Sample Category Title

Trade Idea: GBP/USD – Stand aside

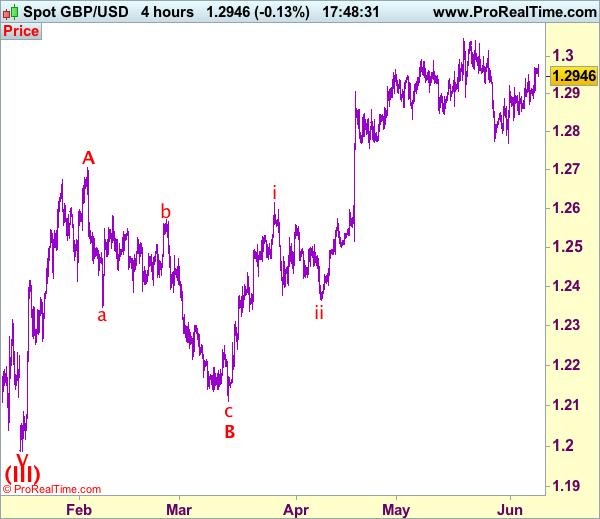

GBP/USD – 1.2943

Recent wave: Wave V of larger degree wave (III) has ended at 1.1986 and major correction has commenced from there for gain to 1.3000 and 1.3140-50

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

The British pound edged higher after brief pullback and gain towards 1.3000 cannot be ruled out, however, reckon resistance at 1.3015 would hold, bring retreat later. Only break of 1.3015 would signal upmove has resumed for retest of 1.3048 resistance break there would confirm and extend headway to 1.3075-80, then 1.3100-10 later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

On the downside, whilst pullback to 1.2900 cannot be ruled out, break of 1.2870-75 is needed to signal top is possibly formed, bring weakness to 1.2850 but break of indicated key support at 1.2830 is needed to revive bearishness and signal the rebound from 1.2769 low has ended, bring further fall to 1.2800 first.

EUR/JPY Monitoring Support At 122.56, EUR/GBP Ready For Another Leg Lower, EUR/CHF Continued Weakness.

EUR/JPY Monitoring support at 122.56.

EUR/JPY is trading lower. Hourly support is given at 122.56 (18/05/2017 low). Hourly resistance can be found at 125.82 (16/05/2017 high). Major support is given at 114.90 (18/04/2017low).

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Ready for another leg lower.

EUR/GBP's bullish momentum has faded around resistance at 0.8787 (13/03/2017 high). The pair is now going lower. Strong support can be found at 0.8304 (05/12/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Continued weakness.

EUR/CHF is trading lower. The pair has broken support given at 1.0866 (18/05/2017 low). We believe that the medium-term pattern suggests us to see continued bearish pressures towards hourly support that can be found at 1.0792 (03/05/2017 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

USD/CHF Heading Lower, USD/CAD Sideways Price Action, AUD/USD Strengthening.

USD/CHF Heading lower.

USD/CHF continues its decline below support given at 0.9692 (22/05/2017 low). Strong resistance is given at 1.0107 (10/04/2017 high). Expected to show continued weakness towards stronger support at 0.9550 (09/11/2017 low).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015

USD/CAD Sideways price action.

USD/CAD is trading below 1.3500. The pair has exited short-term uptrend channel. Hourly support can be found at 1.3424 (28/05/2017 low) then 1.3388 (25/01/2017 high). Expected to show continued very short-term bearish pressures.

In the longer term, there is now a death cross with the 50 dma crossing below the 200 dma indicating further downside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Strengthening.

AUD/USD is pushing higher since the pair has failed to reach hourly support given at 0.7329 (09/05/2017 low). As long as prices remain below resistance at 0.7608 (17/04/2017 high), there are nonetheless strong downside risks.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Stalling Below 1.1300, GBP/USD Short-Term Bullish, USD/JPY Bearish Pressures Under 110

EUR/USD Stalling below 1.1300

EUR/USD is consolidating below strong resistance given at 1.1300 (09/11/2017 high). Hourly support is given at 1.1110 (22/05/2017 low) has been broken. Stronger support lies at 1.0842 (11/05/2017 low) and key support is given at 1.0494 (22/02/2017 low). Expected to show continued bullish pressures.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Short-term bullish

GBP/USD keeps on bouncing from hourly support given at 1.2757 (21/04/2017 low). Hourly resistance lies at 1.3046 (18/05/2017 high). Expected to show continued bullish pressures.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Bearish pressures under 110

USD/JPY is trading lower. The road seems wide open towards strong support located at 108.13 (17/04/2017 low). Hourly resistance is given at 112.13 (24/05/2017 high). Other key supports lie at a distance 106.04 (11/11/2016 low).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

Trade Idea: GBP/JPY – Stand aside

GBP/JPY - 142.40

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Sterling’s rebound from 140.75 turned out to be stronger than expected, suggesting consolidation above this level would be seen and test of resistance at 143.10 cannot be ruled out, however, break there is needed to signal low has been formed there, bring retracement of recent decline towards resistance at 143.95-00 which is likely to hold from here.

On the downside, expect pullback to be limited to 141.50-60 and price should stay above 141.00, bring another rebound later. Below 141.00 would bring retest of 140.75 but break there is needed to signal recent decline has resumed and extend weakness to 140.50, then towards psychological support at 140.00, however, oversold condition should prevent sharp fall below previous support at 139.20, risk from there has increased for a rebound later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

Can Comey, UK Election And ECB Deliver On Super Thursday?

- Comey's text indicates nothing disastrous for Trump today, markets remain cautious;

- GBP and FTSE flat ahead of exit polls this evening;

- EUR edges lower as traders await ECB views on inflation and monetary policy outlook.

All eyes in the US will be on former FBI Director James Comey's hearing in front of the Senate Intelligence Committee today, with further issues for President Donald Trump seen as being possibly problematic when it comes to delivering on his growth policies.

Based on the text of Comey's prepared testimony on Wednesday, it would seem that markets aren't expecting anything too shocking, despite there being a reference to Trump urging him to drop the investigation into former National Security Advisor Michael Flynn. Still, close attention will be paid to the public part of the hearing and should anything very controversial appear, it could impact risk appetite in the markets.

Sterling and the FTSE 100 are both trading relatively flat on the day as traders await the first exit polls this evening. The election campaign has not exactly gone as Theresa May planned or markets expected, with the monumental lead that the Conservatives had over Labour having been slashed in recent weeks, to the point that a majority is now in doubt. Still, markets appear relatively confident that a majority will still be achieved despite poll results ranging from a large majority to none at all.

We've seen previously that these polls can be unreliable – in 2015 in favour of the Conservatives - but we've also seen the populist vote prevail in recent years as well. With polls being so varied, it seems in recent days that markets have largely shrugged them off and instead assumed that May will get her majority. The problem now is that with sterling trading at near nine-month highs against the dollar, having gradually rallied since the start of the month, it is vulnerable to a sharp decline if things don't go as planned. Should we see a hung parliament then things could get messy. While this may also be bad for FTSE initially, given the general knee jerk reaction that can often follow, the weaker pound may boost it in the medium term, as it did in the days after Brexit.

The euro is looking a little soft ahead of the ECB announcement. A leaked draft staff projections yesterday suggested that while the GDP forecast is expected to be raised, inflation is forecast to be lower than previously thought into 2019. While the euro reversed its losses prior to the close on Wednesday, the softness that we're seeing this morning may suggest that traders are preparing for a more dovish forecast. The question now is whether that changes the ECBs outlook for monetary policy and if we see any change in rhetoric today. That could be as simple as a slight amendment to the statement or as bold as suggesting that further adjustments to the bond buying program could be announced before December, when the current program expires.

Elliott Wave Analysis: EURAUD Looking For A Bounce Into Wave B)

We are looking at EURAUD here which dropped in five waves from the highs so a three wave rally can be interesting for some bearish opportunities. We are tracking wave B) which may stop around 1.5050-1.5100 area.

EURAUD, 1H

Technical Outlook: US Crude Oil – Bears To Extend After Limited Correction

US oil is consolidating under fresh one-month low at $45.63 posted after sharp fall on surprise oil stocks build.

Report from Energy Information Administration released on Wednesday showed crude inventories rose by 3.3 million barrels, compared to forecasted draw of 3.5 million barrels.

Oil price was down 4.6% on Wednesday, marking the second big daily loss in two weeks and extending steep descend from $51.98 peak (25 May high).

US crude oil remains under strong pressure and was mainly unaffected by recent rising geopolitical tensions in the Middle East, with recent OPEC decision to extend production cut, giving no results, as rising fears on global oversupply continue to drive oil price lower.

Wednesday’s fall met target at $45.68 (Fibo 76.4% of $43.74/$51.98 rally) where temporary footstep was found. The price may correct higher on oversold daily studies (no firmer bullish signal being generated so far) but strong bearish sentiment suggests limited upside action before bears resume.

Broken weekly cloud top at $46.54 and broken Fibo 61.8% of $43.74/$51.98 at $46.89 mark solid barriers, which should ideally cap, with extended upticks expected to hold below broken daily Kijun-sen at $47.86.

Firm break below $45.68 handle would open way towards key support at $43.74 (05 May spike low).

Only firm break above pivots at $48.00/40 (Fibo 38.2% of $51.98/$45.63 fall / 05/06 June upside rejections) would sideline immediate bearish threats and signal stronger correction.

Res: 46.54, 46.89, 47.13, 48.00

Sup: 45.68, 45.28, 44.81, 43.74

Technical Outlook: USDJPY – Daily Tenkan-Sen/200SMA To Cap Recovery

The pair is probing above 110.00 barrier on Thursday, on the second day of recovery from fresh multi-week low at 109.11.

Strong fall on Tuesday that dented late April's gap did not manage to clearly fill it on first attempt, with subsequent bounce on oversold slow stochastic expected to precede fresh attempts lower.

Firm bearish setup of daily studies maintains pressure for further easing and eventual attack at key short-term support at 108.11 (17 Apr low). Corrective rallies are seen ideally capped by strong barriers provided by descending daily Tenkan-sen (110.41), 200SMA (110.46) and broken Fibo 61.8% of 108.11/114.36 rally at 110.50, before bears re-take control. Conversely, sustained break above that barrier would delay bears for extended recovery.

Today's testimony of former FBI Director Comey is closely watched for stronger signals.

Res: 110.41, 110.46, 110.95, 111.10

Sup: 109.92, 109.73, 109.38, 109.11

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 123.70

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the single currency fell to 122.63 yesterday, as euro has rebounded after holding above previous support at 122.56, retaining our view that further consolidation would be seen and recovery to 124.10-20 cannot be ruled out, however, break of 124.70-75 is needed to signal the retreat from 125.81 has ended, bring a stronger rebound to 125.00 but resistance at 125.31 should remain intact, bring retreat later.

On the downside, below said support at 56-63 would signal another leg of corrective decline from 125.82 top is underway for retracement of early upmove to 122.00, then towards 121.25-30 but oversold condition should limit downside and reckon latter level would remain intact, bring rebound later.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).