Sample Category Title

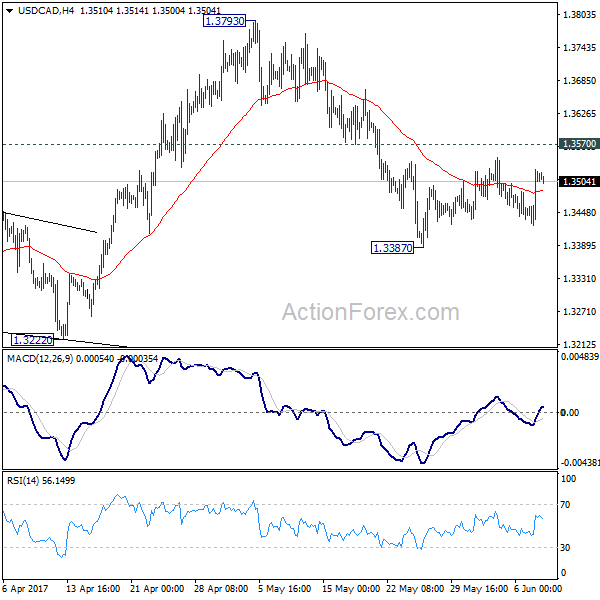

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3448; (P) 1.3486; (R1) 1.3547; More....

USD/CAD recovers but it's still bounded in tight range above 1.3387 temporary low. Intraday bias remains neutral for the moment. While consolidation from 1.3387 might extends, upside should be limited by 1.3570 resistance and bring fall resumption. We're holding on to the view that rise from 1.2968 has completed. And the larger rise from 1.2460 could have finished too. Below 1.3387 will target 1.3222 support first. Break of 1.3222 will affirm our bearish view and target 1.2968 key support level for confirmation. However, break of 1.3570 will turn focus back to 1.3793 high instead.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and could have completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Oil Prices Dropped Sharply Yesterday

Market movers today

Today brings the busiest day of the week in terms of key economic and political events. Market focus will not least be on the ECB meeting today and potential changes to its forward guidance. However, we do not expect the ECB to make any changes to avoid the risk of unwarranted tightening of financial conditions and instead just introduce a more hawkish tone in the post-meeting statement.

In the UK, all eyes will be on the general election with exit polls released at 23:00 CET. The Conservatives' lead in the polls over Labour has narrowed significantly over the past couple of weeks, increasing the risk of a hung parliament. Our main scenario remains that Theresa May wins; however, her margin of victory will be decisive in determining her vulnerability to hardline Brexiters and hence her flexibility in the upcoming Brexit negotiations.

In the US, former FBI director James Comey will testify before the Senate Intelligence Committee at 16:00 CET, where focus will be on any new revelations about his sudden dismissal on 9 May following disagreements with President Donald Trump about the FBI's Russian probe.

In Scandinavia, manufacturing production data in Norway is due to be released, which we estimate will show a solid rebound of 2.0% m/m in April, after the weak reading in March.

Selected market news

Markets are in wai t-and-see mode ahead of the ECB meeting and UK election with no significant moves overnight.

Oil prices dropped sharply yesterday following a report that showed the biggest weekly rise in US stockpiles since 2008. Brent oil prices declined more than USD1 to USD48.4 per barrel. It is the lowest level since November last year and with China showing clear signs of slowdown , risk is mainly on the downside.

Yesterday, an ECB leak suggested that the ECB staff projection at today's meeting will show a downward revision of the projection for inflation to 1.5% for 2017, 2018 and 2019. This is still clearly below the ECB's target in the medium term. The news led to a drop in German yields and lower EUR/USD. Both yields and the EUR have recovered since yesterday though.

North Korea did another missile test this morning, apparently testing short-range missiles designed to at tack ships. This was the 10th missile test by North Korea this year and another provocat ion of the US. However, we still believe that the ‘red line' for the US will be whet her North Korea carries out another nuclear test. They did the last one in September last year and have done five since 2006 with the last three under the current leader Kim Jong-un. The US administration has signalled that a nuclear test would lead to ‘actions' without being specific as to what kind.

Trade Idea : EUR/USD – Hold long entered at 1.1240

EUR/USD - 1.1256

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1258

Kijun-Sen level : 1.1244

Ichimoku cloud top : 1.1267

Ichimoku cloud bottom : 1.1259

Original strategy :

Bought at 1.1245, Target: 1.1345, Stop: 1.1210

Position : - Long at 1.1240

Target : - 1.1340

Stop : - 1.1205

New strategy :

Hold long entered at 1.1245, Target: 1.1345, Stop: 1.1210

Position : - Long at 1.1245

Target : - 1.1345

Stop : - 1.1210

As the single currency rebounded after finding renewed buying interest just above previous support at 1.1202, reviving our bullishness and above resistance at 1.1285 would confirm recent upmove has resumed and extend further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 but overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1240. Only below support at 1.1202 would abort and suggest top is possibly formed, break of 1.1195-97 (50% Fibonacci retracement of 1.1109-1.1285) would add credence to this view, bring retracement of recent rise to indicated support at 1.1164 first.

Currencies: ECB And Comey Hearing To Decide On Nest USD Move?

Sunrise Market Commentary

- Rates: Downward potential Bunds on ECB meeting?

Bunds gained significant ground in the run-up to today's ECB meeting, suggesting that the market reaction could be asymmetric with lower Bunds (higher rates) both in case of a hawkish 'surprise' (our scenario; change forward guidance and risk assessment eco outlook) and in case of a more neutral ECB (via buy-the-rumour, sell-the-fact). - Currencies: ECB and Comey hearing to decide on nest USD move?

Today, the ECB may be slightly more hawkish in its policy assessment, but it likely won't be enough to trigger sustained EUR/USD gains beyond the 1.1300/66 resistance. The outcome of the UK elections won't be available today, but market anticipation on a May victory might be slightly supportive for sterling

The Sunrise Headlines

- US equities recovered from a mid-session dip and eventually closed with small gains. Overnight, most Asian stock markets show similar gains. Local eco data didn't impact trading.

- President Trump asked Comey for 'loyalty' over the 'Russia thing'. Comey said Trump had also urged him to drop any investigation related to former national security adviser Flynn having lied about talks with the Russian ambassador.

- China reported stronger-than-anticipated exports and imports for May despite falling commodity prices, suggesting the economy is holding up better than expected despite rising lending rates and a cooling property market.

- Oil prices were hit hard yesterday after data showed an unexpected rise in US petroleum stocks and a sharp turn lower for petrol and diesel use. Brent crude fell from $50/barrel to around $48/barrel, testing important support.

- Japan's economy grew at slower pace than initially estimated in Q1 (0.3% Q/Q), as an inventory rundown and weaker household spending took some of the shine off Japan's longest economic expansion since 2006.

- Turkey threw its weight behind its ally Qatar, fast-tracking plans to deploy extra Turkish troops to the emirate as Arab rivals cut transport links and supply lines.

- Today's eco calendar is mainly filled with events: the ECB meeting, UK elections and the Comey hearing. Eco data include US weekly jobless claims and final EMU GDP data. Ireland taps the bond market

Currencies: ECB And Comey Hearing To Decide On Nest USD Move?

ECB and Comey to decide on next USD move?

Yesterday, the dollar first traded in the defensive as investors pondered the impact of today's key events, including the Comey testimony, the ECB policy statement and the UK elections. Risk sentiment improved later on and avoided more USD losses. Later in the session, rumours on a softer ECB inflation forecast triggered a modest setback of the euro. EUR/USD finished the session at 1.1257. USD/JPY closed at 109.82, supported by a good close on US equity markets.

Overnight, Asian equities are trading with modest gains. Eco data are mixed. Japan Q1 GDP was revised sharply lower confirming that the BOJ will continue its accommodating policy. The impact on the yen is neglible. USD/JPY tested the 110 barrier this morning, but returned to 109.50 area as the equity momentum eases. The China May trade surplus narrowed. Exports (15.5% Y/Y) and even more imports (14.8% Y/Y vs 8.3% Y/Y ) were higher than expected. The import data suggest ongoing good growth in Q2. This is often a positive for the Aussie dollar, but not today. AUD/USD stabilizes in the 0.7550 area after this week's rebound. EUR/USD also trades little changed in the 1.1250 area.

Today, the focus will be the ECB press conference and the Comey hearing. The first indications of the outcome of the UK election will only come after the market closure. For an in depth analysis of the ECB see the fixed income part of this report. Interest rate markets are positioned for limited/no change in the ECB's guidance. So, any indication of a step direction exit non-conventional policy might push EMU yields higher. At the same time, the euro had a good run of late (reduced political risk & USD softness). So, the positioning in the FX market might be different from that in the interest rate markets. In our working hypothesis, the ECB will move to balanced eco risks. The forward guidance might be slightly less easy. The ‘big work' might be postponed to September. Nuances will decide on the EUR/USD reaction, but we tend to believe that the ECB has to be quite hawkish to inspire a next EUR/USD up-leg. The Comey testimony is a wildcard, but we assume that it won't bring really big trouble for Trump. Such a scenario might be modestly USD supportive . Several other combinations of events are possible, but for now we assume that it will be difficult for EUR/USD to move sustainably above 1.1300/66.

Technical picture

The USD/JPY rally ran into resistance in early May. A mini sell-off pushed the pair below the previous top (112.20), making the short-term picture negative. The post-payrolls USD and the break below 110 made the picture further negative. Return action lower in the 108.13/114.37 range remains possible.

Earlier in May, EUR/USD failed to break below the 1.0821/1.0778 support (gap). Poor US data and US political upheaval propelled EUR/USD north of the 1.1023 range top. The pair initially reached a short-term correction top at 1.1268. There was a minor break after Friday's disappointing US payrolls, but for now there are no sustained follow-through gains. The Trump top/correction top at 1.1300/1.1366 is next resistance. USD sentiment will have to be quite negative to clear this hurdle short-term. A return below 1.1023 would indicate that the upside momentum has eased.

EUR/USD near key resistance ahead of key events

EUR/GBP

Sterling regains slightly ground ahead of the election

Sterling was in consolidation modus yesterday. Trading in the major sterling cross rates was confined to relatively tight ranges given the magnitude of the upcoming event risk. Cable held a tight range around, but mostly slightly north of 1.29 suggesting a tentative sterling positive momentum. The same applies to EUR/GBP. The pair dropped below the 0.87 mark. This was primarily a euro correction on the ECB's inflation rumours, but in a second degree also because of a better bid for sterling. EUR/GBP closed the session at 0.8687. Cable finished the day at 1.2960.

Today, sterling traders will look out for the outcome of the Parliamentary elections. The first indications on the outcome will only be available after the close of the markets. If markets, for one reason or another, would anticipate for a scenario of May reaching a (slightly ) bigger majority, it should be slightly supportive for sterling. In this context, a break of EUR/GBP beyond the recent top might become difficult. First resistance comes in the 0.8774/88 area. EUR/GBP 0.8655 is a first minor support. A sustained return below the EUR/GBP 0.86 would suggest that the worst is over for sterling.

EUR/GBP: most of the bad news for sterling discounted?

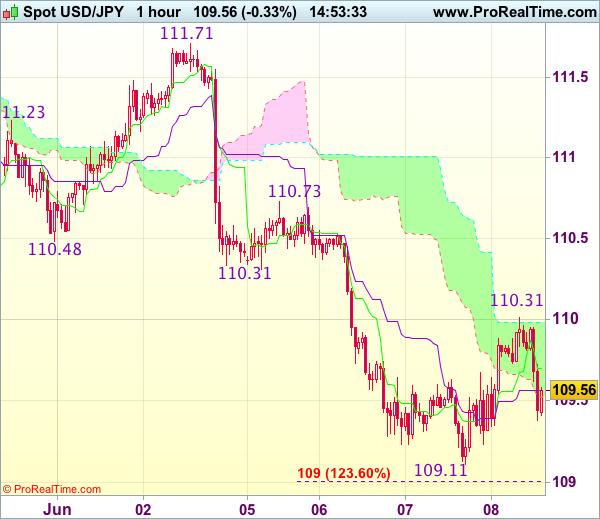

Trade Idea : USD/JPY – Sell at 110.20

USD/JPY - 109.59

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 109.70

Kijun-Sen level : 109.98

Ichimoku cloud top : 109.56

Ichimoku cloud bottom : 109.52

Original strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

Although the greenback retreated after meeting resistance at 110.01, break of yesterday’s low at 109.11 is needed to signal recent decline from 114.37 has resumed and extend weakness to 109.00-05 (1.236 times projection of 111.71-110.31 measuring from 110.73), then towards 108.70-75 but near term oversold condition should limit downside to 108.45-50 (1.618 times projection), bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as previous support at 110.24 (now resistance) should limit upside and bring another decline. Above previous support at 110.31 would defer and suggest low is formed instead, bring a stronger rebound to 110.60 but break of resistance at 110.73 is needed to add credence to this view.

UK Vote The Biggest In Decades

- UK heads to the polls in the most important election in decades;

- Will ECB lay foundations for tapering, lower inflation forecasts, or both?

- Former FBI Director Comey testifies on President Trump.

Thursday promises to be a massive day for financial markets with major risk events taking place in the UK, eurozone and US that could create substantial volatility throughout the day.

The UK will head to the polls in what will be the most important vote in decades to decide who will lead the country into the Brexit negotiations and what direction it will take in the years to come. It’s been a long time since there’s been such a substantial difference between the choices on offer, which makes the result today all the more important.

From a markets perspective, this election is huge and could produce some substantial moves, particularly in sterling, the FTSE and UK debt. As we’ve learned from similar events previously – Brexit, US election - not only is the outcome not always obvious but the market reaction can also catch people off guard and that’s what’s had traders acting with such caution all week.

The most undesirable outcome is surely a hung parliament that produces both domestic political uncertainty and, more importantly, uncertainty and delays in Brexit negotiations. With the currently deadline being March 2019, any delay will be detrimental to the UK in negotiations and could therefore be devastating for sterling. While the knee jerk reaction to this may also be bad for the FTSE, as we saw after the EU referendum, we could see this bounce back quite quickly with the weaker currency benefiting its mostly outward facing companies.

Another major risk event today is the ECB meeting, which after reports yesterday of leaked draft ECB staff projections could be very interesting indeed. The leaked draft indicated that the central bank is revising higher its GDP forecasts but lowering its inflation forecasts through 2019. The euro fell quite heavily after the leak on the belief that such a change could alter the pace or timing of future tapering. It’s currently assumed that further reductions in asset purchases will be planned again at the end of the year, with possibly today’s and September’s meeting being used to lay the groundwork.

Finally today, former FBI Director James Comey will testify before the Senate Intelligence Committee regarding a number of events involving President Donald Trump including the links between his campaign and Russia, as well as allegations that he requested at the time that an investigation into his National Security Advisor – Michael Flynn – be dropped. Traders will be following the public part of the hearing with great interest and should there be any “bombshells”, it could ruffle the markets.

Australia’s Trade Surplus Shrunk To A 6-Month Low Level In April

For the 24 hours to 23:00 GMT, the AUD rose 0.43% against the USD and closed at 0.7546. LME Copper prices rose 0.6% or $35.0/MT to $5575.5/MT. Aluminium prices rose 0.6% or $10.5/MT to $1903.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7540, with the AUD trading 0.08% lower against the USD from yesterday's close.

Earlier today, data showed that Australia's seasonally adjusted trade surplus narrowed more-than-expected to a level of A$555.0 million in April, hitting its lowest level in six months and compared to a revised trade surplus of A$3169.0 million in the previous month. Market anticipation was for the nation to record a trade surplus of A$2000.0 million.

Elsewhere, in China, Australia's largest trading partner, trade surplus expanded less-than-expected to a level of CNY281.6 billion in May, compared to a surplus of CNY262.3 billion recorded in the preceding month. Additionally, the nation's exports grew 15.5% in May, from a gain of 14.3% the previous month.

Moreover, the nation's imports expanded 22.1% in May, compared with an 18.6% rise in the prior month.

Meanwhile, the OECD marginally nudged up its growth estimates for China to 6.6% this year and 6.4% for 2018.

The pair is expected to find support at 0.7521, and a fall through could take it to the next support level of 0.7503. The pair is expected to find its first resistance at 0.7562, and a rise through could take it to the next resistance level of 0.7585.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

OECD Revised Up Euro-Zone’s Growth Forecast, Calls For Tapering ECB’s Stimulus Programme

For the 24 hours to 23:00 GMT, the EUR declined 0.17% against the USD and closed at 1.1258, following a report that the European Central Bank (ECB) will likely cut its inflation forecast at its monetary policy meeting scheduled later today.

In economic news, data indicated that Germany's seasonally adjusted factory orders eased more-than-expected by 2.1% on a monthly basis in April, after advancing for two consecutive months, while markets expected for a fall of 0.3%. In the previous month, factory orders had recorded a revised rise of 1.1%.

Meanwhile, the Organisation for Economic Co-operation and Development (OECD), in its latest economic outlook report, lifted the Euro-zone's growth forecast to 1.8% for this and next year, up from 1.6% for both years, boosted by strong growth in Germany. Additionally, the OECD called for winding down the European Central Bank (ECB) massive bond purchases in 2018 and raise one of its key interest rates by the end of 2018.

Separately, it revised up its 2017 global growth forecast by 0.2% and estimated that the global economy will likely expand by 3.5% in 2017, its fastest pace of growth in 6 years, before accelerating by 3.6% in 2018, as a rebound in global trade trounces fears of a weaker economic outlook in the US. On the contrary, growth forecast for the US was downgraded to 2.1% this year and 2.4% next year, down from its earlier prediction of 2.4% and 2.8%, respectively, due to delays by the Trump administration to push through with its planned tax cuts and infrastructure spending.

Macroeconomic data revealed that mortgage applications in the US rebounded 7.1% in the week ended 02 June 2017, following a drop of 3.4% in the previous week.

In the Asian session, at GMT0300, the pair is trading at 1.1259, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.1215, and a fall through could take it to the next support level of 1.1170. The pair is expected to find its first resistance at 1.1293, and a rise through could take it to the next resistance level of 1.1326.

Going ahead, all eyes would be on the European Central Bank's (ECB) interest rate decision, wherein markets would be keen to know whether the ECB would announce tapering of its massive stimulus programme. Additionally, the Eurozone's 1Q GDP and Germany's industrial production data for April, slated to release in a few hours, will be on investors' radar. Meanwhile, the US initial jobless claims data will also be eyed by traders.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Pound Trading Flat, Ahead Of British General Election Results

For the 24 hours to 23:00 GMT, the GBP rose 0.37% against the USD and closed at 1.2956, as investors bet that Theresa May’s Conservatives will win the UK’s general election.

In economic news, Britain’s Halifax house price index unexpectedly rebounded 0.4% on a monthly basis in May, defying market expectations for a drop of 0.2%. In the previous month, the Halifax house price index had fallen 0.1%.

Meanwhile, the OECD retained its growth forecast for UK, expecting an expansion of 1.6% this year and 1.0% in the next year.

In the Asian session, at GMT0300, the pair is trading at 1.2956, with the GBP trading flat against the USD from yesterday’s close.

The pair is expected to find support at 1.2907, and a fall through could take it to the next support level of 1.2857. The pair is expected to find its first resistance at 1.2987, and a rise through could take it to the next resistance level of 1.3017.

Trading trend in the Pound is expected to be determined by the outcome of UK’s general election.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Economy Expanded At A Slower Pace Than Initially Estimated In 1Q 2017

For the 24 hours to 23:00 GMT, the USD rose 0.31% against the JPY and closed at 109.76.

In the Asian session, at GMT0300, the pair is trading at 109.84, with the USD trading 0.07% higher against the JPY from yesterday's close.

The Japanese Yen lost ground, after data showed Japan's economy expanded at a slower pace than initially estimated in the first three months of 2017.

Overnight data indicated that Japan's final gross domestic product (GDP) rose by 0.3% QoQ in 1Q 2017, less than market expectations for a rise of 0.6%. The preliminary figures had indicated a rise of 0.5%. In the previous quarter, GDP had registered a similar rise. Also, the nation's (BOP basis) trade surplus narrowed less-than-expected to a level of ¥553.6 billion in April, compared to market expectations of a (BOP basis) trade surplus of ¥494.0 billion. In the prior month, the nation had reported a surplus of ¥865.5 billion in the prior month.

Meanwhile, the OPEC estimated Japan's economy to expand 1.4% in 2017, up from a 1.2% increase projected in March, and 1.0% in 2018, up from 0.8%.

The pair is expected to find support at 109.3, and a fall through could take it to the next support level of 108.77. The pair is expected to find its first resistance at 110.19, and a rise through could take it to the next resistance level of 110.55.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.