Sample Category Title

USD/CAD Bulls Test 20-day SMA Resistance

USD/CAD has plunged 2.5% from May 5th to 24th caused by rising oil prices.

The trend has turned to an upswing since May 24th, seeing a 0.8% rebound, helped by a slump in oil prices after the recent OPEC meeting.

On the 4-hourly chart USD/CAD has turned bullish, trading above the downside uptrend line support.

This morning USD/CAD hit a 2-week high of 1.3546.

Currently, on the daily chart, the price is approaching the long-term major resistance zone between

1.3550 - 1.3600, where also the 20-day SMA is situated (1.3560).

The bulls still have momentum, however, be aware that the selling pressure is heavy at this zone.

The resistance level is at 1.3550 followed by 1.3600.

The support line is at 1.3500 followed by 1.3470.

The crucial US labour market data for May will be released today, June 2nd at 13:30 BST. It includes non-farm payrolls, unemployment rate and average hourly earnings.

Please note that the release of US labour market data will likely cause volatility for USD/CAD and other USD crosses.

Be aware that, based on prior experience after the release of the data, market trends sometimes reverse within 1-2 hours after the initial move.

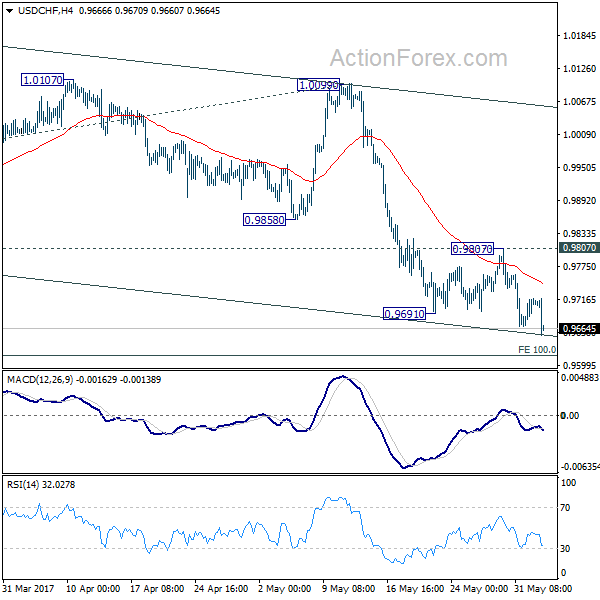

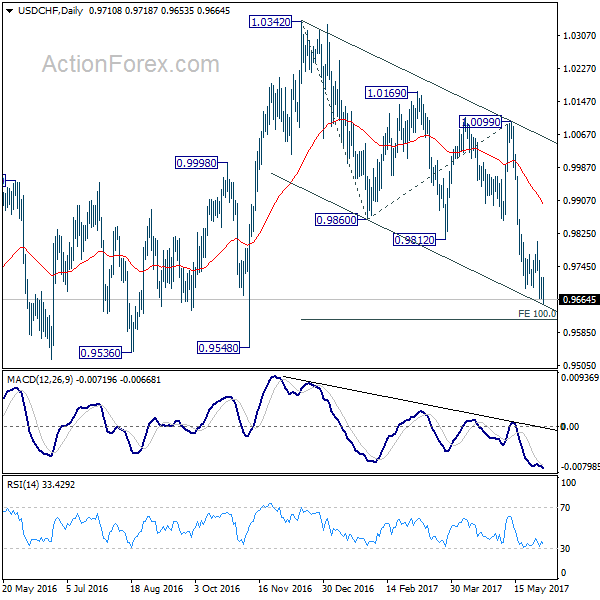

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9644; (P) 0.9702; (R1) 0.9735; More.....

USD/CHF's decline continues today and intraday bias stays on the downside for 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there. But in any case, break of 0.9807 resistance is needed to indicate short term bottoming. Otherwise, near term outlook will remain bearish in case of recovery.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

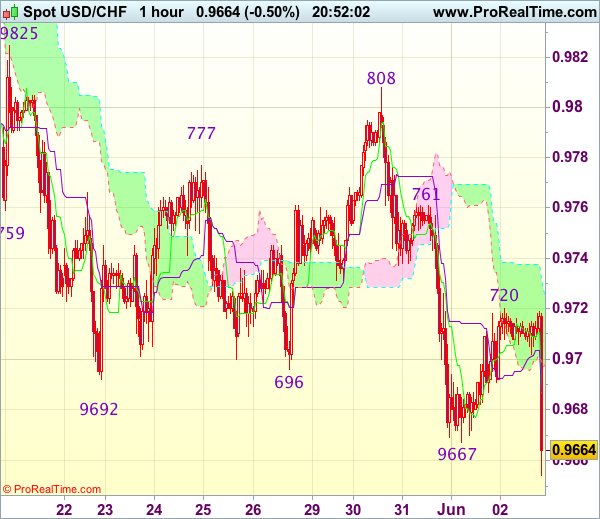

Trade Idea Update: USD/CHF – Sell at 0.9685

USD/CHF - 0.9668

New strategy :

Sell at 0.9685, Target: 0.9585, Stop: 0.9720

Position : -

Target : -

Stop : -

Current selloff in US morning together with the breach of support at 0.9667 confirm recent decline has resumed and bearishness is seen for weakness to 0.9630, then towards 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808), however, near term oversold condition should limit downside to 0.9570 and price should stay well above support at 0.9550, bring rebound later.

In view of this, we are looking to sell dollar on recovery as 0.9685-90 should limit upside. Only break of resistance at 0.9720 would abort and signal a temporary low is formed instead, bring a stronger rebound to 0.9750 and then 0.9770 but price should falter below resistance at 0.9808.

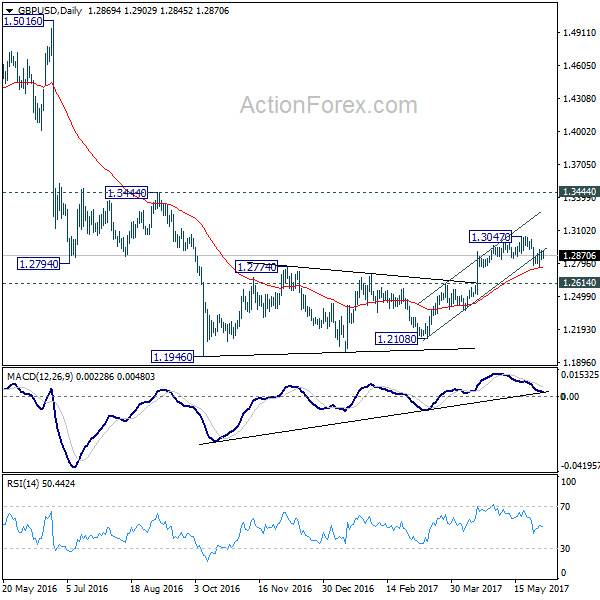

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2833; (P) 1.2874; (R1) 1.2919; More...

No change in GBP/USD's outlook and intraday bias remains neutral. With 1.2926 minor resistance intact, deeper fall is still in favor. We're holding on to view that rise from 1.2108 is completed. Below 1.2768 will target 1.2614 resistance turned support next. Break there should also indicate completion of whole consolidation pattern from 1.1946 and target a retest on this low. Meanwhile, above 1.2926 minor resistance will turn focus back to 1.3047 high instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

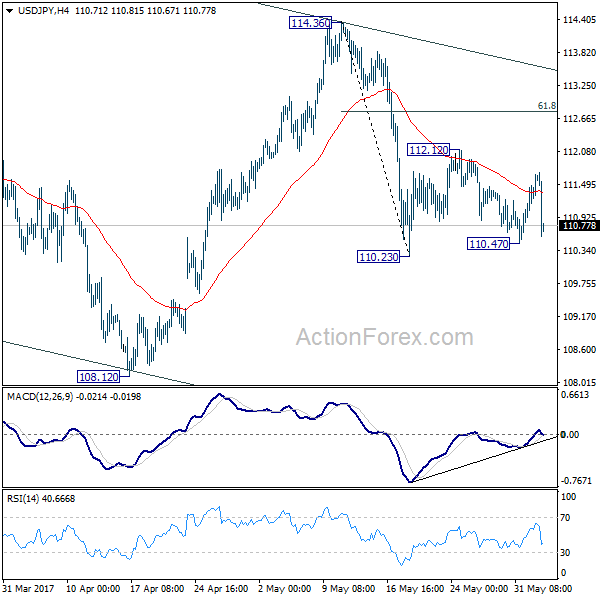

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.83; (P) 111.15; (R1) 111.69; More...

USD/JPY drops sharply in early US session but it's staying in range above 110.23 and intraday bias remains neutral. More consolidation cannot be ruled out. But upside should be limited by 61.8% retracement of 114.36 to 110.23 at 112.78 to bring fall resumption. Below 110.23 will turn bias to the downside and will likely resume the fall from 118.65 through 108.12 low. As fall from 118.65 is seen as a correction, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48. However, sustained break of 112.78 will turn focus back to 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

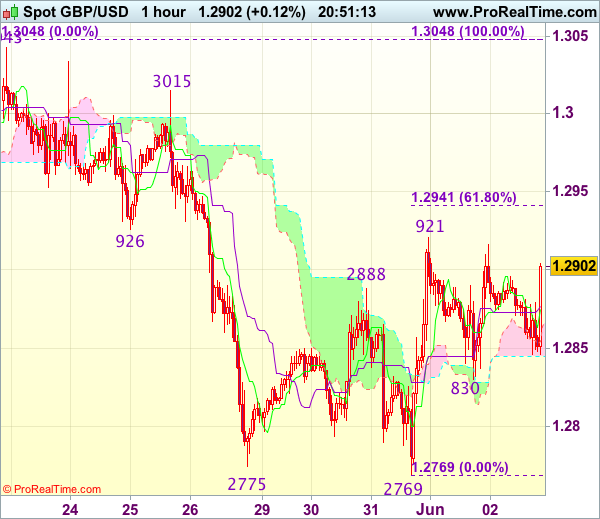

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.2873

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite rebounding to 1.2916 yesterday, as cable has retreated again after faltering below indicated resistance at 1.2921, retaining our view that further consolidation would be seen and weakness to 1.2830 support cannot be ruled out, however, only break there would signal the rebound from 1.2769 has ended, bring further fall to 1.2800 but said support at 1.2769 should remain intact.

On the upside, above 1.2905 would bring another test of 1.2921-26 (resistance and previous support), however, break there is needed to signal low has been formed at 1.2769, bring further gain to 1.2940-45 (61.8% Fibonacci retracement of 1.3048-1.2769) and later towards 1.2970 but overbought condition should cap upside below 1.3000. As near term outlook is mixed, would be prudent to stand aside for now.

Trade Idea Update: EUR/USD – Hold long entered at 1.1205

EUR/USD - 1.1266

Original strategy :

Bought at 1.1205, Target: 1.1305, Stop: 1.1170

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1170

New strategy :

Hold long entered at 1.1205, Target: 1.1305, Stop: 1.1215

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1215

As euro has rallied on dollar’s broad-based weakness after soft NFP data and resistance at 1.1257-68 was breached, confirming our view that early upmove has resumed and test of another previous chart resistance at 1.1300 is underway, above there would encourage for headway to 1.1340-45, however, overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1205. Below support at 1.1202 would abort and signal top is formed instead, risk weakness towards indicated support at 1.1164, once this level is penetrated, this would signal recent upmove has ended, bring further fall to 1.1130-40 first.

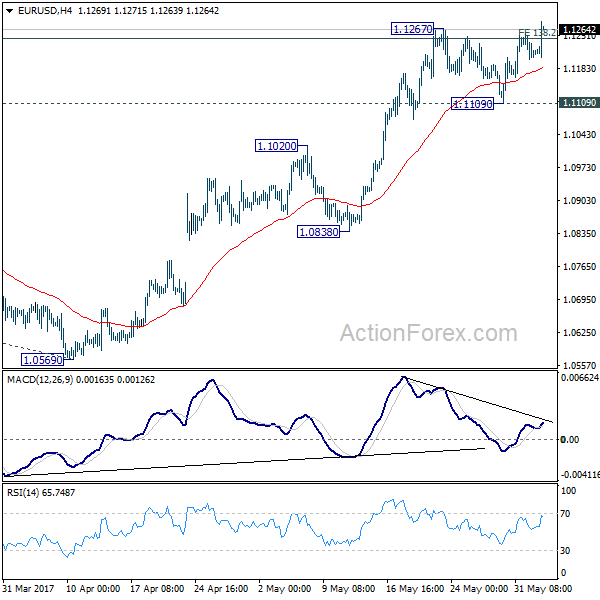

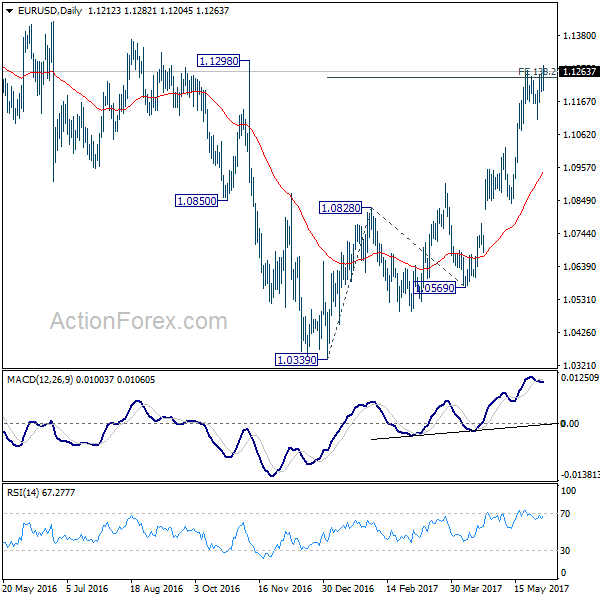

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1189; (P) 1.1223 (R1) 1.1244; More....

EUR/USD's rally resumed by taking out 1.1267 and reaches as high as 1.1282 so far. Intraday bias is back on the upside with focus on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. Near term outlook will now remain bullish as long as 1.1109 support holds. Nonetheless, we'd stay cautious on rejection from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone. Break of 1.1109 will indicate short term topping and turn bias back to the downside.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Dollar Dives Against Euro, Swiss and Yen as Non-Farm Payroll Grew Only 138k in May

Dollar dives sharply in early US session after disappointment from employment data. Non-farm payroll report showed only 138k growth in May, well below expectation of 185k. Prior month's figure was revised down from 211k to 174k. Unemployment rate, though, dropped to 4.3%, lowest since 2001. Average hourly earnings grew 0.2% mom, meeting expectation. But prior month's figure was also revised down from 0.3% mom to 0.2% mom. Also released, US trade deficit widened to USD -47.6b in April. Canada trade deficit narrowed to CAD -0.9b in April. Canada labor productivity rose 1.4% qoq in Q1.

EUR/USD surges through recent high at 1.1267 after the release, resuming near term rally and is having 1.1298 key resistance in focus. USD/CHF extends the current decline to as low as 0.9653 so far. Meanwhile, 10 year yield drops sharply through key near term support of 2.177. Gold jumps sharply to as high as 1278.8 and is heading to 1280 handle.

Germany, France and Italy issued joint "regret" statement

German Chancellor Angela Merkel described US President Donald Trump's decision to withdraw from the Paris climate accord as "extremely regrettable" and she also emphasized that she was expressing herself "in very restrained terms". She called for those who believe "the future of our planet is important" to "continue doing down this path so we're successful for our Mother Earth." Merkel also pointed out that Trump's decision "can't and won't stop all those of us who feel obliged to protect the planet".

French President Emmanuel Macron delivered a three-minute address to Americans in English, streamed live from Elysee Palace. And he offered a refuge to "all scientists, engineers, entrepreneurs, responsible citizens who were disappointed by the decision of the president of the United States" that "they will find in France a second homeland". He called on those people to come and work with the French and pledged that "France will not give up the fight".

Merkel, Macron and Italian Premier Paolo Gentiloni issued a joint statement taking notes "with regret" on Trump's decision. Together they regarded the accord as "a cornerstone in the cooperation between our countries, for effectively and timely tacking climate change". And they added the course charted by the accord is "irreversible and we firmly believe that the Paris Agreement cannot be renegotiated".

Corbyn accused May of being "subservient" to Trump

In UK, Prime Minister Theresa May "expressed her disappointment" to Trump regarding the decision. A spokesperson of the Downing Street said that "the Prime Minister stressed that the UK remained committed to the Paris Agreement, as she set out recently at the G7." And, "provides the right global framework for protecting the prosperity and security of future generations, while keeping energy affordable and secure for our citizens and businesses."

May's rival, Labour leader Jeremy Corbyn accused May of being "subservient" to Trump as she remained silent over the withdrawal from the Paris accord. Corbyn called the decision as "reckless and dangerous" and Paris deal "cannot be up for renegotiation". Green Party co-leader Caroline Lucas condemned May as being "slow and timid" on her response and said it was "another sign of her weakness". She said UK should be "leading the way on tackling climate change".

With six days to go before UK's election on June 9, the Ipsos MORI poll for the Evening standard showed that support for Conservatives was down four point to 45%. Support for Labour went up six points to 50. Latest YouGov polls showed Conservatives at 42% and Labour at 39%.

Elsewhere...

Eurozone PPI rose 0.0% mom, 4.3% yoy in April. UK construction PMI rose sharply to 56 in May. Japan consumer confidence rose to 43.6 in May. Monetary base rose 19.4% yoy in May.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1189; (P) 1.1223 (R1) 1.1244; More....

EUR/USD's rally resumed by taking out 1.1267 and reaches as high as 1.1282 so far. Intraday bias is back on the upside with focus on 1.1298 key resistance. Decisive break there will carry larger bullish implication and target 1.1615 resistance next. Near term outlook will now remain bullish as long as 1.1109 support holds. Nonetheless, we'd stay cautious on rejection from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone. Break of 1.1109 will indicate short term topping and turn bias back to the downside.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y May | 19.40% | 19.60% | 19.80% | |

| 05:00 | JPY | Consumer Confidence May | 43.6 | 43.5 | 43.2 | |

| 08:30 | GBP | Construction PMI May | 56 | 52.6 | 53.1 | |

| 09:00 | EUR | Eurozone PPI M/M Apr | 0.00% | 0.20% | -0.30% | |

| 09:00 | EUR | Eurozone PPI Y/Y Apr | 4.30% | 4.50% | 3.90% | |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 1.40% | 0.20% | 0.40% | |

| 12:30 | CAD | International Merchandise Trade (CAD) Apr | -0.4B | 0.0B | -0.1B | -0.9B |

| 12:30 | USD | Trade Balance Apr | -47.6B | -45.5B | -43.7B | -45.3B |

| 12:30 | USD | Change in Non-farm Payrolls May | 138K | 185K | 211K | 174K |

| 12:30 | USD | Unemployment Rate May | 4.30% | 4.40% | 4.40% | |

| 12:30 | USD | Average Hourly Earnings M/M May | 0.20% | 0.20% | 0.30% | 0.20% |

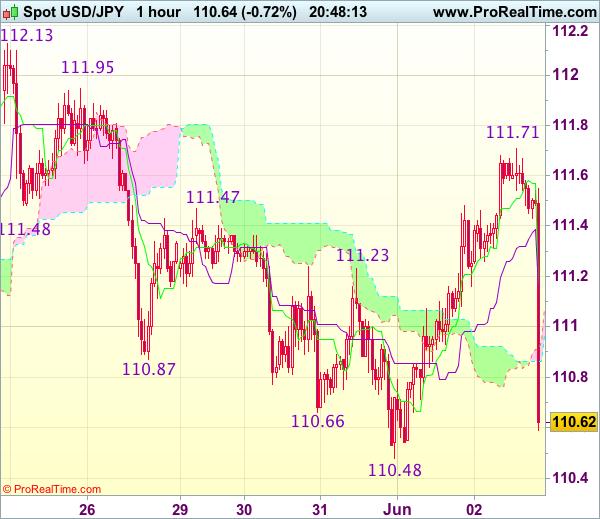

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 110.72

Original strategy :

Bought at 111.20, stopped at 110.85

Position : - Long at 111.20

Target : -

Stop : - 110.85

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback has dropped quite sharply in US morning on back of weaker-than-expected NFP data, dampening our bullishness and suggesting the rebound from 110.48 has ended at 111.71, hence test of this support cannot be ruled out, however, break there is needed to retain bearishness and extend weakness to previous support at 110.24, once this level is penetrated, this would provide confirmation that early selloff from 114.37 top has resumed for weakness to 109.90-00 first.

In view of this, would not chase this fall here and would be prudent to stand aside for now. On the upside, expect recovery to be limited to 111.00 and price should falter below 111.40-50, bring another decline later. Only break of said resistance at 111.71 would revive bullishness and bring another rise to 111.95 and possibly towards resistance at 112.13.