Sample Category Title

Market Update – Asian Session: Japan Q1 Final GDP Revised Lower

Asia Mid-Session Market Update: Japan Q1 Final GDP revised lower; China trade surplus undershoots consensus on higher Import growth

US Session Highlights

(US) DOE CRUDE: +3.3M V -3.5ME; GASOLINE: +3.3M V 0ME; DISTILLATE: +4.4M V +0.5ME (first gasoline build since April)

(IR) Iran Revolutionary Guards spokesperson: Saudi Arabia was behind terrorist attacks in Tehran today - press

Despite tomorrow's super Thursday - UK elections, Comey testimony, ECB meeting and a possible result from Brazilian courts on Temer - stocks managed to post small gains across the board. Political risk in the US, however, seemed to be subsiding after former Dir Comey's opening statement for his congressional testimony tomorrow was posted online. The S&P Energy sector posted large losses, down 1.6% on the day as crude oil prices dropped 5%.

US markets on close: Dow +0.2%, S&P500 +0.2%, Nasdaq +0.4%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Energy

Biggest gainers: SIG +4.0%; ICE +3.4%; GGP +3.1%

Biggest losers: NFX -7.0%; TAP -6.5%; HP -6.0%

At the close: VIX 10.4 (-0.1pts); Treasuries: 2-yr 1.31% (+1bps), 10-yr 2.18% (+3bp), 30-yr 2.84% (+3bps)

US movers afterhours

VSTM To present long-term follow-up data from DYNAMO study at 14th International Conference on Malignant Lymphoma ; +11.3% afterhours

OKTA Reports Q1 -$0.50 v -$0.61e, Rev $53.0M v $48.5Me; Guides Q2 -$0.26 to -$0.25 v -$0.25e, Rev $55-56M v $54.0Me ; +7.4% afterhours

AGX Reports Q1 $1.31 v $0.81 y/y, Rev $230.5M v $130.3M y/y; EBITDA $32.5M v $20.2M y/y; +4.2% afterhours

GEF Reports Q2 $0.67 v $0.71e, Rev $887.4M v $899M; Narrows FY17 adj Class A EPS $2.84-3.02 v $2.92e; -8.7% afterhours

DTEA Reports Q1 -C$0.04 v +C$0.06 y/y, Rev C$48.7M v C$44.5M y/y; CFO resigns; -8.9% afterhours

Politics

(UK) According to Survation poll, Conservative party lead over Labour stands at 41.3% v 40.4%; 1-pt margin is similar to prior; BMG poll has Conservatives ahead of Labour by 46% to 33% margin.

(US) House Speaker Ryan: Obviously not appropriate for Pres Trump to have asked for former FBI director Comey's loyalty - press

Key economic data

(CN) CHINA MAY TRADE BALANCE: $40.8B V $47.8BE; (CNY): 281.6B V 324.1BE

(JP) JAPAN Q1 FINAL GDP Q/Q: 0.3% V 0.6%E; ANNUALIZED GDP: 1.0% (3-quarter low) V 2.4%E

(AU) AUSTRALIA APR TRADE BALANCE (A$): +0.56B V +2.00BE (6th consecutive surplus, smallest surplus in 6 months)

(CN) China Passenger Car Association (PCA): May vehicle sales 1.78M units, +1.2% y/y; YTD sales 9.05M units, -0.9% y/y

Asia Session Notable Observations

Asian equity markets are mixed with modest upward bias as traders look ahead to Super Thursday with some relief. Ahead of his testimony in Congress, the statement of former FBI director Comey indicated he has expressed to Pres Trump that he is not under investigation about alleged Russia campaign meddling, though it did confirm Trump tried to get Comey to ease up on National Security Advisor Flynn. ECB decision will be closely watched for any further discussion of tapering QE, while the UK polls show wide variability of Conservatives lead from 1pt to double-digits.

China Trade surplus was below expectations in both USD and CNY term, but components were more constructive as annual growth in Exports and Imports topped consensus in both currencies. In CNY, Import growth was especially impressive at 22.1% v 8.3%e, with shipments of Iron Ore rising double digits and Oil up over 8% at the highest volume on record.

USD majors were little changed with the exception of a sharp rise in JPY following a press report citing BOJ sources that the central bank is considering ways of communicating it is discussing the shape of Japan's QE exit without signalling it is any closer to doing so. USD/JPY pair fell some 50pips below 109.50 on the report. Timing of the discussion is especially questionable after Japan's Q1 final GDP was revised lower to just 1% annualized from over 2% prelim due to downward revisions in residential investment and consumption.

Speakers and Press

China

(CN) China State Council meeting chaired by Premier Li approves plan to cut corporate taxes by CNY1.0T - Chinese press

(CN) According to China Bank of Communications (BoCom) and Nielsen study, China Wealth Index fell to 135 in May from 138 in Mar - Shanghai Daily

Japan

(JP) BOJ reportedly to re-calibrate communications to acknowledge it is considering how to communicate exit from QE and also convey it will not be on agenda any time soon - financial press citing BOJ sources

(JP) Japan’s FSA said to seek to limit regional banks exposure to bonds – Japanese press

(JP) BOJ's Iwata: BOJ easing not intended to support govt funding - press

(JP) BOJ's Amamiya: Reiterates view that Japan is still halfway to achieving its 2% price target - press

(JP) Japan Cabinet official: Govt's view that economy remains in "moderate recovery" remains unchanged following today's GDP data - press

Australia/New Zealand

(AU) Australia signs multilateral convention to prevent tax avoidance

(NZ) RBNZ: May see significant benefits from Debt to Income instrument - press

Korea

(KR) North Korea said to have been confirmed to fire several projectiles now assumed to be missiles today - Korean press citing joint chiefs of staff

(KR) South Korea govt think tank (KDI) monthly report: Reiterates economy is on modest recovery track - Korean press

Asian Equity Indices/Futures (00:30ET)

Nikkei flat, Hang Seng +0.2%, Shanghai Composite +0.1%, ASX200 +0.1%, Kospi -0.3%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.1%, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1245-1.1265; JPY 109.70-110.00; AUD 0.7525-0.7550; NZD 0.7185-0.7210

Aug Gold -0.5% at 1,287/oz; July Crude Oil +0.3% at $45.99/brl; July Copper +0.6% at $2.57/lb

SPDR Gold Trust ETF daily holdings rise 9.8 tonnes to at 864.9 tonne (3rd consecutive increase)

(CN) PBOC SETS YUAN MID POINT AT 6.7930 V 6.7858 PRIOR; first weaker Yuan fix in 7 sessions

(CN) PBOC injects CNY150B v CNY180B prior in combined 7-day, 14-day and 28-day reverse repos

(JP) Japan MoF sells ¥1.99T in 0.1% 5-year JGB bonds; avg yield -0..65% v -0.117% prior; bid-to-cover: 4.71x v 3.59x prior

Asia equities notable movers

Australia

Goodman Group (GMG) -1.1%; Cut at JPMorgan

BHP (BHP) +0.4%; Raised at UBS

Woodside Petroleum (WPL) -2.2%; Oil price down; Informed that Far will not support the Senegal Development project

Japan

Toshiba (6502) +4.8%; Broadcom said to be close to being named the preferred bidder for chip unit - Asahi

Dentsu (4324) -2.6%; Reports May non-consolidated sales -6.8% y/y

Japan Display (6740) -4.2%; Delays investment in JOLED until at least 2018, with the purchase date yet to be determined

Hong Kong

Cathay Pacific (293) +6.3%; Said to cut about 400 jobs today - HK press

Sino-Ocean Group (3377) -0.8%; May contracted sales

Technical Outlook: Pound Steady Near Two-Week High As Voting Starts

British pound is holding around fresh two-week high at 1.2970 posted on Wednesday, as vote starts. Expectations that Conservative party will win a majority in a Britain's election keep sterling steady.

Polls released on Wednesday showed that Tories keep lead against the Labour party and are on track for a victory that would further boost pound.

Technical studies are bullish and favor further advance. Wednesday's close above weekly cloud base (1.2950) which capped recovery and maintained pressure during past three weeks, could be seen as initial bullish signal.

The pair eyes initial barriers at 1.3000 (psychological barrier) and 1.3047 (18 May recovery peak) and may extend rally towards projected targets at 1.3150/1.3200 on victory that will provide Conservatives a healthy majority in the parliament.

On the other side, pound may come under pressure if Tories' victory provides majority of less than 40 seats in the parliament and risk slide towards 1.2770 higher base zone.

Alternative scenario on Labour victory could trigger stronger bearish acceleration and risk return to 1.2000 zone (lows of post-Brexit vote fall).

Res: 1.3000, 1.3014, 1.3047, 1.3109

Sup: 1.2949, 1.2908, 1.2887, 1.2853

EUR/CHF Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Doji

• Time of formation: 20 Feb 2017

• Trend bias: Up

Daily

• Last Candlesticks pattern: Doji

• Time of formation: 1 Sep 2016

• Trend bias: Near term down

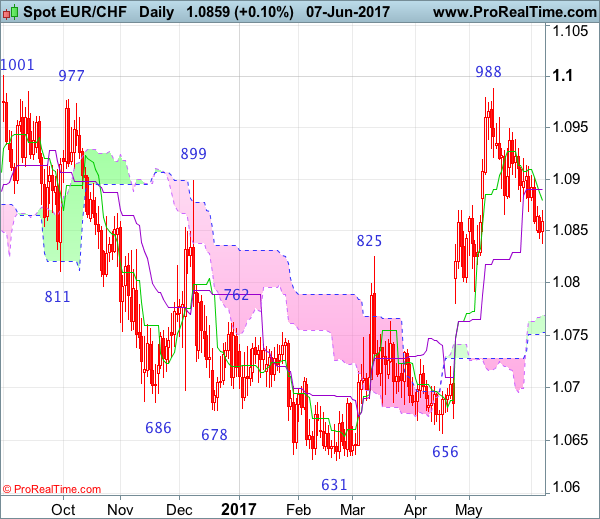

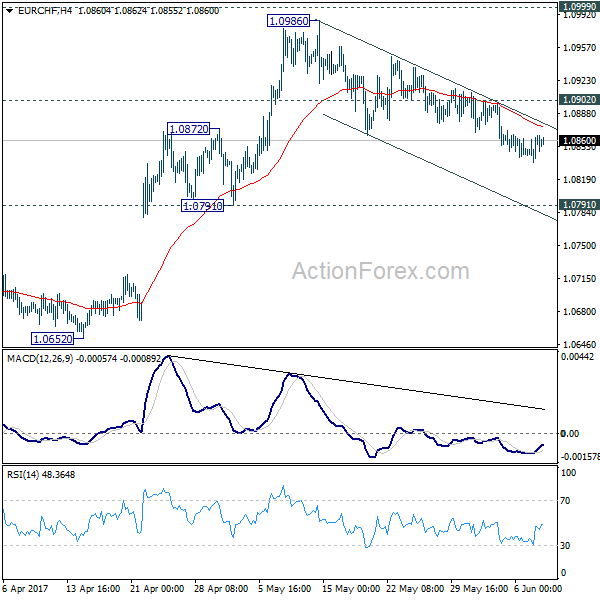

EUR/CHF – 1.0860

The single currency met resistance at 1.0949 last month and has slipped again since, suggesting the fall from 1.0988 top is still i progress and margins weakness from here cannot be ruled out, however, reckon downside would be limited to support at 1.0792 and bring rebound later to 1.0900-10 but break of resistance at 1.0949 is needed to signal the pullback from 1.0988 has ended, bring test of 1.0960, break there would suggest upmove has resumed for retest of 1.0988, then towards previous resistance at 1.1001. Looking ahead, only a break there would retain bullishness and encourage for headway to 1.1050-60, then 1.1100, having said that, price should falter below another previous resistance at 1.1201.

On the downside, expect pullback to be limited to 1.0820 and said support at 1.0792 should hold, bring another rise later to aforesaid upside targets. A daily close below this support at 1.0792 would abort and signal top is formed instead, bring subsequent fall to the lower Kumo (now at 1.0753) and then towards 1.0700-10 but support at 1.0671 should remain intact, the single currency shall stage another rebound from there.

Recommendation: Hold long entered at at 1.0865 for 1.1065 with stop below 1.0765.

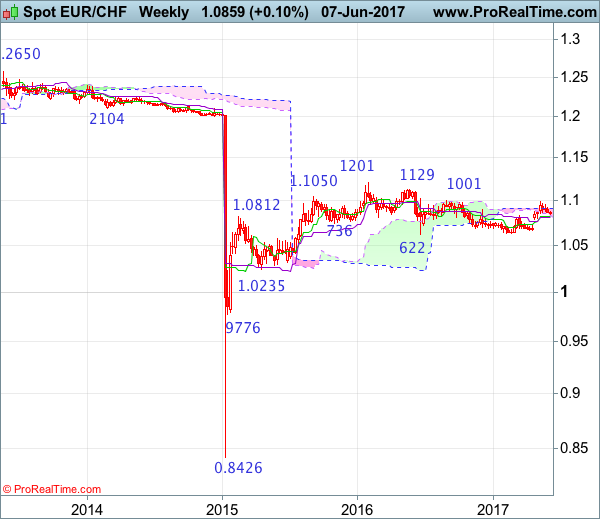

On the weekly chart, euro met resistance at 1.0949 last month and has traded lower, suggesting further consolidation below resistance at 1.0988 would take place, however, reckon downside would be limited and support at 1.0792 should hold, bring another rise later, above 1.0960 would signal pullback from 1.0988 has ended, bring retest of this level, break there would extend recent upmove from 1.0631 to previous resistance at 1.1001, a sustained breach above this level would signal the fall from 1.1201 has ended, bring further gain to 1.1100 and possibly test of resistance at 1.1129 but price should falter below said recent high at 1.1201, bring retreat later.

On the downside, expect pullback to be limited to 1.0820 and said support at 1.0792 should hold, bring another rise. Below support at 1.0780 would abort and signal top has been formed at 1.0988, bring further weakness to 1.0720 but still reckon support at 1.0656 would remain intact, bring another rally later.

Traders Bracing For Big Moves In Euro Cable

After a slow start to the week, traders are getting prepared for a rough ride in the currency markets. Although Comey's testimony has attracted most of the media headlines, we didn't see any significant disclosures from the prepared remarks released yesterday. This explains the recovery in U.S. equities after a fall in the early hours of trading yesterday. While we cannot assume anything, a base case scenario would not be a big surprise to arise from Comey's testimony before Congress. I think that the ECB meeting and the UK election are the risk events that will produce the big moves today.

The Euro has been trending significantly higher for the past three months, appreciating by more than 7% against the Dollar since early March. Although this reflects a sign of confidence in the Eurozone, it's kind of problematic for the ECB who's been fighting deflation for many years. Reports released yesterday citing unnamed official sources indicated that the Central Bank will lower the inflation forecast for the next three years. The impact on the single currency was limited as the lower inflation projections were offset by higher growth expectations. It's obvious we'll not see any change in monetary policy today, and the key driver to the Euro will be the risk assessment on the economy. If the ECB amends its risk assessment to “neutral” from the current “downside”, EURUSD could easily break above 1.13 and move towards 1.15. If the ECB disappoints and Mario Draghi doesn't reflect confidence in the economy's recovery, the EURUSD may be headed for a sharp selloff.

Sterling traders seemed to be pricing a May victory in today's snap election. GBPUSD appreciated 0.4% yesterday as latest opinion polls indicated that a Tory majority is still on the cards. The higher the margin Conservatives win by, the more negotiation power May will have on Brexit terms, and the higher the Pound goes from here. I think that we can easily see a move in excess of 200 pips to the upside or the downside depending on the outcome and how much it deviates from current expectations.

Markets Brace For ‘Super Thursday’

Following a rather slow start to the week, various political and monetary policy events scheduled for today will be shaping the outcome. In the US, former FBI Chief, Comey is expected to testify to Congress. The markets did not react much when a copy of the speech Comey is due to give was released; the implications could be wide and far-reaching. In Europe, the UK's general elections are underway. The British pound is likely to see some volatility. The snap elections were called by the incumbent Prime Minister Theresa May in hopes of consolidating her position. However, with various polls showing a narrowing lead between the Labour party and the Conservative party, the possibility of a hung parliament or a victory by the Tories albeit with smaller margin is real.

The ECB's monetary policy meeting is also scheduled for today. The euro has rallied in expectations of a hawkish ECB meeting. Yesterday, the EURUSD saw some volatility as rumors suggested about the potential changes to the GDP and inflation. The scope for the euro bulls to be disappointed is quite likely with the markets running ahead with expectations ahead of today's meeting.

EURUSD intraday analysis

EURUSD (1.1252): The EURUSD continues to maintain its range within last Friday's high and low. Price action has practically stalled near 1.1275. With price action staying firmly within Friday's high and low of 1.2844 and 1.1204, this range could be breached today into the ECB meeting. For the moment, the bullish flag pattern on the daily chart remains intact with the bias to the upside. But considering that price did not post much gains to the upside, the momentum could be exhausting. Below 1.1245, price action could see a test towards 1.1200. However, a decline below 1.1200 will shift the bias to the downside.

GBPUSD intraday analysis

GBPUSD (1.2953): The British pound posted some gains yesterday, but on the daily chart, the momentum looks to be slowing down. GBPUSD could remain range bound below 1.3000 and 1.2800. A breakout from this level will signal further continuation in the near term. A clear majority for the Tories will no doubt keep the British pound supported to the upside. However, in the event of a break down in price below the 1.2800 support, we can expect to see some strong downside, towards 1.2600 with the possibility to extend the declines to 1.2400 as well.

USDJPY intraday analysis

USDJPY (109.93): The USDJPY managed to post a reversal near the support zone seen at 109.50 - 109.25. Closing on a bullish note at the support zone, the reversal comes after the previous day's strong declines. Price action has lifted firmly off this support level. However, further upside is required to confirm this view. For the moment, the bias remains to the upside on a close above 109.50. This bias validates the upside momentum towards 110.79 where resistance can be developed. The USDJPY could be determined by the developments lined up during the day with further clarity coming out only later.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0841; (P) 1.0853; (R1) 1.0870; More...

No change in EUR/CHF's outlook. Corrective fall from 1.0986 might extend. But downside downside should be contained by 1.0791/0872 support zone, probably around 55 day EMA (now at 1.0829). Rise from 1.0629 is expected to resume later. Above 1.0902 minor resistance will turn bias back to the upside for 1.0986/0999.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

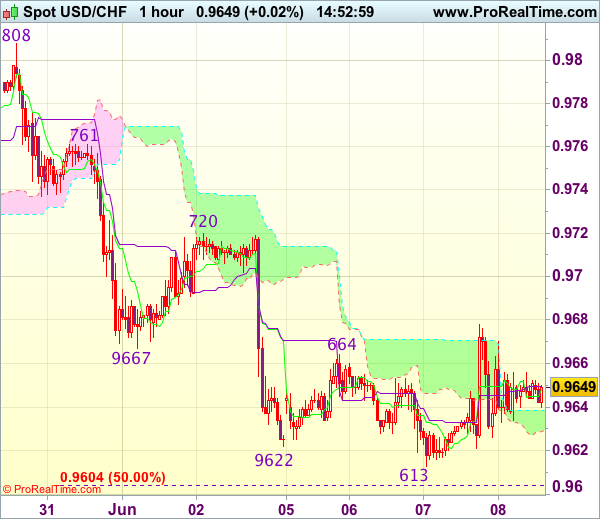

Trade Idea : USD/CHF – Sell at 0.9720

USD/CHF - 0.9645

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9648

Kijun-Sen level : 0.9650

Ichimoku cloud top : 0.9639

Ichimoku cloud bottom : 0.9629

Original strategy :

Sell at 0.9720, Target: 0.9620, Stop: 0.9755

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9720, Target: 0.9620, Stop: 0.9755

Position : -

Target : -

Stop : -

Dollar’s rebound after marginal fall to 0.9613 suggests consolidation above this level would be seen and corrective bounce to 0.9680-85 is likely, however, reckon upside would be limited to resistance at 0.9720 and bring another decline later to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) but oversold condition should limit downside to 0.9570 and price should stay above support at 0.9550, risk from there has increased for a rebound to take place later.

In view of this, we are looking to sell dollar on recovery as resistance at 0.9720 should limit upside. Above 0.9740 would abort and signal a temporary low is formed instead, bring a stronger rebound to 0.9761 resistance but price should falter below resistance at 0.9808.

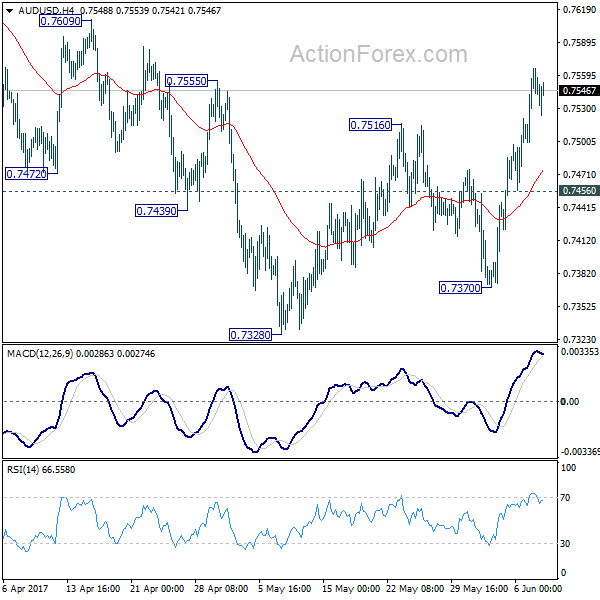

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7510; (P) 0.7538; (R1) 0.7578; More...

Intraday bias in AUD/USD remains on the upside for the moment. Pull back from 0.7748 should have completed at 0.7328. Further rally would be seen to 0.7748 and possibly above. But then, we'll be cautious on topping again as it approaches medium term fibonacci level at 0.7849. On the downside, below 0.7456 minor support will turn bias back to the downside for 0.7328 short term bottom.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8091) and above.

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2973

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2964

Kijun-Sen level : 1.2932

Ichimoku cloud top : 1.2908

Ichimoku cloud bottom : 1.2905

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although sterling has continued edging higher and marginal gain to 1.3000 cannot be ruled out, however, reckon upside would be limited to indicated previous resistance at 1.3015, bring retreat later. Only a break of 1.3015 would signal early upmove has resumed and bring retest of recent high at 1.3048 first.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below the Kijun-Sen (now at 1.2932) would bring test of 1.2900 but only break of support at 1.2871 would signal top is formed, bring weakness towards key support at 1.2830.

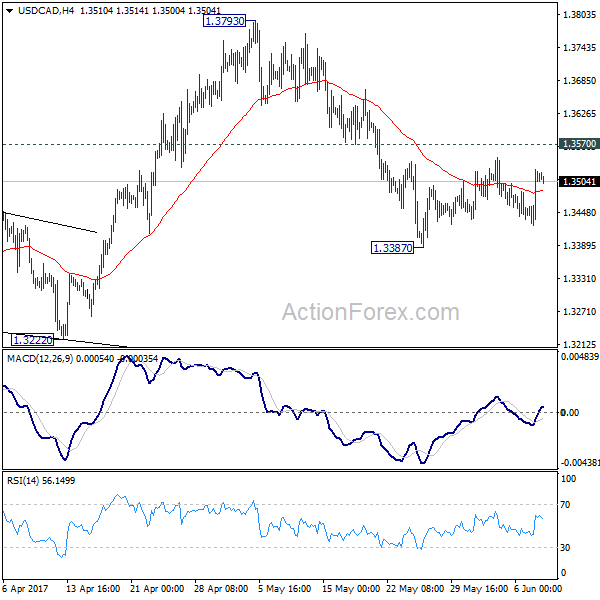

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3448; (P) 1.3486; (R1) 1.3547; More....

USD/CAD recovers but it's still bounded in tight range above 1.3387 temporary low. Intraday bias remains neutral for the moment. While consolidation from 1.3387 might extends, upside should be limited by 1.3570 resistance and bring fall resumption. We're holding on to the view that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.