Sample Category Title

GBP/USD Analysis: To Trade Flat For Another Day

The Cable experienced minor volatility on Tuesday, with the exchange rate mostly gravitating towards the monthly pivot point. Flat trade could indicate that the Pound’s bullish momentum is nearing its end, even though technical studies suggest the opposite. In either case, the Sterling is likely to consolidate for another day, with trade anchored around the 1.29 major level and the three-month up-trend remaining a strong support, which is to limit any losses should those occur today. Gains, however, are unlikely to exceed the 1.2940 handle, as the British currency struggled to climb over this area through all of the previous week. Meanwhile, traders retain a neutral outlook towards the GBP/USD pair, as 52% of all open positions are long.

Trade Idea: GBP/JPY – Sell at 142.00

GBP/JPY - 141.10

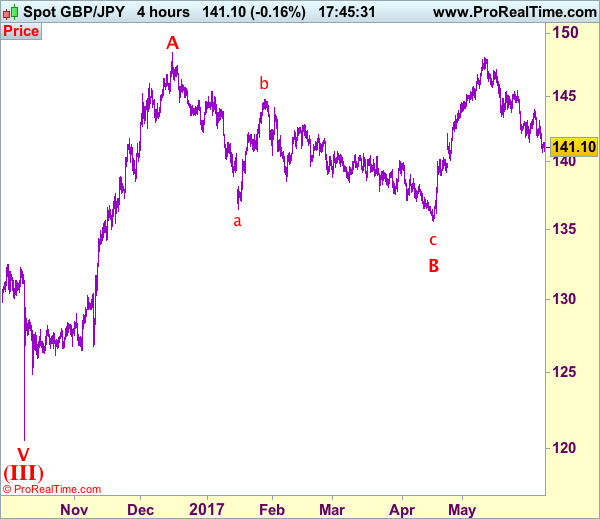

Recent wave: Medium term low formed at 120.50 and (A)-(B)-(C) major correction has commenced with (A) leg ended at 148.45, hence wave (B) is unfolding for retreat to 131.00-10.

Trend: Near term up

Original strategy:

Sold at 143.65, met target at 141.65

Position: - Short at 143.65

Target: - 141.65

Stop: -

New strategy :

Sell at 142.00, Target: 140.00, Stop: 142.60

Position: -

Target: -

Stop:-

As sterling has remained under pressure after recent anticipated selloff, suggesting recent selloff from 148.10 top is still in progress and bearishness remains for this move to extend weakness to 140.50-55, then towards psychological support at 140.00, however, near term oversold condition should prevent sharp fall below previous support at 139.20, risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell sterling again on recovery as 142.00-10 should limit upside and bring another decline later. Above 142.55-60 would suggest low is possibly formed, risk a stronger rebound towards resistance at 143.10 but a sustained breach above there is needed to confirm, bring a stronger rebound towards resistance at 143.95-00.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 140.39; (P) 141.51; (R1) 142.32; More....

Intraday bias in GBP/JPY remains on the downside for 61.8% retracement of 135.58 to 148.09 at 140.35. At this point, we'd continue to look for bottoming around there and bring rebound. Break of 143.93 will indicate near term reversal and turn bias back to the upside. However, sustained break of 140.35 will bring deeper fall to 135.58 key support level.

In the bigger picture, rise from 122.36 medium term bottom is still expected to extend to of 195.86 to 122.36 at 150.42. And decisive break there could pave the way to 61.8% retracement at 167.78. However, as the cross is starting to lose upside momentum, rejection below 150.42 and break of 135.58 support will indicate reversal and bring deeper fall back to retest 122.36 instead.

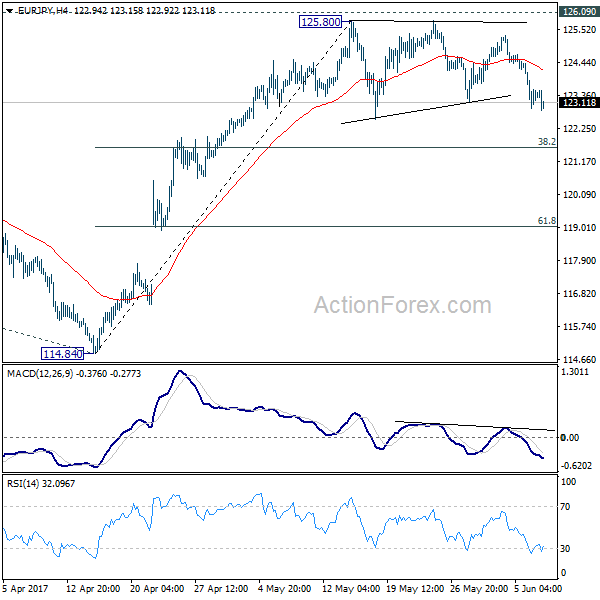

EUR/JPY Daily Outlook

Daily Pivots: (S1) 122.73; (P) 123.56; (R1) 124.19; More...

No change in EUR/JPY's outlook as consolidation from 125.80 is still in progress. Deeper fall could be seen but downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89. Nonetheless, firm break of 121.61 will dampen our bullish view and bring deeper fall to 61.8% retracement at 119.02.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

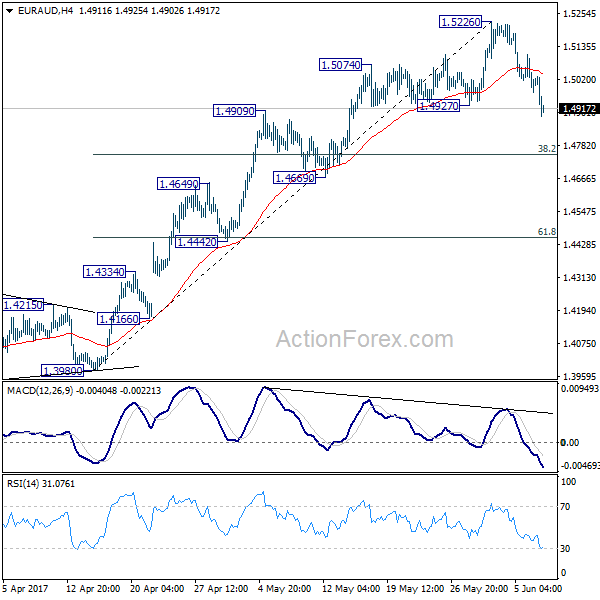

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4961; (P) 1.5034; (R1) 1.5095; More...

The break of 1.4927 support in EUR/AUD indicates short term topping at 1.5226, on bearish divergence condition in 4 hour MACD. Intraday bias is turned to the downside for deeper pull back to 38.2% retracement of 1.3980 to 1.5226 at 1.4750. At this point, we'd expect strong support from 1.4669 to contain downside and bring rebound. Larger rise from 1.3642 is expected to resume later after the pull back completes.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455. Sustained break there will pave the way to retest 1.6587. In any case, outlook will now stay cautiously bullish as long as 1.4669 support holds.

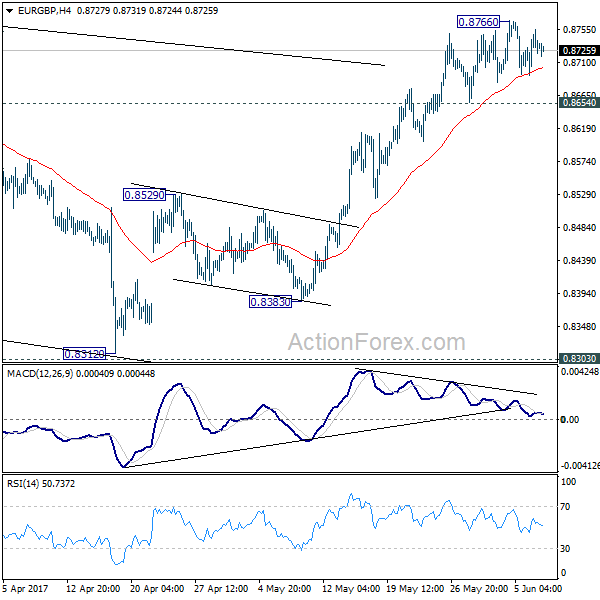

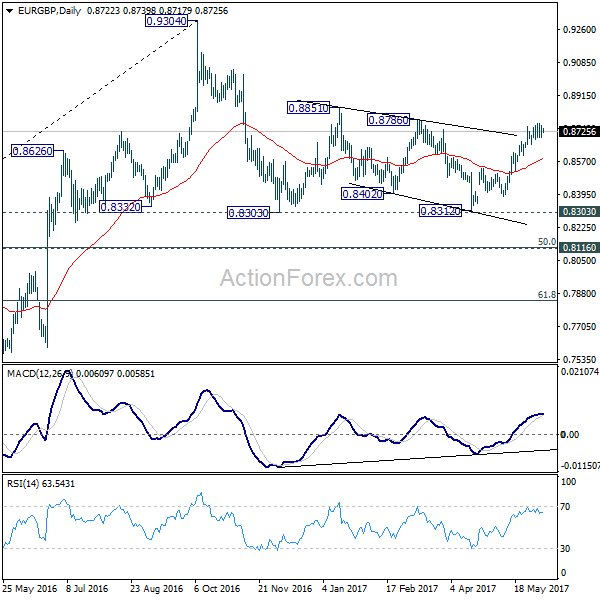

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8700; (P) 0.8727; (R1) 0.8763; More...

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8766 temporary top. Further rally is still expected as long as 0.8654 support holds. Above 0.8766 will target 0.8786 resistance and then 0.8851. Decisive break of 0.8851 will pave the way to retest 0.9304 high. However, break of 0.8654 will indicate short term topping on bearish divergence condition in 4 hour MACD. In such case, intraday bias will be turned back to the downside for 55 day EMA (now at 0.8585).

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. The leg from 0.9304 should have completed after testing 0.8332 structural support. But it's too early to say that larger rise from 0.6935 is resuming. Rejection from 0.9304 will extend the consolidation with another falling leg. Meanwhile, firm break of 0.9304 will target 0.9799 (2008 high). In case of another decline, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0850; (R1) 1.0860; More...

No change in EUR/CHF's outlook. Corrective fall from 1.0986 might extend. But downside downside should be contained by 1.0791/0872 support zone, probably around 55 day EMA (now at 1.0829). Rise from 1.0629 is expected to resume later. Above 1.0902 minor resistance will turn bias back to the upside for 1.0986/0999.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

GBPUSD in Consolidation Around 1.29; Uptrend from March Intact

GBPUSD remains neutral in the near-term while maintaining a medium-term bullish market structure.

The pair has been pivoting around the key 1.2900 level while trading in a range since mid-April between 1.2755 and 1.3045. The market is waiting for a catalyst for the next sustained directional move.

Upside momentum could challenge the May 18 high of 1.3046. A break above this resistance level would trigger a move towards 1.3450, close to the top of a previous range (from July to September 2016).

Support lies at the bottom end of the current range near 1.2755. A deeper decline would target 1.2574 – which is the 50% Fibonacci level of the upleg from 1.2108 to 1.3046.

The broader technical picture looks bullish and the market has only retraced 23.6% of the rise from 1.2108 to 1.3046, keeping the uptrend still intact. There was a bullish crossover of the 50-day moving average with the 200-day MA. This suggests there will be relatively limited downside risk for GBPUSD in the near-term, although a flat RSI indicates that the consolidation phase will likely continue for now.

A drop below the 200-day MA and the 50% Fibonacci would negate the bullish structure from March.

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 123.04

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

Original strategy:

Bought at 123.75, stopped at 123.15

Position: - Long at 123.75

Target: -

Stop: - 123.15

New strategy :

Stand aside

Position: -

Target: -

Stop:-

As the single currency has fallen again after brief recovery and indicated previous support at 123.16 was penetrated, suggesting further consolidation below recent high of 125.82 top would be seen and test of another previous support at 122.56 cannot be ruled out, however, break there is needed to retain near term bearishness for the erratic fall from 125.82 to bring retracement of early upmove to 122.00, then towards 121.25-30 with is likely to hold from here.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 123.55-60 would bring recovery to 124.00, however, only break of 124.70-75 would suggest the retreat from 125.31 has ended, bring a stronger rebound to 125.00 and possibly towards 125.31. Looking ahead, above 125.31 would extend gain towards strong resistance at 125.82 but break there is needed to confirm recent upmove has resumed and extend headway to 126.20-30 and possibly 126.60-70.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Aussie Jumps on GDP; Gold at 1-Month High ahead of Risk Events

The Australian dollar rallied on upbeat GDP data while the greenback steadied after sharp declines this week. Upcoming key risk events tomorrow dampened risk appetite in the markets as investors were cautious ahead of the UK elections, the European Central Bank meeting, and the testimony to a Senate committee by former FBI Director James Comey. This helped support gold near seven-month highs.

The aussie was one of the best performing major currencies against the US dollar in the Asian session as it rose to a one-month high of $0.7543 from $0.7500. Markets were expecting a weaker GDP number but data showed the Australian economy grew 0.3% over the first quarter versus 0.2% anticipated and 1.7% in the year to March compared to a 1.5% rise that was forecast.

Sterling remained resilient ahead of the UK general election tomorrow and traded in a tight range against the dollar, close to the key $1.2900 level.

The euro has been moving sideways all week just below $1.1285. Focus is shifting to the ECB policy meeting tomorrow and expectations are for the central bank to have a more hawkish tone with regards to the Eurozone economy and may even hint that it is exiting from its quantitative easing program soon.

The dollar stabilized against the yen after a big sell-off yesterday and hovered near six-week lows of 109.20 yen. The greenback is being weighed by uncertainty around Thursday's testimony at a Senate Intelligence Committee hearing by James Comey, the former FBI Director who was fired by President Donald Trump. He is expected to testify whether Trump asked him to drop the FBI investigation into former national security adviser Michael Flynn.

Gold gained 1% yesterday to reach its highest level since early November at $1295.97 an ounce. Prices steadied in Asian trading today but the safe haven asset remains supported due to risk aversion and a broadly weaker dollar.

WTI oil prices rebounded to test the $48 a barrel level but gains were capped as the commodity is being put under pressure by tensions in the Middle East amongst oil producers due to a diplomatic rift with Qatar.