Sample Category Title

EUR/JPY Targeting Weekly L5 Camarilla

The EUR/JPY has been dropping towards Weekly camarilla pivots and at this point the price action suggests that it may drop further targeting Weekly L5 at 122.40. Now moment sellers may appear in the POC zone (50.0, ATR pivot, D L5, trend line, bearish order block) 123.60-80. If we don't see any retracement a clear break or 4h close below 122.94 should target W L5 – 122.40. The price is currently below all Daily camarilla pivots and below W L4 that indicates a strong bearish pressure.

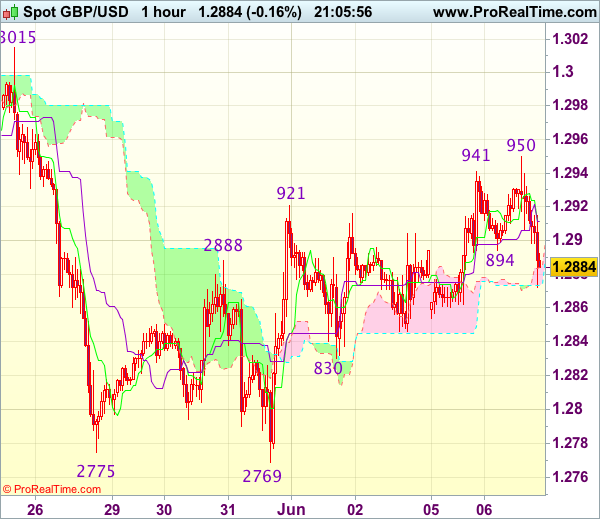

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.2894

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As sterling has retreated after intra-day brief rise to 1.2950, suggesting consolidation below this level would be seen and pullback to 1.2865-70 cannot be ruled out, however, break of indicated support at 1.2830 is needed to confirm top has been formed and suggest the rebound from 1.2769 has ended, bring further fall to 1.2800.

On the upside, expect recovery to be limited to 1.2925-30 and said resistance at 1.2950 should remain intact, bring another retreat later. Only break there would extend the erratic rise from 1.2769 to 1.2970, however, as broad outlook remains consolidative, reckon upside would be limited to 1.3000 and indicated previous resistance at 1.3015 should remain intact. As near term outlook is still mixed, would be prudent to stand aside for now.

Trade Idea Update: EUR/USD – Hold long entered at 1.1205

EUR/USD - 1.1263

Original strategy :

Bought at 1.1205, Target: 1.1305, Stop: 1.1235

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1235

New strategy :

Hold long entered at 1.1205, Target: 1.1305, Stop: 1.1235

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1235

As the single currency has retreated again after faltering below resistance at 1.1285 in part due to cross-selling against yen, suggesting further consolidation below this level would be seen, however, as long as 1.1235-40 holds, mild upside bias remains for recent upmove to resume after consolidation, above said resistance at 1.1285 would extend rise to another previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 but overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1205. Only below support at 1.1202 would abort and signal top is formed instead, risk weakness towards indicated support at 1.1164, once this level is penetrated, this would signal recent upmove has ended, bring further fall to 1.1130-40 first.

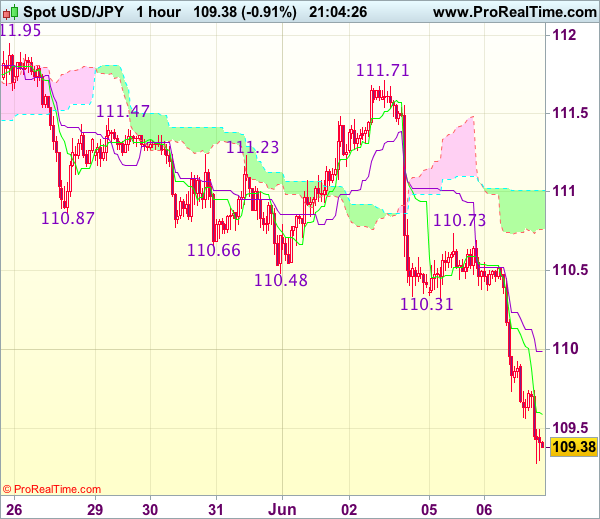

Trade Idea : USD/JPY – Sell at 110.00

USD/JPY - 109.36

Original strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.00, Target: 109.00, Stop: 110.35

Position : -

Target : -

Stop : -

As the greenback met renewed selling interest at 110.73 yesterday and decline has accelerated after breaking below indicated support at 110.24, confirming our bearish view that recent decline from 114.37 top is still in progress and bearishness remains for further weakness to 109.00-05 (1.236 times projection of 111.71-110.31 measuring from 110.73), then towards 108.70-75 but near term oversold condition should limit downside to 108.45-50 (1.618 times projection), bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as previous support at 110.24 should turn into resistance and cap dollar’s upside, bring another decline. Above 110.31 (another previous support) would defer but only break of said resistance at 110.73 would signal low is formed instead.

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.89; (P) 142.49; (R1) 143.13; More....

GBP/JPY's fall from 148.09 resumes today by taking out 141.43 and reaches as low as 140.19 so far. Intraday bias is back on the downside for 61.8% retracement of 135.58 to 148.09 at 140.35. We'll look for bottoming around there. Break of 143.93 will indicate near term reversal and turn bias back to the upside. However, sustained break of 140.35 will bring deeper fall to 135.58 key support level.

In the bigger picture, rise from 122.36 medium term bottom is still expected to extend to of 195.86 to 122.36 at 150.42. And decisive break there could pave the way to 61.8% retracement at 167.78. However, as the cross is starting to lose upside momentum, rejection below 150.42 and break of 135.58 support will indicate reversal and bring deeper fall back to retest 122.36 instead.

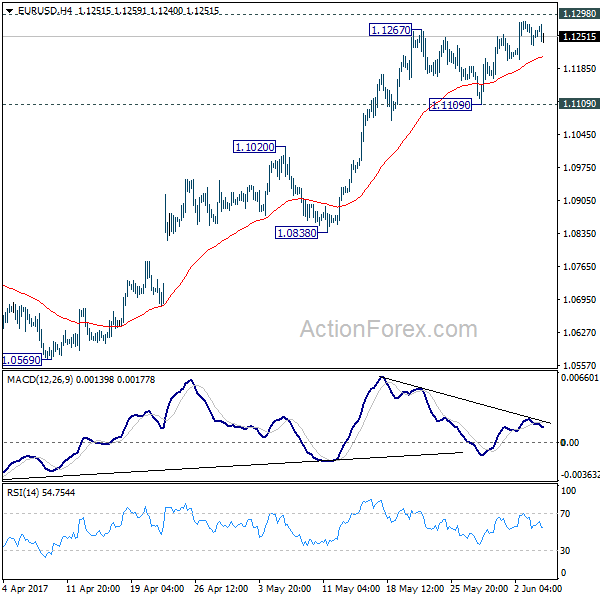

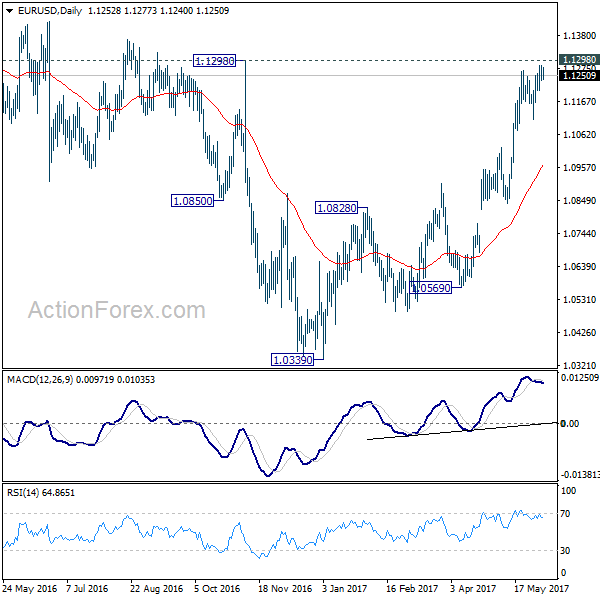

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1231; (P) 1.1256 (R1) 1.1279; More....

With 1.1109 support intact, further rise is still expected in EUR/USD. Decisive break of 1.1298 key resistance will carry larger bullish implication and target 1.1615 resistance next. Nonetheless, we'd stay cautious on rejection from 1.1298. Break of 1.1109 will indicate short term topping and turn bias back to the downside.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

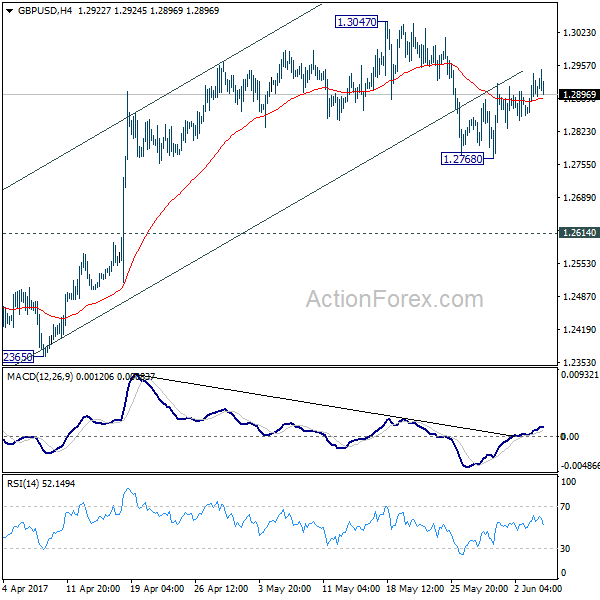

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2856; (P) 1.2898; (R1) 1.2945; More...

Intraday bias in mildly on the upside for 1.3047 resistance. Break there will extend the corrective pattern from 1.1946 for 1.3444 key resistance. On the downside, below 1.2768 will turn bias back to the downside for 1.2614 resistance turned support. Break there will likely resume the larger down trend through 1.1946 low.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

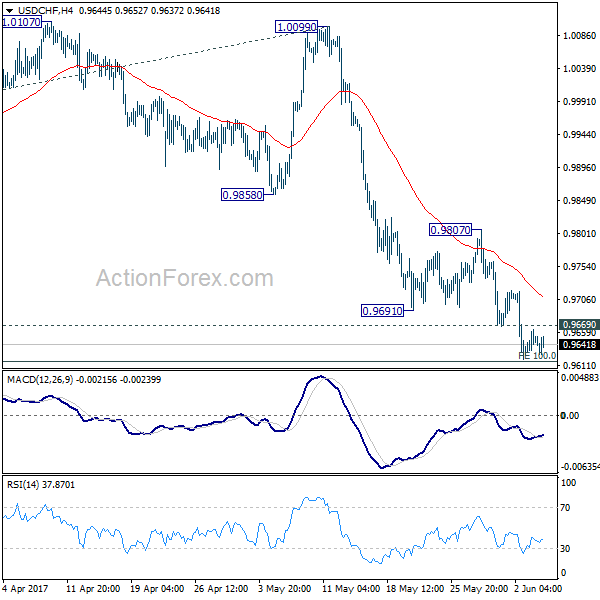

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9627; (P) 0.9645; (R1) 0.9670; More.....

No change in USD/CHF's outlook. Intraday bias remains on the downside and current fall would likely pass through 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. But we'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, above 0.9669 minor resistance will turn intraday bias neutral first. But near term outlook will stay bearish as long as 0.9807 resistance holds.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.27; (P) 110.50; (R1) 110.69; More...

USD/JPY's decline accelerates to as low as 109.27 and intraday bias remains on the downside. Fall from 114.36 is expected to extend to retest 108.12 low first. Also whole decline from 118.65 is seen as a correction and is still in progress. Break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. We'll look for bottoming signal around 106.48. On the upside, above 110.23 support turned resistance will turn bias neutral first. But near term outlook will remain bearish as long as 111.70 resistance holds.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Yen Rally Extends, Eurozone Sentix Confidence Hits Decade High

Yen jumps sharply this week and is extending it's broad based rally today. There are a couple reasons noted in the markets for the move. The sudden escalation in tension in Middle East, between Qatar and other nations, is seen a a factor. The uncertainties over election in UK is another one. However, we'd believe Yen's strength is more concerned with the outcome of former FBI director James Comey and the impact on US President Donald Trump. And investors are getting increasingly impatient on the lack of progress in Trump's tax reform and economic policies. This is clearly seen in the sharp fall in US bond yields and persistent weakness in Dollar.

Eurozone Sentix hits near decade high

Euro remains firm against the greenback in spite of mild retreat. Eurozone Sentix investor confidence rose to 28.4 in June, up from 27.4 and beat expectation of 27.4. That's the highest level in nearly a decade, since July 2007. The current situation index rose to 36.0, up from 34.5. Sentix noted that "the assessment of the current situation climbs to the highest level since January 2008, underlining that it is not just ephemeral expectations, but increasingly hard data, that are driving the upswing in the Eurozone.". Also from Eurozone, retail sales rose 0.1% mom in April, in line with consensus.

Sterling lacks momentum ahead of election

Sterling is mildly firmer against Dollar and Euro this week but lacks decisive momentum. Ahead of UK election on Thursday, renowned physicist Stephen Hawking declared his support for the Labour. He warned that "another five years of Conservative government would be a disaster for the NHS, the police and other public services." Nonetheless, Hawking also criticized Labour leader Jeremy Corbyn as a "disaster" and noted last week that "his heart is in the right place and many of his policies are sound, but he has allowed himself to be portrayed as a left wing extremist."

RBA stands pat as widely expected

As widely anticipated, RBA left the cash rate unchanged at 1.5% today. Policymakers indicated that, "transition to lower levels of mining investment following the mining investment boom is almost complete". Meanwhile, "business conditions have improved and capacity utilization has increased. Business investment has picked up in those parts of the country not directly affected by the decline in mining investment".

While acknowledging growth moderation in the first quarter, the central bank maintained the view that GDP growth would "increase gradually over the next couple of years to a little above 3%". On the job market, policymakers acknowledged the payroll growth but remained concerned over the subdued growth in total hours worked as well as wage growth remains. Policymakers warned that persistently low growth in wage would restrain household consumption.

Gulf rift may benefit Australia

Meanwhile, geopolitical uncertainty in Middle East is seen as a reason support Aussie this week. A boycott over Qatar is expected to disrupt the country's exports, benefitting its rival, Australia, over LNG exports. Natural gas is Australia's third largest exports in value terms, after iron ore and concentrates, and coal. It takes up 5.4% of the country's total exports in 2014. Qatar is the largest exporter of LNG, producing around one-third of the LNG traded. Current development would disruption Qatar's exports, benefiting Australia.

More in Arab Gulf's Banning over Qatar Might Help Australia's LNG Exports

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.27; (P) 110.50; (R1) 110.69; More...

USD/JPY's decline accelerates to as low as 109.27 and intraday bias remains on the downside. Fall from 114.36 is expected to extend to retest 108.12 low first. Also whole decline from 118.65 is seen as a correction and is still in progress. Break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. We'll look for bottoming signal around 106.48. On the upside, above 110.23 support turned resistance will turn bias neutral first. But near term outlook will remain bearish as long as 111.70 resistance holds.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y May | -0.40% | -0.50% | 5.60% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Apr | 0.50% | 0.30% | -0.40% | 0.00% |

| 1:30 | AUD | Current Account Balance (AUD) Q1 | -3.1B | -0.5B | -3.9B | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jun | 28.40% | 27.4 | 27.4 | |

| 9:00 | EUR | Eurozone Retail Sales M/M Apr | 0.10% | 0.10% | 0.30% | |

| 14:00 | CAD | Ivey PMI May | 62 | 62.4 |