Sample Category Title

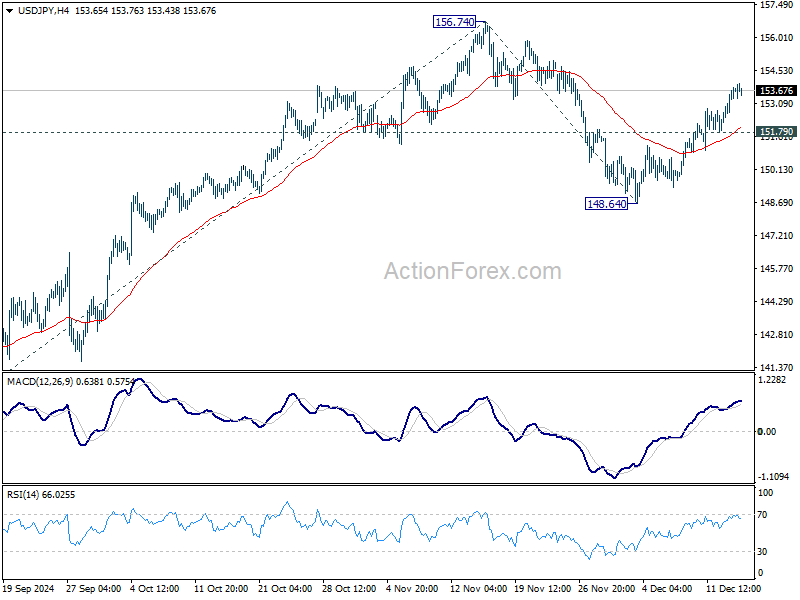

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.80; (P) 153.30; (R1) 154.14; More...

USD/JPY's rebound from 148.64 is in progress and intraday bias stays on the upside for retesting 156.74. Firm break there will resume whole rally from 139.57, and target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 151.79 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 148.64 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

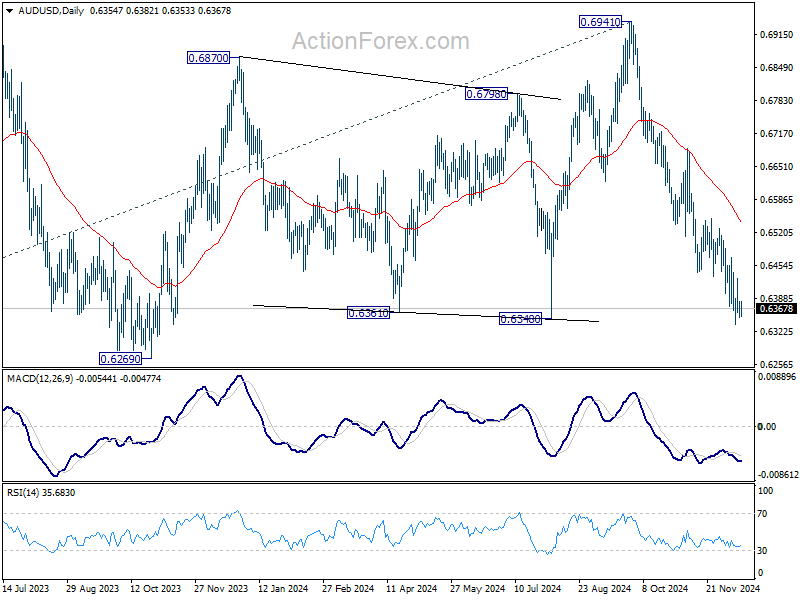

AUD/USD Daily Report

Daily Pivots: (S1) 0.6347; (P) 0.6366; (R1) 0.6380; More...

AUD/USD is staying in consolidation above 0.6336 and intraday bias remains neutral. More consolidations would be seen and another recovery cannot be ruled out. But outlook will stay bearish as long as 55 D EMA (now at 0.6540) holds. Below 0.6336 will resume the fall from 0.6941 to 0.6269 support next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

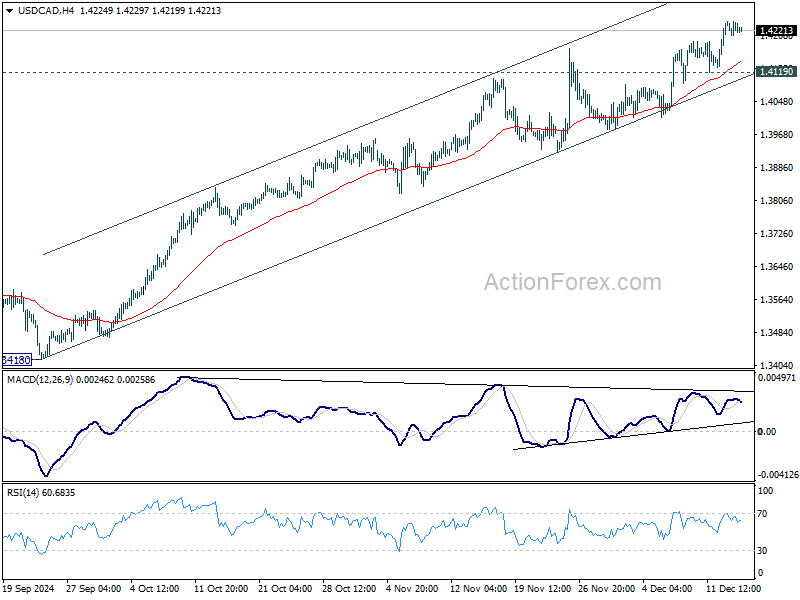

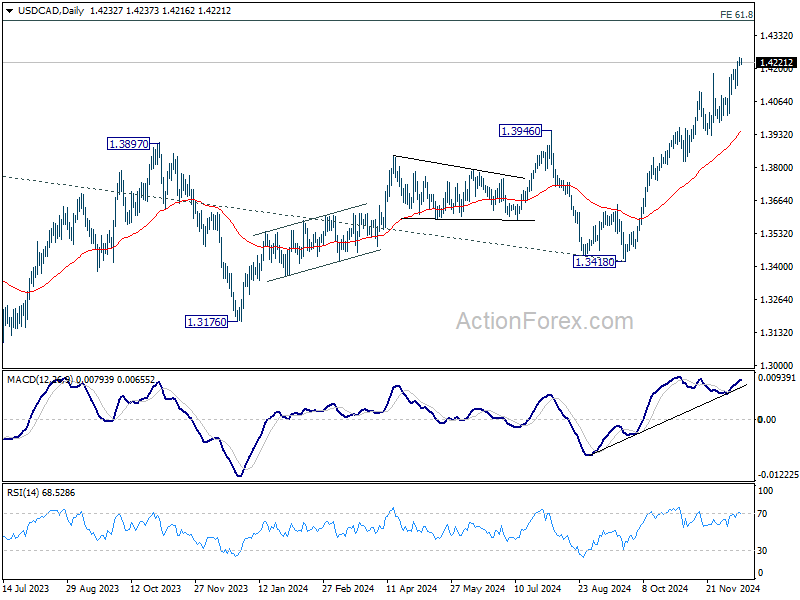

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4210; (P) 1.4228; (R1) 1.4252; More...

Intraday bias in USD/CAD stays on the upside for the moment. Current rally is part of the larger up trend and should target 1.4391 projection level next. Considering bearish divergence condition in 4H MACD, break of 1.4119 support will indicate short term topping and bring deeper correction.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.

Markets Start With Mild Risk-Off Mood, Central Bank Bonanza Continues

The forex market began the week on a subdued note, with mild risk-off sentiment setting the tone. China's latest economic data painted a bleak picture, with retail sales significantly underperforming expectations and fixed asset investment experiencing a deeper decline. While industrial production growth met forecasts, it failed to offset concerns about the broader economic slowdown. The lack of impactful measures from the Chinese government continues to weigh on market confidence. Despite repeated pledges for stronger economic support, tangible actions remain elusive, leaving businesses, consumers, and markets uncertain about the path forward.

In Europe, Euro is under pressure following Moody's downgrade of France's sovereign credit rating from Aa2 to Aa3, now with a stable outlook. The downgrade highlights concerns over France's fiscal trajectory, with Moody's projecting materially weaker public finances over the next three years compared to previous forecasts. This development comes as President Emmanuel Macron appointed centrist François Bayrou as Prime Minister in a bid to stabilize the political climate amid mounting economic challenges. However, Moody’s noted the “very low probability” of substantial fiscal consolidation under the new government, further clouding France’s outlook.

Looking ahead, the focus shifts to three major central bank meetings this week: Fed, BoE and BOJ. Fed’s decision holds the greatest significance as markets seek clarity on the trajectory of rate cuts in 2025 amid persistent inflationary pressures. In addition to central bank meetings, key data releases, including inflation figures, retail sales, and economic sentiment surveys, will be closely watched too.

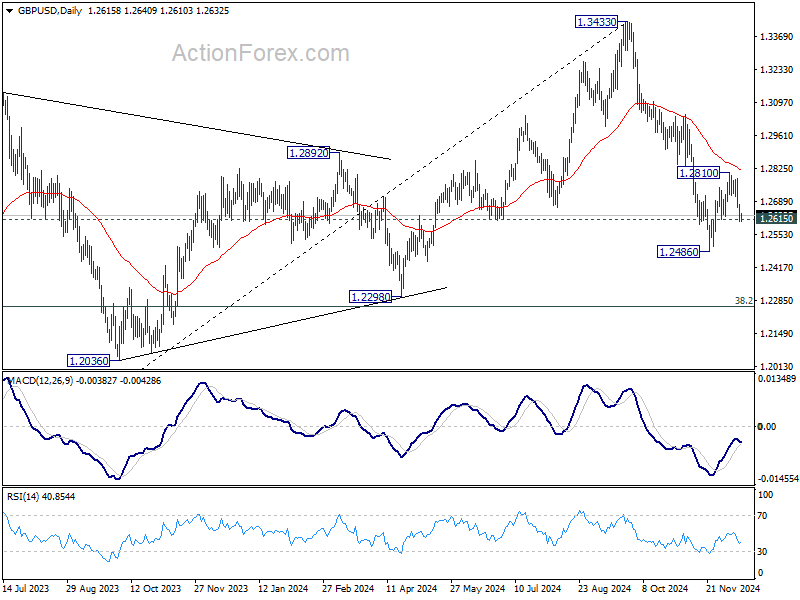

Technically, GBP/USD's corrective recovery from 1.2486 looks completed at 1.2810 already, after be capped below 55 D EMA. An imminent focus is when GBP/USD would break through 12615 minor support to solidify this bearish case. Then, further fall should be seen through 1.2486 to resume the whole decline from 1.3433 to 1.2298 key structural support next.

Japan's PMI composite rises to 50.8, stubborn inflation caps growth

Japan’s private sector activity showed a modest improvement in December, driven by a stronger services sector, while manufacturing continued to contract.

PMI Manufacturing index declined from 49.5 to 49.0, marking the fourth consecutive month of contraction. In contrast, PMI Services index rose from 50.5 to 51.4, lifting Composite PMI from 50.1 to 50.8, indicating mild overall growth.

Usamah Bhatti, economist at S&P Global Market Intelligence, pointed out the contrasting trends: “Services firms saw the strongest rise in new business in four months, while goods producers faced a sharper decline in orders.” This divergence highlights persistent weakness in manufacturing amid subdued demand and improving momentum in the services sector.

Inflationary pressures persisted, fueled by the Yen’s weakness, which increased the cost of imported materials. Input prices rose at the fastest pace in four months, while selling price inflation hit its highest level since May, as businesses passed on rising costs to consumers. Bhatti noted, “Stubborn inflation held back a stronger expansion of the Japanese private sector in December.”

Australian PMI composite falls to 49.9, bolsters case for early RBA rate cut

Australia's December PMI data pointing to a broad-based slowdown. The Manufacturing index fell from 49.4 to 48.2. Services PMI edged down from 50.5 to 50.3. Meanwhile, Composite PMI dropped from 50.2 to 49.9, slipping into mild contraction territory.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, noted that the data reflects growing strain across sectors, with manufacturing leading the downturn and services beginning to falter.

Forward indicators presented mixed signals. While business confidence reached its highest level in over two-and-a-half years, new business growth slowed, and unfinished work declined further. Employment gauge showed its first contraction since August 2021.

Muted selling price inflation provides room for RBA to consider rate cuts in early 2024. However, rising cost pressures remain a concern.

NZ BNZ services jumps to 49.5, closer to stability

New Zealand’s BusinessNZ Performance of Services Index rose significantly from 46.2 to 49.5 in November, signaling a move closer to stabilization. However, the index remains under the no-change threshold of 50.0 and well below its long-term average of 53.1.

Key subcomponents offered a mixed picture. Activity/sales improved from 44.4 to 48.6, and new orders/business rose to 49.8, nearing expansion territory. Employment showed only a slight uptick, from 46.4 to 46.8, reflecting continued caution among firms. Stocks/inventories and supplier deliveries moved into expansionary territory at 52.2 and 52.5, respectively, signaling some recovery in supply chain dynamics.

Negative sentiment among respondents eased, with the proportion of unfavorable comments dropping to 53.6% from October’s 59.1%. However, the ongoing concerns over the economic climate and the cost of living remain dominant themes, indicating persistent headwinds for the sector.

Fed’s hawkish cut and signals for 2025, as central bank bonanza continues

Another important week lies ahead for global financial markets, with three major central bank meetings, and economic data converging to shape sentiment. Fed, BoE, and BoJ are set to reveal their latest policy decision. At the same time, a slate of inflation, consumption, and survey data will offer fresh insights into growth and price pressures.

FOMC’s decision tops the agenda. Markets are fully braced for a 25bps rate cut, bringing the federal funds target range down to 4.25–4.50%. With futures assigning over 95% odds of such an outcome, any deviation seems highly unlikely. Yet there are two crucial questions concern Fed’s forward guidance.

First, will policymakers hint at a pause in January, given that the economy remains robust and labor market risks have receded, while inflation remains sticky? Market probability for a pause next month stands at over 80%, so any confirmation or denial in the FOMC statement or Chair Jerome Powell’s press conference will resonate strongly.

Second, the pace of policy easing in 2025 is under the microscope. Fed fund futures suggest around 33% chance of just two more 25bps cuts next year, below the Fed’s September median projection of 3.4%. The updated dot plot and new economic projections will be parsed closely for alignment with market assumptions, as investors seek clarity on how lingering inflation and incoming administration’s fiscal and trade policies might influence Fed’s approach.

Meanwhile, BoE and BoJ are also in the spotlight. BoE is widely expected to keep rates unchanged, with the outlook for four measured rate cuts next year still holding. This meeting may offer little fresh guidance, leaving traders to wait for the February monetary policy summary.

In Japan, BoJ looks increasingly leaning toward maintaining the status quo in the past two weeks, given the lack of urgency to tighten further before its January economic forecasts. While officials consider patience to be a virtue, the BoJ’s track record of unexpected moves means a surprise cannot be fully dismissed.

Beyond central banks, economic data will help define the contours of market sentiment. Investors will scrutinize US PCE inflation, CPI reports from the UK, Canada, and Japan, as well as retail sales data from the UK and Canada.

Additionally, PMIs from major economies will be closely watched. In particular, Eurozone PMIs, Germany’s Ifo and ZEW surveys will test whether Europe’s growth slowdown is stabilizing or deepening. In Asia Pacific, New Zealand’s GDP figures and a batch of Chinese indicators will contribute to the evolving narrative on trade and regional demand.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Australia PMIs; Japan machine orders, PMIs, tertiary industry index; China industrial production , retail sales, fixed asset investment; Swiss PI; Eurozone PMIs; UK PMIs; Canada housing starts; US Empire state manufacturing, PMIs.

- Tuesday: Australia Westpac consumer sentiment UK employment; Swiss SECO economic forecasts; Germany Ifo business climate, ZEW economic sentiment; Eurozone trade balance; Canada CPI; US retail sales, industrial production, business inventories, NAHB housing market index.

- Wednesday: Japan trade balance; UK CPI, PPI; Eurozone CPI core; US building permits and housing starts, current account, FOMC rate decision.

- Thursday: New Zealand GDP, ANZ business confidence; BoJ rate decision; BoE rate decision; US GDP final, jobless claims, Philly Fed survey, existing home sales.

- Friday: New Zealand trade balance; Germany PPI; UK retail sales; Canada retail sales; US personal income and spending, PCE inflation.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4210; (P) 1.4228; (R1) 1.4252; More...

Intraday bias in USD/CAD stays on the upside for the moment. Current rally is part of the larger up trend and should target 1.4391 projection level next. Considering bearish divergence condition in 4H MACD, break of 1.4119 support will indicate short term topping and bring deeper correction.

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.

Asian Markets Mostly Trade in Negative Territory

Markets

German and EMU yields on Friday initially only showed minor gains, but finally extended the rebound that gradually developed earlier last week. US yields added 5.4 bps (2-y) to 6.9 bps (10-y). There were no important US data, but markets apparently are pondering whether recent solid US activity data, slightly higher inflation and uncertainty on the inflationary impact of future (fiscal) policy, might cause the Fed to turn more conditional on the pace and timing of additional cuts. The new (most likely upwardly revised) dot plot will be instructive on the MPC policy assessment going forward. German yields continued the ‘technical’ post-ECB rebound, rising about 5 bps across the curve; the very long end slightly outperforming (30-y +3.4bps). First post-meeting comments from ECB policy makers showed the usual divide between ‘hawks’ and ‘doves’. However, for now gradualism is the greatest common denominator. Despite a congruent interest rate move between the US and EMU, EUR/USD tried to leave recent lows, but the move lacked conviction (close 1.0501 from 1.0468). Sterling underperformed both the dollar and the euro after disappointing UK October production data and a negative monthly GDP reading (-0.1% M/M for the second consecutive month).Earlier last week, it looked like EUR/GBP was heading for a test of the key 0.8203 2022 low. On Friday, the pair closed north of 0.83(22). The technical picture remains fragile, but there is some breathing space. Equities in Europe and the US closed little changed.

Asian markets mostly trade in negative territory after China reported weak November retail sales (3% Y/Y vs 5% expected), indicating ongoing weak demand growth despite recent stimulus efforts. US yields decline marginally as does the dollar (DXY 106.85, EUR/USD 1.053). Later today, the focus will be on the EMU preliminary PMI’s. Given ongoing political uncertainty in France and Germany and persistent negative headlines on all kinds of economic topics, it’s probably too early to see any sustained improvement yet (consensus sees 49.5 unchanged composite PMI). Weak data might already cap any further rise in short-term EMU yields. 2.20%/2.25 % might provide resistance for the 2-y swap short-term. The picture at the longer and of the curve is more balanced. For the US, we look out whether the services PMI confirms the decline in the services ISM. There are often discrepancies between the two indicators. For the euro (EUR/USD), the EMU data might be the dominant factor short-term. First ST resistance at 1.063 is far away. After Friday’s poor UK data, sterling might become more sensitive to additional negative news (consensus expects composite PMI at 50.6 from 50.5).

News & Views

Rating agency Moody’s downgraded both France (Aa2 to Aa3, stable outlook) and Slovakia (A2 to A3, stable outlook) after Friday’s market close. The decision to downgrade France reflects the view that the country's public finances will be substantially weakened over the coming years because political fragmentation is more likely to impede meaningful fiscal consolidation. A negative feedback loop between higher deficits, a higher debt load and higher financing costs, against the backdrop of significant annual borrowing needs, could be the unwanted outcome. Moody’s expect the deficit to stand at 6.3% of GDP in 2025, before gradually decreasing to around 5.2% in 2027. Debt-to-GDP would increase from 113.3% in 2024 to around 120% in 2027. The decision to downgrade Slovakia's ratings reflects the country's broad institutional challenges amid political tensions. A comprehensive reform programme on the judiciary and the media will weaken the country's checks and balances, amplifying a deteriorating trend already captured in governance indicators. At the same time, increased political fragmentation challenges policymaking in particular on the fiscal front.

The German CDU’s election manifesto will be formally unveiled tomorrow, but the Financial Times in an article comments on a draft it has seen from the poll-leading Christian Democrats. The want to run amongst others on a platform of tougher immigration – “we must decide ourselves once again who comes to us and who can stay” – and an agenda for hard-workers. Proposals include cuts to income tax for people on low- and middle-incomes, a reduction in social security contributions, a gradual decline in corporate taxation from about 30% now to 25% and abolishing the “Soli” surcharge on income tax that was introduced to pay for German reunification. It’s unclear how they would fund these rebates with the CDU staying committed to the debt brake. “The debts of today are the taxes of tomorrow.”

Japan’s PMI composite rises to 50.8, stubborn inflation caps growth

Japan’s private sector activity showed a modest improvement in December, driven by a stronger services sector, while manufacturing continued to contract.

PMI Manufacturing index declined from 49.5 to 49.0, marking the fourth consecutive month of contraction. In contrast, PMI Services index rose from 50.5 to 51.4, lifting Composite PMI from 50.1 to 50.8, indicating mild overall growth.

Usamah Bhatti, economist at S&P Global Market Intelligence, pointed out the contrasting trends: “Services firms saw the strongest rise in new business in four months, while goods producers faced a sharper decline in orders.” This divergence highlights persistent weakness in manufacturing amid subdued demand and improving momentum in the services sector.

Inflationary pressures persisted, fueled by the Yen’s weakness, which increased the cost of imported materials. Input prices rose at the fastest pace in four months, while selling price inflation hit its highest level since May, as businesses passed on rising costs to consumers. Bhatti noted, “Stubborn inflation held back a stronger expansion of the Japanese private sector in December.”

Australian PMI composite falls to 49.9, bolsters case for early RBA rate cut

Australia's December PMI data pointing to a broad-based slowdown. The Manufacturing index fell from 49.4 to 48.2. Services PMI edged down from 50.5 to 50.3. Meanwhile, Composite PMI dropped from 50.2 to 49.9, slipping into mild contraction territory.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, noted that the data reflects growing strain across sectors, with manufacturing leading the downturn and services beginning to falter.

Forward indicators presented mixed signals. While business confidence reached its highest level in over two-and-a-half years, new business growth slowed, and unfinished work declined further. Employment gauge showed its first contraction since August 2021.

Muted selling price inflation provides room for RBA to consider rate cuts in early 2024. However, rising cost pressures remain a concern.

NZ BNZ services jumps to 49.5, closer to stability

New Zealand’s BusinessNZ Performance of Services Index rose significantly from 46.2 to 49.5 in November, signaling a move closer to stabilization. However, the index remains under the no-change threshold of 50.0 and well below its long-term average of 53.1.

Key subcomponents offered a mixed picture. Activity/sales improved from 44.4 to 48.6, and new orders/business rose to 49.8, nearing expansion territory. Employment showed only a slight uptick, from 46.4 to 46.8, reflecting continued caution among firms. Stocks/inventories and supplier deliveries moved into expansionary territory at 52.2 and 52.5, respectively, signaling some recovery in supply chain dynamics.

Negative sentiment among respondents eased, with the proportion of unfavorable comments dropping to 53.6% from October’s 59.1%. However, the ongoing concerns over the economic climate and the cost of living remain dominant themes, indicating persistent headwinds for the sector.

GBP/USD Faces Trouble, USD/CAD Builds on Gains

GBP/USD started a fresh decline below the 1.2720 zone. USD/CAD is rising and might aim for more gains above the 1.4245 resistance.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started another decline from the 1.2800 resistance zone.

- There is a short-term declining channel forming with resistance at 1.2650 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD is showing positive signs above the 1.4200 support zone.

- There is a contracting triangle forming with resistance at 1.4245 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair struggled to continue higher above the 1.2840 resistance zone. The British Pound started a fresh decline and traded below the 1.2750 support zone against the US Dollar, as discussed in the previous analysis.

The pair even traded below 1.2650 and the 50-hour simple moving average. Finally, the bulls appeared near the 1.2610 level. A low was formed at 1.2608 and the pair is now consolidating losses.

Immediate resistance on the upside is near a short-term declining channel at 1.2650. It is close to the 23.6% Fib retracement level of the downward move from the 1.2787 swing high to the 1.2608 low. The first major resistance is near the 1.2674 zone.

The main hurdle sits at 1.2720 and the 61.8% Fib retracement level of the downward move from the 1.2787 swing high to the 1.2608 low. A close above the 1.2720 resistance might spark a steady upward move.

The next major resistance is near the 1.2785 zone. Any more gains could lead the pair toward the 1.2850 resistance in the near term.

Initial support on the GBP/USD chart sits at 1.2610. The next major support sits at 1.2585, below which there is a risk of another sharp decline. In the stated case, the pair could drop toward 1.2520.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair formed a strong support base above the 1.4100 level. The US Dollar started a fresh increase above the 1.4165 resistance against the Canadian Dollar.

The bulls pushed the pair above the 1.4200 and 1.4215 levels. The pair cleared the 50-hour simple moving average and climbed above 1.4240. A high was formed at 1.4245 and the pair recently corrected some gains.

There was a move toward the 23.6% Fib retracement level of the upward move from the 1.4119 swing low to the 1.4245 high. Initial support is near the 1.4215 level.

The next major support is near the 1.4195 level. The main support sits near the 1.4165 zone on the same USD/CAD chart. It is close to the 61.8% Fib retracement level of the upward move from the 1.4119 swing low to the 1.4245 high.

A downside break below the 1.4165 level could push the pair further lower. The next major support is near the 1.4120 support zone, below which the pair might visit 1.4050.

If there is another increase, the pair might face resistance near the 1.4245 level. A clear upside break above 1.4245 could start another steady increase. The next major resistance is the 1.4320 level.

A close above the 1.4320 level might send the pair toward the 1.4365 level. Any more gains could open the doors for a test of the 1.4420 level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

France Downgraded

China’s latest efforts to convince investors that it will boost its economy with great stimulus measures had the same reaction than the previous ones: disappointment. On Friday, the Chinese authorities repeated that they will boost consumption but the lack of details reversed the pre-announcement enthusiasm and sent the CSI 300 more than 2% lower. And the Chinese stocks were sold again today on the back of a significant slow down in retail sales growth last month, as confirmation that whatever is done in China is not bearing fruit. Meanwhile, the Chine yields’ nosedive does nothing to motivate investors to come back. That’s a massive problem that reminds investors of Japan which struggled with the famous ‘liquidity trap’ dilemma for decades – where the low rates couldn’t boost consumption and kept the economy in a low gear for decades. The only thing that could make the difference for China is that Japan was already rich when liquidity trap happened, China is not.

In Korea, the political turmoil continues to weigh on sentiment, while in France, the relief on the appointment of Francois Bayrou – another very established name in French politics – to replace Barnier as the new French PM was clouded by Moody’s downgrading the French credit rating to Aa3 – three levels below the top. Moody’s blamed the political fragmentation, and Bayrou will probably struggle with the same divided government as his predecessor to pass any budget-healing measures.

Nearby, German politicians will hold a confidence vote to pave the way for a Ferbuary snap election. But the German opposition said that they will maintain their borrowing limit unchanged if they come to power next year – as opposed to the earlier statements from the CDU leader Friedrich Merz about his openness to increase that limit to give more support to the economy – which obviously was not ideal for the budget discipline.

To summarize, nothing is less clear than the political picture in the eurozone’s two strongest economies, so the bets that the European Central Bank (ECB) must do the heavy lifting remains strong after last week’s cautious 25bp cut. The expectation is that the ECB will deliver another 25bp cut in January. But the dovishness is mostly priced in, therefore, the EURUSD should find enough support near the 1.05 mark and re-challenge the 1.06 offers.

Across the Channel, Cable is slightly better bid this morning, but Friday’s disappointing set of data – that hinted at surprisingly worse industrial and manufacturing production topped with surprisingly soft services – warned again that the British economy will see the backdrops of tax increases before it starts seeing the benefits of spending. The Bank of England (BoE) is expected to maintain its rate unchanged this week, to make sure to balance out the government’s spending plans, but some officials could sound dovish on the back of weak growth numbers. As per sterling, the selloff could slow on the back of a cautious BoE and an unnecessarily soft Federal Reserve (Fed). But the dream of seeing Cable end the year above the 1.30 is melting by the day.

In Japan, the USDJPY is gaining traction to the upside as investors trim their bets for a Bank of Japan (BoJ) rate hike this week. Some officials had said earlier this month that waiting for the next hike would make little sense – a hawkish risk that should cap the USDJPY’s ascent near 155 into the decision.

In the US, the Federal Reserve (Fed) is expected to trim its rates by another 25bp when it meets this week. Last week’s CPI print was eventless, and the jump in the PPI number was mostly wiped out – as egg prices were mostly responsible for the uptick. What the Fed will announce about the next meetings will probably matter more than this week’s cut. On one hand, Powell recognizes that the US economy and jobs market remain resilient. On the other hand, Trump’s pro-growth policies and tariffs could boost inflation again. So, on both hands, there is nothing that justifies the continuation of regular cuts in 2025.

The S&P500 closed last week near record while Nasdaq advanced to a fresh record high on Friday. This time, it was Broadcom’s turn to shine. The company’s stock price jumped 24% to a record high on Friday after announcing better-than-expected earnings and saying that it expects a booming demand for their custom-made AI chips. Remember, Broadcom and Apple announced to build a chip together a day before. Tech companies’ willingness to build their own chips could be a opening for companies like Broadcom in the AI race – if they succeed in delivering strong, custom-made and cheaper solutions and threaten Nvidia’s share of pie. Nvidia’s ecosystem of software, tools, and AI research infrastructure remains a powerful defense, but its high valuation raises questions.