in Asia around $0.7535, with little reaction to inflation data out of China, its major trading partner.

Chinese data raised concerns over the broader health of the economy as producer prices tumbled, pointing to an easing of broader price pressures. PPI slowed for a third consecutive month with a reading of +5.5% year-on-year in May versus +5.7 % expected. CPI in May was in line with forecasts at +1.5% year-on-year, accelerating faster than April's +1.2%.

The dollar and US equities saw little impact from Comey's Senate testimony, which is perceived as not threatening President Donald Trump's administration for now.

In commodity markets, gold eased lower in Asian trading to $1,271.16 an ounce from a session high of $1281.48, but remained close to yesterday's lows. Oil prices remained weak, with WTI crude near one-month lows around $45.20 a barrel.

Technical Outlook: EURUSD Cracks Tenkan-Sen/20SMA Pivots, Risk Of Deeper Pullback On Firm Break

The Euro is standing at the back foot in early Friday's trading and probes again below 1.1200 handle, after ECB stayed unchanged on Thursday and chief Mario Draghi did not say anything new in his press conference that markets understood as dovish tone.

The pair is probing through sideways-moving daily Tenkan-sen (1.1197) and rising 20SMA (1.1191), clear break of which would generate stronger bearish signal for deeper pullback from fresh high at 1.1285.

Overall bulls may be hurt by such action, as ECB is unlikely to take any action in tightening in the near future while the Fed is widely expected to hike rates in FOMC next week's meeting that may further weigh on Euro's bulls.

However, current easing could be described as correction which should find ground at strong 1.1114/09 support zone (Fibo 38.2% of 1.0839/1.1285 upleg/30 May trough).

Otherwise, strong reversal signal could be expected on break below 1.1109 and extension towards psychological 1.1000 support seen as likely scenario. Broken 10SMA (1.1228) now acts as resistance which capped Asian trading, with close above here needed to sideline increasing downside risk.

Res: 1.1228, 1.1269, 1.1285, 1.1300

Sup: 1.1180, 1.1114, 1.1109, 1.1062

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1207

The intraday bias is bearish, for a slide towards 1.1109 low. A break through the latter will signal a slide towards 1.1020 major support area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1240 | 1.1360 | 1.1180 | 1.1022 |

| 1.1300 | 1.1610 | 1.1109 | 1.0838 |

USD/JPY

Current level - 110.18

The intraday bias is positive and an eventual break through 110.20-30 resistance will initiate a rise towards 111.20, en route to 112.10. Crucial on the downside is 109.70.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 110.20 | 112.10 | 109.70 | 109.08 |

| 111.20 | 114.30 | 109.08 | 108.12 |

GBP/USD

Current level - 1.2726

The break through 1.2870 crucial low signals a reversal at 1.2977 peak and the bias is bearish, for a further slide towards 1.2610 area. Initial intraday resistance lies at 1.2800.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2800 | 1.2970 | 1.2705 | 1.2610 |

| 1.2870 | 1.3050 | 1.2610 | 1.2610 |

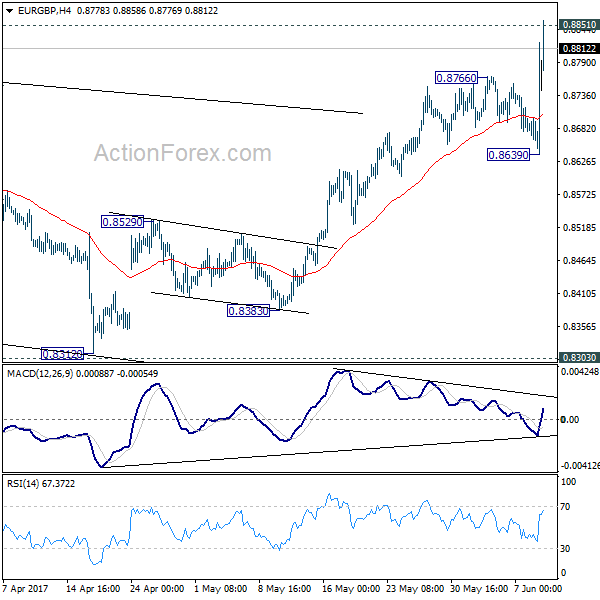

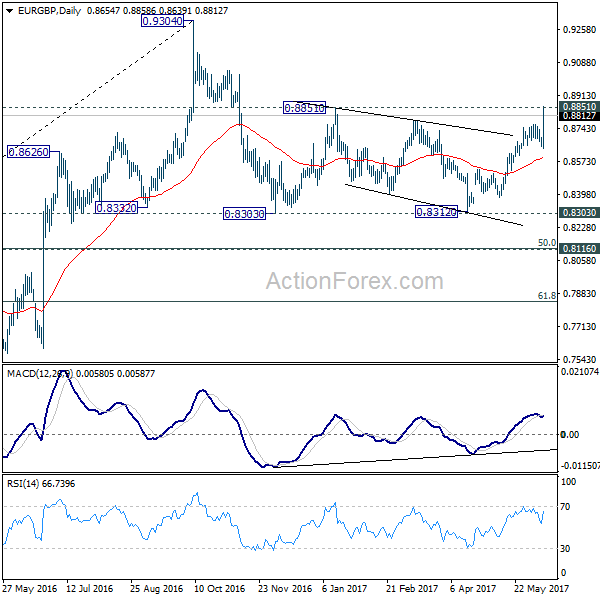

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8638; (P) 0.8668; (R1) 0.8685; More...

EUR/GBP's rally resumed after brief dip to 0.8639 and reaches as high as 0.8858 so far. Intraday bias is back on the upside and decisive break of 0.8851 will pave the way to retest 0.9304 high. There is no firm sign of up trend resumption yet. Hence, we'll be cautious on topping around 0.9304. On the downside, break of 0.8639 is now needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

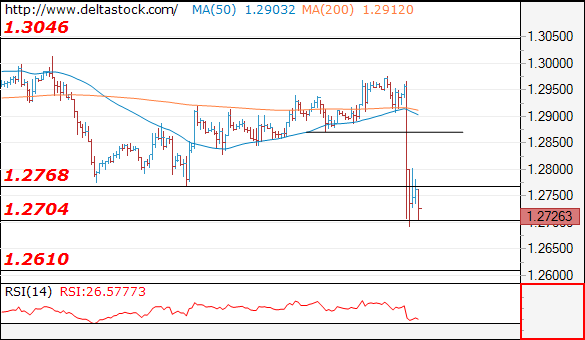

Technical Outlook: Nightmare Scenario For Conservatives Sends Pound Sharply Down

British pound was sharply down after results of UK general election were out and showing that Conservative Party lost majority in the parliament. Nightmare scenario for UK PM Theresa May’s party, as calls for May to resign came immediately after election results.

Since no single party having a clear majority to form the government, the country may fall into political turmoil that could also disrupt Brexit negotiations, just days before start of official negotiations on Britain’s divorce from the EU.

The pound surged through important support at 1.2770 (former higher base/daily cloud top) which generated strong bearish signal, as strong acceleration lower completed Failure Swing pattern on daily chart, confirming strong bearish stance.

Sterling resumed downmove in early hours of European session after consolidation attempts in late Asian hours, signaling strong bearish pressure is building up.

Immediate support at 1.2625/16 (Fibo 61.8% of 1.2365/1.3047/100SMA) is under pressure and further weakness may extend through 200SMA at 1.2576 towards 1.2548 (daily cloud base) and 1.2500 zone (the lowest level before PM May called for snap election).

Political uncertainty is expected to keep sterling under increased pressure, along with technical studies which are firmly bearish on lower timeframes and turning into bearish setup on daily chart.

Meantime, limited corrective actions could be expected, with former strong support at 1.2770 now acting as solid resistance and expected to cap.

Res: 1.2706, 1.3770, 1.2806, 1.2841

Sup: 1.2625, 1.2576, 1.2548, 1.2500

GBP/JPY Daily Outlook

Daily Pivots: (S1) 141.25; (P) 141.81; (R1) 142.89; More....

GBP/JPY's fall from 148.09 resumed after brief consolidation and reaches as low as 142.44 so far. Now that 61.8% retracement of 135.58 to 148.09 at 140.35 is broken and there is no clear sign of bottoming yet. Intraday bias stays on the downside for 135.58 key support next. On the upside, break of 142.75 resistance is needed to indicate completion of fall from 148.09. Otherwise, near term outlook will say mildly bearish in case of recovery.

In the bigger picture, rise from 122.36 medium term bottom is still expected to extend to of 195.86 to 122.36 at 150.42. And decisive break there could pave the way to 61.8% retracement at 167.78. However, as the cross is starting to lose upside momentum, rejection below 150.42 and break of 135.58 support will indicate reversal and bring deeper fall back to retest 122.36 instead.

Market Update – Asian Session: Super Thursday Concludes With Political Chaos In UK

Asia Mid-Session Market Update: Super Thursday concludes with political chaos in UK and more White House scrutiny in US

US Session Highlights

(US) INITIAL JOBLESS CLAIMS: 245K V 240KE; CONTINUING CLAIMS: 1.917M V 1.92ME

(MX) MEXICO MAY CPI M/M: -0.1% V -0.1%E; Y/Y: 6.2% V 6.2%E; CORE CPI M/M: 0.3% V 0.3%E

(QA) Qatar Foreign Min: dispute with Gulf neighbors is threatening the stability of the entire region

(US) Former FBI Dir Comey: the shifting explanations of firing confused and concerned him; administration chose to defame me and the FBI; reasons for firing were lies, plain and simple; I don't think it's for me to say whether conversation with Trump over Flynn investigation was an effort to obstruct; My common sense was that Trump is looking to get something in exchange for granting my request to stay on the job

With all eyes on DC, former FBI Dir Comey's reiterated in testimony the accusations made in his statement released yesterday, and he also accused President Trump of lying about conversations regarding former National Sec Advisor Flynn. However, investors didn't see any cause for panic, and stock markets continued to value stocks positively. Techs and Small Caps made the largest gains on the day, while the broader S&P and blue chips were basically flat.

US markets on close: Dow +0.2%, S&P500 +0.2%, Nasdaq +0.4%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Utilities

Biggest gainers: JWN +10.3%; YHOO +10.2%; NVDA +7.3%

Biggest losers: URBN -10.3%; AAP -3.6%; BWA -3.0%

At the close: VIX 10.2 (-0.2pts); Treasuries: 2-yr 1.32% (+1bps), 10-yr 2.19% (+1bp), 30-yr 2.86% (+2bps)

US movers afterhours

LMNR Reports Q2 $0.24 v $0.18e, Rev $36.9M v $32.1Me; EBITDA $7.8M v $3.4M y/y ; +4.2% afterhours

PAY Reports Q2 $0.30 v $0.30e, Rev $473M v $474Me; Guides Q3 $0.35-0.36 v $0.40e, Rev $463-465M v $485Me; -3.1% afterhours

ENDP FDA requests removal of Opana ER from the market due to risks related to opioid abuse, concern that benefits of the drug may no longer outweigh its risks- FDA requested that Endo Pharmaceuticals remove its opioid pain medication ; -13.6% afterhours

CLDR Reports Q1 -$0.27 v -$0.36e, Rev $79.6M v $75.9Me; Guides Q2 -$0.26 to -$0.24 v $0.25e, Rev $85-86M v $84.0Me, subscription Rev $70-71M, +38-40% y/y ; -15.6% afterhours

Politics

(UK) HUNG PARLIAMENT RESULT CONFIRMED AS CONSERVATIVES FAIL TO SECURE 326 PARLIAMENT SEATS

(US) AG Sessions said to have had a 3rd undisclosed meeting with Russian officials - US press

(US) House passes Dodd-Frank financial law replacement bill - press

Key economic data

(CN) CHINA MAY CPI M/M: -0.1% V 0.1% PRIOR; Y/Y: 1.5% (4-month high) V 1.5%E

(CN) CHINA MAY PPI Y/Y: 5.5% V 5.6%E; 5-month low

(AU) AUSTRALIA APR HOME LOANS M/M: -1.9% V -1.0%E

Asia Session Notable Observations

Asia indices are mixed and volatility has finally settled after a near-24-hour spate of high-profile event risk. In the US, Pres Trump can find solace that he was not the target of FBI investigation. However the charged testimony by former FBI director Comey also paints him in a callous light, subsequent reports that AG Sessions may have had more undisclosed meetings with Russian diplomats, and indication that Democratic leadership is still prepared to pursue obstruction charges leaves the White House - along with its promise of tax reform and infrastructure spending - in peril.

Across the Atlantic, UK elections backfired on PM May, resulting in a hung Parliament rather than her initial intention of bolstering her Parliamentary majority going into Brexit negotiations. Tories' austerity-laden agenda was a tough sell, just as PM May's haphazard communication of policy commitment left her exposed to criticism of being unreliable in negotiations with EU. GBP plunged over 2 big figures to 1.27 after the initial exit polls suggested a strong showing for Labour, hit session lows near 1.2680 after Betfair briefly swung in favor of Labour's Corbyn becoming next PM, and then settled in mid 1.27 range once expectations were distilled to Conservatives ending the day with most votes but shy of the 326 seats needed to form a govt and likely relying on a coalition. PM May will likely pay the ultimate price in the Tory defeat, losing her post.

Asia region was much more subdued relative to ECB-US-UK activity, with developments limited to softer China wholesale and higher consumer inflation. This time around, food CPI decline was much smaller than in the prior month at -1.6% v -3.5% in April. AUD and commodities were little changed on the release.

Speakers and Press

China

(CN) China property investment to keep growing next 1-2 years - Chinese Press

Japan

(JP) BOJ's Kuroda: Japan is no longer experiencing deflation; long way to go until Japan price stability target is achieved - comments in UK

Australia/New Zealand

(AU) Australia Senate to hold inquiry into bank levy plan on Friday, June 16th – Australian Press

Korea

(KR) Korea Joint Chiefs said to investigate report of a small flying object in Gangwon - press

Asian Equity Indices/Futures (01:00ET)

Nikkei +0.4%, Hang Seng -0.4%, Shanghai Composite flat, ASX200 +0.1%, Kospi +0.7%

Equity Futures: S&P500 +0.1%; Nasdaq flat, Dax flat, FTSE100 flat

FX ranges/Commodities/Fixed Income (01:00ET)

EUR 1.1180-1.1235; JPY 109.75-110.35; AUD 0.7525-0.7545; NZD 0.7190-0.7220

Aug Gold -0.1% at 1,278/oz; July Crude Oil flat at $45.66/brl; July Copper -0.3% at $2.60/lb

SPDR Gold Trust ETF daily holdings rise 2.1 tonnes to 867.0 tonne (4th consecutive increase)

(CN) PBOC SETS YUAN MID POINT AT 6.7971 V 6.7930 PRIOR; weakest Yuan fix since June 2nd

(CN) PBOC to inject combined CNY60B v CNY150B prior

(AU) Australia Finance Ministry (AOFM) sells A$800M in 2.75% 2028 bonds; avg yield 2.519%; bid-to-cover 3.08x

Asia equities notable movers

Australia

BlueScope (BSL) +3.6%; Guides H1

SpeedCast (SDA) +1.0%; To be added to ASX200 index

Japan

Toshiba (6502) +8.2%; Bain Capital said to replace KKR in consortium that will include Western Digital and INCJ

FujiFilm (4901) -4.0%; Accounting problems found to extend to Australia operations - Nikkei

Hong Kong

Aac Technologies Holdings (2018) +1.8%; Announces strategic cooperation agreement with Citic Bank for CNY10B

Dongfeng Motor (489) +1.0%; May vehicle sales

China SCE Property (1966) -1.0%; May sales

Nan Nan Resources (1229) -3.6%; FY17 profit alert

Longfor Properties (960) -4.2%; May sales

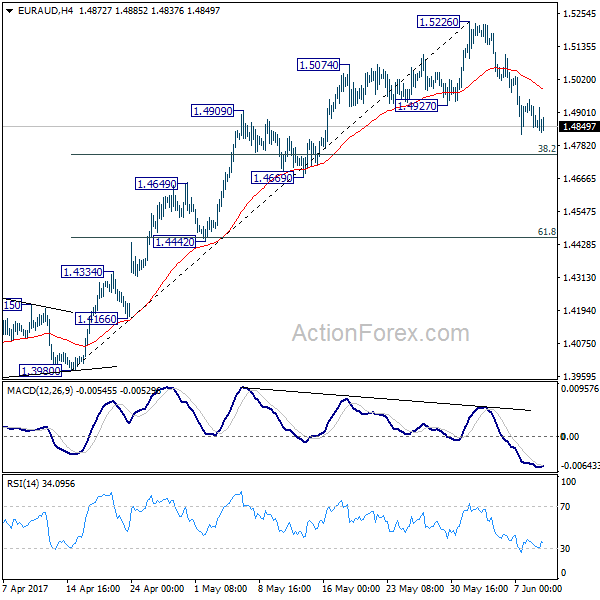

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4821; (P) 1.4885; (R1) 1.4919; More...

The correction from 1.5226 is still in progress and intraday bias stays on the downside. Deeper fall could be seen to 38.2% retracement of 1.3980 to 1.5226 at 1.4750. At this point, we'd expect strong support from 1.4669 to contain downside and bring rebound. Larger rise from 1.3642 is expected to resume later after the pull back completes.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

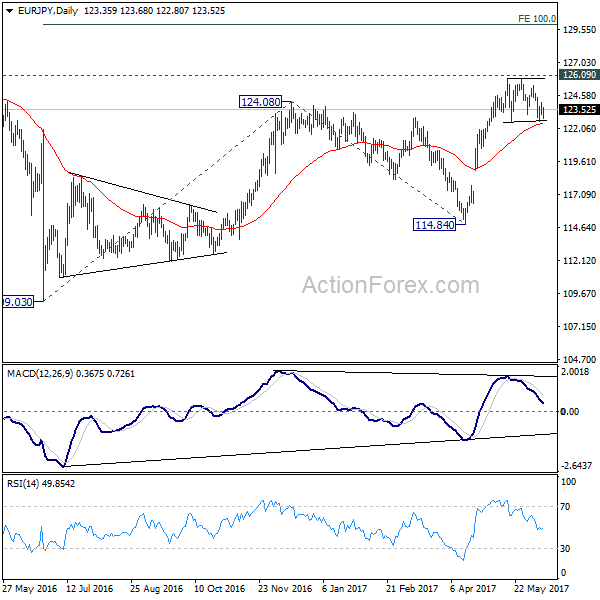

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.01; (P) 123.51; (R1) 123.87; More...

No change in EUR/JPY's outlook as consolidation from 125.80 is still in progress. In case of deeper pull back, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

Research UK: Hung Parliament Adds Government Risk Premium To GBP

- Hung parliament but the Conservative Party seems likely to form a minority government backed by the Democratic Unionist Party (DUP).

- The very slim majority makes it difficult for the new government to govern and it is likely to be put under pressure both by pro-Brexit and pro-EU forces.

- It is difficult to say what this means in terms of Brexit. The new government at least has some thinking to do about how it will proceed with the Brexit negotiations and whether or not to adopt a softer approach.

- Theresa May is currently considering her own position. Therefore, the Conservative Party may be thrown into a new leadership contest.

- A second Scottish independence referendum seems unlikely at this point given the SNP's loss of seats.

- With respect to GBP, we now have a 'government risk premium' on top of the 'Brexit uncertainty premium'. We target EUR/GBP in the range of 0.84-0.90.

Very much against expectations, Theresa May and the Conservative Party fell short of winning enough seats to win a clear majority in the House of Commons. Hence, we have a hung parliament with the Conservative Party as the biggest party. Still, the Conservatives may have won enough seats to remain in power, as Sinn Féin in Northern Ireland has said it will not take its seats (seven seats) and the DUP has said it is willing to cooperate with Theresa May (DUP won 10 seats). Jeffrey Donaldson, an MP from the DUP, has said, 'we have a lot in common, we want to see Brexit work, we want to see the Union strengthened. I think there is a lot of common ground'. See also Reuters. Based on the current projections, we think it is likely that the Conservatives will form a minority government supported by the DUP but it will have a hard time manoeuvring in the House of Commons. It may take at least a few days to form a new government, as the Conservatives probably need to talk with the DUP. Given the very slim majority, it is possible that the new election term will not last the supposed five years, as the government will be weak, not least in connection with upcoming Brexit negotiations.

Theresa May's position has clearly weakened and there is some pressure for her to resign as leader, as the entire Conservative campaign centred on her as a person and her ability to be a stable leader in uncertain times. In her victory speech in her own constituency, Theresa May said that the UK now needs 'a period of stability' without saying whether she wants to stay or not. At least, it was quite interesting that May said that it is the Conservative Party's aim to ensure stability and form a government and not hers. Sources say it will be 50/50 as to whether she resigns or not. Brexit negotiations should have begun in 11 days' time but this seems unlikely given the Conservative Party has now been thrown into a new leadership contest.

Although the polls showed the Conservatives' lead over Labour diminished throughout the election campaign, only a few predicted it would be this close. One reason is that the turnout among young voters – mainly Labour leaning – was higher than in previous elections. Despite the Conservatives winning some of the previous UKIP voters (UKIP totally collapsed from nearly 13% of the votes in 2015 to around 2% now), it was not enough for the Conservatives to increase the number of seats. Overall, the election was a major blow for Theresa May, as prior to it, she was close to 20 percentage points ahead of Labour and Jeremy Corbyn was viewed as a weak leader – now it is quite the opposite.

In Scotland, it is also interesting that the Scottish National Party lost many of the seats they won in the last election in 2015. This – combined with polls suggesting that the Scotsmen want to remain in the United Kingdom – makes it less likely we will get a second Scottish independence referendum.

Brexit clock is ticking but we do not know whether a new government will change the 'hard Brexit' approach

It is difficult to say what this means in terms of Brexit. On the one hand, this could be viewed as a rejection of Theresa May's hard Brexit stance with the UK leaving the single market and the customs union. However, given the election campaign was more about domestic issues like austerity, social care and education than Brexit, it may also be the case that Brexit voters have simply moved on to other issues, as they expect the government to move forward on Brexit. The new government at least has some thinking to do about how it will proceed with the Brexit negotiations and whether or not to adopt a softer approach. Unfortunately, time is short, as there is a sharp deadline by the end of March 2019, where the UK is due to formally exit the EU. No matter which Brexit approach the new government takes, the slim majority means it will be put under pressure both by pro-Brexit and pro-EU forces in parliament. One of the reasons for Theresa May to call for a snap election was to consolidate power within the Conservative Party and the House of Commons, making it easier for her to negotiate Brexit, but the election result has actually made it more difficult. One game changer could be more cooperation across the political centre between moderate Conservatives and moderate Labour MPs.

GBP: worst-case outcome adds to Brexit risk premium

So far, the election outcome looks close to the worst possible for sterling – if any winner, it may be regarded the EU. The prospect of a hung UK parliament based on the first exit poll initially led EUR/GBP to jump above the 0.88 level last night but the knee-jerk reaction has been moderated a bit with the possibility of a Tory-led government that may just about get a slim majority and the cross is trading around 0.8780 at the time of writing. What matters for sterling near term is the strength of the government that goes to Brussels to negotiate Brexit terms on behalf of the UK – and with any possible governing coalition set to be weak, so will GBP be. There is clearly a risk of EUR/GBP breaking above 0.88 again if the Tories fall short of even a slim majority. Notably, speculators covered GBP shorts ahead of the election, suggesting room for speculative GBP selling near term. What matters for the sterling longer term are the Brexit terms – and the prospect for these have not become more favourable following the present election result as negotiation power has essentially shifted from the UK to the EU. However, if the new government adopts a softer Brexit approach it may be GBP positive later on, but it is obviously very speculative at this point.

Our Brexit-corrected medium-term valuation (MEVA) model estimate for EUR/GBP is around 0.83, which notably suggests that even when Brexit uncertainty is out of the way, GBP is not necessarily set for large-scale appreciation. But it remains too early to judge e.g. the implications for trade terms from this election outcome. On top of the 'Brexit uncertainty premium', which has been haunting GBP markets since June last year, a form of 'government risk premium' has now been introduced for the very short term as well: almost irrespective of what government is formed, the UK will not be heading for Brexit negotiations with any great sense of confidence based on the election result as it stands at present, and this will weigh on the pound. We see EUR/GBP in the 0.84-0.90 range near term.

A wildcard for GBP would be a new election: while this would introduce continued uncertainty for the short term, it would also open up the option of a majority government after voters had their say again, and possibly be GBP positive eventually that way around