Sample Category Title

British Pound Trading Higher, Ahead Of UK’s 1Q GDP Data

For the 24 hours to 23:00 GMT, the GBP rose 0.08% against the USD and closed at 1.2971.

In the Asian session, at GMT0300, the pair is trading at 1.2984, with the GBP trading 0.10% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2941, and a fall through could take it to the next support level of 1.2898. The pair is expected to find its first resistance at 1.3013, and a rise through could take it to the next resistance level of 1.3042.

Moving forward, UK's gross domestic product (GDP) figures for the first quarter coupled with mortgage approvals data for April, both due for release today, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Flat In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.18% against the JPY and closed at 111.60.

In economic data, Japan’s final leading economic index recorded a rise to 105.5 in March, from a revised level of 104.7 in the previous month. On the other hand, the nation’s coincident index dropped to 114.4 in the same month, compared to a revised reading of 115.2 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 111.60, with the USD trading flat against the JPY from yesterday’s close.

The pair is expected to find support at 111.34, and a fall through could take it to the next support level of 111.09. The pair is expected to find its first resistance at 111.99, and a rise through could take it to the next resistance level of 112.39.

Looking ahead, investors will concentrate on Japan’s annual consumer price index for April, due to release at night.

The currency pair is showing convergence with 50 Hr moving average and trading below its 20 Hr moving average.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.27% against the CHF and closed at 0.9731.

On macro front, Switzerland’s industrial production declined 4.6% YoY in the first quarter, compared to drop of 3.3% in the prior quarter.

In the Asian session, at GMT0300, the pair is trading at 0.9719, with the USD trading 0.12% lower against the Swiss Franc from yesterday’s close.

The pair is expected to find support at 0.9699, and a fall through could take it to the next support level of 0.9679. The pair is expected to find its first resistance at 0.9758, and a rise through could take it to the next resistance level of 0.9797.

In absence of any major economic releases in Switzerland today, investors will look forward to global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

BoC Left Key Interest Rate Steady At 0.50%

For the 24 hours to 23:00 GMT, the USD declined 0.77% against the CAD and closed at 1.3411.

At its recent monetary policy meeting, the Bank of Canada (BoC) held the benchmark interest rate unchanged at 0.50%. Although the central bank Governor, Stephen Poloz gave a nod to improving economic data, he once again highlighted Canada’s weak wage growth and the slowing pace of underlying inflation, indicating that the economy still has room for improvement. He further added that the current degree of monetary stimulus is appropriate at present.

In the Asian session, at GMT0300, the pair is trading at 1.3398, with the USD trading 0.10% lower against the Canadian Dollar from yesterday’s close.

The pair is expected to find support at 1.335, and a fall through could take it to the next support level of 1.3302. The pair is expected to find its first resistance at 1.3493, and a rise through could take it to the next resistance level of 1.3588.

With no major economic release in Canada today, traders will keep a tab on global macro data for further direction in the currency.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

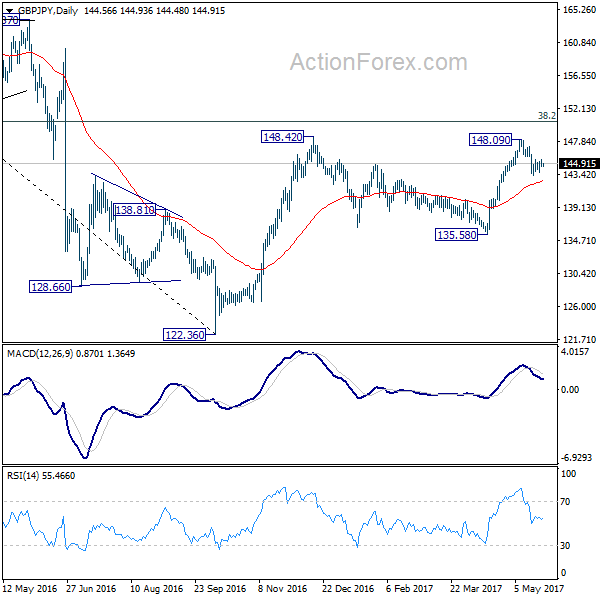

GBP/JPY Daily Outlook

Daily Pivots: (S1) 144.29; (P) 144.85; (R1) 145.21; More....

Intraday bias in GBP/JPY remains neutral as it's staying in tight range of 143.34/145/78. The corrective pattern from 148.09 short term top could extend. On the upside, above 145.78 will turn bias back to the upside for retesting 148.09 first. Meanwhile, break of 143.34 will extend the pull back from 148.09 to 61.8% retracement at 140.35. Overall, we'd still expect the rise from 122.36 to resume after pull back from 148.09 completes. Break of 148.09 will target 150.42 long term fibonacci level first.

In the bigger picture, based on current momentum, rise from 122.36 bottom should be developing into a medium term move. Break of 38.2% retracement of 195.86 to 122.36 at 150.42 should pave the way to 61.8% retracement at 167.78. This will now be the favored case as long as 135.58 support holds.

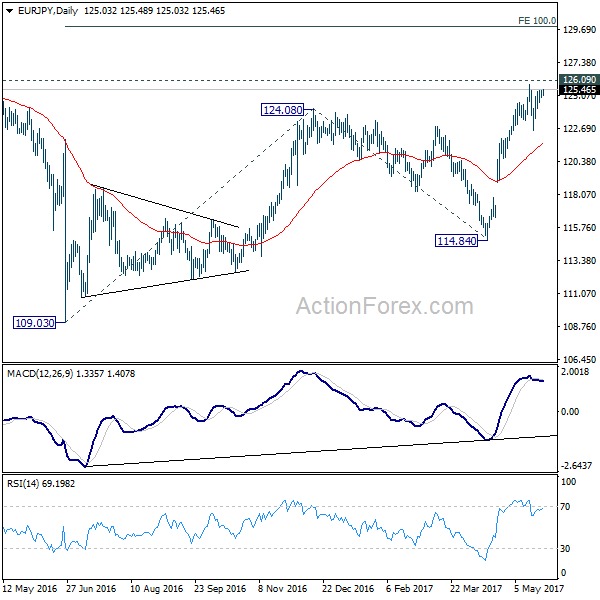

EUR/JPY Daily Outlook

Daily Pivots: (S1) 124.84; (P) 125.12; (R1) 125.34; More...

Intraday bias in EUR/JPY remains neutral as consolidation from 125.80 extends. Another fall could be seen but downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rise resumption. We're staying mildly bullish in the cross. And, break of 126.09 key resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

In the bigger picture, focus is back on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

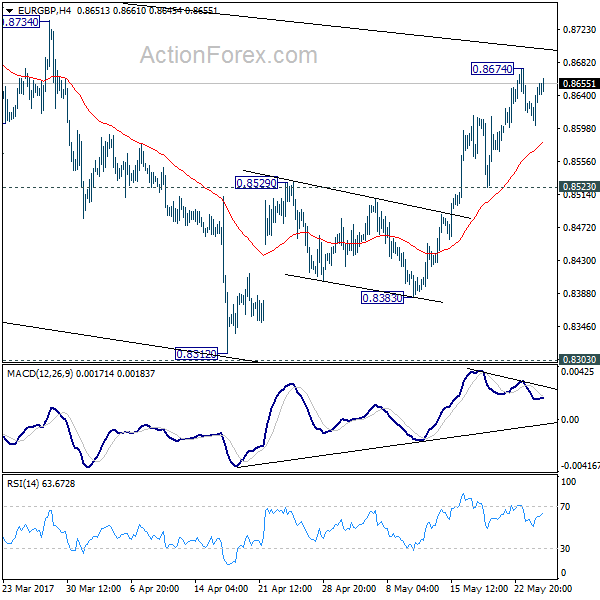

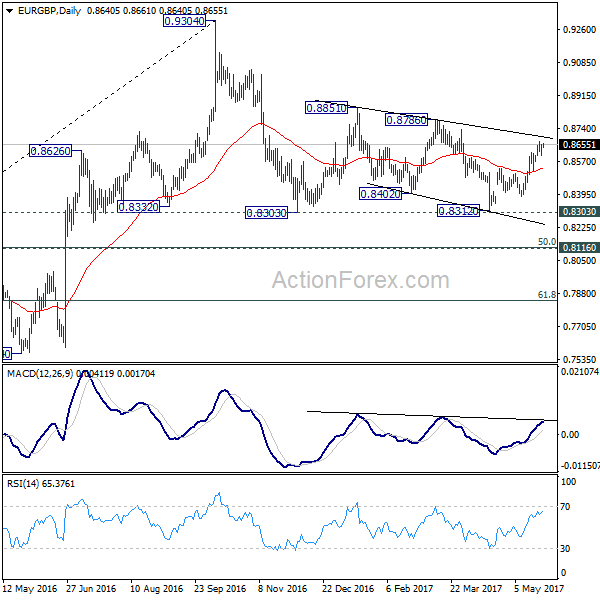

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8613; (P) 0.8634; (R1) 0.8666; More...

Intraday bias in EUR/GBP remains neutral for consolidation below 0.8674 temporary top. Further rise is expected in the cross as long as 0.8523 support holds. Above 0.8674 will extend the rise from 0.8312 to 0.8786 resistance. Note again that price actions 0.9304 are viewed as a medium term corrective pattern that is extending. Break of 0.8786 would now pave the way to retest 0.9304 high. However, break of 0.8523 will indicate that rebound from 0.8312 has completed and turn bias back to the downside.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. In case of deeper fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

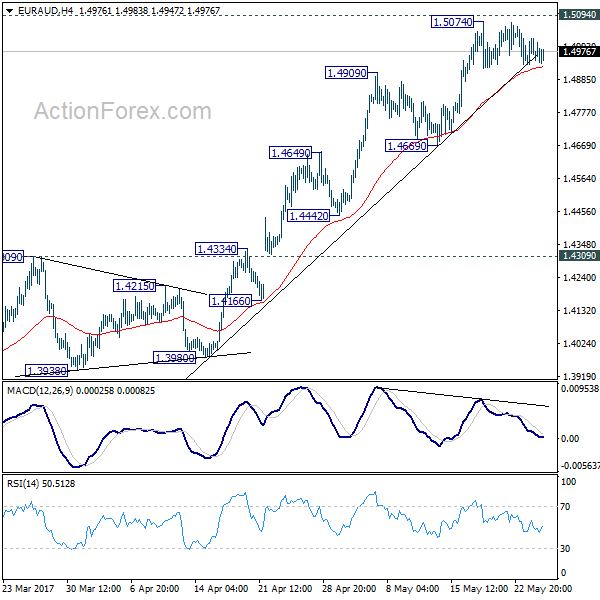

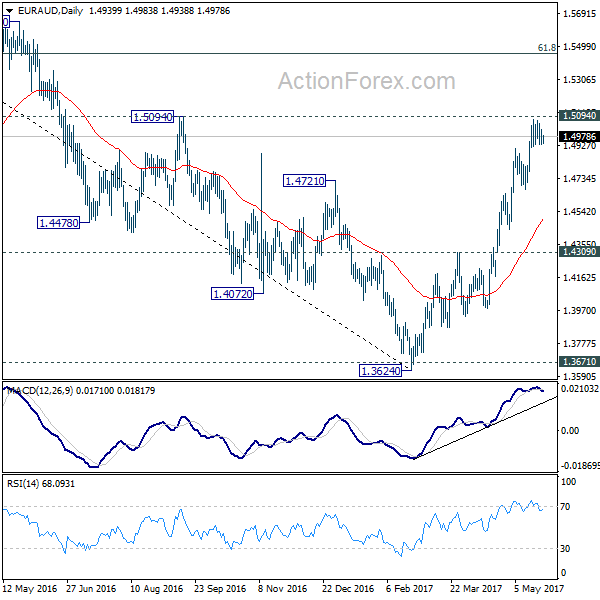

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4913; (P) 1.4966; (R1) 1.5000; More...

Intraday bias in EUR/AUD remains neutral as consolidation from 1.5074 continues. Another fall cannot be ruled out but downside should be contained above 1.4669 support and bring rise resumption. We're holding on to the bullish view that the medium term trend has reversed. Break of 1.5094 resistance will extend the rally from 1.3624 to next medium term fibonacci level at 1.5455. However, considering bearish divergence condition in 4 hour MACD, break of 1.4669 will confirm short term topping and bring deeper pull back, possibly to 55 day EMA (now at 1.4469).

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction should be completed at 1.3624 after defending 1.3671 key support. Rise from 1.3642 is now expected to target 61.8% retracement of 1.6587 to 1.3624 at 1.5455 and above. In any case, outlook will now stay cautiously bullish as long as 1.4309 resistance turned support holds.

Elliott Wave View: ES_F Resume Higher

Short Term Elliott Wave view in ES_F Index suggests the rally to 2403.75 ended Minor wave A. Minor wave B unfolded as an Expanded Flat Elliott Wave structure where Minute wave ((a)) ended at 2379, Minute wave ((b)) ended at 2404.5, and Minute wave ((c)) of B ended at 2344.5. After ending the pullback, the Index started a new leg higher and the rally from 2344.5 low looks to be unfolding as a 5 waves Elliott Wave impulse structure where Minutte wave (i) ended at 2375, Minutte wave (ii) ended at 2361, and Minutte wave (iii) is proposed complete at 2411.25. Expect Minutte wave (iv) pullback to commence soon to correct cycle from 5/19 low before turning higher one more time to end Minutte wave (v). This last push higher will also complete larger degree Minute wave ((i)).

Once Minute wave ((i)) is complete, the Index should pullback within Minute wave ((ii)) in 3, 7, or 11 swing to correct cycle from 5/18 low (2344.7) before the rally resumes again. As the Index has broken above the previous peak at 2404.5, this gives more added conviction that the it has started the next leg higher and thus pullback can likely hold above 2344.7 for more upside. We don’t like selling the proposed pullback and expect buyers to appear again once Minute wave ((ii)) pullback is complete at later stage, provided that pivot at 2344.7 low remains intact.

ES_F Index 1 Hour Elliott Wave Chart

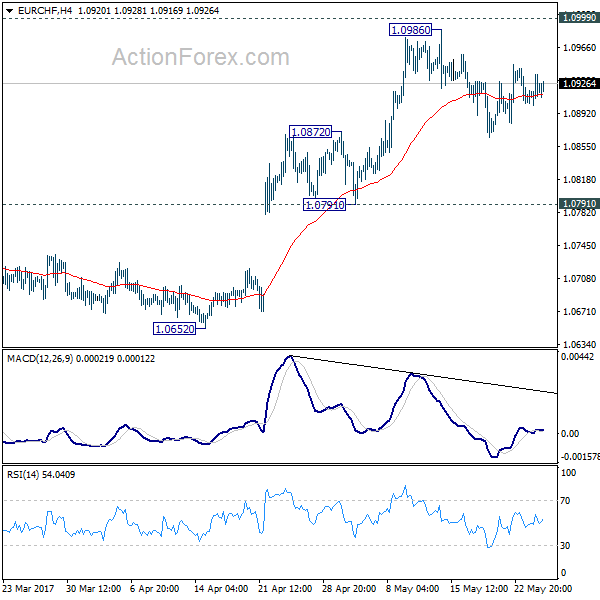

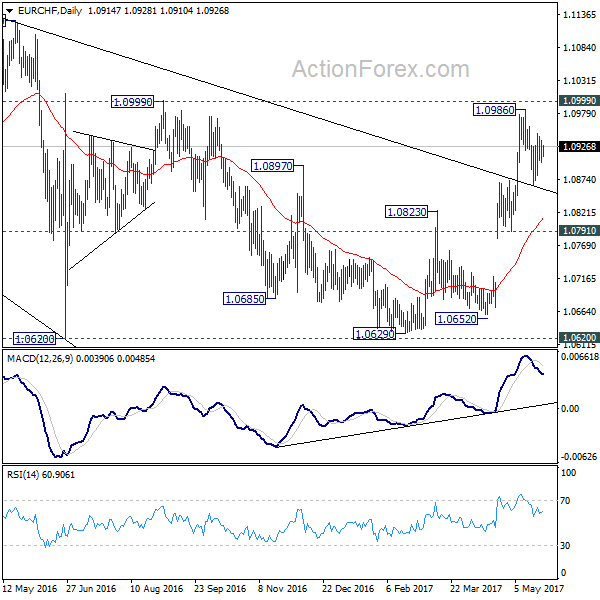

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0900; (P) 1.0919; (R1) 1.0935; More...

EUR/CHF's consolidation from 1.0986 is still in progress and intraday bias stays neutral at this point. Deeper fall could be seen but downside is expected to be contained by 1.0791/0872 support zone to bring rise resumption. As noted before, the consolidative pattern from 1.1198 should be completed. Firm break of 1.0999 resistance will pave the way for a retest on 1.1198 high.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.