Sample Category Title

Fed ‘Confirmed’ Rate Hike In June, Signaled Balance Sheet Reduction To Come Later This Year

The market was disappointed over the FOMC minutes for the May meeting. While the minutes should be considered as a confirmation of a rate hike in June, it raised the uncertainty over the future rate hike path. The members appeared divided over the inflation outlook. While one camp was concerned over the impact of falling unemployment on inflation, another camp remained focused on the downside risk to inflation. Meanwhile, it is getting more likely that the balance sheet reduction might begin 'this year'.

On the upcoming rate hike, the minutes suggested that 'most participants judged that if economic information came in about in line with their expectations, it would soon be appropriate for the Committee to take another step in removing some policy accommodation'. It is highly likely that a rate hike would be adopted in June. However, the path after that is now more uncertain. The Fed reiterated its data-dependent stance on the monetary policy outlook. As suggested in the minutes, 'members generally judged that it would be prudent to await additional evidence indicating that the recent slowing in the pace of economic activity had been transitory before taking another step in removing accommodation'. The market has priced in over 80% of a rate hike next month but expects less than 2 more rate hikes from now towards the end of the year.

Another focus is the agenda on the balance sheet reduction. The minutes unveiled that a briefing on the possible operational approach to balance sheet reduction was provided, aiming at reducing the central bank’s securities holdings in 'a gradual and predictable manner'. The minutes suggested that, under the proposed approach, 'the Committee would announce a set of gradually increasing caps, or limits, on the amounts of Treasury and agency securities that would be allowed to run off each month, and only the amounts of securities repayments that exceeded the caps would be reinvested each month'.

The minutes went on to explain that 'as the caps increased, reinvestments would decline, and the monthly reductions in the Federal Reserve's securities holdings would become larger. The caps would initially be set at low levels and then be raised every three months, over a set period of time, to their fully phased-in levels. The final values of the caps would then be maintained until the size of the balance sheet was normalized'.

The minutes suggested that 'nearly all policymakers indicated that as long as the economy and the path of the federal funds rate evolved as currently expected, it likely would be appropriate to begin reducing the Federal Reserve’s securities holdings this year'. The timing comes earlier than our, as well as the market’s, expectations that the plan on balance sheet reduction would be announced in December this year.

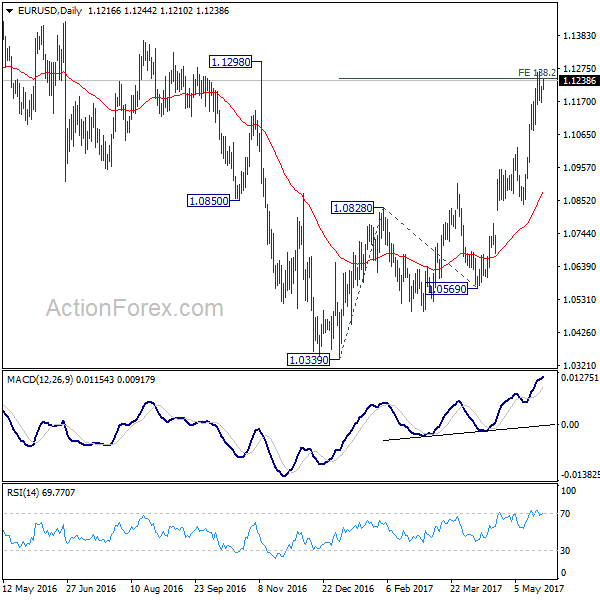

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1184; (P) 1.1202 (R1) 1.1235; More....

EUR/USD is staying in consolidation from 1.1267 temporary top. Intraday bias remains neutral first. Overall, we'd stay cautious on strong resistance from 1.1245/98 (138.2% projection of 1.0339 to 1.0828 from 1.0569 at 1.1245) resistance zone to limit upside and bring reversal. But decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. On the downside, though, break of 1.1020 resistance turned support will indicate rejection from 1.1245/98 and turn bias to the downside for 1.0838 support first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD now far above 55 week EMA. Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

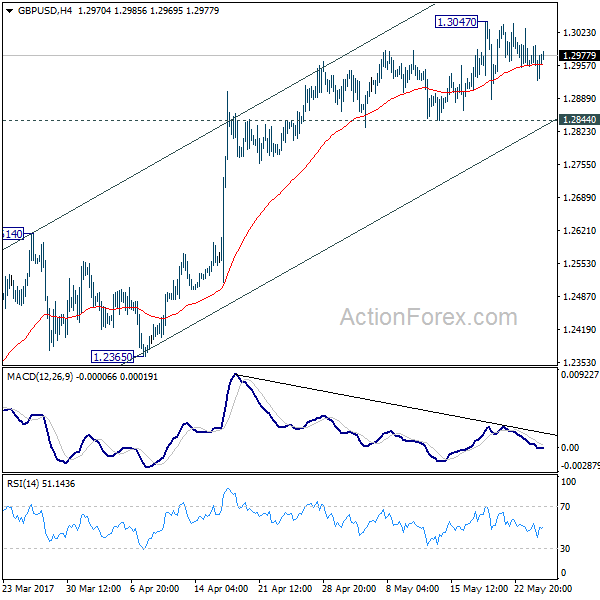

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2934; (P) 1.2967; (R1) 1.3007; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3047 is still in progress. As long as 1.2844 minor support holds, further rise remains mildly in favor. Nonetheless, as we are still viewing price actions from 1.1946 as a corrective move, we'd expect upside to be limited below 1.3444 resistance to bring near term reversal. On the downside, break of 1.2844 will indicate short term topping and turn bias back to the downside for 1.2614 resistance turned support first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There are signs of reversal, like breaking of 55 week EMA, weekly MACD turned positive, and monthly MACD crossed above signal line. But still, break of 1.3444 resistance is need to confirm medium term bottoming. Otherwise, outlook will remains bearish for extend the down trend through 1.1946 low.

U.S. GDP Growth Likely To Remain Under 3% Target Unless Productivity Improves

Key Points:

- U.S. worker productivity continues to decline.

- There are limits to GDP growth through debt.

- 3.00% economic growth unlikely to be reached in the near term.

The current American political cycle could be characterized by its bitter in-fighting and drive towards the partisan side of the fence. In particular, the debate over the U.S. economy appears to be another form of nationalism that both Republicans and Democrats use as a weapon in the war of words over which ideal is best for the economic growth of the nation. However, the truth is that neither party possesses a platform of sincerity and honesty and that without addressing the elephant in the room, productivity, we are unlikely to see a 3% GDP growth rate in anything other than our dreams.

The reality is that the current focus within Washington, as well as financial markets, has largely been centred on hikes to the Federal Funds Rate (FFR), as well as delivering a national budget with plenty of pork for the voters. It appears that both the White House and Congress are hell bent on again resorting to increases in debt to drive a `supposed’ economic recovery and real gains in both jobs and wages. In fact, Trump’s latest budget costing represents a sharp drive to the debt side of the equation and could almost be viewed as the republican version of fiscal stimulus.

However, most economists universally accept that there are limits on how much increased government debt can fuel economic growth, which tends to play into the old adage that there are no free lunches. The reality is that increased monetary and fiscal stimulus has largely failed at producing the sort of GDP gains that the Whitehouse, and the American public, are seeking and that the cost/benefit of the packages are now seriously out of whack. Simply put, eight years of loose monetary policy and QE have had little impact on growth outcomes for America. Subsequently, it makes little sense to undertake the same activities, and expect a different outcome, without addressing the underlying weaknesses.

Most of the economic literature on growth seems to suggest that total factor productivity (TFP) is largely responsible for many of the economic success stories around the globe. In particular, Singapore has experienced huge gains in TFP over the past few decades and, as such, has experienced a wave of economic growth that is admirable. Much of the gains are largely from technological innovation that increases both national and worker productivity and results in a lean and competitive economy in global terms.

However, a cursory review of U.S. Worker Productivity Growth paints a bleak picture as the metric has clearly been within a downtrend over the past 17 years. Although fairly volatile, the indicator clearly demonstrates that the U.S. is losing ground yearly in a global economic battle on productivity and innovation and this certainly doesn’t bode well for GDP gains in the near term

Subsequently, the time might finally have arrived where the political and economic leaders of the U.S. might have to actually address the ongoing slide in domestic worker productivity lest American industries continue to lose their competitiveness in the global market. However, instead of debating the underlying limitation of Keynesian stimulus, or incentivising corporate investment and innovation, Washington instead retreats to political partisanship and ideology.

Largely, the reason for the avoidance of any real debate on the issue is that fact that a technological revolution is coming within the Western world that threatens to cause significant structural unemployment. Machines and technology are poised to revolutionise some sectors and I think many of us can already see the changes with the advent of automatic checkouts at the super market, or online ordering at McDonalds. These innovations are certainly starting to have an impact in the lower skilled worker categories and will continue to do so over the next decade. So now is the time for the U.S. government to start the process of transition in training and upskilling employees to work in different industries with increased worker productivity. However, this requires significant political will and leadership in a time when Washington lacks both.

Ultimately, the reality is that the U.S. is unlikely to see the sort of economic growth they are hoping for whilst there are continuing drags on the domestic economy from poor productivity and increased global trade competition. In addition, a too low for too long monetary policy has reduced the incentive for a drive towards innovation and has, instead, promoted growth through increases in corporate and personal debt. Subsequently, don’t expect the 3.00% growth target to be reached any time soon unless all of these underlying problems are recognised and fixed.

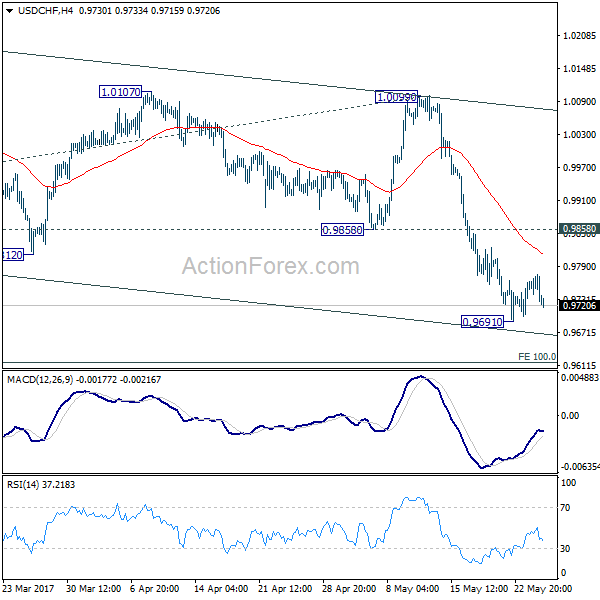

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9713; (P) 0.9745; (R1) 0.9761; More.....

USD/CHF's consolidation from 0.9691 temporary low is still in progress and intraday bias remains neutral. Another recovery cannot be ruled out. But upside should be limited by 0.9858 support turned resistance and bring fall resumption. Whole decline from 1.0342 is still in progress and below 0.9691 will target 100% projection of 1.0342 to 0.9860 from 1.0099 at 0.9617. We'll start to look for reversal signal below there.

In the bigger picture, USD/CHF is bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level.

Loonie Poised To Bounce Back As The Week Closes

Key Points:

- A reversal is looking likely from a technical perspective.

- The bullish trend could extend moving ahead but resistance is in place at 1.3554

- Downside risks mitigated by the 100 day EMA and the medium-term trend line.

The Loonie has been under fire recently but things could be about to improve for the embattled pair in the session to come. Specifically, a number of technical signals are now shifting their bias which suggests a reversal is now on the way. What's more, now that the BoC's interest rate decision is done and dusted, there is little in the way of a rally from a fundamental perspective which should see the technical bias leant on somewhat more heavily moving forward.

Two of the clearest indications that selling pressure may have finally reached an impasse come from the 100 day EMA and the medium-term trend line. Looking first at the moving average, it's fairly plain that dynamic support provided by the 100 day measure is exerting some degree influence on the pair – effectively stalling the prior session's rather voracious plunge lower. As for the trend line, the fact that the pair has respected the line could be a signal that the uptrend is not done just yet and this latest tumble is merely a correction in a longer-term trend.

However, even if this is not the case and we are instead nearing the end of the recent uptrend, we can expect to see at least a little bit of bullishness moving forward. Aside from the factors mentioned above encouraging buying pressure, the movement of stochastics into oversold territory will also be spurring the bulls on. Furthermore, the Loonie is testing the lower boundary of its highly divergent Bollinger bands – a sign that we can expect to see it trend back to the basis line shortly.

In the event that the reversal highlighted above does occur, gains are likely to run into resistance at around the 1.3554 handle. The combination of not only a historical zone of resistance but also the 38.2% Fibonacci level and the basis line of the Bollinger bands around this price should prove more than a match for the bulls who are already on shaky ground. However, there is a slim chance that the overarching bullish trend does continue and trace out a three drive or something similar. This being said, we will need to see the Loonie above the 1.37 handle before we can begin to speculate on such a pattern taking shape.

Ultimately, keep an eye on the pair as, whatever happens, it's likely to be interesting. In particular, monitor the Loonie as it approaches the 1.3554 mark as, if it breaks above this level, it could signal that further gains are on the way. Nevertheless, given that the effects of the ‘Trump Bump' have largely dissipated, it pays to be somewhat pessimistic regarding ongoing USD strength and err on the side of caution

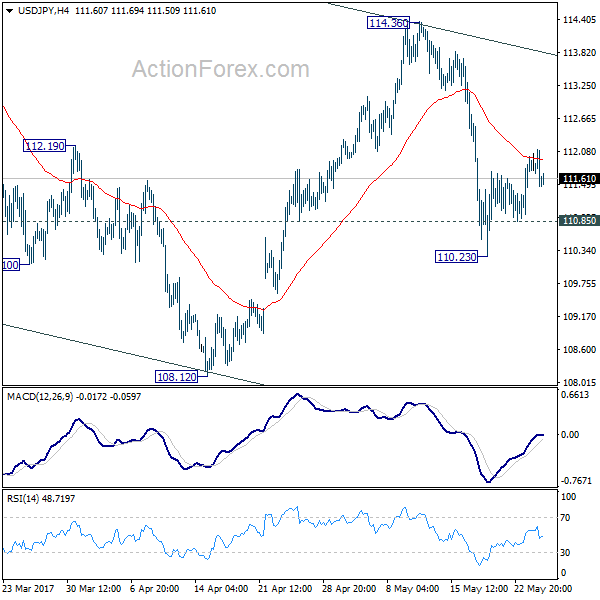

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.26; (P) 111.69; (R1) 111.92; More...

Intraday bias in USD/JPY remains neutral for the moment. The rebound from 110.23 is still seen as a correction even though it might extend. On the downside, below 110.85 minor support will turn bias to the downside to extend the fall from 114.36 to 108.12 low. Break there will resume the whole decline from 118.65. In that case, we'll look for bottoming signal again at 61.8% retracement of 98.97 to 118.65 at 106.48.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

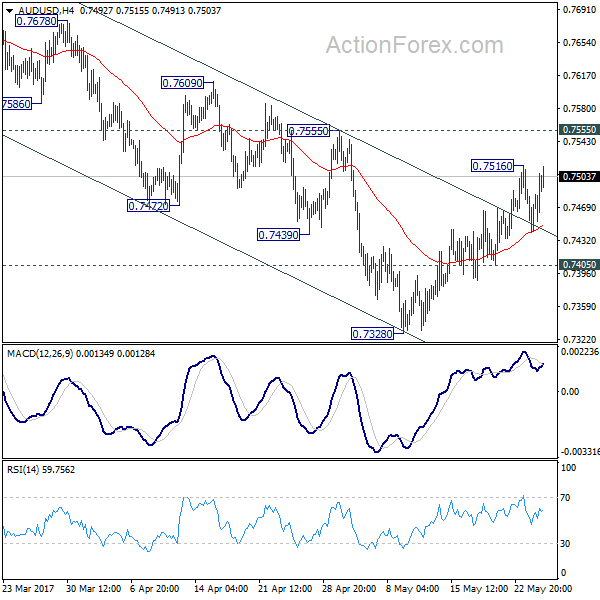

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7461; (P) 0.7484; (R1) 0.7526; More...

Intraday bias in AUD/USD remains neutral for the momentum as it's staying below 0.7516 temporary top. With 0.7555 resistance intact, fall from 0.7748 is still expected to continue. Below 0.7405 minor support will turn bias to the downside for 0.7382. Break there will target 0.7144/7158 support zone. However, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

Market Morning Briefing: Euro (1.1242) Cashed On The Weakness

STOCKS

Dow (21012.42, +0.36%) has moved up in line with our expectation and has entered the near term resistance zone of 21000-21200 and could come off in the near to medium term after some more rise in the next few sessions. A small dip to 20000 is also possible in the near term.

Dax (12642.87, -0.13%) is almost stable and could trade in the 12725-12485 region in the near term. Sideways consolidation is possible before we see a rise towards 12800.

Shanghai (3060.97, -0.10%) is in a down channel and looks bearish on the daily candles but while it trades above important support near 3020 (visible on the 3-day and weekly candles), we could see an attempt to bounce back towards 3090-3100 in the coming sessions.

Nikkei (19849.10, +0.54%) has moved up and is headed towards resistance at 20000. While Dollar-Yen and the US-Japan 10Yr yield spread are moving up, we could expect an upmove in Nikkei too in the near term. Immediate resistance at 20000 is expected to hold just now.

Nifty (9360.55, -0.27%) closed almost closer to our immediate support levels near 9350. In case 9350 breaks on the downside, we could see a fall towards 9250-9200 in the medium term.

COMMODITIES

While Dollar Index had failed to hold it’s gain above 97 levels, Bullion has strengthened again against Dollar yesterday. Gold (1257) and Silver (17.19) are trading well above their crucial support at 1247 and 16.93 respectively. But we would like to be on selling side while gold is trading below 1280 and silver below 17.50 levels due to their short term overbought condition.

Copper (2.58) has found resistance at 2.62 levels. Only above 2.62, higher resistances of 2.68-72 can come into consideration. In the medium term 2.55 are going to be a strong support now but a close below that could open up 2.44-35 levels as well.

Brent (54.50) moved higher and hovering around its crucial resistance of 54.60 which is a significant move for the energy markets. WTI (51.82) is also trading above its major resistance of 51.20. Both of them have tested and bounced a bit from their respective support areas due to a huge decrease (-4.4 MB) in U.S weekly crude oil inventory. Immediate trading range for Brent and WTI could be 53-54.60 and 50.50-52.40 respectively. The only concern is the short term overbought condition though the downside possibly limited to 51.80 for Brent and 49.30 for WTI.

FOREX

Dollar Index (96.94) was rejected exactly from our resistance of 97.45, increasing the chances of seeing 96.50-00 in the next few sessions. 97.45 becomes a significant resistance and near term reversal point, below which the bears remain in total control.

Euro (1.1242) cashed on the weakness of Dollar as it bounced back from the previous swing low of 1.1160. The journey towards the target/resistance of 113.00 may have resumed. Repeat - if any profit booking is seen in Euro either near 1.1300-30 or near the higher long term resistance of 1.1400-50, then corresponding short covering can be expected in Dollar near 96.50 or 96.00.

Dollar Yen (111.53), unable to sustain above the resistance of 112, returned inside the range of 110-112 and may continue moving sideways in the broader range of 111.50-114.00 with no strong directional intent.

While the chances of a sudden sharp rise towards 1.32 can’t be ruled out yet, at the moment Pound (1.2983) is showing a lot of inertia as it continues to grind in the range of 1.2900-1.3100. No weakness as such above 1.2900.

Aussie (0.7509) bounced almost exactly from our support of 0.7430 but not higher than 0.7550 is expected right now. Some selling pressure can be expected from 0.7540-50.

Dollar Rupee (64.74) came down from 64.95, well short of our expected higher target/resistance of 65.10-25. Still no clarity as bidirectional possibilities prevails. From a larger perspective, it must also be noted that the bearish momentum of the major downtrend remains intact below 65.25.

INTEREST RATES

The US yields came off slightly yesterday but overall looks bullish in the near term while immediate supports hold. The 10-5Yr differential (0.47%) has moved up sharply and could head towards 0.475%-0.50% in the near term indicating that the 10Yr could rise faster than the 5Yr in the next few sessions.

The Japan-US (2.21%) looks bearish in the medium term charts and in case it moves down towards 2.1-2.0%, we could see some downward correction in Nikkei and Dollar Yen too. This could be in line with the resistance near 20000 on Nikkei.

The Japanese yields look bullish in the near term. the 10YR (0.05%) and the 30Yr (0.81%) may head towards 0.1% and 0.84% respectively.

The UK yields are falling and may test support levels in the near term. The 10Yr (1.07%) could bounce back from 1% while the 20Yr (1.61%) may head lower towards 1.5%.

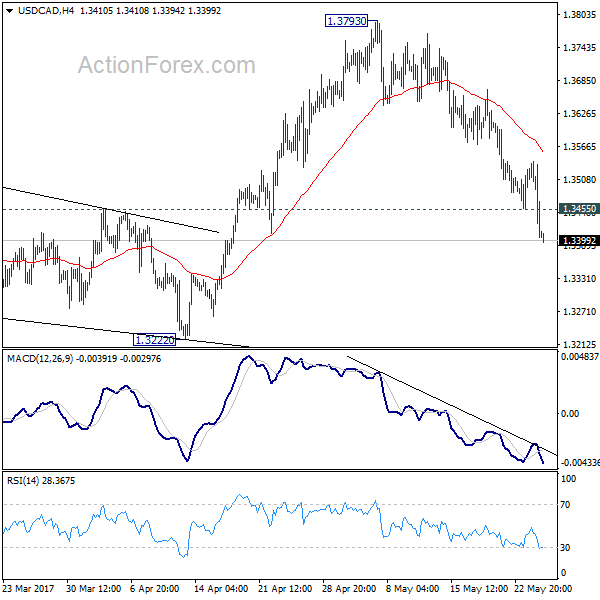

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3361; (P) 1.3450; (R1) 1.3495; More....

USD/CAD's decline continues today and reaches as low as 1.3394 so far today. Intraday bias remains on the downside as the fall from 1.3793 is targeting 1.3222 support next. As noted before, corrective rally from 1.2460 could have finished ahead of 1.3838 fibonacci level. Break of 1.3222 will affirm this case and target 1.2968 key support level for confirmation. On the upside, above 1.3455 minor resistance will turn bias neutral and bring another recovery first.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.