Sample Category Title

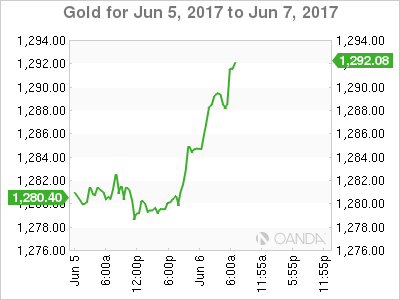

Gold Bulls Approach Major Resistance At 1300 Ahead Of Election

Safe havens have strengthened across the board as the recent risk events have lifted markets’ risk off sentiment. Notably the London terror attack, gulf states cut diplomatic ties with Qatar, and the upcoming UK general election.

Spot gold has seen a significant 6% gain since May 11th. On Tuesday, June 6th, spot gold rallied 1.1%, hitting a high of $1293.54, last seen on April 17.

The bulls still have momentum; on the 4-hourly chart the price is still holding above the downside upward-heading 10-SMA support.

Notably, the price is currently trading at the mid-term major resistance zone between 1290 – 1300. Be aware that pressure at the significant psychological resistance level at 1300 is heavier than other resistance levels.

It is likely that the bulls will test the resistance at 1300 ahead of the general election.

The UK general election will be held on June 8th, which is only 2 days away. Be aware that the election uncertainty will still likely cause volatility for gold prices before and after the release of the election outcome.

The resistance level is at 1295, followed by 1300.

The support line is at 1290, followed by 1287, followed by 1283.

Technical Outlook: US Oil – Near-Term Price Action In Range Between Daily Kijun-Sen And Fibo 61.8% Support

US oil is holding in red for the sixth straight day, pressured by concerns of global oversupply and recent geopolitical tensions in the Middle East.

Bears were so far unable to break strong support at $46.89 (Fibo 61.8% of $43.74/$51.98 rally) which held downside attempts in past two days and also containing today’s action.

Friday’s long-tailed and yesterday’s long-legged daily candles signal strong hesitation at this support, with close below needed to trigger an extension of bear-leg from 29 May lower top at $50.27.

Near-term action is capped under strong barrier at $47.86, provided by broken daily Kijun-sen/50% retracement, with immediate bearish pressure expected to persist while the price is holding below this resistance.

Bearish daily studies keep the downside at risk, however, further consolidation could be expected on oversold slow stochastic.

Extended upticks face solid barriers at $47.86 (daily Kijun-sen) and $48.40 (Monday’s high and strong upside rejection, which are expected to ideally cap.

Res: 47.72, 47.86, 48.40, 48.74

Sup: 46.89, 46.74, 46.00, 45.68

DAX Drops As Eurozone Retail Sales Misses Estimate

The DAX index has posted moderate losses in the Tuesday session. The index is down 0.91%, and is currently at 12,730.00 points. On the release front, eurozone indicators pointed to a slowdown in the retail sector. Retail PMI dipped to 52.0, down from 52.7 points. As well, Retail Sales dropped to 0.1%, down from the previous reading of 0.3%. This was short of the estimate of 0.2%. There was better news from Eurozone Sentix Investor Confidence, which improved for a fourth straight month. The indicator climbed to 28.4 points, above the estimate of 27.6 points. On Wednesday, Germany releases Factory Orders, with the markets braced for a decline of 0.2 percent.

ECB policymakers meet on Thursday for a policy meeting, at which time the ECB will set the new benchmark rate. The central bank has maintained the rate at a flat 0.0% since March 2016, and no change is expected at the upcoming meeting. At the same time, euro-area growth was respectable in the first quarter, and the markets would like the ECB to acknowledge the improvement in its rate statement or at ECB President Mario Draghi’s press conference. The ECB has been cautious and is not expected to announce any changes to its asset-purchase program, which winds up in December. Will the ECB send out a hawkish message? Analysts will be poring over the rate statement and Draghi’s follow-up comments, and any nuances or hints about a tighter monetary policy could push the euro to higher levels.

The Federal Reserve is widely expected to press the rate trigger next week, which would mark the second quarter-point increase in 2017. Even a shockingly soft Nonfarm Payrolls report on Friday hasn’t put much of a dent in these expectations, with are rate hike currently priced in at 91 percent. Another rate hike by the Fed would mark a vote of confidence in the US economy, but Fed policymakers continue to have some concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets remain skeptical, with the odds of a September rate hike at just 22%. However, stronger economic numbers in the third quarter could easily increase the likelihood a September hike.

EUR/USD – Euro Ticks Lower On Mixed Eurozone Data

The euro has ticked lower in the Tuesday session, as EUR/USD is currently trading at 1.1250. On the economic front, there are no major eurozone indicators. In the eurozone, indicators pointed to a slowdown in the retail sector. Retail PMI dipped to 52.0, down from 52.7 points. As well, Retail Sales dropped to 0.1%, down from the previous reading of 0.3%. This was short of the estimate of 0.2%. On a brighter note, Sentix Investor Confidence improved for a fourth straight month, with a reading of 28.4 points. This easily beat the estimate of 27.6 points. In the US, today’s key event is JOLTS Job Openings, which is expected to drop to 5.65 million.

The markets are keeping a close eye on the ECB, as policymakers meet on Thursday for a policy meeting. The central bank has held the benchmark rate at a flat 0.0% since March 2016, and no change is expected at the upcoming meeting. Still, the markets would like to see the ECB acknowledge a stronger eurozone economy, and will be looking for a more hawkish tone from the rate statement and follow-up comments from ECB head Mario Draghi. The ECB has been cautious and is not expected to taper its asset-purchase program, which winds up in December. Still, any hawkish nuances in the rate statement or Draghi’s comments will be seized upon by the markets, and could push the euro upwards.

The Federal Reserve holds its policy meeting next week, and the markets are widely expecting the Fed to raise rates for the second time in 2017. On Monday, the odds of a rate increase stood at 96%, but the odds have dipped to 91%, in response to the dismal Nonfarm Payrolls report on Friday. An increase in interest rates represents a vote of confidence in the US economy, but the Fed continues to have some concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets remain skeptical, with the odds of a September rate hike at just 22%. However, stronger data in the third quarter will likely raise the likelihood a September hike.

Stock Markets Gripped By Geopolitics

Financial markets were caught unaware at the start of the trading week following the shocking reports of the Saudi-led alliance severing diplomatic ties with Qatar. This unexpected development created shockwaves across the region with Qatar's stock market exposed to extreme downside shocks tumbling 7.3% on Monday. For those who were already bracing for extreme volatility ahead of the UK general election, ECB meeting and former FBI director James Comey's testimony, the escalating tensions in the Middle East are likely to leave many on high alert. A variety of geopolitical issues across the globe has clearly left investors on edge which should translate to a drop in appetite for riskier assets.

World stocks were under pressure during Tuesday's trading session as investors adopted a cautious approach by observing the action from a safe distance. Asian shares concluded depressed, following the bearish cues from Wall Street while European equities were gripped by investor anxiety. With the Gulf tensions, the drama surrounding President Trump and the pending UK general elections keeping investors cautious, the upside gains in Wall Street may be limited this afternoon.

Sterling ruled by politics

The Sterling/Dollar was showing early signs of volatility during Tuesday's trading session as pre-election jitters left investors anxious ahead of Thursday's General Election in the UK. With poll results varying from a narrowing lead for Conservatives over the Labour party to a nightmare 'hung parliament' scenario, Thursday's election result remains unclear. This uncertainty ahead of the General Election on Thursday should expose Sterling to further downside pressures.

Although a situation where Theresa May triumphs in the UK General Election is likely to support Sterling, the upside could still face some headwinds. It must be kept in mind that even after the elections are over, ongoing uncertainty revolving around Brexit and the exit negotiations may expose the Pound to downside risks. From a technical standpoint, Sterling remains driven by politics with Thursday's election result playing a key role in where the currency concludes this week. Technical traders will be paying very close attention to how prices react to the 1.3000 resistance and 1.2775 support levels.

Dollar bears unstoppable

The Greenback was attacked by bearish investors on repeated occasions last week as the ongoing political turmoil in Washington weighed heavily on the currency. Sellers were swift to exploit May's soft US jobs report to initiate renewed rounds of selling during Monday's trading session with prices descending towards 96.50.

In a week where major events across the globe are likely to spark volatility, the main event risk for the Dollar will be the testimony of former FBI Director James Comey before the Senate Intelligence Committee on Thursday. Comey's testimony will come under heavy scrutiny with markets paying extra attention to see if anything new is brought to the table. Any new revelations or fresh information on whether President Trump wanted him to stop probing his connections to Russia could leave the Dollar vulnerable to heavy losses.

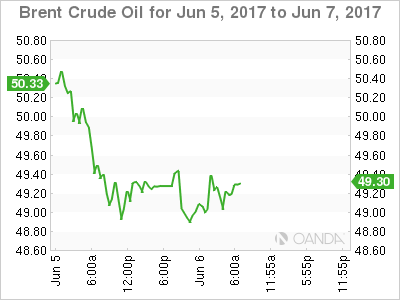

WTI Crude wobbles above $47

The ongoing weakness seen in oil prices continues to highlight how oversupply woes in the markets have hindered investor attraction towards the commodity. In the headlines, the Saudi-led alliance cutting diplomatic ties with Qatar does not actually change the heavily bearish outlook for the Oil markets. With oversupply concerns still a recurrent theme, and OPEC's efforts to re-balance the markets repeatedly sabotaged by US Shale production, WTI Crude remains vulnerable to downside risks.

There are suspicions that the decision by the Saudi-led alliance to cut diplomatic ties with Qatar could spark discussions over whether Qatar adheres to its production quota. The potential threat of Qatar going against the production quota could entice other OPEC members to also defy the conditions of the agreement consequently pressuring oil markets further. From a technical standpoint, WTI Crude is heavily bearish on the daily charts. A breakdown below $47 should encourage a further decline towards $46.

South Africa enters technical recession

Sentiment towards the South African economy took a hit on Tuesday following reports of the nation falling into a technical recession for the first time since 2009. The latest GDP data released by Stats SA showed that the economy declined by 0.7% in the first quarter of 2017 with all industries excluding agriculture and mining contracting. Despite this decline, there remains some optimism over GDP growth finding some ground and rebounding to 0.7% in the second quarter of 2017 amid the stabilizing economic data seen in recent months.

The South African Rand weakened following this news with the USDZAR edging towards 12.9000. Repeated weakness from the Rand should encourage a further incline towards 13.0000 on the USDZAR

Investors – Get Ready For Super Thursday

Capital markets are in a 'wait and see mode' now that the Fed (June 13-14) and the ECB (June 8) are all in a quiet period ahead of their key policy decisions.

The EUR, for now, remains contained on the assumption that the ECB may take a less 'dovish' tone – will the 'single unit' take flight if Draghi and company discuss dropping some of their pledges to ramp up stimulus?

Aside from central banks, most of investors' attention this week has shifted to the U.K's snap election and testimony from former FBI head James Comey on 'Super' Thursday.

Currently, U.K polls are suggesting that PM Theresa May might not be able to bolster her majority, while Comey's testimony may offer clues to how the probe into the Trump campaign's contact with Russian officials will impact the administration's ability to push through its policy agenda.

The 'mighty' dollar trades atop of its eight-month lows with safe-haven assets in vogue, mostly supported by new geopolitical Middle-East concerns – gold and yen remain better bid while U.S yields trade near the lowest levels since November.

U.S data of late has done little to dissuade the market that domestic growth remains intact. Fixed income dealers are forecasting a more than +90% chance of a Fed interest-rate hike next-week.

1. Global equities under risk aversion pressure

The aforementioned geopolitical worries have taken its toll on global equities in the overnight session, a follow on from Monday's modest losses on Wall Street.

In Japan, the Nikkei plummeted -1% pressured mostly by a strong yen (¥ 109.62) sapping sentiment. The broader Topix index fell -0.8% for the biggest decline since May 18.

Down-under, Australia's S&P/ASX 200 Index tumbled -1.5%, the most in more than two-months and this despite the RBA standing pat on interest rates as expected (see below).

In Hong Kong, the Hang Seng Index rallied +0.3% while the Shanghai Composite Index slipped -0.1%.

In Doha, Qatari stocks plunged the most since 2009 yesterday after four U.S Arab allies isolated Qatar over its ties to Iran.

In Europe, indices trade slightly lower across the board, led by the Swiss SMI leading the decliners with notable weakness in the chemical sector. The Airlines are again the focus in the FTSE 100.

U.S equities are set to open in the red (-0.1%).

Indices: Stoxx50 -0.3% at 3570, FTSE -0.3% at 7506, DAX -0.4% at 12774, CAC-40 -0.3% at 5293, IBEX-35 -0.2% at 10867, FTSE MIB +0.1% at 20749, SMI -0.8% at 8976, S&P 500 Futures -0.1%.

2. Oil slides on Middle-East worries, gold shines

Concerns over the rift between Saudi Arabia and allies with Qatar continue to weigh on oil prices and undermine efforts by OPEC to tighten the market.

Saudi Arabia, the United Arab Emirates, Egypt and Bahrain closed all transport links with top 'liquefied natural gas and condensate shipper' Qatar, accusing it of 'supporting extremism and undermining regional stability.'

Benchmark Brent crude is -15c a barrel lower at +$49.32, down around -8% from the open of futures trading on May 25, when an OPEC-led policy to cut oil output was extended into Q1 of 2018. U.S light crude (WTI) is down -15c at +$47.25.

Note: With oil production of about +620k bpd, Qatar is one of the smallest crude producers in OPEC, but some investors fear tension within OPEC could weaken its agreement to hold back production in order to prop up prices.

Some crude 'bulls' believe that inventories in the U.S may provide some near-term relief as we head in to the summer driving season, but the 'bears' counter this argument with continued growth in U.S production to weigh on the inventory discussion.

Ahead of the U.S open, gold is holding steady (+0.7% to +$1,289.19), hovering close to its six-week high print in Monday's session, on weaker global stocks and amid dwindling expectations for aggressive U.S rate hikes this year.

3. Yields curves flatten on fear

The yield on the benchmark U.S 10-year is little changed in the overnight session; at +2.16% it's trading atop its lowest level in more than five-months.

The subdued move in the bond market reflects investors' hesitance to place large bets before Thursday's ECB meet, U.K snap election and former FBI Director Comey's testimony.

Many believe that Thursday's geopolitical outcome is unlikely to stop the Fed from raising short-term interest rates next week, but it raises some question whether U.S policy makers may stand pat during the balance of this year after a June hike.

Note: Expectations of a slow-moving Fed have reduced anxiety over a swift rise in Treasury bond yields, contributing to the slides of bond yields since the Fed's policy meeting in March. The 10-year Treasury yield traded above +2.60% in March.

Fading hopes for greater fiscal stimulus has pushed down the USD and the yield on 10-year Treasury note back to levels seen before Trump's election.

Elsewhere, the yield on Aussie 10-year government bonds have lost -2 bps to +2.37%. In the U.K, 10-year Gilt yields fell -2 bps to +1.04%, in Germany, Bunds lost -2 bps to +0.27%.

4. Dollar trades at eight-month lows

EUR is expected to trade in a contained range between €1.12-€1.13 ahead of the ECB meeting on Thursday. Given some of the expected tapering of QE is already priced in, and given that ECB's Draghi will likely avoid hints at imminent QE tapering even as the ECB is expected to make some 'subtle' changes to its communication, any EUR gains are expected to be somewhat limited.

With the USD trend remaining weak, any downside implications for the EUR are expected to be limited, especially given a low probability the Fed will embark on an 'aggressive tightening cycle.'

In the U.K, a Survation Poll on the Parliamentary elections shows support for Conservatives Party at +41.5% vs. +40.4% for Labour. Despite the disappointing reading for PM May, sterling (£1.2919) remains above the psychological £1.2900 handle.

Note: The Survation poll in particular assumes that a higher young voter turnout would occur; historically this tends not to happen.

The yen has found support from risk averse investors, trading atop of its seven highs at ¥109.64.

Down-under, the AUD (A$0.7482) ended higher overnight after the RBA (see below) left interest rates on hold and downplayed concerns about a slowdown in the economy over recent months.

5. RBA monetary policy decision – Euro retail sales

The RBA left their benchmark overnight rates on hold at a record low +1.5% as Aussie policy makers juggles fears around rising house prices and record household debt, with signs of weakness in the job market and a slowdown in consumer spending.

Governor Philip Lowe in his statement said 'the board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.'

The market has perceived the RBA to be more 'neutral' than expected. Up to this point, policy makers have said little about signs of a slowdown in the economy in Q1; tomorrow's GDP growth data is expected to show the economy barely moved in the first three-month.

Instead, the RBA seems to be is intent on focusing on the expectation that domestic growth will pick up to above +3%, and the transition occurring in the economy away from mining investment as being 'almost complete.' They also added that business conditions have improved and that capacity utilization has increased.

Elliott Wave View: HG#F (Copper) Extension lower

HG#F (Copper) is showing 5 swings incomplete sequence from 2/13/2017 high, preferred Elliott wave view suggests rally to 2.619 completed 6th swing as a FLAT in wave (B) and metal has now resumed the decline in 7th swing. Decline from 2.619 is so far corrective so wave (C) is expected to take the form of an Ending diagonal where wave 1 ended at 2.539 and wave 2 ended at 2.581 as a FLAT. Near-term focus is on 2.526 – 2.500 area to complete 3 waves from wave 2 peak, this area can result in a bounce in 3 waves again which should fail below 2.581 high and more importantly below 2.619 high for extension lower towards 2.376 – 2.2716 area to complete 7 swings from 2/13/2017 high.

HG#F (Copper) 1 Hour Elliott Wave Chart

Elliott Wave View: NZDUSD Showing Impulse

Short term Elliott wave view in NZDUSD suggest that the cycle from 5/11 low (0.6816) is unfolding as an impulsive Elliott wave structure . This 5 wave move could be a wave C of a FLAT correction or wave A of an Elliott wave zigzag structure structure. In either case, after 5 wave move ends, pair should pull back in 3 waves at least as the Elliott Wave Theory suggests. The Minute wave ((i)) ended at (0.6948), Minute wave ((ii)) pullback ended at (0.6880), Minute wave ((iii)) at 0.7121 peak, Minute wave ((iv)) pullback ended at (0.7054) low. Above from there Minute wave ((v)) of C or A already reached the minimum extension area in between inverse 1.236-1.618% extension area of previous wave ((iv)) already at 0.7135-0.7161 area. Which means cycle from 5/11 low (0.6816) is mature and pair can start the 3 waves pullback at any moment.

However as far as dip remains above wave ((iv)) dip (0.7054) & more importantly while the Rsi divergence at the peak stays intact pair may see further advance towards ((v))=((i)) target area at 0.7186-0.7217 area or in case of further strength pair may see 0.618-0.764% fibonacci Extension area of wave ((i))+((iii)) at 0.7243-0.7289 before ending the 5 waves impulse sequence from 5/11 low. Afterwards pair should pullback in 3, 7 or 11 swings for the correction of 5/11 cycle or If the decline turns out to be stronger than expected and breaks the pivot at 5/11 low (0.6816) then that would suggest 5 wave move up from 0.6816 low was part of a wave C of a FLAT from 3/09 (0.6889) low and pair may resume lower.

NZDUSD 4 Hour Elliott Wave Chart

Elliott Wave Analysis: EURUSD Could Face A Significant Turning Point

EURUSD reached new highs on Friday as expected after previous fall in three waves down to 1.1106 which was identified as a contra-trend move. As such, pair can be running into some final stages of a bigger recovery seen on daily chart, but there is still room for 1.1320-1.1360 area before some bearish reversal may show up this week.

EURUSD, 1H

GOLD Bullish Momentum Is Fading, SILVER Continued Bearish Consolidation, CRUDE OIL Strong Decline.

GOLD Bullish momentum is fading.

Gold is pushing higher within uptrend channel. Hourly support is located at 1246 (18/05/2017 low). Stronger support is given at 1195 (10/03/2017 low). Expected to show further upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Continued bearish consolidation.

Silver declines. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to push back towards 61.8% Fibonacci retracement around 17.75.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Strong decline.

Crude oil keeps on declining after the bounce following the short-squeeze move towards $52. Support is given at a distance 43.76 (05/05/2017 low). The technical structure suggests decline towards 43.76.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).