Sample Category Title

Swiss Franc Trading On A Weaker Footing This Morning

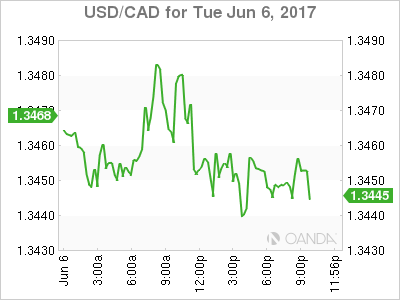

For the 24 hours to 23:00 GMT, the USD declined 0.22% against the CAD and closed at 1.3448.

On the macro front, Canada's seasonally adjusted Ivey PMI registered a drop to a level of 53.8 in May, compared to a level of 62.4 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3450, with the USD trading marginally higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3429, and a fall through could take it to the next support level of 1.3408. The pair is expected to find its first resistance at 1.3479, and a rise through could take it to the next resistance level of 1.3508.

Ahead in the day, traders would focus on Canada's building permits data for April.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Loonie Trading A Tad Lower, Ahead Of Canada’s Building Permits Data

For the 24 hours to 23:00 GMT, the USD declined 0.22% against the CAD and closed at 1.3448.

On the macro front, Canada's seasonally adjusted Ivey PMI registered a drop to a level of 53.8 in May, compared to a level of 62.4 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.3450, with the USD trading marginally higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3429, and a fall through could take it to the next support level of 1.3408. The pair is expected to find its first resistance at 1.3479, and a rise through could take it to the next resistance level of 1.3508.

Ahead in the day, traders would focus on Canada's building permits data for April.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Is The Loonie Set To Recover Once Again?

Key Points:

- The long-term trend line is likely to encourage a reversal.

- Numerous technical reading suggestive of a near-term rally.

- Fundamental outlook is also rather bullish.

The Loonie is poised to have yet another bump in buying pressure as the week closes which could see it back up at around the 1.3554 handle within a week or so. Indeed, the recent decline is already beginning show signs of slowing which is due, in part, to the weaker Canadian economic news. However, the technical bias is also signalling that a change in momentum is now warranted which could really set a fire under the pair.

Specifically, if we take a look at the daily chart, that same trend line that saw the pair reverse only a week or so ago is once again making its presence felt. As a result, we have sound reason to suspect the pair to make a push higher once again. What’s more, the 100 day EMA – an average that has reliably been a source of dynamic support – is well positioned to cap downside risks significantly moving ahead.

In addition to these technical readings, the Stochastics and Parabolic SAR are both indicating that buying pressure should return in short order. Importantly, whilst not currently oversold, the stochastics oscillator is flirting with the vital 20.0 level which will help to put a pin in the bear’s plans to remain in control of the USDCAD. Similarly, the Parabolic SAR reading is yet to invert to bearish which will help to rally the bulls once a green candle is finally seen.

As for the fundamental outlook, this is pretty much in line with the technical bias which comes, primarily, as result of the forecasted Canadian employment data. In particular, the unemployment rate is expected to jump to 6.6% (up from 6.5% previously) which should see the USDCAD receive a bid. Notably, this uptick would come in the wake of an anaemic Ivey PMI figure of 53.8 which could exacerbate buying pressure.

Ultimately, due to both the technical and fundamental biases, we expect to see the Loonie reverse in the very near future. Nevertheless, gains will likely be limited to the 1.3554 mark which is not only a historical high point but also the 38.2% Fibonacci retracement. If gains do extend beyond this level in the near-term, it will likely come as a result of a major fundamental upset – the kind that is notoriously hard to predict.

Gold Reaches A Key Reversal Zone

Key Points:

- Price action reaches a key inflection point and reversal zone.

- Watch for a failure to break through the current resistance zone.

- A downside move back towards $1278 an ounce is likely in the short term

Gold has proved relatively triumphant over the past few weeks as the precious metal has continued to trade within the relatively safety of a rising channel. However, the metal's price action is now reaching a key inflection point that has previously led to a reversal. Subsequently, the question remains as to whether Gold can retain its bullishness in the days ahead or whether I will succumb to the mounting downside pressures.

A cursory review of the chart clearly demonstrates the metal's present conundrum with price action having entered a reversal zone around the $1294 an ounce mark. This resistance level represents the April high and is likely to be a critical level for the commodity as we move forward. A failure to push, and continue its rally, would potentially lead to a sharp decline lower as momentum stalls and the air exits the balloon rapidly. Lending further credence to the bearish scenario is the fact that the RSI Oscillator is also strongly overbought which suggests that a reversal, or a period of moderation, is the likely play.

Fundamentally, Gold has been the net beneficiary or a range of mixed economic data emanating from the U.S. of late with the relatively poor Personal Consumption Expenditure (PCE) from last week. The metric's deflator is typically used by the Fed to measure domestic inflation and, subsequently, the disappointing result poured cold water on the markets near term rate hike sentiment. However, the result may prove to be transitory given that the latest round of JOLTS Job Openings figures showed some strong gains and will very likely please the U.S. Central Bank. Subsequently, Gold is likely to negatively react as we move closer to the Fed's FOMC meeting and a potential rate hike from the central bank and this is likely to see a mean reversion in the near term.

Ultimately, the technical and fundamental factors are aligning to suggest that the precious metal could be facing a decline, or at least a period of moderation, over the short term. Subsequently, the most likely scenario is one where price action fails to breach resistance at $1295.47 and the bears flood in to push the metal back towards the $1278.00 an ounce mark. Once the pullback starts to occur the metal should slide fairly rapidly given the rising downside risks. However, keep a watch for any surprises from the U.S. Unemployment Claims and Wholesale Inventories figures, due out in the days ahead.

Market Morning Briefing: Dollar Index Has Tested The Major Resistance

STOCKS

Almost all equities globally are in a corrective dip mode except Shanghai which seems to have begun a fresh rally for the medium term.

Dow (21136.23, -0.23%) came off from resistance near 21230 and may test 21000 on the downside before bouncing back towards 21300 and higher in the medium term. Near term could see some consolidation or a corrective dip but overall long term looks bullish.

Dax (12690.12, -1.04%) is also in a short correction mode and could rise back soon towards 13000.Downside could be limited to 12600 just now.

Shanghai (3127.91, +0.83%) has risen sharply breaking the immediate resistance near 3120 instead of testing lower levels of 3050 as mentioned yesterday. While the index sustains levels above 3120, it could move higher towards 3170 else a re-test of 3070 is possible.

Resistance near 20200 has held well for Nikkei (19936.42, -0.22%) which fell sharply in the last 2-sessions. It could test 19820 in the next 2-sessions before again bouncing back from there.

Nifty (9637.15, -0.39%) is in a corrective mode now and could extend losses to an extent of 9600-9550 levels. Thereafter a rise back towards 9700-9800 is possible in the near term.

COMMODITIES

In the smaller time frame, Gold (1294) is overbought and needs a pause before attempting higher levels. We have been talking about 1295 for the last few weeks, which has been achieved yesterday. Now a break above 1300 is required before the higher levels of 1350-68 can be seen but a pause in the range of 1245-75 can provide the necessary bullish momentum.

In Silver (17.67) the daily close took place at par with the immediate resistance of 17.65-70. A failure to rise above 17.65-70 levels may trigger a sharp fall towards 16.91 regions.

Copper (2.55) is hovering around its support area of the short term range of 2.55-2.65. Only above 2.65, higher resistances of 2.72-80 can come into consideration.

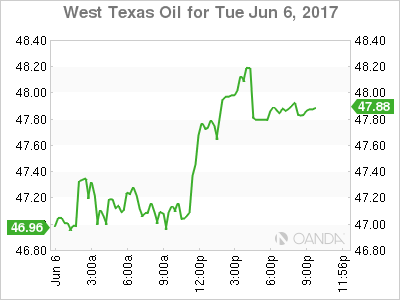

We have been tracking the support of Brent at 48.50-49 and 47 for WTI for the last few days and it has held due to oversold condition, driving both Brent (50.06) and WTI (48.12) up as expected. Now the short term oversold condition has been rectified with this upward movement and the chances of more sideways movement in the range of 50.20-52 (Brent) and 48-49.50 (WTI) are stronger now. The US weekly inventory data (expected a fall by 3.1M B) today at 8:00 P.M is supposed to trigger sharp directional moves this week. At the same time it could be prudent to be prepared for a sudden turnaround to the downside if there is a mismatch between forecast figure and the actual outcome.

FOREX

Tomorrow is going to be a very significant day for the markets as UK election, ECB policy decision and ex-FBI chief Comey's testimony will take place and the investors play safe till then with the prevalent trend continuing so far. RBI policy decision is to determine the near term Rupee direction today.

Dollar Index (96.64) has tested the major resistance of 96.50 which makes it ripe for a turnaround if the events tomorrow dictate that. For the last couple of sessions, we have been cautious about the highly overbought state of Euro (1.1265) and the proximity of the major resistance cluster of 1.1300-1.1450 which may invite a sudden selling. If Euro really weakens from the higher levels, Dollar may bounce back from its support of 96.50-25. Please note, the Euro trend remains up and Dollar trend remains down till now but we stay prepared for the possibility of a sudden trend reversal, which at the moment has 45-50% probability.

Dollar Yen (109.47) has achieved our initial downside target of 109.20 fast below which comes 108.00. It may rise only if Dollar Index manages a turnaround in the next couple of sessions.

Pound (1.2900) remains comatose and may continue for the next 24 hours till the UK election tomorrow, 8th June. While a break beyond the range of 1.2750-1.3050 is required for a clear trending move, we repeat - if the result threatens the current ruling party, then a decline towards 1.2650-00 can be expected but we prefer to wait for the actual result before taking a firm stance.

Aussie (0.7536) has surged on the back of the annual GDP coming in line with the expectations and the RBA seeing the growth accelerating above 3% in the next 2 years. Immediate resistance at 0.7550-60 must be overcome to extend the rally to 0.7600 levels and above.

Dollar Rupee (64.43) saw mild short covering before the RBI policy meet conclusion. This short covering, more than any fresh position, may be just cautionary steps to avoid any event risk. RBI is expected to maintain the status quo tomorrow but any change from the current hawkish bias can trigger an expansion of volatility. Immediate support remains 64.30 with resistance coming at 64.70.

INTEREST RATES

The US yields are almost stable and could bounce a little in the near term. the 10-5 Yr (0.43%) has come off sharply and could test 0.40% in the near term if the current momentum continues. In that case we may expect the near end US yields to remain stable or rise slightly compared to the longer end yields (10Yr and 30YR ) respectively.

The UK-US (-1.17%) has indeed come off sharply as expected and could pull down Pound with itself to lower levels this week. The yield spread could move lower towards -1.25% in the near to medium term.

The Japan-US 10Yr yield spread (2.11%) is headed lower and seems bearish for the medium term. While it moves down, Dollar YEna dn Nikkei could also move down with limited upside for now.

The German-US 2Yr (-2.08%) is trying to break below immediate support levels and could possibly move lower in the near term. the German-US 10Yr (-1.90%) is also moving down and could test -1.95% in the near term. This could possibly indicate an upcoming corrective dip in Euro in the coming sessions.

Traders In ‘Deft’ Mode

Traders in 'deft' mode

A relatively quiet APAC morning session tracking towards 'Super Thursday” as traders remain in deft mode ahead of the main risk events.

Reports that China is ready to buy more US Treasuries has driven US Treasury yields lower providing additional fodder to the sagging US dollar narrative.

Given the enormity of the risk events ahead, currency prognostication is more or less a carnival sideshow at this stage. Certainly, traders will reduce exposures on both sides of the coin as risk reward ratio becomes little more than a coin flip across the board.

EURO

The stage is set, but trade remains uninspiring.Market positioned for a shift in ECB forward guidance, so the tail risk if for a steady as you go from Draghi.

British Pound

GBP ignores data but continues to trade constructively heading into the election. Price action would suggest the market lean if for a Tory majority

Australian Dollar

AUD momentum continues to build from last week’s spell of bearishness.Given market positioning skewed short, I suspect the clean break of .7500 had near term short running for cover.GDP came out on the consensus button.But despite the happy mood on the Aussie desk this morning, lingering concerns about inflation and wage growth will likely temper the mood.Sellers are likely looking to re-enter shorts against the technical backdrop, however, price action suggests that dealers are content to let the event risk dust settle before re-engaging any dollar longs.

Japanese Yen

Offers dominated directional flow overnight, but volumes remain tepid. Certainly, the greenback is getting little support from US yield which plays into the risk aversion play on USDJPY. Exporter flow continues to weigh on the back of dealers minds as a break below the 109.00 level could see a rush to hedge dollar risk and could potentially drive the USDJPY to the low 108.00 level.

Local Asia FX

Ahead today we have the RBI – only 1 of 39 BBG economists predicting a rate cut this time around – though the market is pricing in a cut in upcoming month so market focus is on a shift to dovish guidance

USD/CAD Canadian Dollar Higher As Oil Rebounds After Qatar Turmoil

The Canadian dollar continued to advance versus the US dollar on Tuesday. The price of oil rebounded after losses on Monday following the rift between Qatar and a host of Arab nations accusing the middle eastern country of supporting terrorism. The USD is still struggling under heightened political risk with the upcoming testimony of former FBI director James Comey on Thursday.

Canadian economic data was softer with the Ivey PMI disappointing with a 53.8 reading after a 62.4 reading in April. Economic activity across all sectors in Canada came in below expectations of a flat reading of 62. The employment component is showing signs of cooling and supplier deliveries fell into contraction at 44.6. Next up in the Canadian economic calendar is the release of Building permits on Wednesday, June 7 and Housing starts and NHPI on Thursday, June 8. Housing data has been given more priority as there appears to be an impact to the latest efforts from the government to cool down a real estate bubble. Prices in Toronto have been reported to have grown at a lower rate than last year, although there are signs that Vancouver might be heating up again. Canada's benchmark rate sits at record low 0.50 percent with no hike in sight for 2017.

The USD/CAD lost 0.179 in the last 24 hours. The currency is trading at 1.3450 with the US dollar still under pressure from political risk. Disappointing employment data on Friday and an underwhelming ISM non-manufacturing PMI on Monday (56.9) have not derailed the market's expectations of a U.S. Federal Reserve rate hike on June 14. The CME FedWatch tool is still showing the probability of higher Fed funds rates at higher than 95 percent.

Former FBI Director James Comes testimony on Thursday, a day already full of uncertainty due to the UK elections, could shock the White House. The uncertainty of the outcome is putting downward pressure on the USD. Reports from ABC news are saying Comey will not accuse the President of obstruction of justice, but until the testimony is not done there is little to rule out. Trump for his part said that his tax and health care reforms are coming, and renewed his pledge to build a border wall.

Oil prices gained 1.628 percent on Tuesday. The price of West Texas Intermediate is trading at $48.01 after Monday's drop on the back of the diplomatic rift between Qatar and a host of Arab nations. The turmoil between Organization of the Petroleum Exporting Countries (OPEC) members could spell the end of price stability after the group partnered with Russia and other major non-members to cut production until March 2018.

The Energy Information Administration (EIA) reported on Tuesday that US crude production will reach 10 million barrels a day in 2018 breaking a record that stood since 1970. Higher US production has keep oil prices lower as rig counts have doubled in the last 12 months.

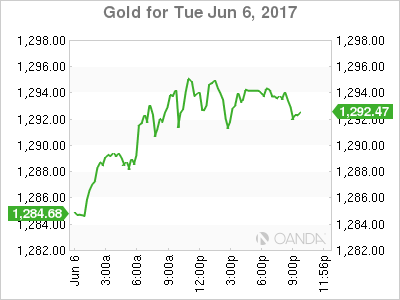

Gold has gained 0.983 percent in the last 24 hours. The yellow metal is trading at $1,292.19 as geopolitical tensions are driving risk aversion higher around the world. The rift between Qatar and other Arab nations, UK elections and the testimony of the former FBI director on Thursday have gold bid. The European Central Bank (ECB) is also scheduled to deliver its monetary policy statement on the same day. Thursday will be a key day for gold traders as trends could quickly reverse once the biggest uncertainties in the market are resolved, or it could lead to higher prices if Brexit and US impeachment risks are higher at the end that day.

Market events to watch this week:

Wednesday, Jun 7

10:30am USD Crude Oil Inventories

9:30pm AUD Trade Balance

Tentative CNY Trade Balance

Thursday, Jun 8

All Day GBP Parliamentary Elections

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Unemployment Claims

Friday, Jun 9

4:30am GBP Manufacturing Production m/m

8:30am CAD Employment Change

8:30am CAD Unemployment Rate

Panda Clouds The USD/JPY Picture

The lockstep correlation with Treasury yields is a driving factor in USD/JPY trading but the revelation that China is on the bond bid changes the equation. The yen was the top performer while the US dollar lagged. Australian GDP is up next.

The bond market might not be all that it seems. US 10-year yields fell to the lowest since the US election night on Tuesday in what looks like a sign of risk aversion and waning hopes for Fed hikes.

Or maybe not

A Bloomberg story, citing sources, said that China has been on the bid since March and may continue to buy. It's no coincidence that 10-year yields peaked at 2.62% in March and have tracked down to 2.14%. The latest leg lower broke the April lows and threatens a return all the way to pre-election levels near 1.80%.

The tight correlation with USD/JPY would imply a corresponding drop back to 100.00.

The China news changes things. It's a sign that 10-year yields are more a reflection of what China reserve managers want to hold, rather than a view of market participants on the economy.

Regardless of who is buying bonds, yield differentials will be important for USD/JPY. But they're not the whole story and the correlation shouldn't be the whole story for USD/JPY either. For the near term, the technicals may dominate as the April low of 108.13 comes into view.

Up next is Q1 Australian GDP. The RBA yesterday brushed off a weak quarter and that helped AUD/USD rise to a one-month high above 0.7500 but the market wants to see just how bad the quarter was. The consensus is for +0.3% q/q growth but some estimates are in negative territory.

Political Uncertainty Drives Gold to 7-Week high; Dollar Extends Losses

Uncertainty ahead of the UK general election and Comey's testimony in the US Congress on Thursday drove gold to a 7-week high in European trading today, while the US dollar made fresh lows.

The greenback has been under pressure since Friday when a disappointing non-farm payrolls report dampened expectations of a third rate hike by the Fed this year, although markets are still pricing a rate increase at next week's FOMC meeting. However, worries of an escalating political fallout in the US from James Comey's upcoming testimony are also weighing on the dollar. The former FBI director is due to appear before the Senate Intelligence Committee on Thursday about his discussions with President Trump regarding dropping the investigation into the ex-National Security Advisor Michael Flynn's alleged contacts with Russia.

Further exasperating the dollar's decline today was a plunge in US treasury yields. The yield on 10-year Treasury notes hit the lowest since mid-November on reports that China is readying to increase its holdings of US government bonds. The dollar index touched a fresh 7-month low of 96.53 earlier today before firming to around 96.62 in late European session. Against the yen, the dollar slid 1% to a 6-week low of 109.27 before later recovering slightly to around 109.45. The rebound came after a rise in the JOLTS job openings in May. Job openings in the United States increased to 6.04 million last month from a revised 5.79 million in April.

The pound meanwhile fell back from 1½-week lows, breaching below the 1.29 level against the dollar in afternoon European trading, having earlier hit a session peak of 1.2950 dollars. Britain goes to the polls on Thursday following Theresa May's call for a snap general election. Sterling has managed to stay resilient despite May's Conservative party sharply reducing its lead over Labour and two major terror attacks in the past two weeks. However, election jitters may finally be hitting traders as the Labour party continues to see rising support with just two days to go till voting day. The pound last stood at 1.2890 dollars in late session.

The euro stuck to a tight trading range on Tuesday and was trading near Friday's 7-month highs at 1.1270 dollars. Expectations that the ECB will change its tone to a less dovish one when it meets for its policy meeting on Thursday continued to support the single currency. There was little reaction to data out of the Eurozone today. The Eurozone sentix index rose by 1.0 to 28.4 in June, beating estimates of 27.5. Retail sales for the region were also released today, with the month-on-month rate falling short of forecasts of 0.2% to rise by 0.1% in April.

The Canadian dollar was slightly weaker in late European trading after the Ivey PMI unexpectedly fell in May. The Ivey PMI, which measures economic activity across all sectors in Canada, fell to 53.8 in May from 62.4 in April. Expectations were for a reading of 62.0. USD/CAD rose to 1.3480 after the data.

Gold prices surged to a 7-week high on Tuesday as Thursday's risk events generated increased demand for safe-haven assets. The yellow metal climbed more than 1% to $1294.80 an ounce in late session.

The yen also rallied today on the back of the increased risk-off sentiment. However, despite the risk aversion, the Australian and New Zealand dollars managed to head higher versus their US counterpart. The aussie was boosted earlier in the day from a positive outlook on Australian growth by the RBA, helping it hit a one-month high of 0.7517 against the greenback. The kiwi was even more bullish as it soared towards 3-month highs to break above the 0.72 level after another increase in global dairy prices. The GDT price index rose by 0.6% at the latest bi-weekly auction, making it the sixth straight increase.

Yen Strengthens on Positive Japanese Wage Report

USD/JPY has posted considerable losses on Tuesday, losing 0.84 percent. In the North American session, USD/JPY is trading at 109.60, marking a 6-month low for the pair. On the release front, Japanese Average Cash Earnings posted a gain of 0.5%, above the forecast of 0.3%. In the US, there was good news from the employment front, as JOLTS Jobs Openings jumped to 6.04 million, crushing the estimate of 5.65 million.

The Japanese yen received a boost on Tuesday, thanks to a solid wage growth report. Average Cash Earnings in April posted a respectable gain of 0.5%, rebounding from a 0.3% decline in the previous release. The dollar has dropped below the 110 level for the first time since April 25. The Japanese economy has shown some improvement, as stronger global demand has buoyed the export and manufacturing sectors. Japan will release Final GDP on Wednesday, and the markets are expecting GDP to be revised upwards to 0.6%, compared to 0.5% in the Preliminary GDP. If the GDP matches or beat this estimate, the yen's gains could continue.

The Federal Reserve holds its policy meeting next week, and the markets are widely expecting the Fed to raise rates for the second time in 2017. On Monday, the odds of a rate increase stood at 96%, but the odds have dipped to 91%, in response to the dismal Nonfarm Payrolls report on Friday. An increase in interest rates represents a vote of confidence in the US economy, but the Fed continues to have some concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets remain skeptical, with the odds of a September rate hike at just 22%. However, stronger data in the third quarter will likely raise the likelihood a September hike.